And like that, it happened. Despite the polls, despite what anyone believed was possible, including many of his own supporters, billionaire developer Donald J. Trump was sworn in as the 45th President of the United States.

Whether you agree with him not, he’s now leader of the world’s largest economy and commander of history’s most powerful military force.

This is something that could only happen in the U.S.

President Trump and now-former President Barack Obama couldn’t be more different in their backgrounds, visions and leadership styles—more so than any other two men whose administrations happen to adjoin the other’s.

|

And yet the transition went remarkably smoothly and orderly.

I don’t believe there’s ever been such a meaningful and potentially consequential transfer of power in U.S. history, with the incoming president all but promising to undo every last policy of his predecessor, line by line. That Obama peacefully and cordially handed over the executive office to a man who led the charge in questioning his legitimacy for a number of years is a testament to the strength and durability of our democratic process.

It’s a process that’s key to America’s exceptionalism.

Although I don’t always agree with Trump, it saddens me to see so much negativity about him in the media and protests in the streets. Now that he’s president, the time has come to unite behind him and root for his success. If he succeeds, America succeeds. If he fails—as many seem to hope for—America fails.

Take Warren Buffett. He backed Hillary Clinton throughout the primaries and general election. And yet just yesterday, on the eve of Trump’s inauguration, he said he supported the new president and his cabinet “overwhelmingly,” adding that he’s confident America “will work fine under Donald Trump.”

I think what Buffett recognizes is that the vast majority of people who voted for Trump did so for the right reasons. Throughout his campaign, Trump’s promise to bring back American jobs and secure the nation’s borders resonated with everyday folks who have begun to feel overlooked. Entrepreneurs, small business owners and those working in the financial industry found hope and encouragement in his pledge to lower corporate taxes and roll back regulations. I believe most Americans, regardless of political ideology, want these things—which is why we saw such a large number of people who previously voted for Obama give Trump their vote this time.

People like Buffett and entrepreneurs have a “growth” mindset because they embrace challenge, persist in the face of setbacks and are willing to put in the time and hard work to achieve their goals. People with a “fixed” mindset, on the other hand, ordinarily avoid challenge and believe their intelligence and talents can’t be developed. It’s people with a “growth” mindset that we want as our business and political leaders.

(To learn more, watch this short TEDx video, “The Power of Belief—Mindset and Success.”)

As I often say, government policy is a precursor to change, and we’re likely about to see some sweeping changes. But as investors, it’s as important as ever that we don’t panic or get distracted by the noise. Instead, continue to focus on the fundamentals and keep your eyes on the long-term prize.

Inflation Plays Catch-Up

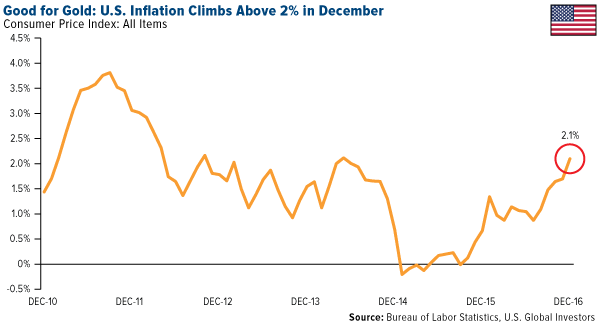

Inflation, as measured by the consumer price index (CPI), got a strong jolt in December, rising 2.1 percent year-over-year, its fastest pace in at least two-and-a-half years. Higher gasoline prices—which rose more than 8 percent in December—and health care costs were the main culprits, with medical bills surging the most in nine years.

Although they might hurt your pocketbook, pricier goods and services have historically been constructive for gold, as I’ve explained many times before. In August 2011, when gold hit its all-time high of $1,900 an ounce, inflation was running at 3.8 percent and the government was paying you an average 0.23 percent on the 2-year T-Note. That means investors were earning a negative 3.5 percent return, which helped boost gold’s “safe haven” status.

I expect CPI to continue to climb throughout this year and next, supported by additional interest rate hikes—two or three in 2017 alone—and President Trump’s protectionist policies.

The metal’s investment case could be strengthened even more now that Trump has officially been sworn in. His personal shortcomings and public office inexperience might raise more than a few “unknown unknowns” for some investors, prompting them to seek an alternative to stocks and bonds. Scotiabank hinted at this in a recent note, saying it expects gold holdings “to increase as investors look to diversify their portfolios in what seems likely to be a challenging year for investors.”

