Holiday Edition: Here Are the Top 6 Frank Talk Posts of 2016

This year has been one for the history books. Donald Trump was elected as the 45th president of the United States, gold had its best quarter in a generation, Warren Buffett decided he likes airlines again and voters in the United Kingdom elected to leave the European Union. Loyal readers of the Investor Alert newsletter and my CEO blog Frank Talk know that we covered it all, too.

As we head into the New Year, I want to share with you the six most popular Frank Talk posts of 2016. Before I do that, however, I think it’s important to note one recurring theme I write about that continues to help our investment team and shareholders better understand the movement in commodities and energy: the purchasing managers’ index (PMI).

Using PMI as a Guide

As I explain in this January Frank Talk, our research has shown that PMI performance is strongly correlated with the movement in commodities and energy three and six months out. PMI forecasts future manufacturing conditions and activity by assessing forward-looking factors such as new orders and production levels.

When a PMI “cross-above” occurs—that is, when the monthly reading crosses above the three-month moving average—it has historically signaled a possible uptrend in crude oil, copper and other commodities. The reverse is also true. When the monthly reading crosses below the three-month moving average, the same commodities and materials have in the past retreated three months later.

In the three months following a “cross-above,” oil rose about 7 percent, 75 percent of the time, based on 10 years’ worth of data. Copper, meanwhile, rose more than 9 percent most of the time.

In November, the JPMorgan Global Manufacturing PMI reading clocked in at 52.1, a 27-month high. This shows that sector expansion has extended for a sixth straight month, which is very encouraging news. Following OPEC's recent production cut, we believe the decision is constructive for energy in the near-term, while a rising PMI is good news for the long term.

We are finally seeing major media outlets and other Wall Street thought leaders recognize the importance of PMI as well.

2016 In Review: The Top 6 Posts

|

Every year I have the opportunity to engage and educate curious investors through my Frank Talk blog, and I am grateful to all of my subscribers who continue to stay engaged with the stories I share. Below are the top six Frank Talk posts of 2016 based on what you found most fascinating. I hope you enjoy this brief recap.

1. Gold Had Its Best Quarter in a Generation. So Where Are the Investors?

In April we were pleased to report that gold was having its best quarter in 30 years—rising 16.5 percent year-to-date at the time. During the first quarter, the yellow metal had its best three-month performance since 1986, mostly on fears of negative interest rates and other global central bank policies.

What we noticed, however, was an anomaly in terms of investor interest. Retail investors were very bullish on bullion but remained bearish on gold stocks.

This was a missed opportunity. Even though gold stocks have retreated since the summer, the NYSE Arca Gold Miners Index is still up 40 percent for the 12-month period. Over the same period, the S&P 500 Index is up only 10 percent, with the Trump rally driving most of it.

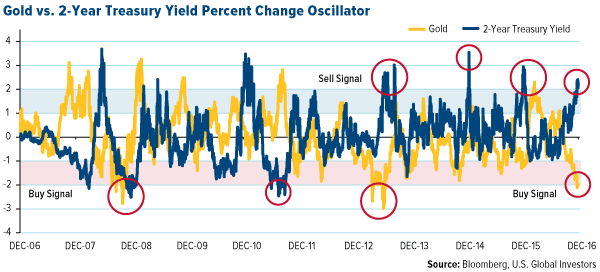

As you can see in the oscillator below, gold is currently down more than two standard deviations. In the past, this was a good time to accumulate, as mean reversion soon followed.

The 2-year Treasury yield, meanwhile, is looking overbought and set to correct, based on our model. The math suggests a nearly 90 percent probability that mean reversion will occur over the next three months, with yields falling and the gold price rising back to its mean.

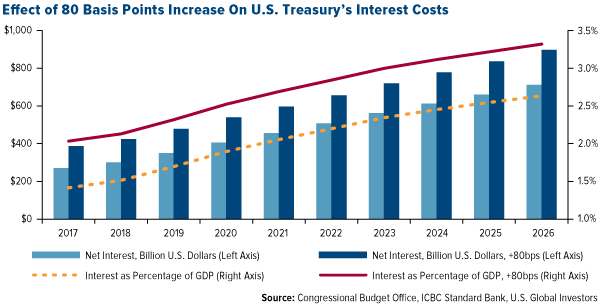

What’s more, ICBC Standard Bank recently highlighted the growing costs of higher yields, which are being overlooked. Net interest payments on the nearly $14 trillion of U.S. debt will amount to around $250 billion this year—or 1.4 percent of U.S. gross domestic product. “If we apply an 80 basis point increase to the net interest forecasts,” the bank writes, “then by 2026 the Treasury would be paying an additional $185 billion in interest annually, and interest will have increased to 3.3 percent of GDP.” This could strengthen the investment case of gold.

