A week and a half ago, the Chicago Cubs trailed by three games to one in the best-of-seven World Series. Even those who don’t follow baseball were aware that the Cubs had not won a championship in more than 100 years. That streak of futility seemed likely to continue.

At that point, Nate Silver’s statistical website (fivethirtyeight.com) posted the observation that the Cubs’ odds of winning were comparable to those faced by Donald Trump. When the Cubs recovered to take the crown, I began to wonder if Mr. Trump would also defy expectations and win the U.S. election. With that outcome now in hand, our attention turns to lessons learned and what might lie ahead.

A mistake many in my profession have made in the past year has been underestimating the difference between overall economic performance and its translation to the fortunes of constituents. This was at the heart of the Brexit vote last June and was the driving force behind yesterday’s U.S. outcome.

We’ve had a seven-year economic expansion, the Standard and Poor’s 500 Index is 200% higher than it was in the spring of 2009 and unemployment is around 5%. In light of the headwinds posed by the post-crisis era (deleveraging, advancing regulation, financial stability), this seems like an excellent performance, at least to me.

But looking beneath the surface, there are many who do not share this opinion. As we wrote last week, the labor force has two faces.

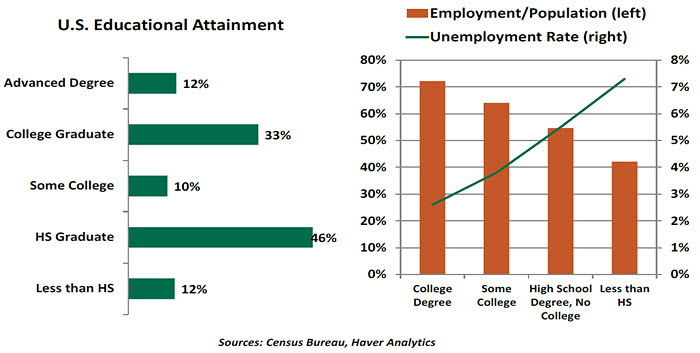

Many have endured both secular and cyclical challenges in finding and keeping work. Those with more modest levels of education are more likely to be unemployed or underemployed and less likely to be participating in the labor force. This group is less likely to have a stock portfolio, so its members have not shared in the market’s gains. And they are more likely to have a home worth less than the outstanding mortgage.

Many of us here, and many of our readers, are college-educated. We spend the lion’s share of our time in the company of others like ourselves. We indulge in research, theory and policy discussions that often review issues at a high level.

Yet college graduates make up only a third of the American population. While we attempt to cover the full economic waterfront effectively through our study, we are not in close touch with the grass roots. Those communities are skeptical about us and our methods of economic study. Studies illustrating the benefits of trade and immigration do not reconcile with visceral feelings on those topics. As Michael Gove, a Brexit supporter, famously said, people “have had quite enough of experts.”

As a result, pundits and pollsters missed the U.S. election results, as they missed the Brexit outcome. The discontent was acknowledged, but it was expected to disappear within the enclosure of the voting booth. Instead, it found its full expression at the ballot box.

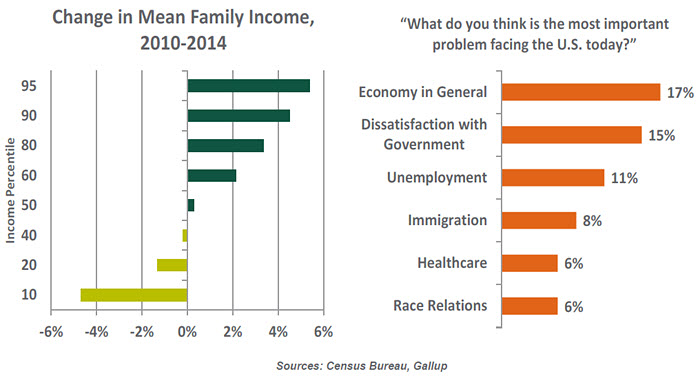

I’ve often been asked whether there is a link between levels of income inequality and economic performance. The studies I’ve read suggest that there isn’t one. But unequal societies can become politically volatile if citizens lose faith in the system. We’ve apparently reached that point in the United States and the United Kingdom, and potentially elsewhere, as we discussed in our narrative on the

roots of populism.

What lies ahead? In these early days after the outcome, the ratio of speculation to understanding is high. Here are some preliminary insights:

- The Republican Party holds the White House and both houses of Congress. But there are important divides within the Party that will need to be ameliorated. Key members of Congress distanced themselves from President-elect Trump during the campaign; they’ll now have to find common ground.

Factions within the party were divided prior to the election, and remain so. This will make for an interesting race for Speaker of the House of Representatives. Paul Ryan, who took the job somewhat reluctantly a year ago, may have difficulty holding on to it. Appointments to key cabinet posts will also be critical to the collaboration. The Secretaries of Treasury, State and Defense, along with the Attorney General, will have a significant role in setting policy.

