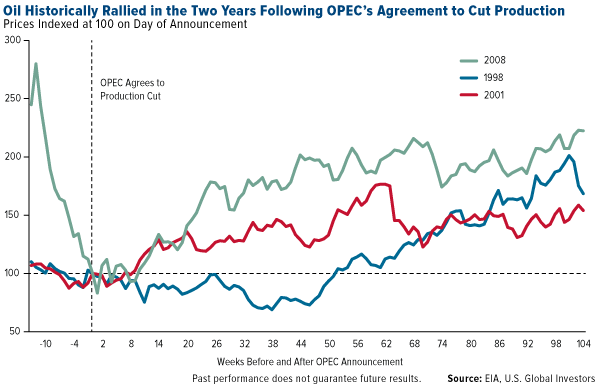

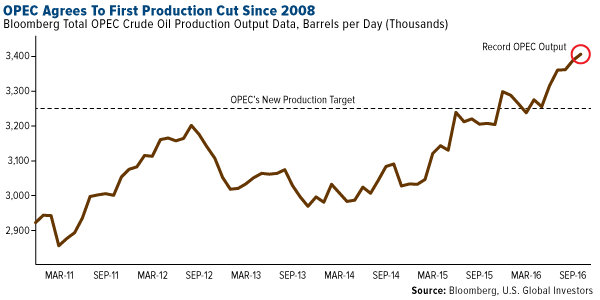

It finally happened. For the first time since 2008, the Organization of Petroleum Exporting Countries (OPEC) agreed to a crude oil production cut this week, renewing hope among producers and investors that prices can begin to recover in earnest after a protracted two-year slump, one of the worst in living memory.

The last three times the cartel agreed to trim output—in 2008, 2001 and 1998—oil rallied in the following weeks and months. Of course, there’s no guarantee the same will happen this time around, as other market forces are at play, but it’s helpful to look at the historical precedent.

OPEC’s decision follows a strong endorsement from Goldman Sachs, which upgraded its rating on basic materials to overweight for the first time in four years. Analysts see commodities gaining 9 percent on average over the next three months, 11 percent over the next six months.

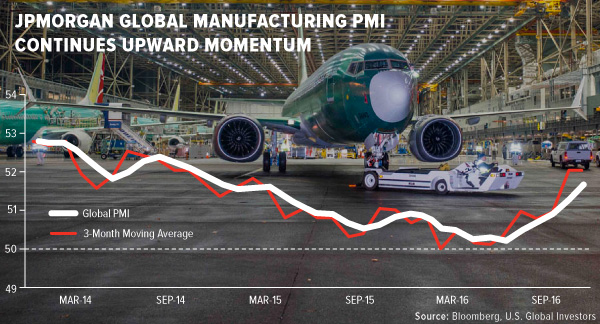

As reported by TheStreet’s Paul Whitfield, Goldman’s change of heart was prompted by “the recent acceleration in global PMIs (purchasing managers’ indexes),” which “suggests commodity markets are entering a cyclically stronger environment.”

The JPMorgan Global Manufacturing PMI rose slightly in November to a 27-month high of 52.1, extending sector expansion for the sixth straight month—very encouraging news.

As I’ve shared with you many times before, our own research has shown a strong correlation between PMI performance and commodity prices three and six months out. I’m thrilled to see Wall Street and media outlets coming around to this realization as well.

In short, OPEC’s production cut is constructive for energy in the near term, while a rising PMI is good news for the long term.

$70 Oil Next Year?

Since oil collapsed in September 2014, as much as $4 billion have been wiped from oil workers’ wages in the U.S. alone, according to Bureau of Labor Statistics data. Countries that rely heavily on oil revenue—Venezuela, Colombia, Russia and Nigeria, notably—have had to stretch balance sheets. And for the first time in nearly 40 years, Alaska, where the oil industry accounts for half of all economic activity, is scheduled to impose an income tax by 2019.

Many analysts now find reason to be optimistic about a recovery in energy. Speaking to the Houston Chronicle, David Pursell of energy investment bank Tudor, Pickering, Holt & Co. predicts “2017 will be a better year for oil and gas activity than we anticipated.” Pursell sees crude possibly rallying above $70 a barrel sometime next year.