2. What Brexit Is All About: Taxation (and Regulation) Without Representation

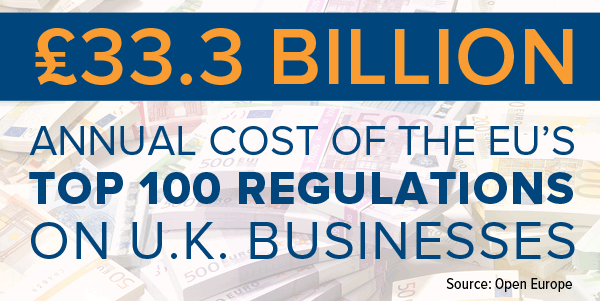

Just three days before U.K. voters went to the polls, I shared my thoughts on why those betting on the “stay” campaign might be surprised to find Eurosceptical Brits prevailing in the Brexit referendum. British citizens voted to exit the EU on June 23, a move that many were not expecting. One of the main grievances of voters was the heavy burden of EU regulations, which are decided by unelected officials in Brussels with little to no cost-benefit analysis.

According to Open Europe, a nonpartisan European policy think tank, the top 100 most expensive EU regulations set the U.K. back an annual 33.3 billion pounds, equivalent to $49 billion.

3. 11 Reasons Why Everyone Wants to Move to Texas

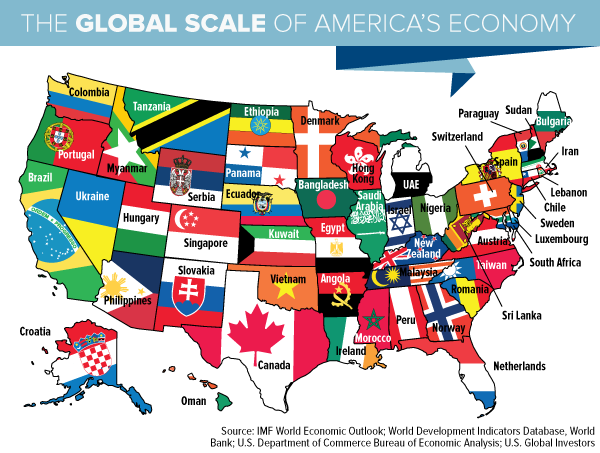

As a “Tex-Can”—born in Canada, living in Texas for the past 26 years—I am so blessed to call Texas my home. Although we are global investors, often focusing on macro-economic issues and government policies, I enjoyed writing this piece highlighting 11 reasons why Texas is truly a remarkable place to live. Did you know if Texas were its own nation, its economy would be about the same size as Canada’s?

Back in October, the Organization of Petroleum Exporting Countries (OPEC) tentatively agreed to a production cut at its meeting in Algiers. Officials announced a “plan” to limit daily production, but I warned investors not to get too excited over OPEC’s decision at the time, since nothing was set in stone. Some OPEC members were already wavering, with Iraq questioning output numbers and Nigeria moving to boost production.

Fast forward to December. For the first time since 2008, OPEC has agreed to a crude oil production cut, renewing hope among producers and investors that prices can begin to recover in earnest after a protracted two-year slump.

5. Use This Tax Strategy Like the Top 1 Percent

Many people might have the impression that the top 1 percent of society—those making over $521,411—deal mainly in exotic investments such as derivatives, fine art and rare French wines. The truth is actually a lot less exciting—they invest in munis. Muni bond income, after all, is entirely exempt from federal and often state and local taxes—a feature that should appeal not just to money-saving, high-net worth individuals but to all investors.

Explore opportunities in muni bond investing!

6. Romania Did This, And Now It's Among the Fastest Growers in Europe

In July I wrote a piece highlighting a country I don’t always discuss—Romania. At the end of last year, and after years of tepid growth, Romania’s government moved to revise its tax code. The country reduced the value added tax (VAT) rate from 24 percent to 20 percent, lowered the income withholding tax rate, nixed a controversial “special construction” tax, simplified deductibles and exempted certain dividends from corporate income tax.

