In the early decades of the 19th century, a new cultural and philosophical movement emerged that embodies all that makes America great. Led chiefly by Ralph Waldo Emerson and Henry David Thoreau, American transcendentalism praises the purity of the individual and stresses the importance of self-reliance.

“The great man is he who in the midst of the crowd keeps with perfect sweetness the independence of solitude,” Emerson wrote.

I recognized these uniquely American values early on when I made the move from Canada to Texas. Individualism, non-linear thinking, a rebellious streak—without them, the U.S. might not have been the birthplace of world-changing innovations such as the locomotive, automobile, airplane and microprocessor.

Today we have these same values to thank for the creation of Facebook, Amazon, Google and other tech giants, without which we can hardly imagine our lives now.

They’ve also helped make many people fabulously wealthy. Of the 400 Americans on Forbes’ wealthiest list, about two thirds can be labeled as self-made, including Jan Koum, a Ukrainian immigrant raised on food stamps who became an overnight billionaire when he sold his instant messaging app, WhatsApp, to Facebook in 2014.

Other countries have little choice but to emulate America’s economic and cultural biosphere that allows such innovations to flourish. In an effort to become a leader in autonomous driving, Germany-based Volkswagen is currently in the process of recruiting as many as 1,000 experts in artificial intelligence, virtual reality and big data—many of whom hail from Silicon Valley and other American tech hubs. According to Volkswagen Chief Information Officer Dr. Martin Hoffman, research teams in Berlin and Munich “work the Silicon Valley way. We have brought the Valley to Volkswagen… with over 20 experts from San Francisco and Boulder, Colorado.”

|

As I’ve pointed out many times before, the reason Silicon Valley must be imported from the U.S.—instead of built in-house—is largely because the European Union’s crushing regulations and policies of envy stand in the way of ingenuity and entrepreneurship. Their best brains, therefore, end up in the U.S., the land of opportunity.

“If anybody believes Europeans will create a better business environment than Americans, they’re completely dreaming,” Mark Tluszvz, CEO of a Luxembourg-based venture capitalist firm, told the Financial Times in 2015. “We don’t have this in our culture."

It’s essential we don’t lose it in our culture, either. Many U.S. lawmakers and bureaucrats, however, seem intent on significantly weakening our ability to innovate and stay competitive. The more rules and layers of regulations that businesses must contend with, the more the U.S. will resemble Brussels.

We can’t allow that to happen.

“Any fool can make a rule, and every fool will mind it,” Thoreau sagely wrote nearly 200 years ago.

Although “fool” might not be the word I would use, it must be recognized that the U.S. became the innovative powerhouse it is today not because of rules but because of the values of individualism espoused by the transcendentalists all those years ago.

Trump Pushing Back on New Rules

I’m convinced this is one of the key reasons why U.S. voters elected Donald Trump, despite his rough edges. Trump has pledged to streamline or altogether eliminate many financial regulations that have stymied the creation of capital over the years, from Dodd-Frank Wall Street Reform to the Sarbanes-Oxley Act (SOX). We add can to this list the Department of Labor’s (DOL) new Fiduciary Rule.

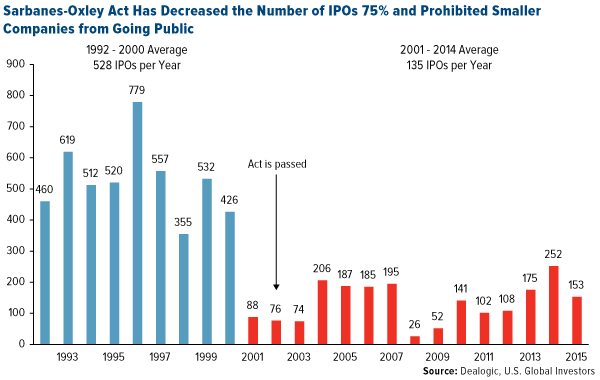

Signed by President George W. Bush, SOX seeks to prevent massive corporate fraud such as we saw from Enron and WorldCom in the early 2000s. Although a noble mission, SOX has had the unintended consequence of barring small to medium public companies from getting ahead. It’s also prevented retail investors from getting in on the ground floor. Because the requisite internal control procedures are so costly and cumbersome—necessitating additional compliance and accounting positions, not to mention hundreds of hours spent on compliance-driven tasks—smaller firms are inevitably at a disadvantage.

