Generation X's Savings Challenge: The Cost of Family Ties

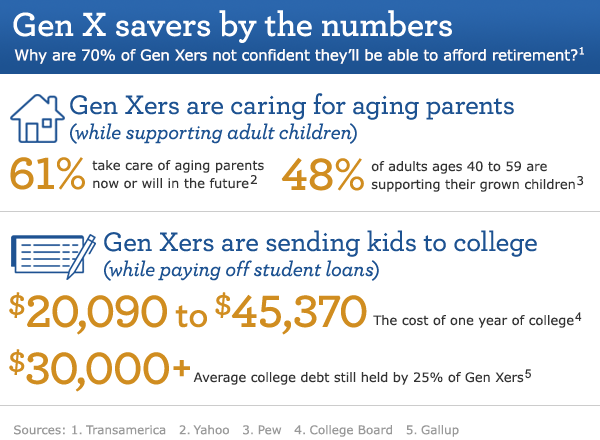

Why is it that 70% of the nation’s 81 million Generation Xers believe they won’t have enough money saved for retirement by age 65, according to the Transamerica Center for Retirement Studies? It’s not for lack of responsibility. When it comes to investing, 77% of Gen X workers are saving for retirement, according to Transamerica’s research. Gen Xers participating in 401(k)s or similar plans contribute a median 7% of their annual pay.

It’s not for lack of progress in the economy, either. As Gen Xers enter their prime earning years, they’ll join younger Boomers as the highest-earning members of the workforce. According to a study from Deloitte:

- Gen Xers will grow their financial assets to $22 trillion and amass a net worth of $37 trillion in 2030.

- Gen Xers will grow their share of America’s net household wealth to about 31% by 2030, up from 14% in 2015.

Given these statistics, one would think Gen Xers should be on track to build reliable nest eggs. So what’s with the lack of confidence in their retirement futures?

If you get to know Gen Xers more closely, you’ll see their generational role in their personal lives presents a roadblock to their retirement plans. Squarely in the middle of the age brackets, Gen Xers are children of Boomers and Traditionalists, and many are parents to Millennials and members of Generation Z. And therein lies the challenge: While Gen Xers want to help their kids and parents, these family ties are costly. The number and scope of people who’ll depend on Gen Xers for financial support will not only grow, but overlap.

With all of these overlapping expenses, what will retirement look like for Gen Xers and how will they prepare? Here are five factors that Gen Xers may want to keep in mind:

- Plan for the retirement that matches reality: Retirement may look different than the classic definition. More than half of Gen Xers plan to work past 65 or not retire at all, reports Transamerica. For some, that’s a necessity. For others, it’s a choice; working provides fulfillment, social interaction, and a paycheck. Either way, the types of investments and allocations investors choose should reflect their plans.

- Know the cost of supporting others along the way: Gen Xers need to be candid about who’ll depend on them, now and in the future, and gauge the true cost of that support. Part of creating a savings plan includes taking into account loved ones’ needs and how much money must be set aside for them now and, in some cases, during retirement. In the context of a portfolio, this could mean finding an appropriate balance between long-term investments and more short-term liquid vehicles.

- Allocate to match financial and family situations: Gen Xers’ investing timelines are smack in the middle of Boomers’ and Millennials’, so asset allocation will likely need to take a more nuanced approach than conservative versus aggressive. Timelines also tend to change with big life events. An unexpected responsibility to a loved one—such as supporting an adult child or aging relative—might mean revisiting how a portfolio is allocated and adjusted for risk tolerance.

- Bring loved ones into the financial mix: Gen Xers are known for being involved in their children’s lives, from volunteering in the classroom to coaching soccer games. So why not invest some time in educating the kids on financial literacy? That goes for grown children, as well—including those who need to repay college debt. Older family members can also help by introducing their Gen X children to the financial professionals who’ve helped them over to the years.

- Get help from someone who gets Gen Xers: Not everyone will truly get a Gen Xer’s affinity for 1980s pop culture, from TV’s “Family Ties” to Hall & Oates’ “Private Eyes.” And not everyone will truly get their financial needs. Gen Xers should seek financial advice from professionals who understand their generation’s views on retirement, financial responsibilities to family, and goals for saving.

Just looking at the numbers, it’s clear that Gen Xers are all about doing the right thing, both in their family lives, their work lives, and in preparing for retirement. If they can find a way to save—while staying on top of the costs of doing right by loved ones—the path to retirement success will become clearer.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 12-2-16 and are those of John Natale, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company. Neither Wells Fargo Funds Management nor Wells Fargo Funds Distributor has fund customer accounts/assets, and neither provides investment advice/recommendations or acts as an investment advice fiduciary to any investor.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management