On Inauguration Day, gold rose a little under 1 percent to close at $1,210.

Whether you support the new president’s policies or not, it’s still prudent to maintain a 10 percent weighting in gold, with 5 percent in gold stocks, the other 5 percent in coins and bullion.

Another Gold Rally in the Works?

Look at the chart below. It’s indexed at 100 on the day the Federal Reserve raised rates in 2015 and 2016 (December 16 and 14, respectively). Although past performance doesn’t guarantee future results, gold prices so far this year appear to be tracking last year’s performance pretty closely, suggesting further upside potential.

In the first half of 2016, gold rallied more than 31 percent, from a low of $1,046 in December 2015 to a high of $1,375 in July. With mid-December 2016 as our starting point, a similar 31 percent move this year would add close to $360 to the price of gold, taking it to above $1,520 an ounce.

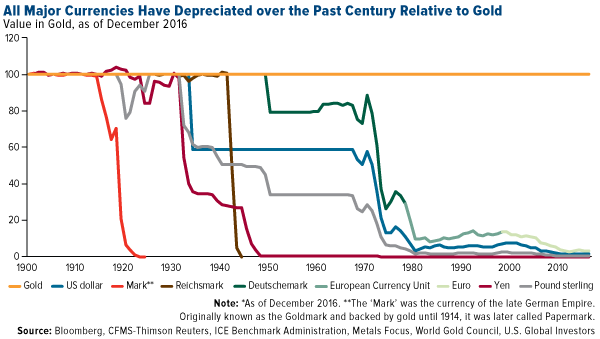

Gold Has a 100-Year History of Outperforming All Major Currencies

In its 2017 outlook, the influential World Gold Council (WGC) listed six major trends that will likely support gold demand throughout the year, including heightened geopolitical risks (Brexit, Trump, the global rise of populism), a potential stock market correction, rising inflation expectations and long-term Asian growth.

The group also calls out currency depreciation. Over the past 100 years, gold has strongly outperformed all major currencies. Whereas global gold supply grows at an annual average of only 2 percent, there’s no limit to how much fiat money can be printed.

Inflation and currency depreciation are among the Fear Trade’s triggers that I often write and speak about.

Spending Watchdog: U.S. Is on an “Unsustainable Fiscal Path”

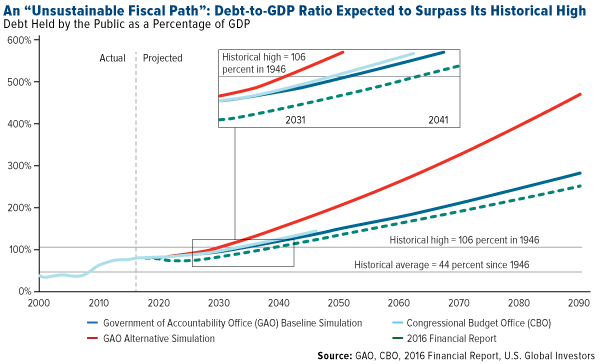

This point about currency depreciation is especially relevant in light of an alarming new report from the U.S. Government Accountability Office (GAO), the nation’s watchdog. According to the report, the federal government’s spending is “unsustainable,” and if no action is taken to rectify the problem, the debt-to-GDP ratio will soon exceed its historical high of 106 percent, set in 1946.

To be clear, that means our nation’s debt will be larger than its economy.

The federal deficit increased to $587 billion in 2016, after six years of declining deficits. Spending increases were driven by entitlement programs such as Medicare and Medicaid, which surged 4.9 percent and 5.3 percent, respectively, during the year.

Whether Trump can change any of this, we’ll just have to wait and see. He seems interested in lowering costs and bringing some fiscal sanity to the government, as demonstrated by his criticism of Boeing over the perceived cost of Air Force One. At the same time, massive tax cuts, coupled with a $1 trillion infrastructure package, will likely drive up deficit spending even more.

All the more reason to have a portion of your portfolio invested in gold and gold stocks.

One Final Thought…

This weekend I’m speaking at the Vancouver Resource Investment Conference, cosponsored by Cambridge House and Katusa Research. I’ll be sure to share my thoughts and observations with you next week!

In the meantime, I wish President Trump all the best!

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.29 percent. The S&P 500 Stock Index fell 0.15 percent, while the Nasdaq Composite fell 0.34 percent. The Russell 2000 small capitalization index lost 1.47 percent this week.