The changes have worked much faster than expected. In the first quarter of 2016, Romania grew 4.3 percent year-over-year, beating the 3.9 percent analysts had expected, and up 1.6 percent from the fourth quarter of 2015.

Keep Calm and Invest On

|

I want to end on one final point. Trump recently responded to the Berlin Christmas Market massacre—the perpetrator of which was just shot dead by police in Italy—saying the event validates his past support of banning Muslims from entering the country and creating a Muslim registry for those already in the U.S.

I’ve said before that people too often take President-elect Trump literally but not seriously, and I think this is one of those cases. I don’t believe he will literally ban all 1.6 billion Muslims from coming into the country, nor does he literally mean it. More likely such a ban would resemble President Jimmy Carter’s temporary cancellation of Iranian visas in response to the hostage crisis, but that’s mere speculation. The issue of Shia-Sunni relations alone is far too complex, with the schism as deep and nuanced as when Protestants broke from the Catholic Church in the 16th century.

But let’s say for a moment that Trump somehow succeeds in implementing a complete ban and creating a registry. These plans would not come cheap. One team of researchers estimated a ban would cost the U.S. economy at least $71 billion a year in lost spending on tourism, education and more. As for a registry, the similar National Security Entry-Exit Registration System (NSEERS)—created in response to 9/11 and dissolved this month by President Barack Obama—cost taxpayers about $10 million a year.

New rules, laws and regulations associated with a ban and registry would also add to our already bloated list of rules, laws and regulations. Trump has said he is committed to axing regulations. I’m all for limiting the regulatory burden, but I wonder what Trump (and incoming Homeland Security secretary John Kelly) would need to cut and streamline to offset the additional rules and costs.

This is the very definition of the law of unexpected consequences, and it’s important to be cognizant of “the negatives of Trump’s anti-globalization ideas,” in the words of billionaire money manager Bill Gross. It’s for this reason that investors should remain diversified, in gold, equities and tax-free municipal bonds.

To all of our readers around the world, I wish you robust health, buckets of wealth and tons of happiness this holiday season!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.46 percent. The S&P 500 Stock Index rose 0.25 percent, while the Nasdaq Composite climbed 0.47 percent. The Russell 2000 small capitalization index gained 0.54 percent this week.

- The Hang Seng Composite lost 2.38 percent this week; while Taiwan was down 2.66 percent and the KOSPI fell 0.31 percent.

- The 10-year Treasury bond yield fell 5 basis points to 2.53 percent.

Domestic Equity Market

Strengths

- Telecommunications was the best performing sector for the week, increasing by 2.40 percent versus an overall increase of 0.25 percent for the S&P 500.

- Micron Technology was the best performing stock for the week, increasing 14.75 percent.

- Disney just became the first movie studio to earn $7 billion at the global box office in a single year. This beats last year's record-breaking year by Universal, which earned $6.89 billion globally thanks to its hits "Jurassic World," "Furious 7," and "Minions."

Weaknesses

- Real estate was the worst performing sector for the week, decreasing by -0.35 percent versus an overall decrease of -0.14 percent for the S&P 500.

- Bed Bath & Beyond was the worst performing stock for the week, falling -13.75 percent.

- Twitter has had a rough week. The stock tumbled 12 percent over the past week after a slew of top executive departures.

Opportunities

- Oprah says she lost 40 pounds on Weight Watchers and the stock soared. Weight Watchers rolled out a new ad campaign featuring claims that media mogul Oprah Winfrey lost 40 pounds on the system. The stock jumped about 11 percent in pre-market trading after the announcement.

- Nike beat on its earnings reports. The sneaker giant earned $0.50 a share, easily beating the $0.43 that analysts had forecast, as sales rose by 8 percent, excluding the currency impact to $8.2 billion.

- Apple is in talks to manufacture in India. The tech giant is in talks with the Indian government to make products locally, a move that Apple hopes will help it gain market share in a country where it holds only 2 percent of smartphone sales, The Wall Street Journal reports.

Threats

- Barron's Magazine couldn't find anyone that thinks the stock market will tank in 2017. Once again, all the analysts were in agreement that "this bull market has legs," as the headline of Vito Racanelli’s article reads. Such one-sider bullish consensus could be a contrarian sign.