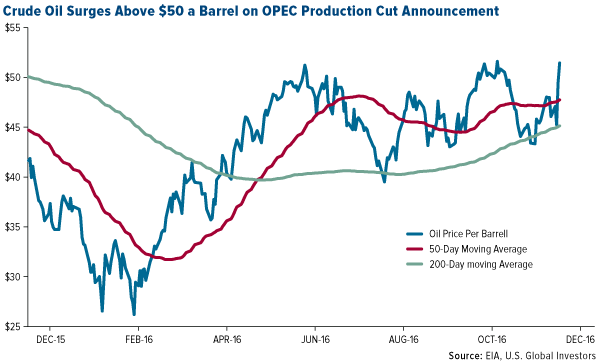

The OPEC deal, announced on Wednesday, aims to reduce production by 1.2 million barrels a day, or about 1 percent of global output. For comparison’s sake, the cartel, which controls a third of all oil production, agreed to a reduction of 2.2 million barrels a day in 2008. Although not an OPEC member, Russia has also agreed to trim production—by about 300,000 barrels a day—the first time it’s cooperated with OPEC since 2001.

Following the announcement, West Texas Intermediate (WTI) crude surged above $50 a barrel.

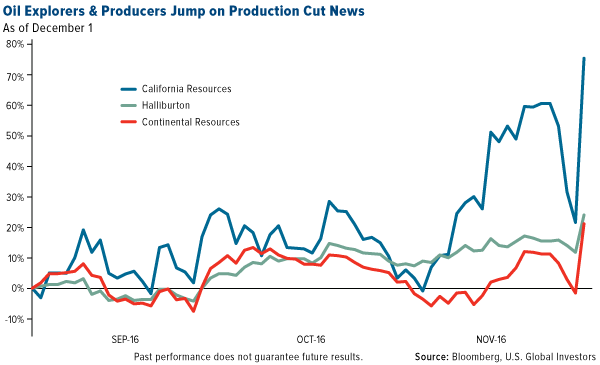

Meanwhile, investors piled into oil ETFs, with inflows into one surpassing $1 billion on Thursday alone. Shares of Halliburton, Continental Resources and California Resources all saw dramatic spikes.

The Challenges Ahead

Some investors are understandably cautious. OPEC doesn’t have the authority to enforce compliance from its 14 member-nations, and output has typically exceeded quotas.

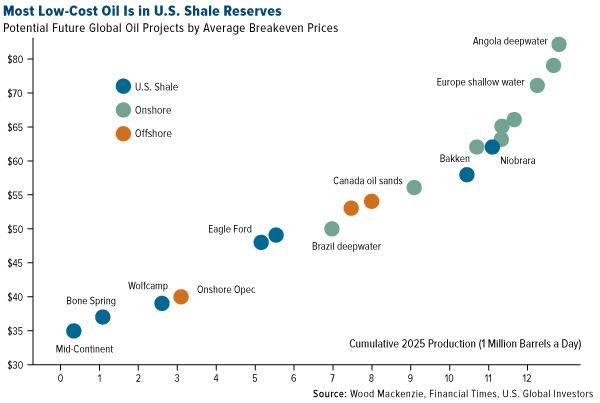

What’s more, it’s likely U.S. shale producers, which today operate at lower costs compared to other players, will be first to take advantage of a bump in prices. Drilling activity is already accelerating. Since May, the number of active oil rigs in North America has climbed 50 percent to 474, as of November 23.

“U.S. oil production growth is all but guaranteed to return in 2017,” according to Joseph Triepke, founder of oil research firm Infill Thinking. Triepke adds that as many as 150 rigs could be reactivated next year in Texas’ Permian Basin alone.

It’s there, in the Wolfcamp formation of the Permian, that the United States Geological Survey (USGS) recently discovered 20 billion barrels of “technically recoverable” oil, the largest deposit ever to be found in the U.S. Bloomberg reports that the deposit is worth an estimated $900 billion at today’s prices.

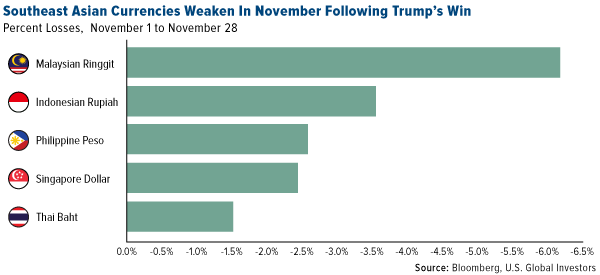

On the demand side, higher prices could spell trouble in emerging countries whose currencies have weakened against the U.S. dollar in recent months, especially since Donald Trump won the presidential election. Because oil is priced in dollars, it’s become more expensive in China and India, the second and third largest oil consumers following the U.S.

