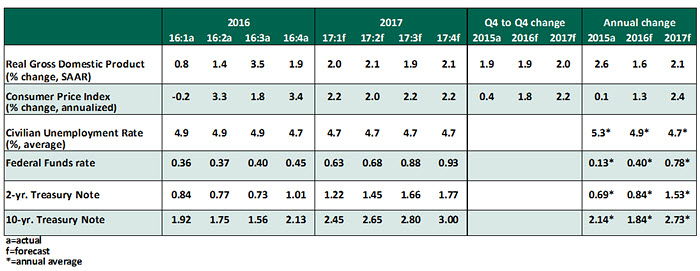

Despite a great deal of news volatility, the U.S. economic landscape is satisfactorily stable. Growth continues, and inflation is not overly threatening. We continue to await further clarity on fiscal policy, which may be some time in coming. As such, our growth forecast does not reflect much of a “Trump Bump.” Real gross domestic product (GDP) grew at an annual rate of 1.9% in the fourth quarter, versus a 3.5% increase in the prior quarter. A large reduction in exports was one reason for slower GDP growth. Growth should be a little better than this going forward, but not by much.

Key Economic Indicators

Key Elements of the Forecast

- Consumer spending slowed in the fourth quarter to an annual rate of 2.5%, despite the large increase in auto sales (18.1 million units in fourth quarter vs. 17.5 in the third). Outlays on both goods and services advanced, but the latter showed a more marked deceleration than the former. Auto sales dipped in January, which likely will trim the pace of overall consumer spending in the first quarter.

- The much-awaited pickup in capital spending may have started in the fourth quarter. Business equipment expenditures, which have been weak since the end of 2015, rose 3.1%. The Institute for Supply Management’s composite index climbed to 56 in January, the highest since November 2014. Other business sentiment surveys remain positive and support expectations of an increase in business spending.

- The housing market faces mixed currents. Favorable employment and income trends point to further housing-sector growth, but rising mortgage rates will be a drag. Residential investment expenditures grew 10.2% in the fourth quarter after two quarterly declines. Sales of new homes fell in December, but advanced at a strong clip (+11.8%) overall in 2016. Although purchases of existing homes slipped in December, the year ended as the best in a decade.

Data indicate that in 2016, home prices hit all-time peaks in 44% of the 201 metro areas with populations of at least 200,000. According to the National Association of Realtors, the marketplace had only a 3.6-month supply of unsold existing homes during December 2016, which is the lowest level since it began tracking the supply of homes in 1999.

A 4.8% unemployment rate and a 227,000 increase in payroll employment in January represent sanguine conditions in the labor market. However, the deceleration in wage growth (+2.5% vs. +2.8% in December) and the dip in Employment Cost Index in the fourth quarter (2.2% vs. 2.3% in the third quarter) suggest that wage pressures are mostly contained. The share of long-term unemployed and those employed part time moved up in January. These elevated levels of these measures compared with the pre-recession readings imply some slack in the economy that is holding back wage growth.

The personal consumption expenditure price index increased 1.6% from December 2015. In the past 12 months, overall inflation has moved up nearly 100 basis points, largely due to increases in the price of oil. Core inflation, which excludes food and energy, stands at 1.70% over the last year, only 30 basis points higher than a year ago. The case for further firming of inflation readings is solid, particularly given that the economy is nearly at full employment.

Fiscal policy under the new administration is evolving. The border adjusted tax is a widely discussed proposal (see comments here), and the latest signals from policymakers are unclear. An expansionary fiscal policy is likely to not only increase growth, but it will raise inflationary pressures.

In this context, the Federal Reserve is placed in a tough spot. Until the size, timing, and composition of the fiscal program and other policy changes are known, the Federal Open Market Committee will be operating in an uncertain environment. Therefore, the Fed is expected to adopt a cautious approach to changes in monetary policy in the near term. We expect the Fed to raise the policy rate twice in 2017, in June and December.

The 10-year U.S. Treasury note yield has been range-bound in the last few weeks after a post-election bump. Bullish economic data, higher energy and commodity prices, and new highs for equity prices present a positive view of economic conditions. Nevertheless, higher inflation, challenges from China, and elections in France and Germany are risks the markets will be watching closely.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2017 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust