Could the Surprising Performance of High-Yield Bonds Continue?

In a surprise to most investors, myself included, high-yield bonds outperformed large-cap stocks for the year to date through November 30, 2016.

Past performance is no guarantee of future results.

Moreover, high-yield bonds outperformed investment-grade debt during the fixed-income sell-off after the presidential election in November. The BofA Merrill Lynch High Yield Master II Index ended November with a -0.39% return, as compared with a -2.37% for the Bloomberg Barclays U.S. Aggregate Bond Index, a broad measure of the investment-grade bond market.

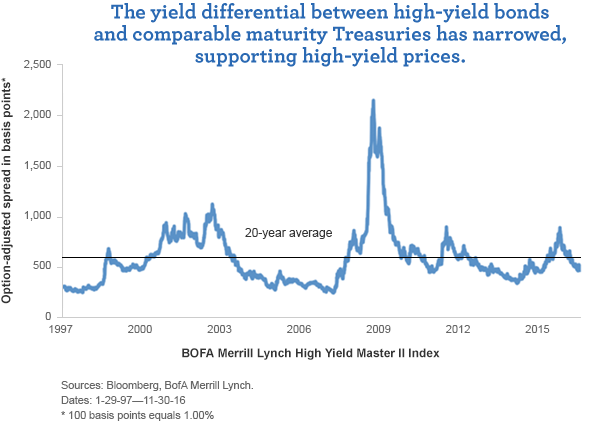

Looking at high-yield performance in another way, spreads—the difference in yield between high-yield bonds and comparable maturity U.S. Treasuries—fell steadily from the beginning of the year. Spreads are now close to their long-term average, pushed lower in part by investors’ continuing hunger for yield in what is still an historically low-yielding environment.

Past performance is no guarantee of future results.

Strong fundamentals could support the income return going forward

The high-yield bond market received support from relatively low default rates. Although the U.S. speculative-grade default rate hit a six-year high of 4.79% in September, according to S&P Global Fixed Income Research, most of the weakness was in the energy sector because of continued low prices for oil and natural gas. Excluding energy and natural gas companies, ratings agency Standard & Poors calculated that the U.S. default rate was a significantly lower 2.44%.

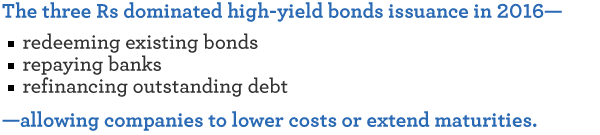

Just as encouraging is how companies used the money they raised in the high-yield bond market. Throughout 2016, what I call the three Rs have dominated—most issuance has been to redeem existing bonds, repay banks, or refinance outstanding debt. This means that companies aren’t increasing debt, but rather lowering costs or extending maturities. Historically, the high-yield bond market has tended to run into problems when a number of bonds near maturity at the same time or when companies suffer a liquidity squeeze because bank lines are cut off. The three Rs could provide future support for the high-yield market, even at these low yield levels.

On the whole, I remain positive on the high-yield market, although I don’t expect the same level of appreciation going forward. I continue to think we’ll see mid-single digit returns—earning the coupons and not losing much to bankruptcies outside of the energy sector. But bond prices are relatively high, with the average price of the market falling just under par (which is 100). I therefore don’t see much of an opportunity for capital appreciation going forward.

Outlook

Macroeconomic conditions seem to put the high yield bond market in a 1% to 2% world. U.S. economic growth ranged between 1% and 2% from the second quarter of 2015 to the second quarter of 2016, and I think it’s possible that growth could remain in that general range in the near term. Likewise, U.S. Treasury rates are falling within the range of 1% of 2%, with the exception of short-term Treasury bills, and the U.S. inflation rate has remained below 2%. Against that backdrop, Federal Reserve (Fed) Chair Janet Yellen telegraphed that the Fed remains data dependent. The Fed is likely wary of raising its key rate too quickly for fear of sparking an adverse market reaction that could bleed into the real economy.

In such an environment, I would be more willing to pick up additional yield by purchasing a longer-duration bond than take on default risk by going down in quality. At the end of the day, generating good returns in the high-yield bond market is about collecting income and protecting principal. Although I don’t foresee a near-term credit crisis, a substantial rise in interest rates might be even more unlikely.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 12-15-16 and are those of Margie Patel, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company. Neither Wells Fargo Funds Management nor Wells Fargo Funds Distributor has fund customer accounts/assets, and neither provides investment advice/recommendations or acts as an investment advice fiduciary to any investor.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management