As a result, many small to mid-sized companies are delaying going public, or avoiding it altogether, to escape the regulatory burden. Before SOX, there were an average 528 IPOs a year. Since it was enacted, that number has fallen to 135, a decline of nearly 75 percent.

As for Dodd-Frank, signed by President Barack Obama, market experts ranging from Warren Buffett to Alan Greenspan support its repeal, with Buffett saying the legislation “has taken away the Federal Reserve’s ability to act in a crisis.” Many banks have done away with free checking, giving lower-income customers fewer and fewer banking options.

Joining the chorus in calling for deregulation is billionaire CEO of Koch Industries, Charles Koch. Speaking to ABC’s “This Week” back in April, he called our political and economic system rigged “in favor of [multibillion-dollar] companies like ours,” and criticized “corporate welfare that benefits established companies and makes it difficult for somebody to get started.”

Protecting the Little Guy?

These rulings, among others, have been detrimental to the formation of capital, especially for the little guy, whom they purport to be protecting. But it doesn’t exactly help or protect the little guy if his investment, banking and business options are dramatically limited. See this chart I shared with you back in July, which shows how retail investors have been locked out of participating in the best-performing asset classes.

Or consider the DOL’s new Fiduciary Rule. When it goes into effect in April 2017, it will inevitably limit the number of investment products available to retail investors. The ruling states that all retirement planners, advisors and broker-dealers must now “act in the best interests of clients” and charge only “reasonable” fees. This all sounds fine, but what’s naturally going to happen is financial professionals—in an effort to remain compliant with the rule—will recommend only the least expensive products, regardless of whether they’re a good fit. Many mutual funds—which might be better performing but have higher expenses than other investment vehicles—will fall off of brokerage firms’ platforms.

It would be like the DOL telling consumers they can only shop at Walmart and buy their coffee from Dunkin’ Donuts because anything more expensive—Target or Starbucks, say—is “riskier,” even though they’re of higher quality.

This type of anti-capitalist mindset is expected in the EU, not the U.S. Trump’s win certainly puts a target on the DOL’s Fiduciary Rule, which he has pledged to repeal, but like Sarbanes-Oxley and Dodd-Frank, we’ll have to wait and see.

And Yet, Business Owners Are Optimistic

Whether Trump can succeed at reversing some of these rules remains to be seen. If you remember, Obama failed to roll back—and, in fact, he extended—Bush-era legislation he strongly campaigned against, such as the Patriot Act and Bush tax cuts. The same might very well happen under Trump. Even Carl Icahn—whom Trump named as his special advisor on deregulation—has commented that Dodd-Frank is needed.

But Trump is a pragmatist, as Obama himself described him. “He is coming into this office with fewer set-hard-and-fast policy prescriptions than other presidents,” Obama said.

Indeed, Trump isn’t guided by ideology from the religious right, as Bush was, or the socialist left, as Obama was. Remember, he long identified himself as a Democrat and has supported Democratic candidates (including Hillary Clinton). So I think that, after 16 years of Bush and Obama, the pendulum is finally swinging back to the center. The question is: Can Trump make it work?

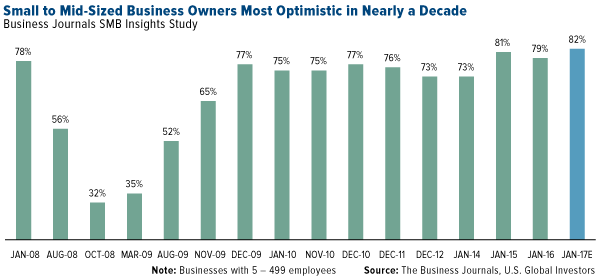

Many small to mid-sized business owners seem to believe he can. In a Business Journals survey taken the day after the election, 82 percent of businesses said they felt confident their prospects would improve over the next 12 months. That’s the highest reading in nearly a decade.

