How Do Investors' Economic Outlooks Affect Valuations?

Value is in the eye of the beholder. Disagreements about whether something is cheap or expensive have typically driven people to trade. Those who assign more value to something tend to buy from those who assign less. It’s simply a way that markets work. It should be no wonder there is no universal agreement about whether stocks are cheap or expensive. If there were universal agreement, no trading would take place.

As I’ve written before, I prefer to look at a medley of measures, but it’s also important to look at the context of those different equity valuation metrics. To me, it looks like investors have almost fully embraced the idea of low growth and low inflation. If either of these factors surprise to the upside, we could exit the relatively narrow trading range the market has been in for the past few months.

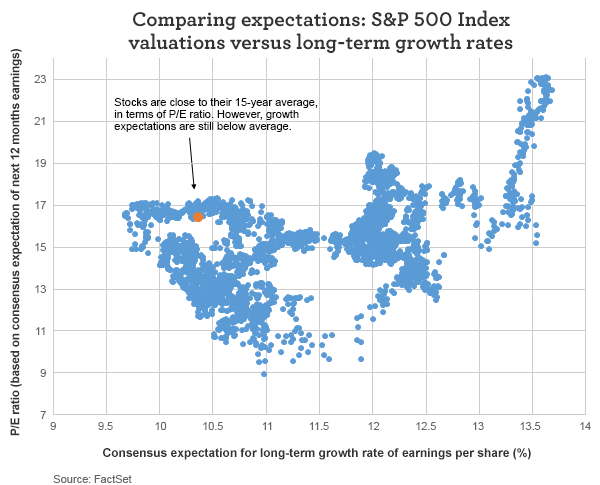

Based on the consensus expectation of next 12-months earnings for the S&P 500 Index, stocks are pretty much at their 15-year average in terms of price/earnings (P/E) ratio. The expectation for long-term growth (LTGR) in earnings per share is significantly below average.

Just looking at the historical relationship between the P/E ratio and LTGR, stocks could be cheap or expensive, since an LTGR of 10.35% (the current measure) has supported P/E ratios ranging from 12 to 18. Currently, the P/E ratio is 16.45. This is why context matters. Some people like looking at the low yield on Treasury securities and arguing that low yields support higher stock valuations. I don’t think that works very well. I think it’s more reasonable to look at the high-yield bond market instead of the Treasury market. A comparison of higher-risk assets such as stocks to credit lower-risk securities like Treasuries, is fraught with problems. Looking at the high-yield bond market could be a more reasonable measure of the opportunity cost of investing in stocks. However, stocks have tended to have higher risk potential than high-yield bonds.

The current yield-to-worst of the BofA Merrill Lynch High Yield Master II Index (a broad index of the U.S. high-yield bond market) is 5.98%. That’s below the 15-year average yield of 8.55%. Low yields in the high-yield bond market have gone a good way towards pushing up stock valuations, but that’s not the whole story; low inflation expectations also help. The inflation compensation reflected in the Treasury-forward market (based on comparing the 10-year yield to the five-year yield) is 1.57%. That’s well below the 2.59% average of the past 15 years.

Low growth expectations push valuations down, but low yields and low inflation have helped push valuations up. Together, these factors could support the S&P 500 Index at around 2,250. That’s simply the price that would be historically consistent with the prevailing levels of earnings, expected growth, yields on junk bonds, and inflation compensation. But what if companies prove to be able to grow faster than what is currently implied? What if LTGR goes from being 1.11 standard deviations below its historical average to simply its average? That, I think, could help support the S&P 500 Index at 2,350.

However, there’s also a risk that people could start anticipating faster inflation. If inflation compensation goes from its current 1.57% reading to something like 2%, the historical relationship between the S&P 500 Index and these different factors would imply a fair value of 2,025 for the S&P 500 Index.

I think the thing to watch in the near-term is what rises first (or faster): people’s expectations for growth, or their expectations for inflation. As it is, I think stocks are pretty reasonably valued, but that assessment is given in light of the current economic context. The economic context can change, and so can the fair value of a stock.

*Standard deviation of return measures the average deviations of a return series from its mean and is often used as a measure of risk. Standard deviation is based on historical performance and does not represent future results.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 10-26-16 and are those of Dr. Brian Jacobsen, CFA, CFP®, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company. Neither Wells Fargo Funds Management nor Wells Fargo Funds Distributor has fund customer accounts/assets, and neither provides investment advice/recommendations or acts as an investment advice fiduciary to any investor.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management