- The Hang Seng Composite gained 0.12 percent this week; while Taiwan was down 0.51 percent and the KOSPI fell 0.54 percent.

- The 10-year Treasury bond yield fell 7 basis points to 2.47 percent.

Domestic Equity Market

Strengths

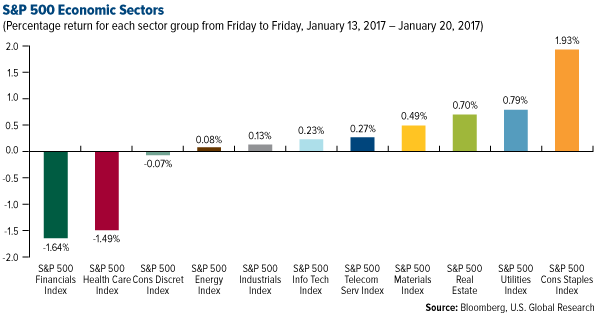

- Consumer staples was the best performing sector of the week, increasing by 1.93 percent versus an overall decrease of 0.15 percent for the S&P 500.

- CSX Corp was the best performing stock for the week, increasing 14.25 percent.

- Netflix surprised Wall Street on Wednesday when it reported fourth-quarter earnings and subscriber growth. In the U.S., net additions totaled 1.93 million, much better than the consensus forecast among analysts of 1.38 million and Netflix's own prior estimates. Earnings per share were $0.15, two cents above the median forecast. Netflix's performance drove its stock higher in after-hours trading. On Thursday, it hit an all-time high of $143.45.

Weaknesses

- Financials was the worst performing sector for the week, falling 1.64 percent versus an overall decrease of 0.15 percent for the S&P 500.

- Bristol-Myers Squibb was the worst performing stock for the week, falling 12.43 percent.

- Tiffany & Co. said sales at U.S. stores open for at least one year fell 4 percent during November and December compared with a year ago. "Management attributed the lower sales to local customer spending, with a decline in U.S. sales exacerbated by a 14 percent decline at the company's flagship store on Fifth Avenue in New York, which we attribute at least partly to post-election traffic disruptions," the company said in a statement.

Opportunities

- Ford's CEO shared his vision of the future this week. "Our view is that the industry offerings, 15 years from now, is that there are going to be more electrified offerings than there are internal combustion engines," Ford CEO Mark Fields told Business Insider.

- GM says that it will invest $1 billion in its factories and create or keep 1,000 jobs as part of its normal process of upgrading factories, the Associated Press reports, citing a person familiar with the matter.

- With real exports of food and beverage products surging in recent months and sales growth expectations bottoming out, the recent share price decline in the packaged foods industry could be an opportunity to get in before the bounce.

Threats

- The FTC alleges that Qualcomm paid Apple billions of dollars in rebates to use its chips. The Federal Trade Commission said a deal between Apple and Qualcomm included "substantial incentive payments" on the condition that Apple would continue using Qualcomm's baseband processors "exclusively" in all iPhone and iPad models from 2011 and 2012.

- According to a BCA analysis of relative industrials performance since the early 1990s, every time the ISM manufacturing new orders sub-index hit 60, industrial stocks will suffer in the coming quarters, as too much optimism is already discounted.

- While momentum and buoyant expectations have been a powerful support for equity markets, it is critical to keep a close eye on the cyclical valuation backdrop to avoid getting caught up in any hype. For instance, the total market capitalization (MC) of the U.S. stock market is more than 120 percent of (nominal) GDP, more than double the 2008 trough. MC as a share of GDP has only been higher during the Internet bubble in the late-1990s. MC to GDP has averaged 75 percent over the last 45 years.

The Economy and Bond Market

Strengths

- The Philadelphia Federal Reserve's manufacturing outlook index came in at 23.6, significantly above expectations of 15.8. "Forty percent of the firms reported increases in activity this month; 17 percent reported decreases," said the release from the Philly Fed. The activity index reading was the highest since November 2014.

- Housing starts jumped more than expected in December. Housing starts rose by 11.3 percent at a seasonally adjusted annual rate of 1.226 million, according to the Commerce Department.

- Initial jobless claims unexpectedly tumbled to 234,000. Moreover, the four-week moving average was 246,750, a decrease of 10,250 from the previous week's revised average. This is the lowest level for the average since November 3, 1973, when it was 244,000.

Weaknesses

- After a big jump post-election, the Empire Manufacturing report for January backed off of its recent highs, missing consensus forecasts in the process. While economists were forecasting the headline reading to come in at a level of 8.5, the actual reading came in at 6.5.