How Markets Are Betting

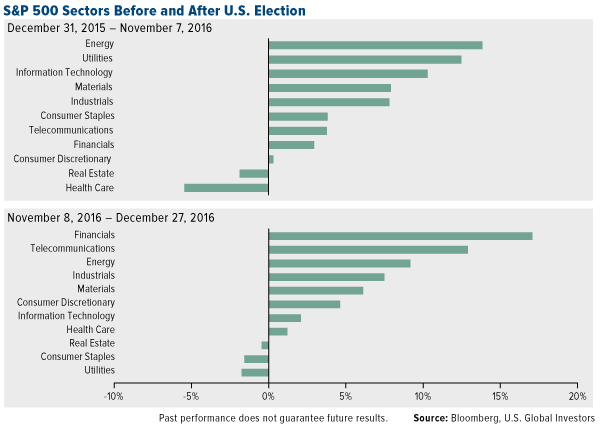

As I’ve pointed out before, investors seem to be betting that, despite the uphill battle ahead, Trump can deliver on financial deregulation. Below, the chart shows sector performance before Trump’s election compared with performance since the election. As you can see, financials jumped seven places to become the top-performing sector. What’s more, health care turned positive, suggesting investors are confident Trump and the Republican-controlled Congress can dismantle Obamacare.

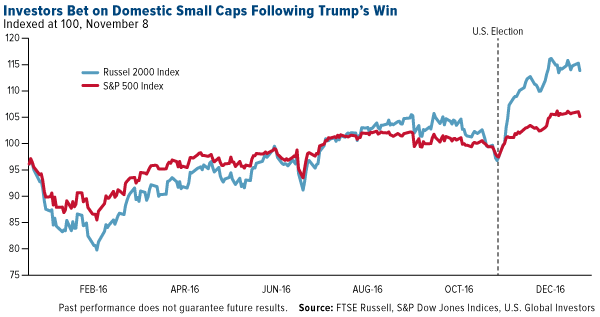

Small-cap stocks, as measured by the Russell 2000 Index, are also way up on bets that Trump’s protectionist policies will benefit domestics with limited exposure to foreign markets, more so than multinational blue-chip stocks.

It might be too soon to tell, but I expect these trends to carry on into 2017.

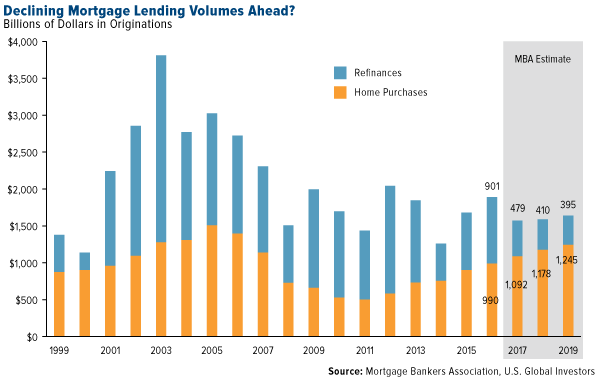

Rising Rates Ahead in 2017

With economic conditions and expectations improving, especially since the election, it’s very likely the Federal Reserve will continue to tighten throughout 2017. Rate hikes will be limited, but 3 percent mortgage rates are probably a thing of the past.

Lenders are already slashing their refinance-volume expectations for 2017 and beyond, according to a mortgage lender sentiment survey conducted in December by Fannie Mae.

In addition, Kroll Bond Rating Agency (KBRA) believes we’ve likely seen peak lending: “While 2016 has been an excellent year for the U.S. mortgage industry, with almost $2 trillion in new loan originations, we believe that this year is also likely to be the peak in terms of lending volumes for years to come.”

As I’ve pointed out several times before, when interest rates are on the rise, short-term municipal bonds are the place to be, since they’re less sensitive to rate increases than longer-term bonds, whose maturities are further out.

I want to wish all of my loyal readers, investors and shareholders a most Happy New Year! As we begin a new American chapter in 2017, complete with a new series of challenges both big and small, remember to hold fast to H.O.P.E.—Have Only Positive Expectations!

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.86 percent. The S&P 500 Stock Index fell 1.10 percent, while the Nasdaq Composite fell 1.46 percent. The Russell 2000 small capitalization index lost 1.05 percent this week.

- The Hang Seng Composite gained 2.03 percent this week, while Taiwan was up 1.93percent and the KOSPI fell 0.46 percent.

- The 10-year Treasury bond yield fell 9 basis points to 2.45 percent.

Domestic Equity Market

Strengths

- Real estate was the best performing sector for the week, appreciating 1.17 percent versus an overall decrease of 1.10 percent for the S&P 500 Index.

- Newmont Mining was the best performing stock for the week, increasing 8.37 percent. Some think this move was attributed to short covering since the total number of shares sold short continues to decline.

- The Dow Jones Industrial Average closed just below 20,000, but the Russell 2000 small cap index stole the show with a 19.48 percent return for the year.

