A Roadmap for Muni Investors on Public-Private Infrastructure Partnerships

The increasing role of the private sector in financing public transportation projects may provide an investment opportunity for municipal bond investors. In fact, President-elect Donald Trump has called for $1 trillion investment in infrastructure, much of which will depend on public-private investment for funding. Below is a review of these types of infrastructure projects, known as private-public partnerships (P3s), which have been a response to chronic funding shortages at the governmental level, and which are increasingly using municipal bonds as a cornerstone of their capital structures. These types of municipal bonds may offer incremental yield and portfolio diversification for municipal bond portfolios.

P3s and muni bonds—part of the infrastructure solution

In recent decades, P3s have become more common for two reasons. First, government entities (for example, a state department of transportation[DOT]) face funding challenges and benefit from having a private partner that is capable of bearing the financial and construction-completion risk of its infrastructure projects. Second, innovations in design and technology as well as greater complexity of infrastructure projects have meant that private participants are often better able to efficiently construct and manage operations than governmental organizations.

The reason P3s have increased their use of municipal bonds to finance projects is due to the cost effectiveness of tax-exempt debt for the concessionaire, or private entity. First, P3 projects were historically financed by a private entity using alternative financing such as bank loans, lines of credit, private equity, and corporate debt, which usually have higher yields and are therefore more expensive. Second, the federal Transportation Infrastructure Finance and Innovation Act (TIFIA) loan program, a federal credit program established by the U.S. Department of Transportation, has helped finance more than $81 billion in infrastructure investment. This program requires that senior debt have an investment-grade credit rating, and from an issuer’s perspective, this requirement helps makes tax-exempt debt attractive because of the strong demand in the municipal market for investment-grade securities.

As an example of a P3, the state of Indiana in 2006 sold a concession of the 156-mile Indiana Toll Road to a private consortium. In this case, the consortium paid the state $3.8 billion for the right to maintain, operate and collect the tolls (subject to regulations laid out in the concession agreement) on the road for 75 years.

Innovative financing structures have resulted from several negative experiences in the nascent P3 market in the U.S. (including the bankruptcies and restructuring of several toll roads) that seek to reduce the issuer’s credit risk. These new structures include alternative user-fee schemes (such as variable demand pricing and managed lanes) and availability payments (payments made by the public governmental sponsor to private entities based on delivery and maintenance of a specific asset). In addition, these for-profit private entities have implemented innovative pricing structures previously not palatable to the politically-sensitive government entities in order to both capture value from customers and manage congestion.

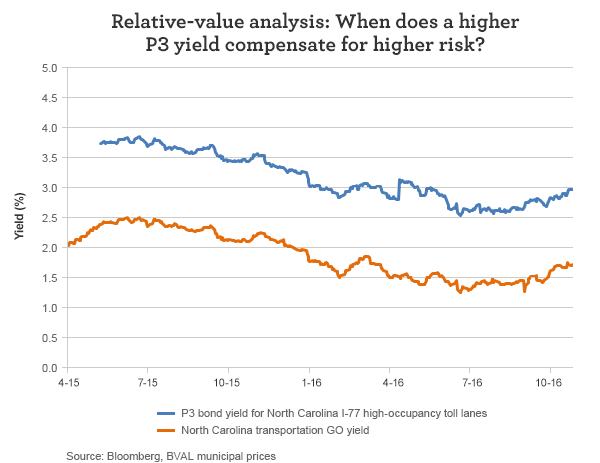

Example 1: Comparing P3 to traditional muni bonds

This example looks at a P3 project that has a user-fee scheme of managed lanes. According to the Federal Highway Administration, the number of vehicle miles traveled in the United States has increased more than 70% in the last 20 years, while highway capacity has only grown by 0.3%. As a result, managed lanes have been developed as a strategy to regulate ever increasing demand and best use available and unused capacity. A managed lane project is typically a “freeway-within-a-freeway” where a set of lanes within the freeway is separated from general-purpose lanes and is tolled or restricted to only certain vehicles (high-occupancy, for example) to mitigate congestion on general-purpose lanes. Such projects often have prohibitively high startup costs and are exceedingly complex, and this has provided an opportunity for private parties to design, build, and operate these assets.

For many managed-lanes projects, the project risks are unique to each project, requiring an understanding of the project construction risk, the drivers of demand for this asset as well as potential technical and regulatory issues that may arise. This project-specific analysis contrasts with the credit analysis of state DOTs and metropolitan planning organizations (MPOs) that often have taxing authority and a much more diverse portfolio of assets that in sum can subsidize any single underperforming asset. As such, public ratings of these projects are typically much lower (and provide greater investing upside and downside) than bonds issued by the DOTs or MPOs.

The chart below compares yields for a P3 bond and a comparable general obligation (GO) transportation bond. The P3 bond is for the I-77 high occupancy toll lanes project in North Carolina and is rated BBB-. The traditional transportation bond is the state of North Carolina’s GO, which is AAA-rated by all three credit-rating agencies. Both bonds feature similar structures (both have 2026 maturities, are callable in 2025, and have 5% coupons). Clearly, the P3 bond provides incremental yield but reflects increased credit risk. While the additional yield may be attractive, understanding the credit fundamentals that account for the yield difference is necessary to make investment decisions.