Gold Looks Technically Oversold, Ready for a Price Reversal

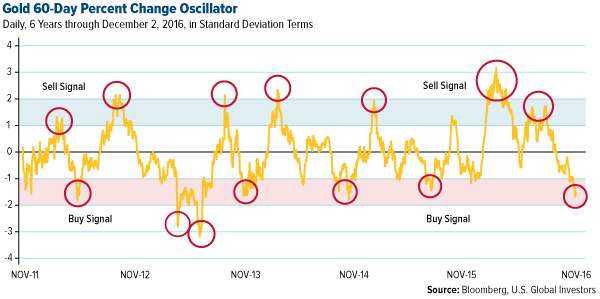

As I often say, every asset class has its own DNA of volatility, which is measured by standard deviation. Specifically, standard deviation gauges the typical fluctuation of a security or asset class around its mean return over a period of time ranging from one day to 12 months or more.

This brings us to mean reversion, which is the theory that, although prices might trend up for some time (as in a bull market), or fall (as in a bear market), they tend to move back toward their historic averages eventually. Such elasticity is the basis for knowing when an asset is overbought or oversold—and when to sell or buy.

As you can see in the oscillator below, gold looks oversold right now and is nearing a “buy” signal, after which we can statistically expect it to return to its mean.

Gold’s current standard deviation for the 60-day period is about 7 percent—you can reasonably expect it to move this much over a two-month period, therefore, 68 percent of the time.

For more on standard deviation and mean reversion, I invite you to download my whitepaper, “Managing Expectations: Anticipate Before You Participate in the Market.”

Awaiting the Italy Referendum

2016 hasn’t been shy about pitching some unexpected political curveballs, from Brexit in the U.K. to the election of Donald Trump here in the U.S.

But 2016 isn’t over yet and might still have a surprise up its sleeve.

|

This Sunday, Italy’s voters will head to the polls and decide whether proposed amendments to the country’s nearly 70-year-old constitution pass or fail. If approved, the amendments will structurally change the size and scope of the nation’s government. Among the most significant changes are the composition of Parliament, how bills become law and the balance of power between the central government and the nation’s 20 regional jurisdictions. A “yes” vote would allow Italian Prime Minister Matteo Renzi, in power since February 2014, to streamline the lawmaking process and introduce sweeping economic reforms.

A “no” vote would leave the constitution as it is, with Renzi pledging to step down if voters reject his amendments. What happens next is unclear, but a referendum for Italy to leave the European Union—an “Itexit”—has been suggested by the populist Five Star movement.

As of today, national polls are giving “no” the edge. But after polls were so wrong about Brexit and Trump, can we really take them seriously anymore?

Elections have consequences, and some in the media are calling the Italian referendum even more consequential than Brexit. I’ll be watching the results closely this Sunday and will share with you my full thoughts next week.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.10 percent. The S&P 500 Stock Index fell 0.97 percent, while the Nasdaq Composite fell 2.65 percent. The Russell 2000 small capitalization index lost 2.45 percent this week.

- The Hang Seng Composite lost 0.45 percent this week; while Taiwan was up 0.33 percent and the KOSPI fell 0.19 percent.

- The 10-year Treasury bond yield rose 3 basis points to 2.39 percent.

Domestic Equity Market

Strengths

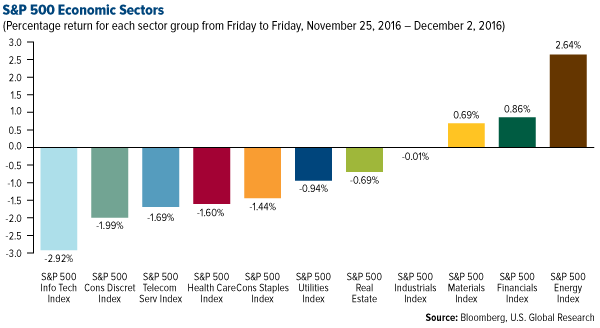

- Energy was the best performing sector for the week, increasing by 2.64 percent versus an overall decrease of -0.98 percent for the S&P 500.

- Transocean was the best performing stock for the week, increasing 14.49 percent. The company’s stock rallied after the news that OPEC agreed to cut production.

- Goldman Sachs is trading at its best level since the financial crisis. Shares of the investment bank ended Wednesday at $219.29, its highest level since the end of 2007. Goldman has gained about 36 percent since August 31.

Weaknesses

- Information technology was the worst performing sector for the week, falling by -2.92 percent versus an overall decrease of -0.98 percent for the S&P 500.

- Vertex Pharmaceuticals was the worst performing stock for the week, falling -13.98 percent. Sentiment toward the company has been worsening and was dealt a new blow after Barclay’s analysts downgraded the stock.

