Disrupt… Or Get Disrupted

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

This week I was in Vancouver attending YPO EDGE, the annual summit for business executives from more than 130 countries. YPO, which stands for Young Presidents’ Organization, has roughly 24,000 members worldwide. Together, they employ 15 million people and generate a massive $6 trillion in revenue annually.

What I appreciate about YPO is that it stresses peer-to-peer learning. Those who think it’s all about networking and cutting deals are missing the point.

The theme this year was disruption—how innovative breakthroughs in technology, medicine, transportation, machine learning and more have transformed, and will continue to transform, the world we live and work in.

|

“Disrupt, or get disrupted,” John Chambers, executive chairman and former CEO of Cisco, said during his conversation with CNBC’s Tyler Mathisen.

Chambers was speaking specifically of what he calls the “digital era,” which will soon replace the information age. The internet of things is expanding very aggressively right now, but it’s still in its infancy. In 10 to 15 years, Chambers says, more than 500 billion devices worldwide will be connected to the internet. This will irrevocably change how we live our daily lives, conduct business, deploy health care, invest and more.

So what does this mean? For one thing, Chambers estimates that as much as 40 percent of companies now in operation around the world will not exist “in a meaningful way” sometime within the next two decades. To survive, companies will need to reinvent themselves by integrating digitization into the fabric of their business strategy. In the world Chambers imagines, every company will be, at its core, a technology company, and data will become the new oil.

After his presentation, I had the pleasure to share a few words with Chambers in private. I was amazed to hear that, during his tenure as CEO in the 1990s, Cisco had an unbelievable compound annual growth rate (CAGR) of 65 percent. I was even more amazed to hear that he managed to turn 10,000 of his employees into millionaires. I don’t know if that’s a record, but it wouldn’t surprise me if it was. He told me that he wouldn’t be able to do the same today because of our current tax laws. In any case, Chambers embodies all that makes America great—curious, innovative, forward-thinking and willing to share his share his success with his employees.

How to Pick Home Run Stocks, According to Moneyball

A lot of what Chambers talked about during his presentation reminded me of one such disruptor, Billy Beane, the former general manager of the Oakland A’s and subject of Michael Lewis’ 2003 bestseller Moneyball: The Art of Winning an Unfair Game, which was later turned into a 2011 film starring Brad Pitt. Despite being about baseball, it’s one of the best books on stock-picking ever written.

|

For those unfamiliar, Moneyball tells the story of the A’s’ famous 2002 season and Beane’s efforts to build a competitive team despite a lack of revenue and the recent loss of several key players, among other disadvantages. Making matters worse, conventional factors for selecting new players—long perpetuated by the “wisdom” of industry insiders—had grown stale, antiquated… and just plain wrong. Appearance, personality and other biased perceptions were still very much part of the selection process.

With little else left to lose, Beane focused on what he felt were better indicators of offensive performance, including on-base percentage and slugging percentage. This allowed him to cut through the biases and find overlooked, undervalued, inexpensive players. “An island of misfit toys,” as Jonah Hill’s character Peter Brand puts it in the movie.

Beane, in other words, became a value investor—one who depended not on emotion or “instinct” but empiricism and quantitative analysis. All of the picks who fell into his model were mathematically justified.

The strategy worked better than anyone expected. Although the A’s had one of the lowest combined salaries in Major League Baseball, they finished the year first in the American League West. Their winning streak of 20 consecutive wins that season remains the longest in American League history.

| Team | Number of Wins | Season | |

|---|---|---|---|

| A’s | 20 | 2002 | |

| White Sox (tie) | 19 | 1906 | |

| Yankees (tie) | 19 | 1947 | |

| Royals | 16 | 1977 | |

| Mariners (tie) | 15 | 2001 | |

| Red Sox (tie) | 15 | 1946 | |

| Twins (tie) | 15 | 1991 | |

| Source: MLB, U.S. Global Investors | |||

Beane changed the game—literally. Today, nearly every club in the MLB relies on “sabermetrics,” or baseball statistics, to select players. This helps them develop a “portfolio” of constituents whose overlooked potential gives the club the greatest odds possible of outperforming the “market.”

As active managers, we try to do the same. Like Beane, we use a host of quantitative, top-down and bottom-up factors to help us find the most undervalued precious metals and resource stocks.

