Gold Gets a Shot in the Arm from Inflation and China

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

|

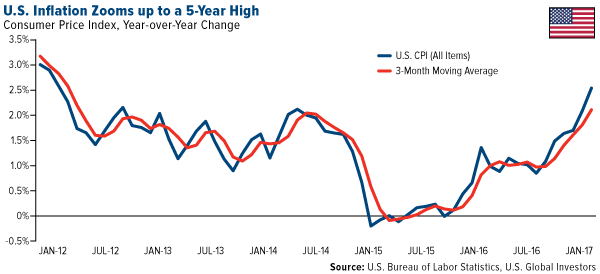

Inflation just got another jolt, rising as much as 2.5 percent year-over-year in January, the highest such rate since March 2012. Led by higher gasoline, rent and health care costs, consumer prices have now advanced for the sixth straight month. In addition, January is the second straight month for rates to be above the Federal Reserve’s target of 2 percent.

Air fares are also climbing, and speaking of air fares, billionaire investor Warren Buffett added to his domestic airline holdings, we learned this week. Buffett’s holding company, Berkshire Hathaway, is now the second-largest holder of American Airlines, with an 8.79 percent share of the company. It also increased its holdings in Delta Air Lines by over 800 percent, to 60 million shares. The company now owns 43.2 million shares of Southwest Airlines, and it increased its stake in United Continental to about 28 million shares.

What else is driving the airline industry?

A March rate hike now looks all but imminent. Many economists—including the Goldman Sachs economists I had the pleasure to hear speak this week—expect to see at least three such hikes this year alone.

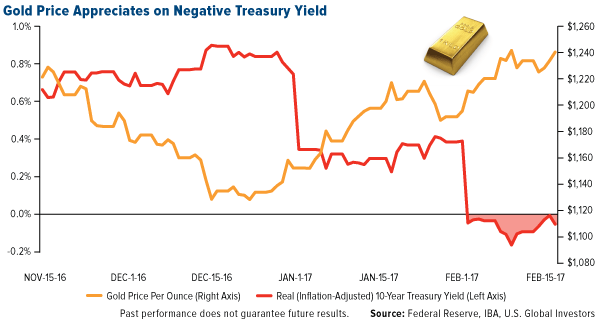

Gold responded accordingly, closing above $1,240 for the first time since soon after the November election. Below you can see the gold price charted against the inflation-adjusted 10-year Treasury yield, which is now in subzero territory.

The question I have is: Why would an investor deliberately choose to lose money? But that’s precisely what’s happening now with inflation where it is.

| 2-Year | 3-Year | 10-Year | |

|---|---|---|---|

| Treasury Yield | 1.22% | 1.95% | 2.45% |

| Consumer Price Index | 2.50% | 2.50% | 2.50% |

| Real Yield | -1.28% | -0.55% | -0.05% |

|

As of February 16

|

Source: Federal Reserve, U.S. Global Investors

|

||

These were among some of the topics addressed by former Fed Chair Alan Greenspan, who spoke with the World Gold Council (WGC) for the winter edition of its “Gold Investor.”

|

"Significant increases in inflation will ultimately increase the price of gold,” Greenspan said. “Investment in gold now is insurance. It’s not for short-term gain, but for long-term protection.”

He also reiterated his view, which I share, that gold is much more than just a metal but a currency:

I view gold as the primary global currency. It is the only currency, along with silver, that does not require a counterparty signature. Gold, however, has always been far more valuable per ounce than silver. No one refuses gold as payment to discharge an obligation. Credit instruments and fiat currency depend on the credit worthiness of a counterparty. Gold, along with silver, is one of the only currencies that has an intrinsic value. It has always been that way. No one questions its value, and it has always been a valuable commodity, first coined in Asia Minor in 600 BC.

Although major stock indices continued to hit fresh all-time highs this week on hopes of tax reform and fiscal stimulus, it’s important to temper the exuberance with a little prudence. The bull market, currently in its eighth year, is facing some significant geopolitical and macroeconomic uncertainty, and we could be getting late in the economic cycle. This makes gold’s investment case even more attractive. For the 10-year period, the yellow metal has shown an inverse correlation to risk assets such as stocks and high-yield bonds. It might be time to ensure that your portfolio has the recommended 10 percent in gold—that includes 5 percent in gold coins and jewelry, the other 5 percent in quality gold equities and mutual funds.