- Guess shares plunged after the company reported an earnings miss and disappointing fourth-quarter guidance. The stock plunged as much as 14 percent in extended trading.

Opportunities

- Sony is on track to crush Facebook and HTC in virtual reality sales. Sales of Sony's PlayStation VR are on track to total 745,434 units in 2016, ahead of HTC Vive's 450,083 and Facebook's Oculus Rift's 355,088.

- AT&T has unveiled DirecTV Now. The streaming-TV service launches Wednesday and will give subscribers 60 channels for $35 a month or 120 channels for $70 a month.

- Tiffany's sales jumped for the first time in two years. Tiffany & Co reported its first rise in sales in eight quarters as strong sales in Japan and China more than offset a decline in the United States, its biggest market.

Threats

- Smith & Wesson plunged 8 percent after-hours on Thursday on light EPS guidance. The gun maker’s shares sank after the election on concern that reduced fears of gun control would slow sales.

- Prior to the current incidence, a 50 basis point rise in the JP Morgan Global Government Bond Yield over three months has occurred only eight times this century. On three out of the eight occasions, world equities rose modestly, but on the other five they fell. On all eight occasions, the equity market's subsequent three-month performance consistently deteriorated, on average by -7 percent, compared to the preceding three-month performance. For reference, today's preceding three-month performance is just 0.7 percent.

- According to BCA, the recent underperformance of emerging market equities is a warning sign for U.S. cyclical versus defensive sectors, as emerging markets and the relative performance of U.S. cyclical versus defensive stocks have tended to move hand-in-hand.

![[thumb]](/images/content_image/data/e8/e835fae1c0d5bab5e46aaaf377505a65.jpg)

December 1, 2016Modis Demonetization Is a Cure Worse Than the Disease |

![[thumb]](/images/content_image/data/8d/8db00e4be59f5c7ca7ed4ada56619ee8.jpg)

November 29, 2016A Tale of Two Economies: Singapore and Cuba (UPDATE) |

![[thumb]](/images/content_image/data/ef/ef6a2bd424a0e64774f164cdc53ed2e5.jpg)

November 28, 2016The Great American Splurge |

The Economy and Bond Market

Strengths

- GDP crushed estimates thanks to consumer spending. The U.S. economy grew by 3.2 percent in the third quarter — better than expected and initially reported — according to the second estimate of GDP, released Tuesday. Consumer spending was stronger than previously estimated, and it was the main reason overall economic growth was revised higher. Personal consumption grew by 2.8 percent, up from 2.1 percent in the Commerce Department's initial estimate.

- It was another good employment report, with the U.S. economy adding 178,000 net new jobs in November and the unemployment rate falling to a new cyclical low of 4.6 percent from 4.9 percent.

- U.S. manufacturing crushed expectations in November, with the ISM purchasing managers’ index (PMI) rising to 53.2 in November (52.5 expected.) However, the strong U.S. dollar remains a headache for producers in the sector given that it makes it more expensive for people outside of the U.S. to buy American products.

Weaknesses

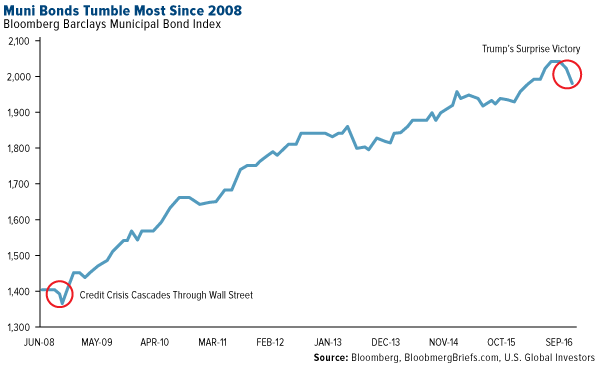

- Bonds got demolished last month. Global bonds lost $1.7 trillion of value in November, according to Bloomberg. Additionally, municipal bonds lost 2.1 percent, the worst month since October 2008 when financial markets seized up after the collapse of Lehman Brothers.

- This latest employment report showed the participation rate falling to 62.7 percent, which halts what had looked like a promising, nascent uptrend.

- Despite the improving labor market, wages were surprisingly soft. Average hourly earnings fell 0.1 percent month-over-month and annual wage inflation slowed to 2.5 percent from 2.8 percent.

Opportunities

- The November nonmanufacturing ISM survey on Monday will provide a useful and timely read on the state of the economy.