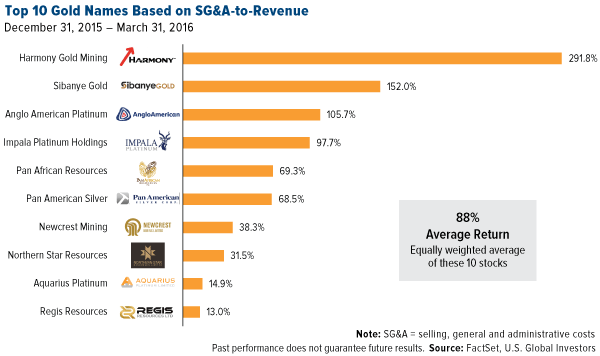

One such factor, low SG&A-to-revenue, I shared with you back in September. “SG&A” stands for “selling, general and administrative expenses” and refers to the daily operational costs of running a company that are not related to making a product. It stands to reason that a company with lower-than-average expenses relative to its revenue might have wider margins than a company with oversized expenses, but few investors look at this metric outside of quants.

Using this factor, we found 10 names whose average returns in the first quarter of 2016 amounted to a phenomenal 88 percent—nearly double what the Market Vectors Gold Miners ETF (GDX) returned over the same three-month period.

Of course, a company must meet several other factors before it qualifies for our models, but this is just one example of the type of rigorous quantitative analysis we conduct.

Probability Is in the Pudding

In Moneyball, Lewis quotes Dick Cramer, cofounder of STATS, a sports statistics company: “Baseball is a soap opera that lends itself to probabilistic thinking.”

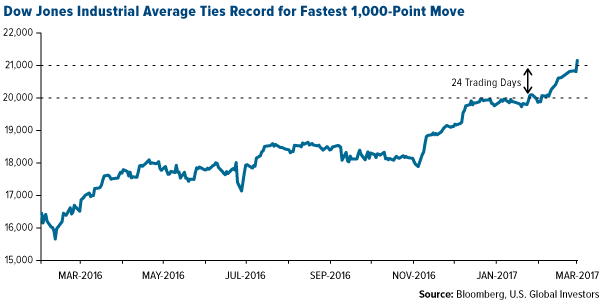

The world of investing is the same, and lately there’s been no better soap opera than watching the major indices hit near-daily all-time highs on hopes that President Donald Trump and the Republican-controlled Congress can lower taxes, slash regulations and find the money to invest in the military and infrastructure. On Monday this week, the Dow Jones Industrial Average posted its 12th straight day of gains, a winning streak we haven’t seen in 30 years. And on Wednesday, it tied a previous record, set in 1987, for the fastest 1,000-point move. It took only 24 trading days for the Dow to surge from 20,000 to 21,000. (Since then it’s fallen below that mark.)

But like baseball, investing lends itself to probability thinking, and here we have experience as well.

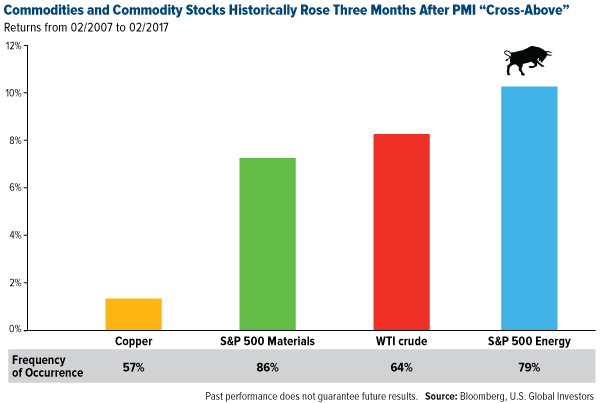

As I’ve said a number of times before, we closely monitor the monthly Global Manufacturing Purchasing Managers’ Index (PMI) because it’s forward-looking rather than backward-looking, like gross domestic product (GDP). As such, we’ve found a high correlation between the PMI reading and the performance of commodities and energy one, three and six months out. When a “cross-above” occurs—that is, when the monthly reading crosses above the three-month moving average—it has historically signaled a possible uptrend in crude oil, copper and other commodities. Our research shows that between February 2007 and February 2017, the S&P 500 Energy Index rose 10.2 percent, 79 percent of the time after a “cross-above,” while the S&P 500 Materials Index rose 7.2 percent, 86 percent of the time. Knowing this helps us anticipate the opportunities ahead.