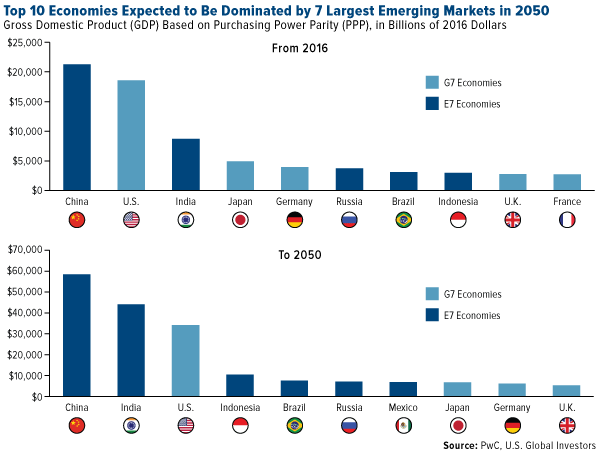

The long-term investment case for gold looks just as compelling following bullish reports this week from PricewaterhouseCoopers (PwC) and Morgan Stanley. China and India are the world’s top two consumers of gold, and both countries are expected to make huge economic gains in the next few decades. This is likely to boost gold demand even more, which has a high correlation with discretionary income growth.

China alone consumed approximately 2,000 metric tons in 2016, or roughly 60 percent of all the new gold that was mined during the year, according to veteran mining commentator Lawrie Williams, who based his estimates on calculations made by BullionStar’s Koos Jansen. The 2,000 metric tons is a much higher figure than what analysts and the media have been telling us, but I’ve always suspected China’s annual consumption to run higher than “official” numbers.

According to PwC’s models, China and India should become the world’s number one and number two largest economies by 2050 based on purchasing power parity (PPP). China, of course, is already the largest economy by that measure, but PwC sees the Asian giant surpassing the U.S. economy on an absolute basis by as early as 2030.

As for India, it “currently comprises 7 percent of world GDP at PPP, which we project to rise steadily to over 15 percent by 2050,” PwC writes. “This is a remarkable increase of 8 percentage points, gaining the most ground of any of the countries we modeled.”

I think it’s also worth highlighting Indonesia, which is expected to replace Japan as the fourth-largest economy by midcentury. E7 economies, in fact, could end up dominating the top 10, with Mexico moving up to number seven and France dropping off. You can see the full list on PwC’s site.

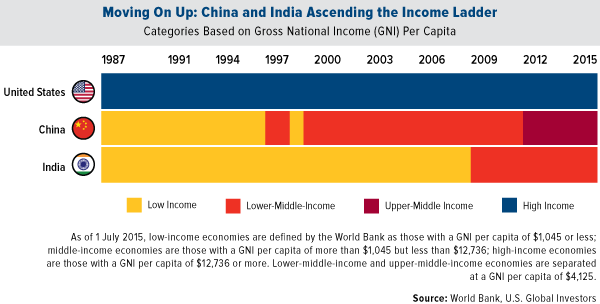

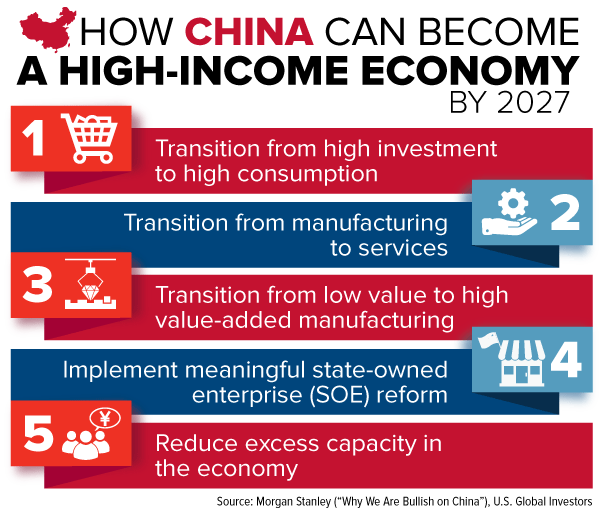

China Set to Become High Income by 2027

Then there’s Morgan Stanley’s 118-page report, “Why we are bullish on China.” The investment bank sees a number of dramatic changes over the coming years, the most significant being China’s transition from a middle-income nation to a prosperous, high-income nation sometime between 2024 and 2027. (The high-income threshold is a gross national income (GNI) of around $12,500 per capita.) This would make China one of only three countries with populations over 20 million that have managed to accomplish this feat in the past 30 years, the other two being South Korea and Poland.

This trajectory is supported by a number of expectations, including, most importantly, Morgan Stanley’s confidence that China will manage to avoid a debt-related financial crisis, as some investors might now believe is forthcoming. The bank’s view is that the Chinese government will successfully provide “adequate policy buffers and deft management of the policy cycle” to ensure the growth of per capita incomes.