All of this is to note that the President-elect’s campaign proposals will not necessarily sail through the legislative process unaltered.

- U.S. fiscal policy is poised to become more stimulative. Mr. Trump, advised by some of the original supply-side thinkers, proposed immense tax cuts from the campaign trail. While Congress may not agree to all the elements he wants, it will likely lean in a similar direction. As we wrote in our piece “A Taxing Campaign,” movement on the corporate income tax code and policy to address the mountain of profits currently held overseas will be a first order of business.

Infrastructure spending, which has become a global mantra, is likely to increase. All of this should be positive for U.S. economic growth. But there are questions about what it means for debt and deficits. Economic scoring was not kind to the Trump plan, projecting significantly higher deficits if the outline is adopted as offered. Inflation could be heading northward.

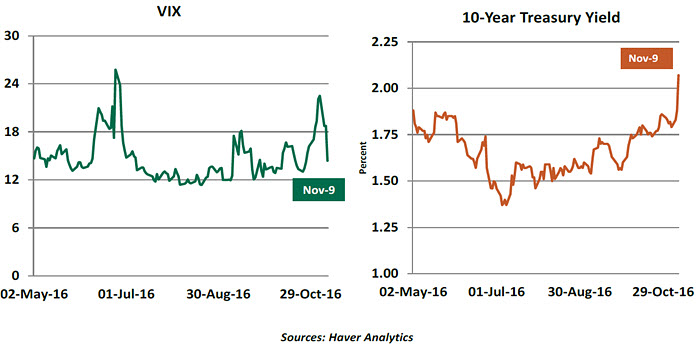

Reacting to this possibility, market interest rates have continued a climb, initiated last month, that has brought the yield on the 10-year U.S. Treasury above 2% for the first time since the early weeks of 2016. Keeping deficits in reasonable check will require some craft; Congress may rekindle offset requirements for new initiatives, like the pay-as-you go system that has been used twice in the last 25 years.

- The election will have short- and long-term impacts on the Federal Reserve. There is still a month to go before the next Federal Open Market Committee meeting, which provides plenty of time for the post-election volatility to dissipate. Market-implied odds of a December interest rate increase were essentially unmoved by the balloting, remaining at about 78%.

But the election could produce more lasting consequences for the Fed’s structure and independence. Proposals to audit the conduct of monetary policy might certainly gain steam. This would threaten the independence of monetary policy, which has been a tenet of central banking during the past 40 years. On the surface, some of the new president’s fiscal ideas could create higher levels of inflation; markets would certainly be most comfortable if the Federal Reserve were in a position to lean against any excesses.

There will also be many opportunities for the new administration to place its stamp on the Federal Reserve Board. At one point during the campaign, Trump promised to fire Janet Yellen. That won’t be immediately possible; her term as chairman runs through February 2018. But there are two spots currently open on the Board, nominees for which have been languishing without hearings. New appointments might be confirmed sometime early in 2017 and bring a somewhat more hawkish tone to the debate.

- European political establishments must be terribly unnerved. They will be attempting diplomacy with an American president who has very limited experience in the area and who has expressed admiration for Vladimir Putin. Traditional parties will be challenged to build a kind of firewall against the spreading populism. The referendum in Italy (December 2016), and upcoming elections in the Netherlands (March 2017), France (April 2017), and Germany (fall 2017) could add to the challenge of maintaining global ties.

- All of the time and political capital spent on the Trans-Pacific Partnership and the Transatlantic Trade and Investment Partnership will have to be written off. Proponents of the arrangements may have the misfortune of bad timing, but trade advocates everywhere have done a poor job of explaining how their efforts accrue to the common good.

Trade policy will be an important point of reconciliation between the president-elect and Congress. The latter has traditionally been supportive of free trade, but the electorate has spoken clearly, and negatively, on the topic. Mr. Trump suggested on the campaign trail that he might abandon the North American Free Trade Agreement, and he may be able to take this step without the approval of Congress. But it is more likely that the administration will pursue negotiated modifications.

The U.S. orientation towards China should be handled with care. China was fingered as an unfair trader during the campaign and pledges were made to bring jobs lost to Asia back to the United States. But again, sudden movements might be very counterproductive, given the somewhat fragile state of China’s economy as it works through industrial transition amid high debt levels and asset prices. And as we wrote a few weeks ago, technology has been a bigger threat to manufacturing jobs than Asia has.

Some people I have spoken to since the voting have expressed a wish to migrate elsewhere. Passions of this kind are not unusual. But I hope that, upon reflection, Americans will choose instead to be actively engaged in addressing the issues of our times. Facing these challenges, and each other, in a productive manner is the only way forward.

© https://www.northerntrust.com

© Northern Trust

Read more commentaries by Northern Trust