- According to BCA, The S&P materials sector is rolling over relative to the broader market after a brief bout of strength. Downside risks remain acute. The strong U.S. dollar will exact a toll on U.S. exporters, particularly if emerging markets and China do not experience acceleration in final demand. Furthermore, BCA’s Cyclical Macro Indicator for the materials sector is hitting new lows, diverging negatively from the share price ratio, underscoring that below-benchmark allocations remain appropriate.

- The sudden surge in the financials and industrials sector has caused a sharp correction in the growth vs. value (G/V) share price ratio. These two sectors are heavily represented in value indices, while technology is a growth heavyweight, underscoring why rising bond yields and hopes for a fiscal stimulus bonanza have triggered such a violent G/V reaction. However, extrapolating the last six weeks to continue over the next six months is dangerous.

The Economy and Bond Market

Strengths

- U.S. GDP growth had its best performance in two years during the third quarter, reports MarketWatch. The economy expanded at a seasonally adjusted 3.5 percent annualized rate, according to data from the Commerce Department, driven by stronger consumer spending.

- Existing home sales rose to their best level since the financial crisis. Sales increased by 0.7 percent at a seasonally adjusted annual rate of 5.61 million, according to the National Association of Realtors. Sales spiked in the Northeast, where slower price growth made it easier for buyers to close deals, according to the NAR. New home sales jumped more than expected. New home sales climbed by 5.2 percent at a seasonally adjusted rate of 592,000 in November, according to the Census Bureau.

- U.S. consumer confidence jumped to a 13-year high. The monthly consumer sentiment index increased to 98.2, the highest level since January 2004, from a preliminary reading of 98.

Weaknesses

- According to CNN Money, there is a “great rotation” taking place in the stock market – stocks are hot, bonds are not. Since the election of Trump, investors have pulled $37 billion from bond funds, with most of that money rotating into stock funds. CNN Money says this “great rotation” could be a major story in 2017.

- December’s flash PMI surveys show a slowing in the pace of economic growth at the end of the year, according to Markit data. Although the flash Markit Composite PMI fell from 54.9 to 53.7, the economy nevertheless moved up another quarter of solid expansion. Markit also reported that hiring and business confidence picked up.

- Personal consumption growth looks to have slowed to around 2 percent in the fourth quarter, down from a pace of 3 percent in the third quarter. The soft November spending data will likely lead to downward revisions for fourth-quarter GDP forecasts.

Opportunities

- Lower U.S. borrowing costs have presented an opportunity for many Canadian companies, reports Bloomberg. Just this year, Canadian companies have issued about $69 billion of debt in U.S. markets, up 12 percent from a year ago. According to the article, the move south is being driven by the lure of lower borrowing costs in America’s larger market, where “the high-quality debt of Canadian companies is being lapped up.”

- Goldman Sachs believes that some areas of the market are better at pricing in Trump’s economic policies than others, reports Bloomberg. “The stunning run in equities post-Trump appears to have looked past the fact that the economy is already running close to full employment,” note analysts Charles Himmelberg and James Weldon. “So far, the (currency) and bond markets appear to have the firmer grip on this reality,” the Goldman pair continues. Perhaps the old markets maxim is correct – bond traders are the smart money.

- Bond yields in the U.S. may fall in the near run after their recent sharp rise, especially as yields are at multi-sigma levels. The odds of a temporary reversal are high.

Threats

- According to BCA, the U.S. Treasury curve is set to bear-steepen further. Core PCE inflation is still running below the 2 percent target and the 5-year/5-year TIPS breakeven inflation rate is at 2 percent, below the 2.4-2.5 percent zone that is consistent with the Fed's inflation target. Hence, there is no rush for the Fed to send a message that it will move aggressively to snuff out incipient inflationary pressures. Instead, the Fed will likely convey that there is no need to be aggressive given the downside risks, and that it will continue to be sensitive to any negative market response to a more restrictive monetary policy. The Fed should react in this manner at least until long-dated TIPS breakevens are firmly anchored in a 2.4-2.5 percent range. BCA thinks it will take at least until the second half of next year for long-dated TIPS breakevens to return to 2.4-2.5 percent, due to the slow uptrend in actual core inflation. As such, they expect the Treasury curve will bear-steepen and TIPS breakevens will continue to rise in the first half of 2017. Once breakevens reach 2.4-2.5 percent, the yield curve will transition from bear-steepening to bear-flattening.