In addition, since President Donald Trump has officially withdrawn the U.S. from the Trans-Pacific Partnership (TPP), China could very well use this as an opportunity to take the lead in global trade, Morgan Stanley writes. This view aligns with comments I’ve previously made. China is already reportedly weighing its options with two alternative free-trade agreements (FTAs), one that includes the U.S. (the Free Trade Area of the Asia Pacific) and one that does not (the Regional Comprehensive Economic Partnership). It’s probably safe to say, however, that given Trump’s opposition to FTAs, trade negotiations involving the U.S. are unlikely to happen anytime soon.

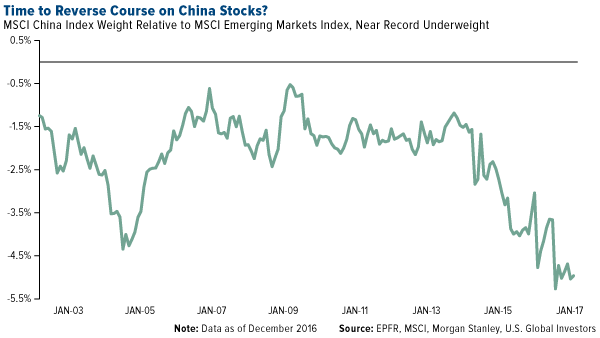

Investors Underweight China

Taken together, this is all good news for gold. Again, when incomes rise in China and India, gold demand has historically benefited.

But it also makes China a compelling place to invest in. And yet investors have tended to be shy, underweighting the country for at least a decade in relation to the broader emerging markets universe.

This, despite the fact that China has largely outperformed emerging markets for the last 15 years. According to Morgan Stanley, the MSCI China Index has delivered a compound annual growth rate (CAGR) of 13 percent for the 15-year period, versus the MSCI Emerging Markets Index’s CAGR of 10 percent over the same period.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.75 percent. The S&P 500 Stock Index rose 1.51 percent, while the Nasdaq Composite climbed 1.82 percent. The Russell 2000 small capitalization index gained 0.79 percent this week.

- The Hang Seng Composite gained 1.54 percent this week; while Taiwan was up 0.97 percent and the KOSPI rose 0.27 percent.

- The 10-year Treasury bond yield rose 1 basis point to 2.42 percent.

Domestic Equity Market

Strengths

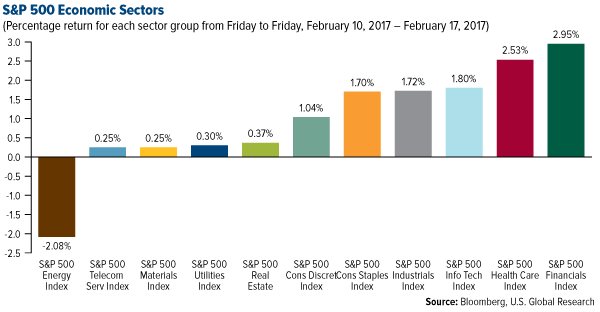

- Financials was the best-performing sector of the week, increasing 2.95 percent versus an overall increase of 1.38 percent for the S&P 500 Index.

- St. Louis-based Mallinckrodt Pharmaceuticals was the best-performing stock for the week, increasing 11.10 percent.

- Goldman Sachs is at an all-time high. Wednesday's session not only marked Goldman's second straight close in record territory but saw shares eclipse the October 2007 all-time high of $250.70 a share.

Weaknesses

- Energy was the worst-performing sector for the week, falling 2.08 percent.

- TripAdvisor was the worst-performing stock for the week, falling 9.50 percent.

- TOSHIBA tumbled after announcing its massive write-down. The Japanese company fell more than 10 percent at its open in Tokyo following its announcement that it was taking a $6.3 billion write-down on its U.S. nuclear unit, Reuters reports.

Opportunities

- This week, Warren Buffett's Berkshire Hathaway disclosed a significant commitment to the U.S. airline industry, saying it had raised its stakes in Delta Air Lines and American Airlines and taken a new position in Southwest Airlines. According to a regulatory filing, Buffett purchased $2.2 billion in shares of Southwest. He also owns about $2 billion of American, United Airlines and Delta. The investments total more than $8 billion.

- Snapchat's parent company, Snap Inc., is seeking to price its initial public offering at $14 to $16 a share, setting its valuation below initial expectations. An updated regulatory filing confirmed Snap is looking to sell 200 million class A shares, raising about $3.2 billion.