- Consumer confidence soared to a post-recession high. According to the Conference Board's monthly report published on Tuesday, the confidence index rose to 107.1, the highest level since July 2007. This was the first full report from the Conference Board since the U.S. election.

- Upcoming Chinese PPI and CPI data on Friday will be important to watch for more evidence that deflationary pressures in the Chinese economy are abating.

Threats

- The results of this weekend's Italian referendum will dictate how global financial markets open the trading week. A "No" victory could cause a knee-jerk sell-off in Italian assets and "risk off" in global markets.

- A "serious hangover" is about to hit the bond market. According to the fixed income strategists at Societe Generale, a structural shift is coming for the bond market that will end the multi-year run up in the price of debt. A combination of government policies, central bank tightening, and increasing global growth will put a stop to the so-called "bond party" of the past 30 years and cause a "serious hangover."

- While the housing market has continued to perform strongly, the recent rise in bond yields and mortgage rates could begin to cool things down.

Gold Market

This week spot gold closed at $1,175.79, down $8.11 per ounce, or 0.69 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week up by 3.88 percent. Junior miners underperformed seniors for the week, as the S&P/TSX Venture Index gained 2.01 percent. The U.S. Trade-Weighted Dollar Index finally saw some weakness, posting a loss of 0.78 percent for the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Nov-29 |

Germany CPI YoY |

0.8% |

0.8% |

0.8% |

|

Nov-29 |

U.S. GDP QoQ |

3.0% |

3.2% |

2.9% |

|

Nov-29 |

U.S. Consumer Confidence Index |

101.5 |

107.1 |

100.8 |

|

Nov-30 |

Eurozone CPI Core YoY |

0.8% |

0.8% |

0.8% |

|

Nov-30 |

U.S. ADP Employment Change |

170k |

216k |

119k |

|

Nov-30 |

Caixin China PMI Mfg |

51.0 |

50.9 |

51.2 |

|

Dec-1 |

U.S. Initial Jobless Claims |

253k |

268k |

251k |

|

Dec-1 |

U.S. ISM Manufacturing |

52.5 |

53.2 |

51.9 |

|

Dec-2 |

U.S. Change in Nonfarm Payrolls |

180k |

178k |

142k |

|

Dec-6 |

U.S. Durable Goods Orders |

0.7% |

-- |

4.8% |

|

Dec-8 |

ECB Main Refinancing Rate |

0.000% |

-- |

0.000% |

|

Dec-8 |

U.S. Initial Jobless Claims |

250k |

-- |

268k |

Strengths

- The best performing precious metal for the week was platinum, up 2.34 percent, followed by palladium with nearly flat returns. Platinum group metals have lifted somewhat with the anticipation of stronger industrial growth.

- Even though investors can’t seem to unload gold fast enough, coin collectors are benefitting, reports Bloomberg. U.S. Mint gold-coin sales jumped for a fourth straight month, the longest streak since 2003. And in India, despite the fall in sales of jewelry due to demonetization, gold imports remained stable at around 100 tonnes in November (from 97 tonnes in October).

- According to Bloomberg Intelligence, the five-year average gold premium is typically around $5.50 an ounce in China, but has soared to almost $40 an ounce, as falling prices invite “bargain buying” among the Chinese. As the Financial Times reports, China has curbed gold imports as the government tries to clamp down on capital leaving the country, along with the yuan falling to its lowest against the U.S. dollar in eight years.

Weaknesses

- The worst performing precious metal for the week was gold with a loss of 0.56 percent, with silver putting in a 1.27 percent gain. Perhaps we are beginning to see somewhat of a floor develop, particularly with gold miners’ shares putting in a gain for the week too.

- As gold prices reach a 10-month low this week, gold traders are the most bearish since May, reports Bloomberg. The yellow metal is headed for its biggest monthly drop since 2013, while investors continue to pull money out of funds that are linked to the metal – holdings in gold-backed ETFs contracted 5.3 percent since November, according to Bloomberg data. Even gold put options jumped as futures continue to head down.

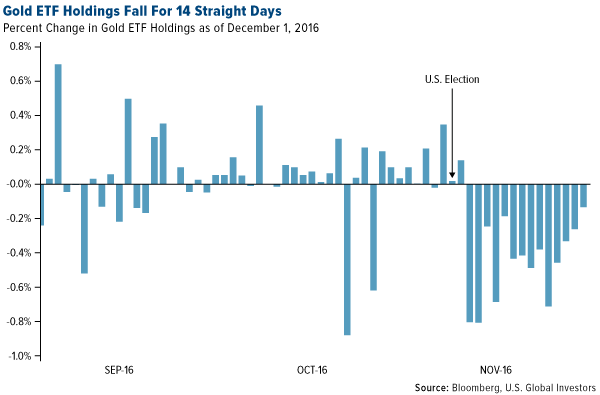

- Gold is headed for its fourth weekly drop, the longest down streak since May, reports Bloomberg. As seen in the chart below, the gold fund selling spree continued this week, with holdings falling for a fourteenth straight day, as of Thursday.