Weaknesses

- Information technology was the worst performing sector for the week, falling by 1.45percent versus an overall decrease of 1.10 percent for the S&P 500.

- Arconic Inc., a global provider of lightweight multi-material solutions, was the worst performing stock of the week, declining 7.62 percent. The company is down about 1.2 percent since it was spun off from Alcoa early last month.

- Disney was down 1.04 percent for the week, even after box office sales topped $650,000,000 worldwide for “Rogue One: A Star Wars Story.” I hear Disney investors saying, “Help me Obi Wan.”

Opportunities

- Buybacks are back on! Earlier in the week Goldman Sachs reported corporate buybacks had a HUGE rebound, jumping 71 percent compared to the same period last year.

- Not only did the market trade at all-time highs, but so did the value of most houses. The Case-Shiller 20-City composite home price index came in up 5.5 percent year-over-year.

- With good news like we just read it’s no wonder Consumer Confidence came in higher than expected at 113.7. This is the strongest reading since 2001.

Threats

- While a strong dollar is optimistic for U.S. consumers it comes at a price to global companies that derive revenue for sources outside of the United States. If the dollar continues the upward ascent we can see future sales and revenue forecasts reduced.

- Home prices continue to outpace gains in wages and personal income. If this continues, home prices will soon become out of reach. Additionally, house flipping is making a comeback. The Wall Street Journal reported investors who flipped a home reached the highest level since 2007.

- Initial jobless claims were reported on Thursday, in line with expectations. Some might consider this a threat since good reports reinforces the Fed’s willingness to increase the federal funds rate.

The Economy and Bond Market

Strengths

- Home prices went up sharply in October. The S&P Case-Shiller 20-city composite home price index posted a 0.6 percent month-over-month rise in October, better than the prior month’s 0.4 percent rise. The index was up 5.1 percent year-over-year, an increase from September’s 5.0 percent annual rise.

- The Richmond and Dallas Fed Manufacturing Indexes came in stronger than expected. Richmond was 8 versus expectations of 5 while Dallas was 15.5 versus expectations of 10.2.

- Consumer confidence climbed in December to the highest level since August 2001, as Americans were more upbeat about the outlook than at any time in the last 13 years, according to a report Tuesday from the New York-based Conference Board. The Conference Board Confidence Index increased to 113.7, better than November’s 109.4 and consensus of 108.2.

Weaknesses

- The Wall Street Journal is the latest to take note of the potential pressure the rising dollar could place on the economy. A recent article notes that while the dollar’s strong appreciation over the past two years is a sign of rising optimism for the U.S. economy, it also promises to hit U.S. manufacturers reliant on sales in overseas markets. It adds that many companies have started to dial back forecasts as a result of the appreciation. It also noted that some dealers of Harley Davidson and Caterpillar equipment said they are bracing for Japanese rivals to capitalize on the yen’s weakness and undercut them on price.

- Pending home sales declined 2.5 percent (forecast was for 0.5 percent gain) after rising 0.1 percent the prior month. The drop in contract signings was the first in three months and shows the impact of a surge in borrowing costs. A further increase in mortgage costs risks reducing affordability as gains in property values have been outpacing income growth.

- American consumer comfort, according to the Bloomberg Consumer Comfort Index, dropped to 46 in the period ended December 25, the first retreat in five weeks, from 46.7. However this measure is closing in on its best year since before the last recession.

Opportunities

- Global investors' equity holdings rose to six-month highs in December on bets that U.S. President-elect Donald Trump's promised fiscal splurge would spur higher growth and inflation, a Reuter’s monthly poll showed on Thursday. Trump's plans to cut taxes and boost spending have sent Wall Street to record highs in December as investors pile into everything from banks, to energy and materials and other infrastructure-related names. If his proposed infrastructure spending, fiscal easing and tax reforms are effectively implemented, the U.S. reflation stimulus will likely strengthen GDP growth, inflation and earnings growth.

- Bonds are rallying. U.S. 10-year yields continue to fall. The yield peaked in mid-December near 2.64 percent. With Friday’s two basis point decline, it is at 2.45 percent, which is below the 20-day moving average for the first time since November 9, the day after the U.S. election.

- According Jennifer Vail, head of fixed income research at U.S. Bank Wealth Management, high-yield bonds will outperform in 2017 as investors seek coupons high enough to offset price declines from the Fed’s anticipated rate hikes.

