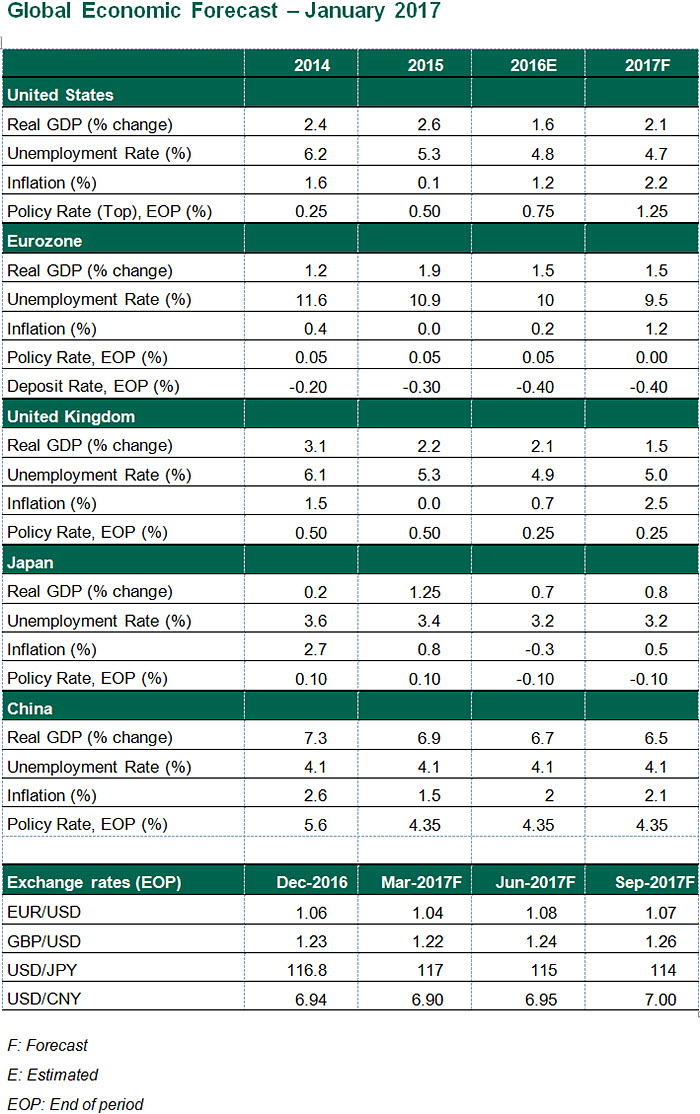

Global Economic Outlook - January 2017

We’ve always waited until the first week of January to issue our outlook for the new year. The extra time usually allows us to digest additional data and identify emerging trends, with the hope of enhancing the accuracy of our forecast.

We can’t say this year that the past few weeks have been very accretive to our understanding. Rarely have we looked ahead to a period with so many uncertainties, many of which are rooted in the global transformational election results of last year. It will no doubt be an interesting year to write about, but is currently a difficult year to anticipate.

Here are the main themes that will likely drive international economic outcomes in 2017:

The New Sheriff(s) in Town

The incoming U.S. administration and Congress have mapped out some ambitious plans for steering the economy. New governments in several other key countries will be taking their seats and making their marks this year. Fiscal stimulus will likely be stressed over monetary accommodation for the first time in many years, and borders may become less open to goods and people.

How will all of this affect growth and inflation? Will current indebtedness limit the scale of any stimulus? And how will measures taken in one country affect economic policy elsewhere?

Euro-anxiety

Already reeling from the Brexit vote and the fall of the Italian government, the fabric of the European Union (EU) will be stretched further in 2017. Preparations for Brexit negotiations will continue to elevate uncertainty. Dutch elections will take place in March, and the French presidential campaign will follow soon thereafter. Germans go to the polls in the fall. In all three countries, there is significant anti-European sentiment.

Our central outlook does not call for populist governments to emerge from any of the three key eurozone elections in 2017, and the context for constructive negotiations between the United Kingdom and the EU may be greater than some think. But “headline risk” is high.

The Fed’s Delicate Dance

The U.S. Federal Reserve (Fed) has been extraordinarily cautious thus far and would like to continue a slow normalization of monetary policy. Yet the risk for inflation may be on the upside for the first time since 2007.

Will the Fed lean aggressively against escalating inflation? Political pressure (not to mention new appointees to the Board of Governors) may lead them to hold back. The consequences of hesitation could be heightened inflation expectations and higher long-term interest rates, which could have international repercussions. The finances of several emerging markets appear tenuous, and China continues its efforts to address an overhang of domestic debt.

The following are specific summaries covering the world’s major centers.

