Stock markets have been very quiet lately, but as we get ready to enter 2017, things may change. Here's why.

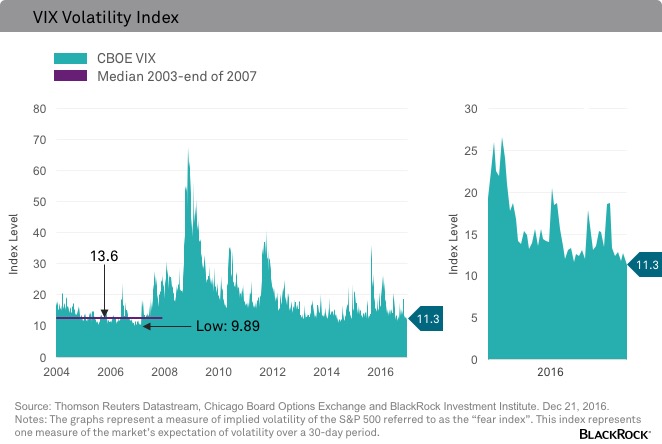

Ideally, the holidays should be calm. Thankfully the market is obliging. Equity market volatility, as measured by the VIX Index, recently dipped below 12, close to multiyear lows. We’ve seen this pattern repeatedly over the past 10 years and it rarely ends well.

We’ve been here before, most recently last summer. In late August I described the unusually low level of volatility. By early September the VIX Index had spiked roughly 70% compared to the August low. It repeated the pattern again around the U.S. election in November (see the chart above). We may be setting up for a similar pattern in early ’17. Here are three reasons volatility is unlikely to remain this low too far into 2017.

Are you prepared for higher volatility? Join in >

1. Equity investors are alone in their torpor.

While the VIX and other measures of equity market volatility are flirting with historic lows, volatility in other asset classes remains elevated relative to the summer levels. Currency volatility, as measured by the CVIX, remains about 20% above the fall lows. U.S. bond market volatility, measured by the MOVE Index, is off the November high but stays 30% above the October bottom. Only equity market investors are convinced that volatility will remain low in the near term.

2. Political Risk is elevated but not reflected.

Many factors, from credit market conditions to economic expectations, drive volatility. Not all are market related. Historically, equity market volatility has been correlated with general political and policy uncertainty. Using the Economic Policy Uncertainty Index as a proxy, since the mid-90s policy uncertainty has explained roughly 25% of the variation in the VIX Index. While the U.S. election is finally over, there is significant uncertainty as to the future direction of policy. The timing and form of corporate and individual tax reform, deregulation and trade policy remain in an indeterminate state. This should be adding to, not subtracting from, volatility.

3. The market is losing its safety blanket.

While prone to episodic spikes, volatility on average has been muted for some time. This is partly a function of very benign monetary conditions and a child-like faith in the ability of central banks to provide a backstop in the event of any selloff. Unfortunately, central banks are fast approaching the limits of unconventional monetary policy. While conditions in Japan and Europe are likely to remain ultra-accommodative, the Federal Reserve (Fed) has resumed its tightening cycle, a trend likely to accelerate next year. Adding to the tightening of financial conditions, the U.S. dollar has advanced roughly 10% from its August lows.

In the near term, momentum and positive seasonality will probably be enough to carry the market. But as the calendar turns, things may change. The market has many things going for it in 2017: optimism for faster growth, a more secure financial sector and the potential for corporate tax reform. Complacency, however, is not on the list.

Russ Koesterich, CFA, is Head of Asset Allocation for BlackRock’s Global Allocation team and is a regular contributor to The Blog.

Investing involves risks, including possible loss of principal. Past performance is no guarantee of future results.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of December 2016 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results.

©2016 BlackRock, Inc. All rights reserved. BLACKROCK is a registered trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

USR-11192

© BlackRock

Read more commentaries by BlackRock