Example 2: Focusing on credit trends

Private parties in P3s have had mixed experiences due to unforeseen fluctuations in traffic, recessions, and unrealized traffic demand. To alleviate these risks, availability payment structures have been developed to help eliminate the risk of uncertain traffic patterns for the concessionaire. Since payments are contingent upon successful completion of the asset and contractually-mandated asset maintenance, understanding construction and performance risk is essential; once the project is successfully delivered, only performance risk remains a credit concern.

For an investor, these types of projects could be an opportunity, particularly since many of these bonds have experienced credit rating upgrades as they near completion. The credit ratings of these bonds initially are often in the BBB- category, reflective of the construction risk, and have then migrated closer to the public sponsor’s higher credit rating as construction progresses. It is our belief that once the projects are successfully delivered, the ratings of the P3 bonds will be higher (though likely lower than the public sponsor’s ratings) from initial levels as the principal project risk (construction) is eliminated. However, these structures are not immune to distress—the I-69 project was downgraded by Fitch Ratings several times to B-rated from its initial rating of BBB-rated due to continued delays in construction and contractor disputes. The I-69 experience should serve as a cautionary tale for investors moving into the sector to capture potential rating upside.

The table below displays the differences between the initial rating of these P3 projects with that of their public sponsors. Although the table shows only a limited number projects, one can see credit ratings modestly migrate upward as these projects move toward completion.

Projects backed by availability payments have potential for credit rating upside

|

Ratings |

|||||

|

Project |

State |

Public sponsor |

Initial |

Current |

Public sponsor |

|

I-595 Corridor |

FL |

Florida DOT |

NA |

NA |

NA |

|

Port of Miami Tunnel |

FL |

Port of Miami |

NA |

NA |

NA |

|

FasTracks Eagle P3 |

CO |

Denver Reg. Trans. Dist. |

Baa3/--/BBB+ |

Baa3/--/BBB+ |

Aa3/A/AA- |

|

Presidia Parkway |

CA |

California DOT |

NA |

NA |

NA |

|

Ohio River East End Crossing |

IN |

State of Indiana |

--/BBB/BBB |

--/BBB/BBB+ |

Aa1/AA+/AA+ |

|

Goethals Bridge |

NJ |

Port Auth NY NJ |

--/BBB-/BBB- |

--/BBB-/BBB |

Aa3/AA-/AA- |

|

I-69 Section 5 |

IN |

Indiana DOT |

--/BBB-/BBB |

--/BB-/B |

Aa1/AA+/AA+ |

|

I-4 Ultimate |

FL |

Florida DOT |

NA |

NA |

NA |

|

Pennsylvania Rapid Bridges |

PA |

Pennsylvania DOT |

--/BBB/-- |

--/BBB/-- |

Aa3/AA-/-- |

|

Portsmouth Bypass |

OH |

Ohio DOT |

Baa2/BBB/-- |

Baa2/A-/-- |

Aa1/AA+/AA+ |

|

Next Generation Fiber Optics |

KY |

State of Kentucky |

Baa2/--/BBB+ |

Baa2/--/BBB+ |

Aa3/A/-- |

|

Purple Line Light Rail |

MD |

Maryland DOT |

--/BBB+/BBB+ |

--/BBB+/BBB+ |

Aa1/AA+/AA+ |

Sources: Wells Capital Management, Moody’s Investor Service, Standard and Poor’s, and Fitch Ratings as of October 28, 2016.

Conclusion

Due to funding pressures at the governmental level, private concessionaires have become an increasingly important partner for transportation infrastructure delivery in the 21st century. With the prominence of the TIFIA program, municipal bonds have become an integral and cost-effective financing vehicle for these types of projects and private entities.

The credit analysis for P3 projects, however, are different and more onerous than that of a state DOT or regional transportation authority because of the discrete risks the private operators face. A lack of taxing power, nonexistent non-operational or outside financial support and the limited scope of the assets naturally leads to lower credit quality for the concession project (and therefore offer incremental yield); however, experience in and understanding of innovations in tolling and new funding models (availability payments), can potentially generate excess investment returns. Properly understanding the construction risk of a project backed by availability payments might lead to the purchase of a BBB-rated security that can turn into an A or higher-rated bond within a couple years. Similarly, an in-depth understanding of the demand dynamics for a managed lane project could result in not investing in an opportunity deemed too speculative.

Undoubtedly, the fiscal pressures faced by governments combined with demand for transportation infrastructure will continue to lead government officials to look to the private sector for infrastructure delivery. Meanwhile, having an in-depth understanding of the legal, economic, and technical issues associated with these projects is essential for investing in this growing sector.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 11-28-16 and are those of Lyle Fitterer, CFA, CPA, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company. Neither Wells Fargo Funds Management nor Wells Fargo Funds Distributor has fund customer accounts/assets, and neither provides investment advice/recommendations or acts as an investment advice fiduciary to any investor.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management