- Restaurant Brands, which owns Burger King and Tim Hortons, reported a higher-than-expected quarterly profit. Sales at stores open for at least one year climbed while costs fell. The company is interested in buying Popeyes, according to Reuters. A deal would take Popeyes' Louisiana-style fried chicken and biscuits to a global market.

- According to Michael Paulenoff, president of Pattern Analytics, a correction could be on the horizon. He said declining volume in the stock market is one red flag. In the two weeks leading up to the election, about 743 million shares changed hands on the New York Stock Exchange each day. So far this year, NYSE volume is averaging 660 million. That compares to an average of 772 million during all of 2016. "For decades, rising volumes have preceded a rise in prices in the stock market. Likewise, declining volumes lead to a decline in prices," Paulenoff said.

- Cisco sees softness in its core business. The technology company beat on the top and bottom lines but said revenue from its key next-generation network (NGN), switching and data center products decreased 10 percent, 5 percent and 4 percent, respectively.

- Cigna is suing Anthem after walking away from their merger. Cigna has filed a $13 billion lawsuit against Anthem for what it called "the lost premium value to Cigna's shareholders caused by Anthem's willful breaches of the Merger Agreement." Anthem responded by saying the terms of the agreement did not allow Cigna to back out of the merger and that it intended to follow through on the deal.

February 15, 2017Could Streamlining Regulations Benefit Commodities? |

February 15, 2017Frank Holmes: Ignore the Fed “Noise” |

February 14, 2017Understanding the Gold Market with Frank Holmes |

The Economy and Bond Market

Strengths

- The Philly Fed's manufacturing index soared to 43.3 in February, the highest level since 1984. The data shows an increase in current activity as firms report higher sales and shipment.

- Building permits increased by 4.6 percent at a rate of 1.285 million, indicating a forthcoming pickup in construction.

- Retail sales were much stronger than expected in January, climbing by 0.4 percent, according to the Commerce Department. However, a large amount of help came from gasoline sales, as prices continue to increase after the oil crash.

Weaknesses

- Industrial production, the Federal Reserve's gauge of the manufacturing sector, disappointed at the beginning of 2017. It slipped by 0.3 percent, while capacity utilization fell to 75.3 percent from 75.6 percent.

- Eurozone GDP missed estimates. The eurozone's economy expanded at a 0.4 percent rate in the fourth quarter, data provided by Eurostat shows. That was below the 0.5 percent that economists were anticipating.

- The Japanese economy grew at a 0.2 percent clip in the fourth quarter, missing economists' expectations of 0.3 percent, as growth slowed for the third consecutive quarter.

Opportunities

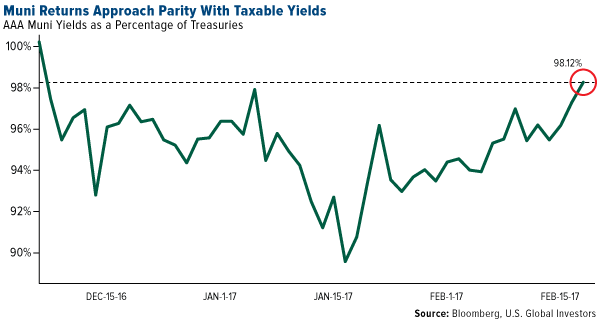

- State and local bonds are looking more attractive amid the uncertainty of the municipal market’s tax-exempt status under the Trump administration. The ratio of yields on an index of top-rated, 10-year bonds against the returns of similarly dated Treasuries rose to 98.12 percent, the most since December 7. Given the unlikelihood of any adverse tax reform, this could present an advantageous entry into municipal bonds.

- The release of the flash purchasing managers’ indices on Tuesday will provide an important indicator of future growth expectations.

- The release of February’s University of Michigan Sentiment report next Thursday will reveal if consumers’ confidence in the economy continues to be robust.

- A solution for Greece remains elusive. Eurozone countries look likely to miss a self-imposed Monday deadline to agree on aid measures for Greece, which is scheduled to run out of cash in July, when it has to make repayments of more than €6 billion.

- According to the Bank of America Merrill Lynch Global Fund Manager Survey out on Tuesday, a higher percentage of investors in February believe the dollar is overvalued than in more than a decade. According to the results, 41 percent of fund managers believe that the "most crowded trade" is being long the U.S. dollar, followed by 14 percent citing short government bonds and 13 percent long U.S. /EU corporate bonds. The BAML Fund Manager Survey questioned 210 investors with a combined $632 billion in AUM.