- The NAHB Housing Market Index for January came in at 67, missing consensus expectations of 69 and lower than the previous month’s reading of 70.

- Building permits for December disappointed, falling 0.2 percent vs the expected growth of 1.1 percent.

Opportunities

- According to Matthew Hornbach, global head of interest-rate strategy at Morgan Stanley, the 10-year yield will end 2017 at 2.50 percent, which is around the same level that it entered the year. What that means from a return perspective is that Treasuries should be okay this year. Forward yields are higher than 2.50 percent in certain parts of the curve and so to the extent that he is correct and 10-year yields end around 2.50 percent, investors in government bonds should have a positive total return.

- President Donald Trump vowed to restore America’s promise. In his inaugural address, Trump pledged to transfer power from Washington, D.C., back to the American people. He called for defending the U.S.’s borders while rebuilding its infrastructure. Every decision, whether on trade, taxes or immigration, will be made to benefit American workers and families, he said. While he expects other nations to put their interests first as well, he said the United States will reinforce old alliances and build new ones.

- Several regional Fed surveys are being released next week. If their capex intentions components hold on to previous sharp gains, it would be a strong signal that core durable goods orders (Friday) are about to surge.

Threats

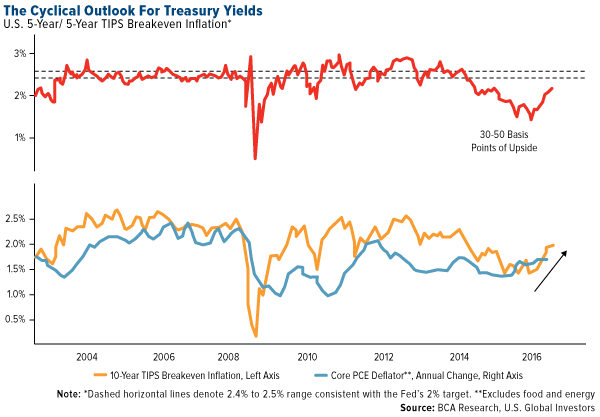

- According to BCA, rising inflation expectations should push 10-year U.S. Treasury yields higher over the next 12 months. With stronger growth and an already tight labor market, core inflation should continue to gradually rise toward the Fed's target. BCA expects trailing 12-month core PCE inflation will reach the Fed's 2 percent target near the end of 2017. Consequently, the cost of inflation protection embedded in bond yields will also converge with levels that are consistent with the Fed's target. Their forecast is that level should be in the range of 2.4 percent to 2.5 percent for long-dated TIPS breakevens. With the 5-year/5-year forward TIPS breakeven rate at 2.13 percent and the 10-year TIPS breakeven rate at 2 percent, long-dated Treasury yields have approximately 30-50bps of upside from the inflation component alone.

- The Congressional Budget Office (CBO) said the GOP's Obamacare repeal could leave 27 million people without health insurance and cause premiums to skyrocket. The CBO projections are based on the 2015 ACA repeal bill that was vetoed by President Barack Obama. A new repeal bill is currently being drafted and could have some differences.

- Federal Reserve Chair Janet Yellen warned against running the economy “hot.” Speaking at the Stanford Institute for Economic Policy Research on Thursday evening, Yellen said, "I think that allowing the economy to run markedly and persistently 'hot' would be risky and unwise."

Gold Market

This week spot gold closed at $1,210.57, up $12.99 per ounce, or 1.08 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.74 percent. Junior tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index climbed just 0.39 percent. The U.S. Trade-Weighted Dollar Index finished the week down by 0.38 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jan-17 | Germany ZEW Survey Expectations | 18.4 | 16.6 | 13.8 |

| Jan-17 | Germany ZEW Survey Current Situation | 65.0 | 77.3 | 63.5 |

| Jan-18 | Germany CPI YoY | 1.7% | 1.7% | 1.7% |

| Jan-18 | Eurozone Core CPI YoY | 0.9% | 0.9% | 0.9% |

| Jan-18 | U.S. CPI YoY | 2.1% | 2.1% | 1.7% |

| Jan-19 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Jan-19 | U.S. Housing Starts | 1188k | 1226k | 1102k |