Opportunities

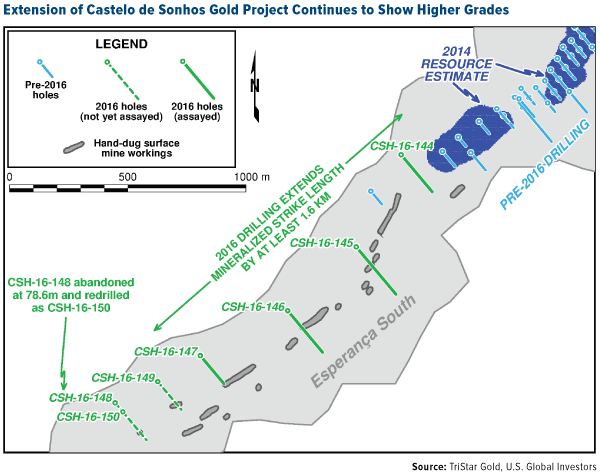

- A release from TriStar Gold highlights recent resource growth potential, specifically confirming that two step-out holes at the company’s Castelo de Sonhos gold project show gold mineralization extending at least 1.6 kilometers (km) to the southwest (and beyond the resource area defined by the company in its 2014 Technical Report). Both drill rigs have now moved to Esperanca Central and are drilling to the north of the current area, the report continues. Nick Appleyard, TriStar’s President and CEO, commented that drill results are exceeding expectations and are all “significantly higher than the average drill results that were used for the 2014 estimate in terms of grades and thicknesses.” Drilling stopped in 2014 to conserve cash but the improved market conditions have made it possible for explorers to access capital markets. TriStar controls a 14 km long anomalous gold in soils, with widths ranging from 350 to 850 meters at Castelo do Sonhos. The planned drill program could confirm significant resource growth potential for TriStar Gold.

- K92 Mining announced this week the initial results of the ongoing grade control drilling program at its Kainantu Gold Mine. According to the company, the results have significantly increased both the predicted grade and contained gold ounces in the first two planned production stopes. One highlight specifically notes that the grade increased from 5.82 grams per ton of gold in the original model, to 9.21 grams per ton in the new model. Drilling density is being improved to 15 meter centers versus earlier work at 50 meter centers.

- In a news release this week, BNY Mellon’s Pershing announced the launch of BMO Gold Deposit Receipts (GOLDRs). According to the release, the GOLDRs act as a book-entry solution for investors who want bullion in their brokerage account without experiencing the inconveniences that typically accompany purchasing and storage. GOLDRs represent ownership in one ounce of fully-allocated physical gold bullion held at the Royal Canadian Mint. “The solution is the first of its kind to allow bullion to be held in a brokerage account, providing new opportunities for advisors to offer an alternative means for their clients to invest in gold,” with options for physical deliver, should the buyer desire, the release reads.

Threats

- The combination of India’s currency recall and the potential for an increase in U.S. interest rates, Indian stocks and the rupee had their worst November performance in five years, reports Bloomberg. One anecdote from an unemployed teacher in India shines light on the currency situation. The Bloomberg story explains that the man needed money to cover emergency expenses, but was unable to get a loan since he was out of work. In August he took a 14-gram gold bangle and used it as collateral for a six-month loan of 27,500 rupees. Since then, however, the gold-loan business has gotten bumpy following Modi’s decision to invalidate 500 and 1,000 rupee notes. Now, the shortage of legal tender is hurting lenders and Indians are scrambling to get their hands on valid currency.

- According to an analyst with Centrum Wealth Management in Mumbai, Payal Pandya, demonetization will “be a blow” for the gold-loan business, Bloomberg reiterates. Pandya believes that companies might have to slash projections of loan growth for the year by 5 percent to 7 percent. A Nov. 23 report from Ambit Capital analysts notes that a shortage of cash is also putting a squeeze on India’s $40 billion jewelry market, with transactions potentially shrinking as much as 30 percent due to a shortage of notes. Bloomberg sums up the article with the following: “India’s government wants the economy to be less resilient on cash and especially gold, which many Indians use to store their wealth.”