- Consumer prices rose by the most in four years in January, according to the Department of Labor. The consumer price index (CPI) — comprised of a basket of items ranging from clothes to pills — climbed 0.6 percent month-on-month. While some inflation is good, too much could negatively impact the economy.

Gold Market

This week spot gold closed at $1,235.71, up $2.06 per ounce, or 0.17 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 1.67 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index rose 0.93 percent. The U.S. Trade-Weighted Dollar Index finished the week up by just 0.10 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Feb-14 |

Germany CPI YoY |

1.9% |

1.9% |

1.9% |

|

Feb-14 |

Germany ZEW Survey Current Situation |

77.0 |

76.4 |

77.3 |

|

Feb-14 |

Germany ZEW Survey Expectations |

15.0 |

10.4 |

16.6 |

|

Feb-14 |

U.S. PPI Final Demand YoY |

1.5% |

1.6% |

1.6% |

|

Feb-15 |

U.S. CPI YoY |

2.4% |

2.5% |

2.1% |

|

Feb-16 |

U.S. Housing Starts |

1226k |

1246k |

1279k |

|

Feb-16 |

U.S. Initial Jobless Claims |

245k |

239k |

234k |

|

Feb-22 |

Eurozone Core CPI YoY |

0.9% |

-- |

0.9% |

|

Feb-23 |

U.S. Initial Jobless Claims |

241K |

-- |

239k |

|

Feb-24 |

U.S. New Home Sales |

575k |

-- |

536k |

Strengths

- The best performing precious metal for the week was silver, up 0.31 percent, just edging out the gains in gold. Bloomberg reports that China’s holdings of U.S. Treasuries have dropped by the most on record last year. The second-largest economy has been seeking to rely less on U.S. currency. Japan, which is the largest holder of Treasuries, also sold nearly $202 billion in Treasuries last year. These countries seem to be backing away from financing the U.S. government in the era of the Donald Trump presidency, and concerned about the prospects of rising inflation. Flows into the largest exchange-traded debt fund, featuring Treasury Inflation Protected Securities, increased to $547 million during the past two weeks. Meanwhile, China's gold reserves have held steady.

- Gold has rallied in seven out of eight weeks lately on concerns that the stock rally is done and investors are anticipating that inflation will take off. Analysts at Commerzbank commented that gold is “finding support from a weaker U.S. dollar and falling bond yields. In addition, rate hike expectations have declined.”

- The Perth Mint reports rising sales this year. Neil Vance from The Perth Mint said, “Certainly in terms of geopolitical issues, we still see people moving into precious metals for that safe haven.” In addition to strong sales in the U.S., the mint reported exceptional sales in China, partly due to a popular rooster coin in conjunction with the Lunar New Year.

Weaknesses

- The worst-performing precious metal for the week was palladium, down 0.87 percent. Hedge fund managers boosted their bullish bets on palladium this week to the highest level in three weeks. Jonathan Butler, a precious metals strategist at Mitsubishi in London, commented that “U.S. equities continue to ride high in expectation of Trump’s corporate tax reform, and this has weighted on gold.” Butler went on to say, “Gold is probably going to be on the defensive this week,” based on Federal Reserve Chair Janet Yellen’s testimony.

- Gold imports by India declined in January, due to the government’s actions to limit black money. According to an unidentified source in the finance ministry, overseas purchases were 58.6 metric tons in January, a drop of 28 percent from a year earlier. Imports dropped 41 percent in the first 10 months of the financial year.

- Freeport McMoRan has been on something of a rollercoaster with the government in Indonesia. In January, the company suspended shipments of copper from its Grasberg mine, and earlier this week, the company suspended copper concentrate output. By the end of the week, however, Freeport received approval for exports to resume. The approval would be good for one year, and then under review every six months. The situation will likely remain tense as one analyst we spoke with noted that Indonesian business leaders are arguing over how they will divide up the foreign owned assets of the mining companies operating in country that are being challenged by a government crackdown.

- Gold may get a boost over additional uncertainty due to the turmoil regarding President Trump’s now-former national security advisor Michael Flynn. Flynn resigned Monday amid allegations that he lied about his contacts with a Russian official, and the U.S. intelligence agencies and the FBI are conducting multiple investigations into the extent of improper contact between other members of Trump’s staff and Russia. Trump responded that the real crime is illegal leaks of information.

- Acacia Mining is the latest gold mining company to announce that it is increasing its dividend. Both Pan American Silver and Randgold Resources announced hikes in their dividend in recent days. Acacia will more than double its annual dividend, and its stock climbed on expectations that gold production will increase after extending the life of one of its mines in Tanzania. This is the latest in a trend whereby management at gold mining companies is showing stronger confidence in its operations to increase dividends with more certainty that profits will be sustainable.