The United States – Managing at Full Employment

The incoming administration in the United States will be working with Congress to formulate a new economic strategy. Reductions in both personal income tax rates and corporate tax rates appear likely. In addition, a national infrastructure program is slated to be considered. Yet given Congressional concerns about the size of the U.S. national debt, the size of the programs will likely be smaller than proposed by the president-elect during the 2016 campaign. Further, it may take time for passage and implementation. We are therefore not expecting significant economic growth in 2017 stemming from changes in fiscal policy.  Our baseline forecast anticipates that modifications will be made to the Affordable Care Act, but we are not expecting it to be repealed. No new trade arrangements are likely to be passed, but existing trade agreements should remain in place. Our assumption is that the U.S. government will not enact punitive tariffs against China or any other trading partner. While changes to immigration policy are likely to be proposed, their scale should not affect long-term population estimates for the U.S.

Our baseline forecast anticipates that modifications will be made to the Affordable Care Act, but we are not expecting it to be repealed. No new trade arrangements are likely to be passed, but existing trade agreements should remain in place. Our assumption is that the U.S. government will not enact punitive tariffs against China or any other trading partner. While changes to immigration policy are likely to be proposed, their scale should not affect long-term population estimates for the U.S.

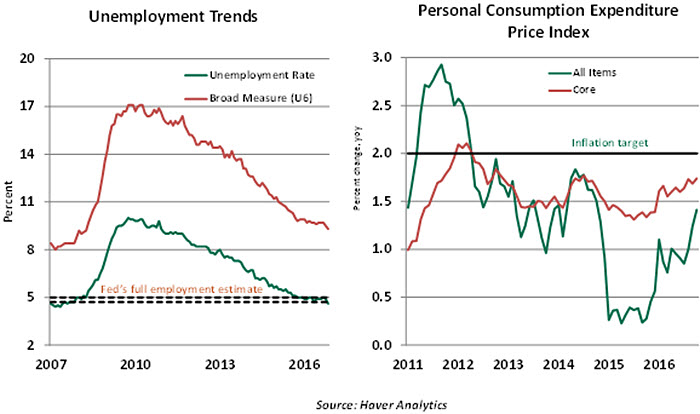

Under these conditions, we predict that U.S. real economic growth will advance at a 2.0% pace during 2017. Consumer spending and housing market activity should continue to advance nicely. Business spending has been weak in 2016, but energy-related investments should show an improvement as oil prices recover.

As the economy is operating close to full employment, further strengthening of employment conditions could kindle wage pressures. Inflation expectations rose significantly in the final months of 2016, and in 2017, inflation is predicted to match the Fed’s 2.0% target.

In this economic environment, we expect the Fed to proceed in a gradual manner. We are expecting two interest rate hikes in 2017: at mid-year and at year-end. We also expect the Fed’s balance sheet to be allowed to start declining sometime in 2017 as the policy of reinvesting maturities is brought to a close.

Uncertainty about the scale and scope of fiscal policy changes is the main risk element for the U.S. forecast. We’ll be watching events in Washington more closely than usual.

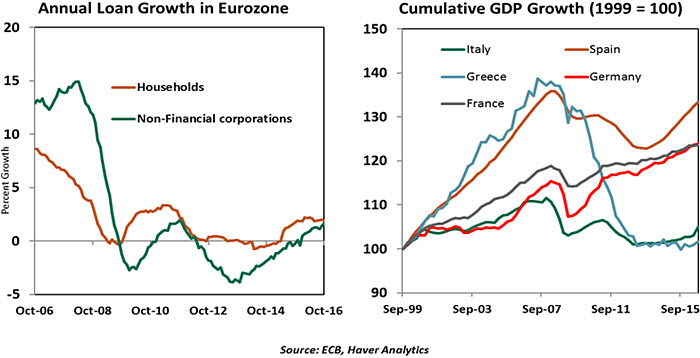

Eurozone – Tiptoeing Through the Political Minefield

The core of Europe has performed remarkably well in spite of political headwinds. We expect the Continent’s expansion to continue at a tepid pace. The banking sector’s woes, stimulus tapering from the European Central Bank (ECB) and the uncertainty surrounding key elections are weighing down expectations.

The outlook for headline inflation in the euro area is stronger, as oil prices have almost doubled from their lows of last January. We expect inflation to average 1.2% in 2017. This will diminish real incomes in the euro area and could impair consumption. With unemployment in many countries still high, compensating increases in wages seem unlikely.  At the ECB’s latest meeting, it committed to continue its bond buying until the end of 2017 – albeit at €60 billion per month versus the current €80 billion. It also changed the technical criteria around the eligibility of bonds for purchase to deal with scarcity of eligible assets. Since we expect core inflation to remain subdued, and with lending growth improving only very slowly, the ECB may not be done with quantitative easing.