| Jan-19 | U.S. Initial Jobless Claims | 252k | 234k | 249k |

| Jan-19 | China Retail Sales YoY | 10.7% | 10.9% | 10.8% |

| Jan-26 | Hong Kong Exports YoY | 6.7% | -- | 8.1% |

| Jan-26 | U.S. Initial Jobless Claims | 246k | -- | 234k |

| Jan-26 | U.S. New Home Sales | 585k | -- | 592k |

| Jan-27 | U.S. GDP Annualized QoQ | 2.1% | -- | 3.5% |

| Jan-27 | U.S. Durable Goods Orders | 2.7% | -- | -4.5% |

Strengths

- The best performing precious metal for the week was palladium with a gain of 4.92 percent. Most of the gains came on Friday after Sibanya Gold’s proposed acquisition of Stillwater Mining passed U.S. antitrust conditions. Not only does Stillwater produce palladium, it’s also one of the largest recyclers of used automobile catalytic converters. James Steel of HSBC has noted that the supply of palladium has stagnated in recent years while auto sales have soared.

- Gold traders and analysts surveyed by Bloomberg are bullish on the metal for a fourth straight week, citing uncertainty surrounding Donald Trump’s inauguration today. “As the inauguration of Trump draws close, I think people are realizing that potentially this could be a very stormy Presidency and gold may well benefit from that,” said David Govett earlier in the week, an analyst at Marex Spectron Group in London. The start of the year is usually positive for gold, reports Bloomberg.

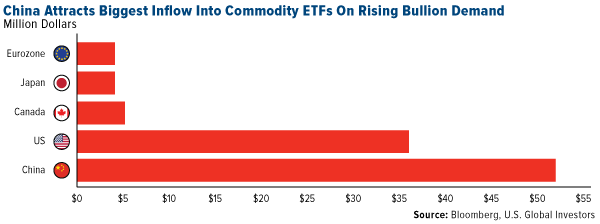

- As you can see in the chart below, China attracted $52 million into commodity-linked ETFs over the past week. A weakening yuan and capital outflows from the Asian nation are adding to the global forces helping to boost demand for gold, reports Bloomberg. Investors are seeing an alternative after the yuan sustained its worst annual loss against the dollar in more than two decades, the article continues.

Weaknesses

- The worst-performing precious metal for the week was platinum, down 0.71 percent. BofAML Global Research forecasted that there is little upside for platinum this week, despite increased demand, as South African producers are putting more ounces on the market at a time when discipline is needed.

- Following seven days of gains, gold finally snapped its best run since November as an interest rate outlook was eyed this week, reports Bloomberg. Vyanne Lai, an economist at the National Australian Bank in Melbourne, says there is recognition that an expected acceleration of rate hikes in 2017 by the Federal Reserve will be an important driver for the metal.

- Despite the chatter of faster inflation, gold traders are pricing in a relatively calm market, according to Bloomberg. Wagers on gold volatility are near a two-year low, diverging from a gauge of inflation bets by the most since September 2014. “The cost of hedging against SPDR Gold Shares declines in the next three months is falling back toward its annual mean, after surging to a more than one-year high following U.S. presidential election,” the article continues.

Opportunities

- Gold bulls looking forward to a rally in bullion with the arrival of a new U.S. president may have history on their side, says Bloomberg. “Gold has averaged gains of almost 15 percent in years marking the inauguration of a new president since the 1970s, advancing in five of those seven years,” the article continues. And because markets are seeing the first annual return for raw materials since 2010, many fund managers that played the last commodity slump want back in, according to Societe Generale SA and Barclays.

- An article in Advisor Perspectives this week highlights Jeffrey Gundlach’s response to the excessive debt, high price-to-earnings (P/E) levels and political uncertainty investors face as they enter the Trump era. He says that U.S.-centric portfolios should diversify globally and that investors should brace for moderately higher inflation. Gundlach notes that the U.S. is “richly valued,” so now is the time to look at other markets. However, he doesn’t recommend Europe due to “election risks” in France and the Netherlands. Gundlach has advocated a “permanent” gold position for investor’s portfolios since 1990 and there are numerous gold miners that are based outside of the U.S.

- Bloomberg released an insightful piece this week on Paul Huet, CEO of Klondex Mines, calling him a “Canadian mining darling,” who finds profitable gold production in projects that no one else wants. Huet became CEO in 2012 when the company had just $400,000 in cash, one asset and $7 million in invoices. Five years later, writes Bloomberg, Klondex shares are outperforming its peers while remaining undervalued. The company has been profitable for nine of the last 10 quarters and, according to Huet, it could produce north of 250,000 ounces of gold equivalent in the “very, very near future.” Production guidance for 2017 is expected to increase by 37 percent as the Hollister mine should begin production in the next six months.