- Two top gold forecasters see further losses for the yellow metal in 2017, reports Bloomberg. Both Oversea-Chinese Banking Corp and ABN Amro see gold slipping to $1,100 an ounce by the end of next year. “From an investor point of view, there is little reason to own gold,” Georgette Boele, a currency and commodity analyst with ABN Amro said.

Energy and Natural Resources Market

Strengths

- Crude oil was the best performing commodity for the week following OPEC's first supply cut agreement in over eight years. As a result, crude oil climbed to its highest level this year on expectations for OPEC to reduce output by 1.2 million barrels per day.

- The best performing sector for the week was the S&P Super Composite Oil and Gas Exploration and Production Index. The index rose 6.44 percent on the back of rallying crude oil prices this week.

- Halliburton, one of the world’s largest oil field services companies, was the best performing stock this week finishing up 9.41 percent. The stock rallied on the back of momentum gained this week in the incredible crude oil rally.

Weaknesses

- Zinc was the worst performing commodity this week falling 6.8 percent. After an incredible 50-percent rally over the past year, zinc prices are beginning to pull back as China moves to limit speculative trading in base metals futures.

- The worst performing sector this week was the NASDAQ Clean Energy Index. The index fell 4.54 percent on speculation that U.S. government policies will move to favor traditional energy sources over renewable alternatives.

- The worst performing stock for the week was Alcoa Inc., the world’s third largest producer of aluminum. The company fell 8.39 percent on the back of Deutsche Bank downgrading it to a strong sell rating.

Opportunities

- Natural gas prices continued to rise this week thanks to falling stockpiles. A weekly withdrawal of 50 billion cubic feet and lower temperatures forecast should provide a positive read through for natural gas prices.

- Base metal prices continue to rise in light of stronger macroeconomic data. A strong print in U.S. GDP this week of 3.2 versus analyst expectations of 3.0 has supported commodity prices, even in spite of the rallying U.S. dollar.

- Automakers beat November sales estimates in spite of a slow start to the month, keeping 2016 within reach of another record year. This data should provide a positive read through for platinum group metals which are used intensively in auto manufacturing.

Threats

- China tightened gold import quotas this week as an effort to curb capital flight and limit the renminbi's decline. As one of the two largest global importers of gold, China's action is bearish for the yellow metal.

- Caterpillar, one of the largest construction machinery companies in the world and a proxy for industrial demand, stated this week that analysts are too optimistic of its projected earnings for 2017.

- Industrial metals plummeted this week roughly 11.6 percent suffering their largest fall since March of this year. The move downward was ignited by China further tightening trading rules and margins in its futures exchange. Until regulators in China can clamp down on excessive speculation, further volatility is expected in the industrial metals universe.

China Region

Strengths

- China’s manufacturing sector grew at its strongest pace in more than two years in November, reports Reuters. The government’s official purchasing managers’ index (PMI) came in at 51.7 from 51.2 in October.

- China’s nonmanufacturing PMI, a measure of activity outside of factory gates, rose for the third straight month to 54.7 in November from 54.0 in October.

- Japan’s Nikkei closed up 11 percent on Thursday, the highest since December 2015, reports Reuters. The move comes after this week’s OPEC agreement to cut crude output for the first time since 2008, along with a weaker yen, the article continues.

Weaknesses

- China Foreign Direct Investment Flows (M&A a part) have turned from persistently positive to sharply negative, hurting China’s Forex Reserves and thereby the fall in the Chinese yuan in currency markets. Worried about Forex Reserves outflows, Beijing announced new limits on outbound M&A.

- Macau’s casino shares dropped in Hong Kong trading following news that the city may require inbound travelers to disclose cash holdings of more than $15,000 at entry. Some analysts think that the move could be part of China clamping down on capital controls. The risk is that this could be just the beginning, with more measures going forward.

- The worst performing country in the region this week was China down 55 basis points and the worst currency was Indonesian rupiah down 4 basis points.

Opportunities

- According to China’s State Administration of Foreign Affairs (SAFE), the nation’s government is cracking down on sham overseas direct investments, reports CNBC. An internal document from the People’s Bank of China (PBOC) shows that $290 billion left China to overseas markets from January to October of this year, with no signs of slowing down.

- During the 10th National Congress of the Association of Literature and Art on Wednesday, Chinese President Xi Jinping called upon artists in the country to “consolidate the confidence in Chinese culture and use art to inspire people,” reports China Daily. He outlined four expectations to guide artists and writers to serve the people and create more inspiring and classical works to revive the nation.