- Kyrgyzstan’s central bank is promoting gold saving with its citizens. The country’s rural population still values its assets in cattle, but Governor Tolkunbek Abdygulov says his “dream” is for each citizen to own at least 100 grams, or 3.5 ounces, of gold. Gold is also Kyrgyzstan’s biggest export. “Gold can be stored for a long time and, despite the price fluctuations on international markets, it doesn’t lose its value for the population as a means of savings.”

Threats

- In the fourth quarter, U.S. home-loan delinquencies increased for the first time since 2013. This could be a warning sign for the strength of the overall economy. However, when looking at ETFs that track the Chicago Board Options SPX Volatility Index (VIX), assets have shrunk in an odd indicator of calm as investors are weary of volatility-based losses.

- The World Gold Council published its February issue of “Gold Investor,” which includes an interview with former Fed Chair Alan Greenspan. Greenspan stated: “If the gold standard were in place today, we would not have reached the situation in which we now find ourselves. We cannot afford to spend on infrastructure in the way that we should. The U.S. sorely needs it, and it would pay for itself eventually in the form of a better economic environment (infrastructure). But few of such benefits would be reflected in private cash flow to repay debt.” Greenspan essentially concludes that “the gold standard is a way of ensuring that fiscal policy never gets out of line,” which, clearly, is not a feasible option for the U.S. any longer.

- Inflation came in at 2.5 percent this week, a bit higher than the 2.4 expected. Yellen’s testimony indicated the potential for a rate hike in March, which would be sooner than many expected. Ward McCarthy, chief financial economist for Jefferies in New York, said, “The acceleration in the inflation picture along with the continued strong performance of the consumer sector opens the door and increases the probability that the Fed will raise rates as soon as March.”

Energy and Natural Resources Market

Strengths

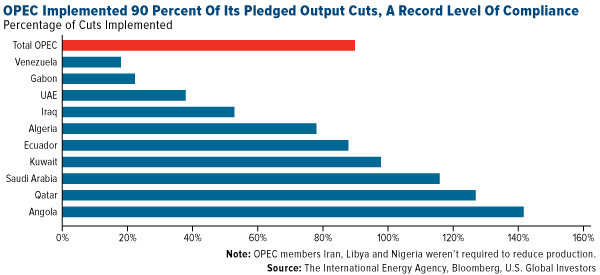

- OPEC hit a record level of initial compliance from November’s agreement. The group has implemented 90 percent of its pledged output cuts which is a record level not seen in past agreements. According to Michael Hinds, an analyst at Goldman Sachs, the oil market could soon start to price in scarcer supply inferring higher prices.

- The best performing sector for the week was the S&P Super Composite Steel Sub Industry Index. The index rose 3.26 percent on the back of rallying steel makers as market participants take place in the reflation trade.

- Bunge Limited, a global agribusiness and food company, was the best performing stock this week finishing up 13.8 percent. The stock rallied on the back of stellar earnings results of $1.70 EPS versus analyst expectations of $1.57 EPS.

Weaknesses

- Natural gas was the worst performing commodity this week falling 6.36 percent. The drop in the price of natural gas was driven by a disappointing inventory draw of 114 billion cubic feet (Bcf), the lowest draw in the last three months.

- The worst performing sector this week was the S&P/TSX Composite Diversified Metals and Mining Sub Industry Index. The index fell 9.6 percent as select members within the group report disappointing earnings results.

- The worst performing stock for the week was First Quantum Minerals, a Vancouver-based metals and mining company. The company fell 11.6 percent on the back of disappointing earnings results of 4 cents EPS versus analyst expectations of 8 cents EPS.

Opportunities

- Global industrial activity is set for a solid 2017, according to Macquarie Bank, a leader in commodity research. The bank highlights that global industrial output grew by 0.96 percent in the fourth quarter of 2016, the best performance since the fourth quarter of 2013. Growth accelerated sequentially in each quarter of last year which marks both an uptrend and momentum. A positive read-through for industrial materials.

- Despite bearish signals, big bets on oil continue according to Reuters. Over the last two weeks, U.S. stockpiles have reached their largest levels ever recorded; however, market participants continue to position themselves as OPEC cuts may result in a market rebalancing. A positive read-through for oil.