Threats

- The cash ban in India is making it very hard for gold lovers in the country to purchase wedding rings and jewelry, reports Bloomberg. A majority of consumers have a lot less cash these days, and many retailers aren’t equipped to accept credit cards because India’s jewelry industry runs mostly on cash. According to the World Gold Council, gold demand in India probably tumbled to a seven-year low in 2016.

- Deutsche Bank WM is not bullish on gold in 2017, citing the outlook for a stronger U.S. dollar, and also noting U.S. inflation not going up significantly. The bank expects gold to trade around $1,200 by year-end, but still recommends it as a hedge to clients.

- Comments made by Fed Chair Janet Yellen on Wednesday spurred a rise in U.S. yields and the U.S. dollar, writes BBH in its CurrencyView report this week. “She spoke after headline CPI rose above 2 percent for the first time in a couple of years and reports of the largest rise in industrial output since November 2014,” the note reads. Some observers saw in Yellen’s comments stronger confidence in the economy which could bolster the case for a rise in interest rates.

Energy and Natural Resources Market

Strengths

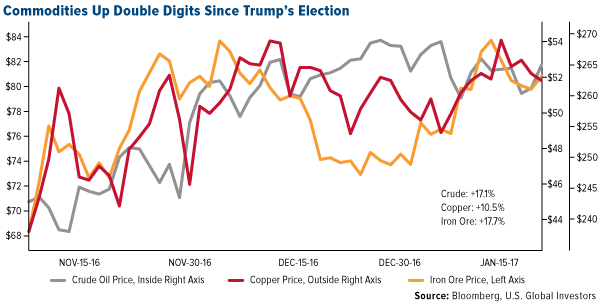

- Commodities are up double digits since Trump’s election last November. Crude oil, copper and iron ore have rallied 17.1, 10.5, and 17.7 percent respectively. As today marks the official inauguration of President Donald Trump, the incredible performance from these key commodities suggests that the reflation trade is officially in motion, which should be further supported by President Trump’s pro-growth policies moving forward.

- The best performing sector for the week was the S&P Super Composite Construction and Materials Index. The index rose 2.87 percent as the imminent inauguration of President Trump led investors to position on a sector that presents itself as a direct beneficiary of Trump’s campaign promises of infrastructure expansion.

- Alcoa Corporation, one of the world’s largest producers of aluminum, was the best performing stock this week finishing up 7.69 percent. The stock rallied after Wilbur Ross, President Trump’s nominee for Secretary of Commerce, stated that the U.S. should focus on increasing tariffs on imported steel and aluminum.

Weaknesses

- Nickel was the worst performing commodity this week falling 5.7 percent. The drop in the commodities price was driven by the easing of the nickel-ore exports ban in Indonesia. Indonesia is estimated to produce 12 percent of global nickel output. The ban had been in place since January 2014.

- The worst performing sector this week was the S&P/TSX Composite Diversified Metals and Mining Sub Industry Index. The index fell 2.8 percent driven by a drop in hard coking coal prices, which have fallen 23 percent year-to-date. China announced its ambition to reduce its steel milling capacity by up to 12 percent, a measure that could result in weaker demand for coking coal prices in 2017.

- The worst performing stock for the week was Reliance Industries Ltd, and refining and petrochemicals company based in India. The company fell 6.3 percent after revealing large write downs in its key oil and gas assets.

Opportunities

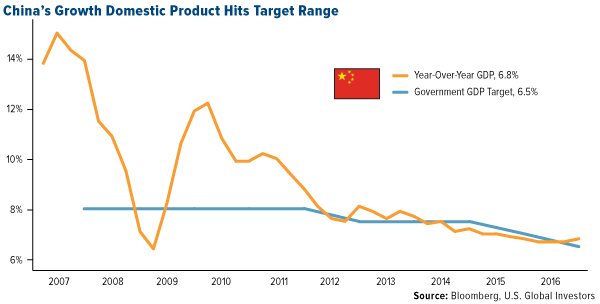

- China GDP hit its 2016 target. Despite potential negative headwinds, the economy of China has avoided a hard landing in 2016 as a result of robust monetary and fiscal stimulus. The economy grew at 6.7 percent for the full year and at a surprising 6.8 percent in the fourth quarter, comfortably within the government’s target range of 6.5 to 7 percent. A positive read-through from the world’s engine of economic growth.