Threats

- After six straight years of growing U.S. investment-grade corporate-debt sales, bankers and investors are pegging 2017 as the year the frenzy finally fades. The new year has several hurdles in place already. For one, interest rates have risen to two-year highs, making borrowing more costly, and the pipeline for new-acquisition financing is smaller than 2016’s. Uncertainty around potential tax reform and trade wars in a Trump administration may also sideline more issuers.

- A drop in U.S. exports last month pushed the country's trade deficit in goods higher. According Evercore ISI, the widening trade gap through November will probably reduce fourth-quarter GDP by 0.3 percent, cutting their prior estimate of +2.5 percent to +2.2 percent.

- Manufacturing conditions in the Midwest softened in December, according to the latest Chicago PMI report (54.6 vs. expectation of 56.8), but the region still remains in an expansionary mode. It is not quite clear whether such elevated levels in factory-related sentiment will persist given the two battering headwinds of an appreciating U.S. dollar and a rising interest rate environment.

Gold Market

This week spot gold closed at $1,152.27, up $18.32 per ounce, or 1.62 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 8.38 percent. Junior tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index climbed 4.70 percent. The U.S. Trade-Weighted Dollar Index finished the week with a drop of 0.58 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Dec-27 |

U.S. Consumer Confidence |

109.0 |

113.7 |

109.4 |

|

Dec-29 |

H.K. Exports |

-1.0% |

8.1% |

-1.8% |

|

Dec-29 |

U.S. Initial Jobless Claims |

265k |

265k |

275k |

|

Jan-2 |

Caixin China PMI Mfg |

50.9 |

-- |

50.9 |

|

Jan-3 |

Germany CPI YoY |

1.4% |

-- |

0.8% |

|

Jan-3 |

U.S. ISM Manufacturing |

53.7 |

-- |

53.2 |

|

Jan-4 |

Eurozone CPI YoY |

0.8% |

-- |

0.8% |

|

Jan-5 |

U.S. ADP Employment Change |

170k |

-- |

216k |

|

Jan-5 |

U.S. Initial Jobless Claims |

263k |

-- |

265k |

|

Jan-6 |

U.S. Change in Nonfarm Payrolls |

175k |

-- |

178k |

|

Jan-6 |

U.S. Durable Goods Orders |

-- |

-- |

-4.6% |

Strengths

- The best performing precious metal for the week was palladium with a gain of 3.32 percent. HSBC noted they expect the rise of palladium prices to continue into 2017 with limited supply growth and steady auto demand.

- According to a Bloomberg survey late this week, gold traders and analysts are bullish on gold for the first time in three weeks. The change in sentiment was reflected in holdings in gold-backed ETFs, which rose 0.5 metric tons to 1,778.3 as of Thursday. This rise broke the 33-day drop in gold assets held in ETFs, which was the longest-running drop since 2004.

- Precious metals are enjoying a year-end rally, with gold rising above $1,150 per ounce earlier in week and finishing above that level by Friday, snapping a three year losing streak with an 8.56 percent gain. As shown in the chart above, gold prices track very closely with real interest rates. What turned out to be a test of wills a couple days after the Fed interest rate hike in December, real rates jumped to 71 basis points, yet gold held on at $1,130 support, and real rates finally backed off below 50 basis points by year end. At the start of the year, 71 basis points of positive yield had gold pinned down almost $90 lower

Weaknesses

- The worst performing precious metal for the week was platinum, with a gain of only 1.15 percent as it rallied along with the precious metal group going into yearend, possibly on short covering.

- China’s gold imports in November were the lowest all year. Net purchases were about 40.6 metric tons, down from 60.4 tons in October and 66.8 tons in November of last year. Depreciation of the renminbi currency has made imports more expensive.

- The impact of demonetization in India is still being felt in gold demand. Gold imports in India for 2016 were much lower than the annual average of 1,000 metric tons, with just over 600 tons this year. Analysts anticipate that demand will be similarly low in 2017. In Dubai, the gold market has noted a marked absence of Indian buyers since the demonetization. Typically, the Dubai Gold Souq market would process about 15 percent of sales with Indian rupee transactions.

Opportunities

- Political surprises and uncertainty with Donald Trump’s election are reviving gold’s “safe haven” attraction for investors. Mark O’Byrne, a director at broker GoldCore Ltd. commented, “140 characters of unfiltered Trump is likely to create tensions with America’s largest trading partners. Markets that are already shaken by the fallout from Brexit, the coming elections in Europe and indeed the increasing specter of cyber warfare could again see a safe-haven bid.” Indeed, Trump’s choice for the Office of Budget and Management, Mick Mulvaney, owns significant amounts of precious metals and gold mining stocks, according to financial disclosures. Mulvaney has been known to be critical of the Federal Reserve.