At the ECB’s latest meeting, it committed to continue its bond buying until the end of 2017 – albeit at €60 billion per month versus the current €80 billion. It also changed the technical criteria around the eligibility of bonds for purchase to deal with scarcity of eligible assets. Since we expect core inflation to remain subdued, and with lending growth improving only very slowly, the ECB may not be done with quantitative easing.

Eurozone countries seem to have a little more latitude to use fiscal policy to boost growth. Unfortunately, the countries in the best position to take this step need it the least, while the neediest countries have the most severe budget problems. Expect Greece to be back in the headlines during the early portion of the year, once again testing the harmony of its supporters.

Our forecast for 1.5% growth in 2017 assumes that anti-EU parties will not prevail in national elections in the Netherlands, France, Italy, and Germany. Both the Netherlands and Italy have a fractious political system that is unlikely to give anti-EU parties sufficient power to rock the boat, while support for the anti-EU Alternative for Germany (AfD) party has yet to reach a critical mass. France, on the other hand, needs to be watched closely as the anti-EU National Front’s Marine Le Pen is almost certain to reach the second round of the presidential elections. Any credible signs of a major European capital deciding to exit from the union would be enough to plunge the eurozone into a full blown crisis.

United Kingdom – A Slow Separation

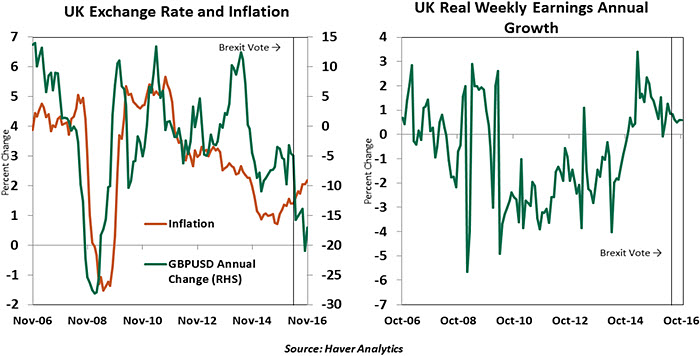

The shape, size, and schedule of Brexit will dictate the direction of the British economy in the years to come. While Article 50 will almost certainly be triggered in March of this year, the actual exit from the EU is likely to take much longer than the prescribed two years. This will be a long-running economic drama. The key question for the U.K. outlook is how the uncertainty introduced by Brexit discussions will affect economic activity. Will firms downsize their presence in the U.K. and relocate to the Continent? Will there be an outflow of European migrant workers? Will companies and consumers hold onto their wallets until the contours of a new relationship between Britain and the EU become clear?

The key question for the U.K. outlook is how the uncertainty introduced by Brexit discussions will affect economic activity. Will firms downsize their presence in the U.K. and relocate to the Continent? Will there be an outflow of European migrant workers? Will companies and consumers hold onto their wallets until the contours of a new relationship between Britain and the EU become clear?

To date, Brexit has not hindered the U.K. economy. Consumption, the largest contributor to U.K gross domestic product (GDP), has been buoyant, indicating that imported inflation (which has diminished real earnings growth) hasn’t bitten yet. However, spending habits take time to adjust, and it is only a matter of time before the decline in purchasing power starts dampening household consumption.

While the weaker sterling has given a terms-of-trade boost, we expect the impact on exports to be limited. Investment hasn’t yet declined amid the incipient uncertainty, but it is not expected to accelerate. Prime Minister Theresa May promised some additional fiscal support, but austerity still seems to be winning the day. Overall, we expect growth to slow down to 1.5% in 2017, with risks on the downside.

The Bank of England has been vocal about its willingness raise rates if currency-induced inflation gets out of hand. However, we see these communications as part of a strategy to anchor inflationary expectations rather than a statement of policy intent. We believe that weak economic activity will force the Bank of England to keep policy rates unchanged.

China – The Challenge of Controlling Capital

The Chinese are moving cautiously to rebalance its economy away from exports and manufacturing and towards household consumption and services. Counter to this long-run objective, an activist fiscal policy focused at public investment was essential to meeting the Chinese government’s annual growth target last year.

In 2017, we expect the fiscal impulse to remain strongly positive and the Chinese economy to grow at 6.5%. Price pressures are expected to remain neutral, with the inflationary impact from a weaker currency and stronger global commodity prices likely to be offset by softness in the domestic economy.  Our forecast assumes there will be no material change in the U.S.-China trade relationship, hawkish rhetoric notwithstanding. At the same time, even a slow burning trade war might force the Chinese policy makers to prioritize the much delayed domestic reform process. For the time being, financial stability is the top concern for policy makers. Debt levels in the country continue to escalate; the People’s Bank of China will likely have to apply further macro-prudential measures to mitigate financial risks.