- Top oil companies are back in acquisition mode this year, targeting smaller exploration and development companies to boost reserves, according to Reuters. Since November of last year, there have been 11 deals done by the world’s largest oil companies with a combined value of $31 billion.

- Gold rallied more than 1 percent this week, the largest price jump since late November. As the prospects of a weakening dollar loom to bolster U.S. trade and uncertainty surrounding the United Kingdom’s Brexit plan, investors are beginning to acquire more of the shiny metal as sentiment is shifting towards the uncertainty camp.

Threats

- Coking coal, the best performing commodity of 2016, fell 6.6 percent this week as Chinese mines raise output. The price of the commodity rocketed last year as the Chinese government introduced production curbs in an effort to improve the profitability of the heavily indebted industry. As prices have gone too far too fast, putting pressure on steel prices, the authorities in Beijing are now putting pressure to increase output adding supply to the market and curbing the high price of the commodity.

- OPEC needs further output cuts to balance the oil market this year, according to the Financial Times. The cartel has forecasted that overhang in supply will continue to threaten prices this year as forecasted demand is 32.1 million barrels per day versus a target output level of 32.5 according to its monthly report. Demand is not expected to outpace supply until the third quarter of this year where demand is estimated to reach 33.3 million barrels per day and the backlog in supplies from 2014 is cleared.

- Key growing areas for soybean’s in Argentina continue to experience heavy rainfall and disruption to production. In the first two weeks of 2017 the key growing areas have suffered the equivalent of 6 months’ worth of precipitation, ruining all seeded fields. A negative read-through for the agricultural producers in the region.

China Region

Strengths

- China was the best performing country in the region this week up 33 basis points. Shares extended their rally on Friday, after reports that policymakers have offered funds to some lenders to meet cash demand before the Lunar New Year holidays. The rally also continued amid speculation that China plans to relax curbs on stock-index futures trading that led to a 99-percent plunge in volumes.>

- The Malaysian ringgit was the best performing currency in the region this week up 44 basis points. The ringgit has depreciated about 6 percent against the U.S. dollar since Donald Trump’s surprise win in the U.S. election -- the worst hit among Asian emerging markets -- prompting Bank Negara to take steps to restrict some offshore foreign-exchange trading to curb the currency’s slide.

- The materials sector was the best performing sector this week up 1.76 percent.

Weaknesses

- Thailand was the worst performing country in the region this week down 78 basis points.

- The Indonesian rupiah was the worst performing currency in the region this week down 71 basis points.

- Energy was the worst performing sector this week down 1.75 percent.

Opportunities

- Chinese high-rollers are finally returning to Macau, two years after an anti-corruption crackdown by China’s government scared many of them away from the world’s largest gambling hub. VIP gaming, measured by revenue from the baccarat card games favored by high-stakes gamblers from China, rose 13 percent in the last three months of 2016, marking a turnaround since the first quarter of 2014, data from Macau’s Gaming Inspection and Coordination Bureau show. Mass market games improved 7.3 percent, the second-straight quarter of gains.

- The Philippine peso, which weakened 4.6 percent over the past 12 months, is forecasted to be the most resilient to external risks this year, according to a Bloomberg survey of 10 foreign-exchange analysts. The Thai baht and Indian rupee together rank second, while China’s yuan is last. According to the analysts, external factors won’t impact the peso much because the nation doesn’t largely depend on trade, especially with China or the U.S. China-dependent economies are likely to be hit the most by Trump policies as his eyes are more on China.

- As the acceleration in China’s PPI number has been suggesting, China nominal GDP accelerated to 9.9 percent year-over-year in the fourth quarter, up almost 400 basis points since its low of 6 percent in 2015. Looking at the fourth quarter, real GDP growth came in at 6.8 percent year-on-year, picking up from 6.7 percent in the third quarter and exceeding expectations of another 6.7 percent reading. The data also confirm the gradual shift to more services, more consumption – while less agriculture, less manufacturing and less mining. Pick-up in China economic activity provides some respite to emerging markets, especially as the commodity and trade cycle likely bottomed in 2016.

Threats

- Asia’s nascent exporters are about to confront a potentially major setback. Economists are concerned that a recent upswing in Asian trade will struggle to survive an expected U.S. turn to protectionism under Trump’s presidency. The incoming president’s threatened tariffs and policies on China could harm solid demand from the world’s number two economy that’s been the key to the region’s export recovery.