- Copper prices continue to rally on the back of the strike at BHP Billiton’s mine, Escondida, the largest copper mine in the world. As no progress has been made to resolve the strike at the mine, supply continues to remain constricted adding pressure to prices globally. However, analysts at Argonaut securities in Hong Kong believe that participants have yet to price in improving economic fundamentals in China which may result in further gains in the long term. A positive-read through for copper.

Threats

- The German steel federation sees Chinese overcapacity persisting, according to Reuters. China’s overcapacity was 360 million tonnes last year and is expected to remain well above 300 million tonnes by 2020. A key determinant to the commodities demand is construction activity in China. In order to reduce the current oversupply that exists, China must experience robust growth in the coming quarters and years. A negative read-through for long-term steel prices.

- The future of coking coal’s rally is in question according to Don Lindsay, the CEO of Teck Resources. Mr. Lindsay stated that coking coal groups must wait on supply clues from Beijing policymakers in the weeks to come. As coking coal is the leading ingredient in steel making and the country reduces production to reduce oversupply, coking coal prices may fall in the months to come.

- Stock levels for food commodities are at record levels, according to analyst Carlos Mera of Rabobank, a leading global food and agribusiness bank. Mera states that in addition to record inventory levels of various agricultural commodities, major economic and geo-political headwinds are shifting supply and demand dynamics for the world’s largest consumers, China and India, which may potentially put downward pressure on various agricultural commodities in 2017. A negative read-through for agricultural commodities.

China Region

Strengths

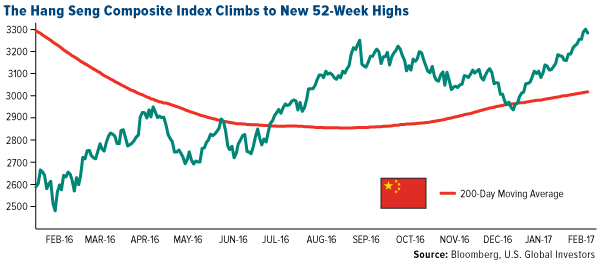

- The Hang Seng Composite Index (HSCI) climbed to new 52-week highs this week, rising 1.62 percent.

- According to Bloomberg, a once-popular trade against Chinese-listed stocks in Hong Kong is starting to fizzle out. As global equity markets have rallied, perhaps surprising naysayers, the short interest on BlackRock’s Hong Kong-listed A-shares ETF dropped to a one-year low.

- Chinese bank stocks are taking off this week, reports Bloomberg, drawing investor interest at least in part because of the banks’ cheapness and relatively high dividend yields. “A rising rate environment that is based on an improving economic foundation is good for the banks,” said Richard Xu, an analyst at Morgan Stanley in Hong Kong.

Weaknesses

- Indonesia’s Jakarta Composite Index fell 0.39 percent for the week, among the worst regional performers.

- As authorities stepped up scrutiny of overseas acquisitions and other deals to keep money from leaving the country, China saw last year’s record outbound investment slump last month, reports Bloomberg. The decline was mainly due to the prior year’s high base and distortions caused by the recent week-long Lunar New Year holiday, the article continues.

- A South Korean court approved a special prosecutor’s second request for the arrest of Samsung heir and leader Lee Jae-Yong (“Jay Y. Lee”), according to Bloomberg. Lee, who has been the de facto head of Samsung since his father was hospitalized in 2014, now faces allegations of bribery, perjury and embezzlement.

Opportunities

- Chinese companies have had their eye on cracking the U.S. auto market with low-cost passenger vehicles for some time now, reports Bloomberg. With some anticipation of Trump’s “America First” policies, they’re buying up American parts makers at a record pace instead. There were at least seven announced auto-related deals in the U.S. involving Chinese companies last year, the article continues.

- The China Financial Futures Exchange announced that it will relax restrictions on the domestic stock-index futures trading, according to Bloomberg. Margin requirements and fees will be lowered, and according to industry leaders, the relaxed measures should boost market liquidity and trading activity.

- China’s Foreign Minister Wang Yi told U.S. Secretary of State Rex Tillerson on Friday (in their first face-to-face meeting since Tillerson took up his job), that the common interests shared by China and the U.S. far outweigh the countries’ respective differences, reports Reuters. "China and the United States have joint responsibility to maintain global stability and promote global prosperity, and both sides' joint interests are far greater than their differences," Wang said during the meeting.

Threats

- China continues to brace for the possibility of tension with U.S. President Donald Trump, reports Bloomberg. According to people familiar with the matter, China is asking companies this month to estimate the highest duties they can bear in preparation for possible U.S. tariffs.