- Barry Rehfelt noted in an article published by TheStreet that the stock market rally could provide an incentive for investors to look to gold. Although there have been recent gains in the stock market, there is a threat of a trade war with China, which would impact the stock market. Rehfelt reminds readers that gold does well in uncertain times. In addition, UBS anticipates gold will average $1,350 per ounce in 2017, noting that the current weaker environment could be a good buying opportunity.

- Commerzbank has expressed belief that gold bullion will be positive in 2017, also related to the upcoming Trump presidency and the U.K.’s talks to leave the European Union. Gold has had its longest run of gains this week, since early November just before the election. Ironically, most of the media is citing the surprise Trump win as the reason gold fell but the U.S. election results came out as India’s Prime Minister Modi announced his surprise crackdown on tax evasion with demonetization of the Indian economy. The unpredictability of President Elect Trump may turn out to be just what investors thought: good for gold.

Threats

- The Shanghai Gold Exchange, the world’s biggest physical gold exchange, is imposing limits on the size of transactions that can be made, starting on January 1. The maximum transaction will be 500 kg, half of the current limit of 1,000 kg. Analysts say the move is targeted at institutional investors. However, critics note that the size of transactions won’t limit the amount of gold traded, as larger amounts can be broken up into multiple trades. It is doubtful the smaller transaction size limit will lower the volatility of the Shanghai gold market.

- Consumer inflation expectations have fallen to a 143 month low, according to the Gavekal Capital Blog. Investors may be expecting higher inflation next year, but consumers expect inflation to have a more nascent effect in 2017. Expectations have round tripped back to pre-2000 levels.

- Australian miner Kingsgate has been ordered by Thailand’s government to shut down operation of its Chatree mine. Thailand’s prime minister has warned the mining company that it would be a “waste of time and have no benefit” to sue the government. This is likely yet another instance of government seizure of a natural resource for its own benefit similar to Venezuela’s attempt to expropriate several of its gold deposits from the nondomestic companies that made the original discovery.

Energy and Natural Resources Market

Strengths

- Aluminum, zinc, and nickel inventories officially all fell for 2016, bucking the longer term trend of increasing inventories according to research that was released by Macquarie Bank this week. This is the first positive year since 2012 for these commodities. Given that commodities follow multiyear cycles, the upward movement in prices this year suggests that we could have a number of positive years to come following the weakness over the past three years.

- Iron ore was the best performing commodity for 2016. After a tumultuous couple of years, the commodity rose 77 percent this year on the back of bargain hunting from the distressed values earlier this year. The primary driver for the commodities appreciation was a rebound in Chinese PMI and an increase in home sales, both of which drive steel production.

- The best performing sector for the year was the S&P/TSX Composite Diversified Metals & Mining Sub Industry Index. The index rallied a whopping 130.5 percent this year due to rallying metals prices this year in both the industrial and base metals complex. The rebound in coal and base metals led the index higher than expected as increased Chinese housing demand helped raise prospects for miners globally.

Weaknesses

- Corn was the worst performing commodity for 2016, dropping 2.5 percent. The commodity has had a rough time since 2014 with prices in free fall due to oversupply. Although 2016 marks an improvement from the commodity’s original 10 percent drop in 2014, medium term fundamentals suggest the oversupply condition may continue and do not support a rally just yet.

- The worst performing sector for this year was the S&P Super Composite Oil & Gas Refining & Marketing Sub Industry Index. The index fell 1 percent this year on the back of oil’s strong rebound throughout 2016. Additionally, the index was hit hard by higher environmental compliance led by rallying RIN prices (RINs are serial numbers assigned to each batch of oil to track production required by federal law), which significantly impaired the profitability of the sector.

- U.S. gasoline consumption fell for the fourth straight month in a row. Consumption fell to 9.095 million barrels per day in October from 9.492 in September, according to the Energy Information Administration (EIA) which releases a report highlighting monthly petroleum supply. It is worthwhile to note that demand is at its lowest level since January of 2016, a negative read-through for oil demand and the refining sector.