- According to Evercore ISI, a dangerous confrontation looks likely post Jan 20, as incoming President Trump moves to reset U.S.-China economic relations. The U.S. will want to inflict economic pain on China, likely eliciting a China response of unknown consequence, size and duration. This is delicate and could quickly spin out of control, threatening other parts of the 2017 U.S. economic agenda. Chances for wider global economic disruption are high, not low.

- Monthly data show China’s industrial output slowed to 6 percent year-on-year in December from 6.2 percent, fixed asset investment decelerated to 8.1 percent year-to-date in December from 8.3 percent in November. Retail sales gained steam, rising 10.9 percent, up from 10.8 percent. Together, this data points to a moderation in momentum headed into the start of 2017.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 1.9 percent. The second round of voting for the constitutional amendment package started this week, and a referendum on the Executive Presidency is likely to take place in the first half of April. Next week the central bank of Turkey will meet and Fitch will review the country’s credit rating.

- The Polish zloty was the best performing currency this week, gaining 91 basis points against the U.S. dollar. Fitch ratings agency affirmed Poland’s Long-Term Foreign and Local Currency Issue Default Ratings at “A-“, with a stable outlook. Fitch’s decision was supported by solid fundamentals, including a healthy banking system and sound monetary framework.

- The telecommunication service sector was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 1.9 percent. European auditors want Greece to secure additional tightening measures of 700 million euros ($746 million) in order to meet the fiscal target for 2018. About 500 million euros of these measures have been agreed to so far.

- The Turkish lira was the worst performing currency this week, losing 1.3 percent against the U.S. dollar. Despite measures that were implemented in order to support the lira, the currency is still weakening. A significant rate hike is needed to save the currency; however, the central bank may not be able to raise rates before the referendum on the Executive Presidency.

- The real estate sector was the worst performing sector among eastern European markets this week.

Opportunities

- The European Central Bank (ECB) decided to leave its main interest rate unchanged and will continue to make asset purchases of 80 billion euros ($84.2 billion) a month until the end of March. The bank will make asset purchases of 60 billion euros a month from April to December. Mr. Draghi said that inflation will likely rise more rapidly than the policymakers expect over the coming months, thanks to higher oil prices, but characterized the state of underlying inflationary pressure as “weak.”

- Czech Republic’s sovereign debt will be rated by Standards & Poor after the close on Friday. The expectation is that there will be no change to the rating; S&P will keep Czech at Investment grade “A” with a stable outlook. The country’s rating has been improving steadily, fostering a downward trend in yields on Czech government bonds. The yields have been falling at all maturities over the past 15 years, except for the period of monetary turbulence and at the start of the financial crisis in 2007–2008, and are currently at historic lows.

- Today Melania Trump became only the second First Lady not born in the United States. Melania Trump was born as Melanija Knavs in Slovenia, a small country located in southern Central Europe, bordering with Italy, Austria, Hungary, Croatia and the Adriatic Sea. Slovenia gained its independence from Yugoslavia during the 1991 collapse of communism. Her success of becoming First Lady could draw attention to her birthplace.

Threats

- The euphoria over Vladimir Putin having an admirer in The White House is declining. Rex Tillerson, Trump’s nominee for secretary of state who is also a former Exxon Mobile chief and who has known Putin since 1999 (and received a medal of friendship from him in 2012), called Russia a “danger” to U.S. interests. Andrew Kortunov, director of the Russian International Affairs Council, said Tillerson’s testimony shows how deeply anti-Russian sentiment is running in Washington.

- In Poland, the Development Ministry has presented a proposal to liquidate interchange fee completely and ban bank fees on issuing and using ATM cards and current accounts. The move is aimed at limiting the circulation of cash, which should reduce the shadow economy and cut the cost of administration. However, the proposal is negative for banks as the cost for the banks could reach PLN 1.5-4 billion.

- Russia’s government is working on measures to limit the ruble’s volatility. One of the options the government has is to buy foreign currency, and the buying will be limited to the amount of excess revenue the government gets from higher-than-forecast oil prices. The Russian budget is based on the crude oil price of $40 per barrel. At an average oil price of $50 per barrel, Russia will get an extra 1 trillion rubles ($16.7 billion) in revenue this year. Should the central bank use the whole amount to buy foreign currency, the ruble will weaken by 2 to 3 percent against the U.S. dollar, according to Raiffeisenbank JSC and Renaissance Capital.

© US Global