- Although India, Indonesia, Malaysia and Vietnam have largely escaped U.S. President Trump’s glare on trade issues, the U.S. does run trade deficits will all of them. These countries could be particularly vulnerable to attack, reports Bloomberg news. “Trade deficits are a problem. At any moment there could be an angry Donald Trump in your face or a Twitter coming your way,” said Deborah Elms, executive director of the Asian Trade Centre. “Have other countries woken up to this problem? Perhaps not.”

- This week was an eventful one for North Korea headlines: allegations of a bizarre North Korean-sponsored assassination of the estranged potential rival and half-brother of Kim Jon Un in a Kuala Lumpur airport, and a confirmed ballistic missile test to boot. China’s foreign ministry opposed North Korea’s ballistic missile test and called on all sides to avoid escalating tensions, reports Bloomberg. This was the first provocation from Kim Jong Un’s regime since U.S. President Trump took office.

Emerging Europe

Strengths

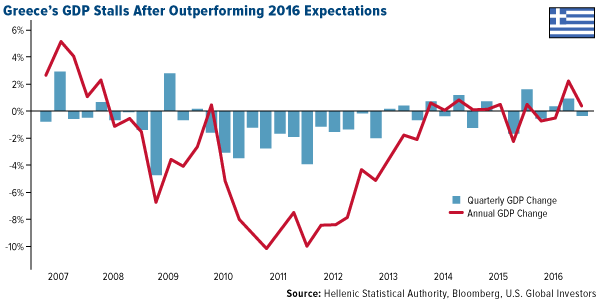

- Greece was the best performing country this week, gaining 2.5 percent. Greece is working on its second review with creditors and it is possible that bailout deal could be reached soon.

- The Turkish lira was the best performing currency this week, gaining 1.9 percent against the U.S. dollar. The currency continues its recovery after depreciating 15 percent in the fourth quarter of last year as central banks continue to use unconventional moves to support the lira.

- The health care sector was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 1.6 percent. Russia posted a January budget deficit of 23.4 billion rubles ($406.05 million) while Bloomberg’s survey forecasted a 225 billion ruble surplus. Brent crude oil declines by 1.7 percent and closed at $55.43 per barrel.

- The Polish zloty was the worst performing currency this week, losing 1.1 percent against the U.S. dollar. According to Marcin Sulewski from Bank Zachodni, the zloty is correcting after somewhat excessive gains at the start of the year, predicting the downward move to continue next week.

- The telecommunications sector was the worst performing sector among eastern European markets this week.

Opportunities

- After nearly eight years of talks, European Union lawmakers approved the EU-Canada Comprehensive Economic and Trade agreement CETA on Wednesday. It will go into provisional effect and lift tariffs on roughly 9,000 industrial, agricultural and food items. The European Commission said CETA is expected to give a 23-percent boost to bilateral trade that was worth EUR63.5 billion of goods in 2015 and EUR 27.2 billion in service in 2014. CETA’s full implementation still requires ratification by more than 30 national and regional parliaments in the EU.

- Next week preliminary PMI data for February will be released and Bloomberg economists predict strong results once again. Manufacturing PMI is expected to be at 55, Service PMI at 53.8, and Composite at the 54.4 level.

- Retail sales in Poland surged an annual 11.4 percent last month, compared with a gain of 6.4 percent in December. Industrial production increased 9 percent, topping estimates, and construction surprised by growing 2.1 percent. Social spending and a program of child benefits have helped offset the decline in aid from the EU. Now gains in manufacturing, investment and exports are setting the stage for quicker growth to continue.

Threats

- The Greek economy unexpectedly contracted in the fourth quarter of 2016. Gross domestic product fell 0.4 percent in the final three months of last year after growing 0.9 percent in the previous quarter. The median estimate in a Bloomberg survey was a 0.4 percent expansion. Most of the recovery in the third quarter was driven by consumption, but people were more cautious with their spending toward the end of the year.

- Political uncertainty will continue to affect markets this year; Credit Suisse Group AG Chief Executive Officer Tidjane Thiam said this week. Populist candidates in the Netherlands, France and Germany are creating fear of the breakup of the European Union. Deutsche Asset Management has cut European holdings in its multiasset funds to the lowest on record due to how European elections may impact markets.

- Resignation of Michael Flynn, U.S. National Security Advisor, is a negative signal to Russia, according to Leonid Slusky, chairman of the international affairs committee in the state of Duma, parliament’s lower house. Flynn was the most publically positive figure on Russia among Trump’s key foreign policy staff, and his departure could be a precursor of a more natural/negative stance from Trump toward Russia.

© US Global Investorss

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All