Our forecast assumes there will be no material change in the U.S.-China trade relationship, hawkish rhetoric notwithstanding. At the same time, even a slow burning trade war might force the Chinese policy makers to prioritize the much delayed domestic reform process. For the time being, financial stability is the top concern for policy makers. Debt levels in the country continue to escalate; the People’s Bank of China will likely have to apply further macro-prudential measures to mitigate financial risks.

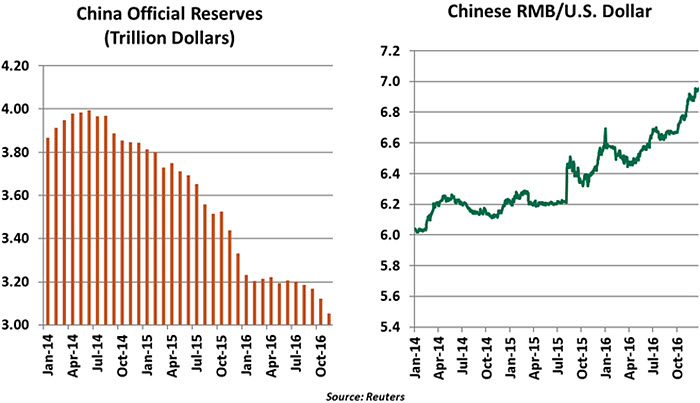

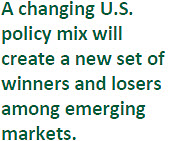

The decline of the Chinese RMB accelerated in 2016 and gained momentum after the U.S. presidential elections. However, we do not see this as part of a deliberate strategy to gain export competitiveness but as a result of the steady outflow of capital.

The sustained weakness in currency and capital outflows are mutually self-reinforcing, and the People’s Bank of China (PBOC) would rather rein in the outflow and live with a stronger RMB than have a weaker currency that could imperil financial stability. (In fact, the PBOC took steps toward that outcome this week.) The rapid decline in official reserves has prompted a number of restrictions on capital outflows, and we would expect this policy to extend into the new year. The balancing act on this front should test even the best of Chinese gymnasts.

Japan – The Same Old Story

Unfortunately, the Japanese economy is likely to grow at an uninspiring pace in 2017. Though the weaker yen will boost export revenues, there will be some negative impact on real disposable incomes, and therefore consumption. While some marginal fiscal support would be welcome, the fundamental issue of low potential growth lingers. For the time being, we expect the economy to expand by 0.8% in 2017.

Structural reforms, the so-called third arrow of ‘Abenomics’, are essential to lift Japan out of its current path. But these measures have yet to be deployed wholeheartedly. For example, the government’s welcome focus on boosting incomes for non-regular employees has not been matched by enthusiasm for broader changes in the Japanese labor market. Labor force participation among women, a focus for policy makers, remains low relative to other industrialized countries.

Inflation in Japan will likely trend marginally higher (though still below the 2 percent target), reflecting a slight improvement in business expectations, a weaker yen, and higher global commodity prices. We expect some technical adjustments in the Bank of Japan’s (BoJ) asset purchase program and negative interest rate regime – rising global yields would make BoJ’s yield curve control policy more onerous to execute. But we do not foresee any fundamental shift in the monetary policy framework or stance.

Japan’s fundamental problem—unfavorable demographics—remains a severe limitation.

Emerging Markets – A Year of Caution

When America sneezes, the world catches a cold - or so the saying goes. This time around though, the recovery of the U.S. economy and the accompanying rise in U.S. yields appears to be one of the key risks to emerging markets (EMs).

Cheap dollar funding costs prompted a debt binge in some EMs during the post crisis years, something that is becoming increasingly difficult to sustain. Narrowing interest rate differentials between the U.S. and EMs would make it difficult to finance large current account deficits in many EMs. We expect the fallout to be much smaller than “taper tantrum” since the U.S. monetary policy normalization has been priced in for a while now.  Countries with significant trade exposure to the U.S. could be hit by a double whammy of restricted inflows and a decline in exports if the new U.S. administration delivers on its anti-trade rhetoric. This would complicate the task for EM central banks as they try to balance a slowing economy with capital outflows. We believe most central banks would prioritize the former, as tight monetary policy to limit capital outflows has proved to be a failed strategy in previous crises.

Countries with significant trade exposure to the U.S. could be hit by a double whammy of restricted inflows and a decline in exports if the new U.S. administration delivers on its anti-trade rhetoric. This would complicate the task for EM central banks as they try to balance a slowing economy with capital outflows. We believe most central banks would prioritize the former, as tight monetary policy to limit capital outflows has proved to be a failed strategy in previous crises.

However, the much beleaguered commodity-producing EMs in Latin America, Russia, Middle East and Africa can look at 2017 with some hope as the expectations of U.S. “reflation,” along with the recent Organization of the Petroleum Exporting Countries (OPEC) agreement, has pushed global commodity prices higher.