Opportunities

- Natural gas prices continue to surge as cold weather depletes inventories in the U.S. Supply in the market has tightened at a much faster pace than many analysts originally forecasted going into this winter. As the market continues to improve, natural gas drillers have added more than 30 percent to their rig count, something they have not done in years, a bullish sign for natural gas.

- Gold rallied this week as investors exit their bearish bets. Since the U.S. election, gold has been beaten down hard as investor sentiment shifted gears into potential growth prospects that are in the pipeline for fiscal 2017, as President-elect Trump begins his term. However, investors are beginning to worry about the prospects of inflation as the Federal Reserve begins their hiking cycle which is positive for gold investors.

- 2016 led rallies in zinc and coal, but 2017 could be the year of nickel and oil. Nickel will be finishing 2016 with a rally of 22 percent; however, developments such as the Philippines President Rodrigo Duterte’s rally against mining companies and Indonesia’s export ban may dramatically hamper the metals fundamentals and create a severe supply shortage. Oil may have had a rocky start to 2016 but finished the year up 45 percent. The deal that was made between OPEC members and Russia will serve as a very positive catalyst going into 2017, and analysts at BMO believe the commodity will hit 60 dollars a barrel and may even have room to run to 80 before year end.

Threats

- Crude oil slid after a bigger than expected inventory build, the largest in six weeks according to the American Petroleum Institute, when analysts were estimating a draw. As supply dynamics are still attempting to find their equilibrium price point, oil continues to trade range bound. In order for oil to turn the corner in the near term, inventory builds must come in considerable lower than current data suggests.

- Rising U.S. mortgage rates forced home sales to tumble according to data released this week. Home sales plunged 2.5 percent for the month of November, their lowest level in nearly a year. Although this is not a clear long term trend, it is an area of caution for 2017 as a slowdown in home sales is negative for building material demand.

- General Motors is temporarily idling five U.S. assembly plants in an attempt to reduce bloated inventories. The sector has experienced rapid growth over the past five years as a result of cheap consumer financing; however, interest rates on car loans are slowly rising while terms are much longer than before. According to the research organization IHS Automotive, sales could slide by more than 200,000 vehicles if the company permanently suspends production from these plants. These developments could be negative for platinum group metals and steel demand.

China Region

Strengths

- While Vietnam’s fourth-quarter GDP came in slightly below expectations (but still relatively scorching compared to most peers) at a year-over-year 6.21 percent growth rate, fourth-quarter numbers were still up handily from last quarter’s 5.93 percent pace.

- Year-over-year exports in Thailand rose 10.1 percent in the November period, well ahead of last month’s year-over-year decline of 4.3 percent.

- Industrial Production numbers for South Korea came in better than expected, with month-over-month growth of 3.4 percent for the November period (better than 0.8 percent anticipated in surveys) and year-over-year growth of 4.8 percent (ahead of the 1.5 percent expected in survey data).

Weaknesses

- The Chinese yuan has continued to weaken, with the offshore CNH hitting more than 6.985 this week. China also diluted the weight of the strengthening U.S. dollar in its own currency basket while simultaneously adding additional currencies.

- Though the Conglomerate sector of the Hang Seng Composite Index was the “weakest” sector for the week, it still rose 0.52 percent from last week’s trading.

- The application software provider Sinosoft Technology Group Ltd. (1297 HK) fell nearly 21 percent for the week after a Chinese research group targeted the company for a short sale. Sinosoft recovered some of its losses in trading on Friday.

Opportunities

- Bloomberg analysts expect a roughly 7 percent rise in gambling revenue for Macau next year, which has been somewhat resurgent throughout the second half of this year.

- It is just over a month before the start of the Lunar New Year holidays, which may bring some positive sentiment and seasonality to the coming weeks.

- This weekend we get China’s official Manufacturing PMI, expectations for which stand at a 51.5, down slightly from a previous print of 51.7. We’ll get several more PMI data next week from other countries in the region, as well as Caixin China data.

Threats

- Taiwanese President Tsai Ing-wen, who visits the western hemisphere next month, has scheduled apparently “private and unofficial” stopovers in the United States, angering China as speculation continues over U.S. President-elect Trump’s Taiwan and/or “One-China” policies.

- Yuan weakness and capital outflows from China remain an ongoing threat.

- Xinhua reports that China’s Ministry of Commerce anticipates slowing automobile sales next year following 2016’s big boom. The Ministry of Finance announced a cut in automobile tax reductions for 2017 (or rather, a non-extension of existing incentives, if you will).