- According to CNBC, homebuilding stocks have been some of the best trades following the U.S. election, surging more than 9 percent, in part, to strong earnings and an improved economic outlook. Despite the strong moves, however, there is a chance that they could lose their positive momentum. Many of the homebuilding stocks have retreated in the past week and a half, the article continues. On CNBC’s “Power Lunch” this week, Oppenheimer technician Ari Wald used a chart of a home construction ETF to explain his concern. “The lower relative highs over the past few years do indicate a more questionable long-term trend,” Wald said.

- A report published by Bank of America Merrill Lynch Global Research on Monday shows that more than 30 percent of high-grade credit investors listed “populism in politics” as their biggest concern for the next 12 months, reports Bloomberg. Only 9 percent named this as their main worry back in October and ahead of the surprise election of Donald Trump. Thirteen percent of the 68 investors polled listed “rising bond yields” as their biggest concern, up from 6 percent in October, according to the report.

Gold Market

This week spot gold closed at $1,133.77, down $1.07 per ounce, or 0.09 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.94 percent. Junior tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index fell 0.96 percent. The U.S. Trade-Weighted Dollar Index finished flat this week with a gain of just 0.05 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Dec-22 |

U.S. GDP Annualized QoQ |

3.3% |

3.5% |

3.2% |

|

Dec-22 |

U.S. Durable Goods Orders |

-4.8% |

-4.6% |

4.8% |

|

Dec-22 |

U.S. Initial Jobless Claims |

260k |

275k |

254k |

|

Dec-23 |

U.S. New Home Sales |

575k |

592k |

563k |

|

Dec-27 |

U.S. Consumer Confidence |

108.5 |

-- |

107.1 |

|

Dec-29 |

H.K. Exports |

-0.2% |

-- |

-1.8% |

|

Dec-29 |

U.S. Initial Jobless Claims |

265k |

-- |

275k |

Strengths

- The best performing precious metal for the week was gold, down just 0.08 percent. Gold is steady in year-end holiday trading, reports UBS, and is trying to form a base around these levels. Physical markets have perked up, helping the market find stability. UBS says there is lack of urgency to jump into the yellow metal right now, and there “is room to be patient and gradually build strategic positions.” Similarly, Comerzbank AG believes gold is finding support from slightly declining bond yields and a marginally weaker U.S. dollar.

- India’s Commerce Ministry has recommended slashing the duty on gold imports from 10 percent to 6 percent, reports Bloomberg, as the higher duty encourages smuggling of the precious metal.

- In other gold-related news from Deutsche Bank, the group assesses the value of the gold “cost curve” when it comes to providing a fair value reference for the metal. Skeptical at first, the bank now recognizes that since 2000, the 90th percentile producer has been a good indicator of the minimum weekly gold price in a given year. “Under these assumptions, the gold price in 2017 would average $1,200 an ounce, with the minimum weekly price falling to $1,060 an ounce.

Weaknesses

- The worst performing precious metal for the week was palladium, down 5.39 percent. Russia reported that palladium output rose 1.7 percent on the year. The market may also start to get nervous about the likelihood that China removes its tax incentive on sales of small-engine cars at the end of the year where palladium is used in the catalytic converter to clean pollutants from the exhaust. Chinese car sales having been booming in recent months at an unsustainable pace so we could see weaker sales in 2017 if there is a change in policy.

- The Bloomberg Dollar Spot Index is heading for its best quarter since 2008, reports Bloomberg, on the back of Donald Trump’s election and the boost in interest rates by the Federal Reserve. Gold is holding near 10-month lows, according to another Bloomberg story and their survey of traders shows they are net bearish for a second week. Holdings in gold-backed ETFs contracted for a twenty-ninth day, as of Thursday, extending the longest run of ETF sales since September 2004. Gold prices have fallen for six straight weeks and hedge funds cut their bets on a rally to the lowest since February.

- In a press release this week, New Gold Inc. announced that Hannes Portmann has been named President of the company. Randall Oliphant will continue in his role as Executive Chairman and Brian Penny will continue as Executive VP and CFO. In a note from JPMorgan this week, the group highlights another company with management changes. After 20 years with Eldorado Gold, CEO Paul Wright has decided to retire, gifting his role to George Burns, the current COO of Goldcorp.

