Inflation Overshooting: Lessons from the U.K.

U.S. interest rates moved markedly higher following the election of Donald Trump as President. Some attribute this to better growth prospects, some attribute it to less foreign demand for U.S. assets, and others point to the possibility of higher inflation. After years of sub-2% inflation, higher inflation may be welcomed by the Federal Reserve (Fed). However, if inflation rises above 2%, how much inflation overshooting would the Fed tolerate before taking action? The Fed’s United Kingdom (U.K.) counterpart the Bank of England (BoE) may provide a good model to look at, as investors seek answers to this question.

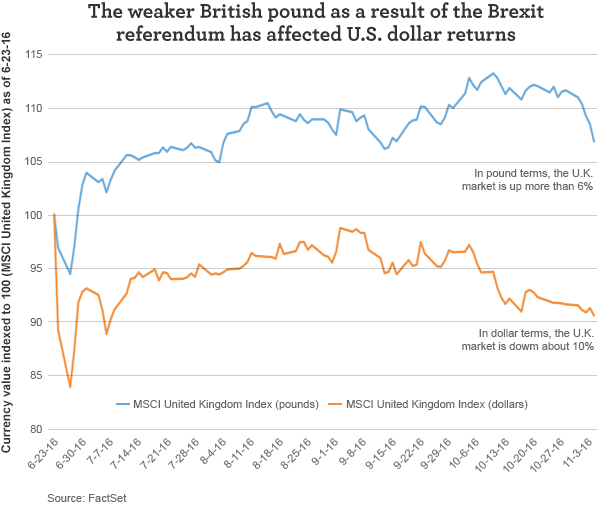

Inflation actions in the wake of Brexit

The BoE came out quickly post-Brexit with an aggressive stimulus program, cutting its bank rate, re-launching a government bond-buying program, and purchasing corporate debt. Lately, the U.K.’s economic data hasn’t been as bad as the BoE originally feared, which could stem from the fact that Brexit hasn’t happened, yet. For now, U.K. citizens can still travel freely throughout the E.U. and businesses can still sell into the E.U. market.

The pound’s decline has lifted inflation a bit, which has made British goods cheaper in the E.U.; it may also make it more profitable to sell British goods into the E.U. The converse is that goods sold by the E.U. into the U.K. have been either more expensive or less profitable for sellers. This has already caused a mini-crisis in the prices of some popular consumer goods. The BoE’s inflation forecasts have suggested that inflation could rise to 2.75%, which is well above the central bank’s 2% target. While the forecast indicates an inflation “overshoot,” the BoE said it will tolerate it. Anything above that reading and the BoE may need to tighten monetary policy.

A U.K. inflation overshoot should be temporary, if it’s only due to a weaker pound. Behind the scenes, prices would merely be adjusting to a new level—unless the pound continues to weaken. This is very different than a permanent increase in the rate of inflation; a one-time adjustment in the price level should only result in a temporary change in the inflation rate. Only if the price level keeps rising at a faster pace would it likely result in an actual increase in the rate of inflation—which is something the BoE would likely react to.

What can the U.S. learn from U.K. monetary policy?

Many central banks—especially the Fed—can learn from the BoE. The BoE’s innovation lies in how it communicates a limited tolerance for inflation overshooting. Energy and other commodity prices dropped in 2015 and early-2016. As we reach the anniversary of the depths of those price declines, year-over-year comparisons will make it look like inflation is picking up. Indeed, inflation may be picking up, but some of this is simply adjusting to a price level change and not necessarily a change in the trajectory of inflation. This will likely make it look like the U.S. is having an inflation overshooting issue, when it’s mostly just transitory.

By explicitly stating it was willing to tolerate inflation overshooting its target, the BoE gave the economy and investors room to handle these large year-over-year price adjustments without having to panic that inflation was running too hot. The central bank also provided a threshold for investors to watch as a guide to future changes in monetary policy. This helps brace people for higher inflation, but also sends a message that the BoE is on the watch and won’t let inflation rise too far.

What investors may want to keep in mind

While 2017 may be the year people talk about inflation overshooting, it will also likely be a year that central bankers hone their communication skills in describing how much or how little they are willing to tolerate. For investors, this means that they won’t get away from the constant parsing and deconstructing of Fed speeches and pronouncements. In fact, it might become even more important to listen to what the central bankers say, rather than watching what they do.

If the Fed says it can tolerate a limited amount of inflation overshooting, here’s what investors could see in the markets:

- Inflation is likely to be temporarily elevated, but should reset lower if commodity prices don’t keep moving higher.

- Stocks may falter if concerns emerge based on this question: “What if inflation is more persistent than the Fed thinks?” That could mean less stimulus rather than more.

- Bond yields could fall as the Fed would likely signal it has a watchful eye on inflation.

- Commodity prices could fall and the dollar could strengthen as the Fed may decide to hike interest rates a bit more than currently anticipated.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 11-16-16 and are those of Dr. Brian Jacobsen, CFA, CFP®, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company. Neither Wells Fargo Funds Management nor Wells Fargo Funds Distributor has fund customer accounts/assets, and neither provides investment advice/recommendations or acts as an investment advice fiduciary to any investor.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management