Emerging Europe

Strengths

- Hungary was the best performing country this year, gaining 32.6 percent in local currency. The top four holdings in the Budapest Stock Exchange Index add up to 95 percent of the index. These include: OTP Bank which gained 40 percent; Mol Hungarian oil, up 44.8 percent; Richter, a pharmaceutical company which gained 12.9 percent; and Magyar Telekom which appreciated by 22.6 percent.

- The Russian ruble was the best performing currency this year, gaining 17 percent against the U.S. dollar. The currency was supported by a rebound in the price of Brent crude oil, which gained more than 50 percent. Oil appreciated strongly after OPEC announced production cuts on November 30.

- The energy sector was the best performing sector among eastern European markets this week.

Weaknesses

- The Czech Republic was the worst performing country this year, losing 3.6 percent in local currency. The top five holdings of the Prague Stock Exchange Index add up to 90 percent of the index. The biggest negative impact on the Czech bourse came from the performance of Vienna Insurance Company, a dual-listed Austrian name losing 16.4 percent, along with Komercni, a Czech bank, declining by 10.6 percent.

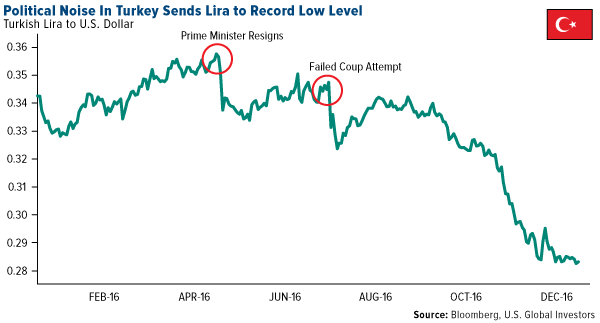

- The Turkish lira was the worst performing currency this year, losing 17 percent against the U.S. dollar. Political and geopolitical risk weighed on the lira. At the beginning of the year the Prime Minister of Turkey resigned, and in July the country attempted a coup which followed by purges across many sectors as President Recep Tayyip Erdogan pressed down on political opposition.

- The industrial sector was the worst performing sector among eastern European markets this week.

Opportunities

- The central bank of the Czech Republic expects inflation to accelerate to 2 percent in the third quarter of next year, and may remove a cap on the koruna. The market has already started to bet on the foreign-exchange regime changing and selling the euro against the koruna as one of the top trades for 2017 for JPMorgan Chase & Co. and UBS Group AG.

- The U.S. will start easing its penalties (imposed on Russia over annexation of Crimea in 2014) during the next 12 months, according to 55 percent of respondents in a Bloomberg survey. Without the restrictions, Russia’s economic growth would get a boost equivalent to 0.2 percentage points of gross domestic product next year and 0.5 percentage points in 2018. Donald Trump’s surprise election in November is feeding expectations of policy change toward Russia.

- FTSE Index provider classifies Romania as a frontier market and in September of this year added it to the watch list for possible promotion to Secondary Emerging Market status. Romania meets eight of the nine “Quality of Markets” criteria required for attaining Secondary Emerging Market status, with recent developments in the infrastructure of the market being received positively by international portfolio investors. The one outstanding criterion is sufficient broad-market liquidity to support a sizeable global investment. Romania may be coming closer to emerging market status.

Threats

- The European political calendar is full for the next 12 months and could create some political tension. British Prime Minister Theresa May gave March 31 as the deadline for triggering Article 50, which will start the process of Brexit. In April, France will hold presidential elections. A Marine Le Pen victory could create crisis in the European Union area given her antipathy to this area. It could also promote a more populist, industrial-policy driven agenda. In August, Germany will hold national elections. Angela Merkel announced her decision to run for a fourth term. Her leadership is critical to retain investment confidence in the region. However, her supporters have declined in number due to her immigration policies.

- The Bank Credit Analyst research team predicts the dollar bull market to stay intact over the coming year with the Trade Weighted Index rising by around 5 percent, which should be negative for riskier emerging Europe assets. The group remains bearish on emerging Europe currencies.

- The outflow of assets from Turkey could continue next year and the lira may remain vulnerable to external conditions and political risks feeding into higher inflation. The Turkish economy faces recession risks as the third quarter GDP contracted 1.8 percent on a year-over-year basis, the first contraction since the third quarter on 2009. The coup attempt in July appears to have hurt the economy more than expected.

© US Global Investors