Opportunities

- UBS writes that precious metals could enjoy some upside come January, according to 10 years of historical monthly performance from 2006 to 2015. The data shows that for gold, January offers the best average monthly return at 4.35 percent, with just three negative Januarys in the sample (better than any other month). Similarly for silver, January offers the best average monthly return at 6.01 percent, with just three negative Januarys as well and also better than any other month. Bloomberg also shares an outlook for gold, using five charts to explain why miners are running out of the metal: 1) dwindling discoveries, 2) capex cuts, 3) falling reserves, 4) supply crunch coming and 5) the race for reserves: M&A. Exploration and development companies which can make or have a significant discovery should remain well bid.

- Millennials in China now account for 68 percent of diamond jewelry sales by value, according to research from De Beers SA, the world’s biggest diamond producer. Millennial women, defined by De Beers as those aged from 18 to 34, spent about $26 billion on diamond jewelry in 2015 in the world’s four main markets (acquiring more than any other generation), reports Bloomberg.

- U.S. debt dynamics are set to turn positive for gold in 2017, writes ICBC Standard Bank in a recent note, highlighting that the costs of higher yields are being overlooked. The Congressional Budget Office (CBO) calculates that net interest payments on the around $14 trillion of U.S. debt, will amount to around $250 billion this year (around 1.4 percent of U.S. GDP). “If we apply an 80 basis point increase to the CBO’s net interest forecasts and keep the other variables unchanged, then by 2026 the Treasury would be paying an additional $185 billion in interest annually, and interest will have increased to 3.3 percent of GDP,” the report continues. In the note Tom Kendall stresses the key point is that the financing costs for the U.S. have already jumped, whereas the Trump administration’s policies may or may not have a positive impact on U.S. growth and the effects will be lagged. Thus any disappointments on the growth front combined with higher interest costs and contentious negotiations on raising the debt ceiling in the first quarter, could well result in a more bullish scenario for gold.

Threats

- As David Rosenberg highlights in a piece for The Globe and Mail, back in September Donald Trump declared that markets are in a “big, fat ugly bubble.” Rosenberg believes Trump may be right on this one – this is the most expensive market in 15 years. In fact, if the P/E ratio does its own version of mean-regression, then the equity market is discounting 33 percent earnings growth in 2017. “Look, if the market was even discounting 10 to 15 percent earnings per share growth, there is some moderate upside,” he continues. “But Mr. Market is priced for a one-in-20 event that only occurs at the early stages of the cycle, not heading into year number eight.”

- With equity markets in record territory, Drew Mason from St. Joseph Partners also notes what this has done for the bond market (losses approaching $2 trillion since the election). Mason writes, “It appears likely that at some point, bondholders will begin to increase allocations to gold and silver.” California Public Employees’ Retirement System announced it is looking to pair back its global equity and private equity exposure by 5 percentage points in favor of a larger allocation to real assets, inflation and liquidity asset classes.

- While total gold imports into India were up 28 percent in November from October, much of the flow likely reflects the immediate reaction to the demonetization of 1,000 and 500 rupee notes, reports UBS, whereby consumers turned to gold amid policy uncertainty. UBS thinks gold purchases could be affected by the transition from cash to electronic/digital payment systems. It seems as if you have wealth outside of a government approved account, it is seen as “dirty money” and is confiscated. This type of policy change could put downward pressure on gold demand. A headline from the Economic Times sums up the situation quite well: “Gold’s global safety net fails as India demand dries up on cash ban.”

Energy and Natural Resources Market

Strengths

- Natural gas prices rose 7.7 percent this week following a major inventory drawdown as cold weather swept the country last week. The weekly storage drawdown of 209 billion cubic feet (BCF) marks the tenth largest weekly withdrawal in the past six years. Further to that, the weekly draw was more than twice the five-year average for late December draws (101 BCF), thus giving natural gas prices a head start to the winter season.

- The best performing sector for the week was the Alerian MLP Index. The index rose 3.8 percent as the sector has entered onto watch lists for major infrastructure investors. Blackstone Private-equity Group LP is currently in talks to purchase assets owned by Energy Transfer Partners LP, in a move that suggests global investors believe Trump's deregulation plans may unleash growth in the sector.

- OCI N.V., a producer of fertilizers and industrial chemicals in the Netherlands, was the best performing stock this week finishing up 9.7 percent. The stock rose on the back of rallying urea fertilizer prices this week.

Weaknesses

- Copper dropped to its lowest level in one month on the back of a major inventory build. The London Metals Exchange surprised metal speculators by reporting that copper inventories had the biggest one day build in over 15 years, putting a halt to copper’s rally.