- A long-awaited trading link between Shenzhen and Hong Kong stock exchanges is set to open on December 5, reports MarketWatch. This would make hundreds of China’s fastest-growing companies available to foreign investors, the article continues. According to one Goldman Sachs analyst, the new connection will “essentially create the second largest equity market globally by market cap.”

Threats

- As Southeast Asian currencies slide, the region is bracing for rising debt bills, reports Bloomberg. The repayment amount on dollar-denominated bonds for companies, banks and governments in the area will rise 8 percent next year to $19.7 billion, the article continues. As you can see in the chart below, weakening currencies threaten to push up servicing costs on the debt.

- Pressure is mounting for Taiwan’s newest leader Tsai Ing-wen and her Democratic Progressive Party (DOO) to show more success, only six months into the presidency, reports the South China Morning Post. Tsai’s approval rating has sunk to 26 percent from 47 percent in June, as policy fights slow reform.

- Chinese leaders are concerned about a fledgling independence movement and recent protests in Hong Kong (which returned to mainland rule in 1997 with a promise of autonomy), reports Reuters. Zhang Dejiang, senior Chinese official responsible for Hong Kong affairs, “hopes Hong Kong compatriots can clearly oppose Hong Kong independence, jointly safeguard Hong Kong’s social and political stability,” and “amass popular sentiment to seek development and promote harmony,” the article continues.

Emerging Europe

Strengths

- Romania was the best-performing country this week, gaining 1.6 percent. Bucharest stock exchange gains were led by refining company OMV Petrom and Banca Transylvania.

- The Russian ruble was the best-performing currency this week, gaining 1.6 percent against the dollar. The Russian currency grew stronger due to OPECs decision to cut the production of oil. Brent crude oil gained 13.6 percent and closed at $53.8 per barrel.

- Energy was the best-performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst-performing country this week, losing 1.3 percent. Shares of Dogan Holding Company, the Turkish media and energy group that also owns Trump Towers in Istanbul, declined by 14.8 percent after one of its executives was detained in Ankara. The Istanbul stock exchange continued its sell off due to domestic and geopolitical tension.

- The Turkish lira was the worst-performing currency this week, losing 1.8 percent against the dollar. President Erdogan demanded lower interest rates in a public speech and Prime Minister Yildirim announced that the executive presidency bill will be in Parliament next week. Once it passes through Parliament with minimum 330 votes, Turkey will hold a referendum within 60 days.

- The industrial sector was the worst-performing sector among eastern European markets this week.

Opportunities

- Inflation data reported for Poland showed zero year-over-year change, ending 28 months of deflation. The latest projections by the central bank’s staff see price declines ending this year and inflation reaching 1.3 percent in 2017 and 1.5 percent in 2018.

- Francois Fillion from the center-right Republican Party and supporter of Vladimir Putin will run in France’s presidential election next year. Fillion’s vision is that France and Europe should be a little closer to Moscow and little more distant from the U.S. He has repeatedly opposed economic sanctions against Russia following annexation of Crimea. Donald Trump has promised more respect for Russia and another Russian friendly face may enter the Elysee Palace in France next year.

- The manufacturing purchasing managers’ index (PMI), which is closely watched by policymakers, increased 0.2 points to 53.7, to reach its highest point since the start of 2014. European Central Bank (ECB) president Mario Draghi has been clear in his belief that the accommodative policy has been a major driver behind continental Europe’s recent recovery. But, the eurozone faces a series of political risks, starting with presidential election this Sunday in Austria and constitutional referendum in Italy on Monday.

Threats

- Turkey’s central bank has said Turkish companies had foreign currency liabilities of about USD 210 billion at the end of September. And, the problem may be getting worse. The rollover ratio for Turkey’s corporate sector was more than 160 percent in the first nine months of this year, according to the central bank. Rising rates in the U.S. will negatively affect the lira and increase Turkey’s borrowing cost.

- Pavel Kushnir, Deutsche Bank’s oil and gas analyst, in his research wrote that Russian oil companies can best adjust to lower crude oil prices, given the progressive tax system and potential ruble devaluation. OPEC agreed to cut production and if oil continues to recover, Russian names may underperform as the same factors would not allow them to fully benefit from the higher price.

- In Turkey almost 600, worth 10 billion dollars, were siezed by the government in allegations of terrorism. The seized entities include three commodities-related companies and industrial companies ranging from construction to energy to carpet making. The fate of these companies will depend on the criminal investigation. But, if the terrorist link is established, then they will be sold.

© US Global Investors