- The worst performing sector this week was the BI Global Coal Producers Top Competitive Peers Index. The index fell 6.9 percent on the continuation of met coal prices continuing to fall downwards.

- The worst performing stock for the week was Severstal PJSC, the largest steel producer in Russia. The company fell 6.3 percent on the back of falling steel prices.

Opportunities

- Commodity prices may continue to rally as supply and demand dynamics are tightening, according to Citi. With 2016 almost in the books, commodities are posting their best annual performance in over five years. The trend should continue in 2017 says Citigroup, a bank which has been notoriously bearish on commodities, by stating that “there is absolutely no doubt that commodity markets are at a turning point.”

- The Brent forward curve is signaling that oil storage tanks will start emptying the second half of 2017, according to oil traders surveyed by Reuters this week. As crude oil trades range bound and overhang continues to exist in inventories, higher demand in the future is slowly starting to emerge where oil fundamentals may turn bullish in late 2017.

- U.S. Gulf Coast refiners cash in on rising fuel demand in Mexico. The neighboring county has seen major increases in fuel imports over the past 27 consecutive quarters, as a result of increased gasoline demand and the failure to expand its domestic refining capacity.

Threats

- China may fall short of its 6.5 percent in economic growth objective, according to president Xi Jinping. Xi stated that the country doesn’t need to meet its objective if doing so will create too much systematic risk and jeopardize its long-term growth prospects. In 2015 policy makers pledged an annual growth rate of at least 6.5 percent through 2020. Falling short of their growth objectives will have negative ramifications for industrial metal demand, a negative read-through for base metals.

- Commodity prices may be susceptible to major swings in 2017 as commodity exporting nations prepare for the potential of protectionist measures in the U.S. Following the victory of President-elect Donald Trump, markets have reacted to a stronger U.S. dollar, and are making preparations for potential protectionist policies against their imports. Some economic commentators have warned that a wave of protectionist measures may sink the world into a global recession, with negative implications for commodity prices.

- Greater volatility is expected to affect agricultural commodities. Argentina, the world’s third largest producer of soybeans, has had a very tough time planting crops over the past few weeks as the country has faced severe rainfall. Rain is also affecting other major agricultural producers in South America making harvest predictions difficult.

China Region

Strengths

- Taiwan’s November period year-over-year export orders rose 7.0 percent, well ahead of estimates for a gain of only 5.0 percent.

- Singapore’s year-over-year industrial production came in up 11.9 percent, handily beating estimates for a mere 1.6 percent print and marking its highest level in more than two years.

- South Korea’s KOSPI Index barely nudged out the Shanghai Composite Index for the best relative performer for the week (although all regional indices finished down for the last five days). The KOSPI finished out the week down only 31 basis points, while Shanghai finished down 41 basis points.

Weaknesses

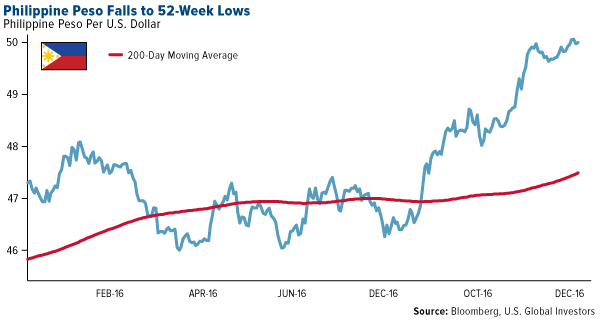

- The Philippine peso fell (climbed, in U.S. dollar terms) to 52-week lows (highs)—just over 50—this week ahead of the country’s central bank announcement, although after the central bank held interest rates at 3 percent the peso strengthened on Friday to about 49.70. The country’s PCOMP Index (the week’s worst regional performer) made no such recovery and dropped to multi-month lows on Friday, finishing down a little over 4 percent for the week.

- All sectors in the HSCI Index finished in the red for the week; telecommunications held up the best (down only 1.10 percent) while energy (down 3.75 percent) performed worst in that timeframe.

- The Hang Seng Index fell to correction territory on Friday.

Opportunities

- China’s level of copper imports in November rose to the highest level in five months, jumping 46 percent from the October reading.

- According to Bloomberg News Energy Finance, India is set to add more than 10 gigawatts of renewable energy capacity in the year 2017.

- It is just over a month before the start of the Lunar New Year holidays, which may bring some positive sentiment and seasonality to the coming weeks.

Threats

- Several South Korean insurance companies’ shares tumbled this week after Samsung Fire & Marine Insurance announced an auto premium rate cut of 2.4 percent, creating sympathy selling and expectations of lower rates from other insurers.

- President Xi Jingping announced that he remains comfortable with a GDP growth rate averaging below 6.5 percent (that is, below the level to which policy makers had previously committed through 2020). While a positive, perhaps, if unshackling policy makers from taking unnecessary risks, explicit lower growth expectations may also have adverse effects in some markets.

- Yuan weakness and capital outflows from China remain a threat.

Emerging Europe

Strengths

- Poland was the best performing country this week. Strong economic data supported stocks trading on the Warsaw stock exchange despite increasing political noise in the country. Industrial output, construction output and retails sales improved on a year-over-year basis. The Producer Price Index increased 1.7 percent in November from a year ago, suggesting a long awaited pickup in inflation.

- The Russian ruble was the best performing currency this week. Brent crude oil is little changed this week, but the ruble most likely is supported by year-end tax payments. Export-focused companies are converting part of their dollar and euro revenue into local currency to pay year-end taxes.

- The utilities sector was the best performer among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week. The MSCI Russia Index has gained more than 50 percent year-to-date. Investors may be taking some profits before year end.

- The Romanian leu was the worst performing currency this week. Romania’s Social Democrats, who won this month’s general election, picked former Regional Development Minister Sevil Shhaideh for the country’s premier. Social Democrats are forming their government again, after premier Victor Ponta stepped down in November 2015.

- The consumer staples sector was the worst performing sector among eastern European markets this week.

Opportunities

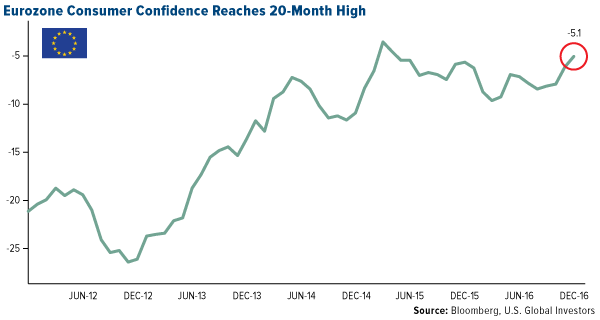

- Confidence in the eurozone increased by 1.1 points to reach -5.1 for December, according to flash estimates from the European Commission. A measure below zero indicates net negative sentiment, but the score is well above the long-term average. Howard Archer, chief U.K. and European economist at HIS Markit, said: “This reinforces hopes that the eurozone will have seen some pick-up in GDP growth in the fourth quarter and is set to see a decent start in 2017.”

- Total labor costs in the eurozone were up 1.5 percent year-over-year in the third quarter, with wages and salaries increasing 1.6 percent. Although slightly weaker than first quarter, the figures were an improvement on the 1 percent growth seen in the second quarter. The biggest increases were in Central and Eastern Europe, with Romania, the Czech Republic and Bulgaria as the biggest risers.

- The difference between bond yields in the U.S. and Germany is at its largest in more than a quarter of a century. U.S. government debt yields 2.56 percent, against a 0.27 percent yield for comparable German bonds. According to some analysts, the large gap in yields will continue to drive the euro down. For the eurozone, a weaker currency will likely be welcomed as it makes exports more competitive at a time when inflation is not a worry.

Threats

- It has been a week of death and chaos overseas in Europe. Russia’s ambassador to Turkey was assassinated at an Ankara’s art gallery. In Zurich a man opened fire on people praying in an Islamic center. And in Berlin, a truck drove into a crowded Christmas market. Acts of terror across European countries have intensified.

- The United States updated and tightened its sanctions against Russia on Tuesday as part of its efforts to punish the country for its 2014 annexation of Crimea, just a month before President-elect Donald Trump brings a more Russia-friendly foreign policy to the White House. Last week, the eurozone extended its sanctions on Russia for the next six months.

- Poland is under political stress after protests over media restrictions imposed by the country’s right-wing government carried on for several days. The current ruling party, Law & Justice, proposed reducing journalists’ access to parliament from January 1, creating a wave of anti-government protests in major cities. European Commission Vice President, Frans Timmermanscomes, criticized the Polish government for new problems relating to the rule of law, giving two months to resolve the issues.

© US Global Investors