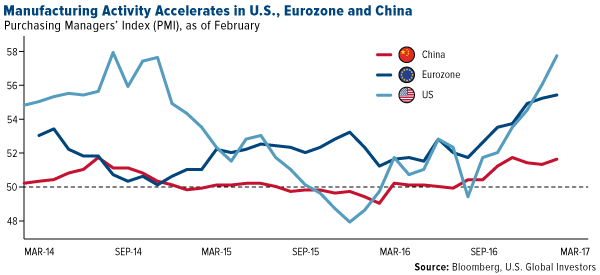

In February, the global PMI rose to 52.9, a 69-month high. It was also the sixth straight month of manufacturing expansion, which bodes well for commodities, materials, miners and other key assets we invest in.

Individual PMI readings for the U.S., eurozone and China—which together make up about 60 percent of global GDP—all advanced in February.

The eurozone’s reading of 55.4 was its highest since April 2011, with expansion being led by the Netherlands, Austria and Germany. The region is more optimistic about the future than at any time since the debt crisis, and the weakened euro has provided a welcome tailwind to help boost sales and exports.

China’s PMI held above 50.0, indicating industry expansion, for the seventh straight month in February on improved new order inflows, higher demand and greater optimism.

The U.S., meanwhile, ended the month with an impressive 57.7, its highest reading since August 2014. Of the 18 manufacturing industries that are tracked, 17 reported growth, including machinery, computer and electronic products, metals, chemical products and others. New orders rose significantly, from 60.4 in January to 65.1 in February, as did backlog of orders, which advanced a whopping 7.5 percent.

Mark Your Calendars!

Join me later this month in St. Petersburg, Florida, for the 19th Anniversary Investment U conference! I’ll be speaking on gold, airlines and infrastructure. Tickets are now available. I hope to see you there!

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.88 percent. The S&P 500 Stock Index rose 0.67 percent, while the Nasdaq Composite climbed 0.44 percent. The Russell 2000 small capitalization index lost 0.03 percent this week.

- The Hang Seng Composite lost 1.32 percent this week; while Taiwan was down 1.05 percent and the KOSPI fell 0.73 percent.

- The 10-year Treasury bond yield rose 16 basis points to 2.48 percent.

Domestic Equity Market

Strengths

- Financials was the best performing sector of the week, increasing by 2.02 percent versus an overall increase of 0.67 percent for the S&P 500.

- Albemarle was the best performing stock for the week, increasing 12.74 percent.

- Snap Inc. had a monster debut. Shares of the social-media company shot up 44 percent in its market debut to close at $24.48 a share, giving Snapchat's parent company a market cap of more than $33 billion. Snap is now bigger than Macy's ($10 billion), Twitter ($11.3 billion), American Airlines ($23.6 billion), and Target ($32.9 billion).

Weaknesses

- Telecommunications was the worst performing sector for the week, falling -1.13 percent versus an overall increase of 0.67 percent for the S&P 500.

- Frontier Communications was the worst performing stock for the week, falling -14.84 percent.

- Hershey is eliminating 15 percent of its workforce. The chocolate maker says that it is embarking on a multiyear program to improve profitability and that it expects that program to incur pretax charges of $375 million to $425 million and provide $80 million to $100 million in benefits. Shares tumbled as much as 7 percent after Tuesday's closing bell.

Opportunities

- Weight Watchers exploded after beating on earnings and guidance. Shares rallied by as much as 15 percent after the company announced earnings of $0.20 a share, swinging from a loss in the same period a year ago, and guidance that easily outpaced expectations.

- Apple ticked up as Buffett bought more shares. Buffett more than doubled his holding as of December 31, raising his stake in Apple to about 133 million shares. Buffett also revealed a $1.6 billion gain in his Apple investment.

- Two of the biggest local-TV station owners in the U.S. are talking about a deal. Sinclair Broadcast Group has approached its rival Tribune Media about a potential combination, Reuters reports.

Threats

- Stocks have rallied more than 11 percent since the election amid speculation that President Trump's plans to cut taxes, roll back regulations, and spend $1 trillion on infrastructure will get the U.S. economy growing at the 3 percent that the administration has targeted. While stocks look unstoppable right now, there have been a number of warning signs — from declining volumes to a mismatch in volatility expectations and economic uncertainty — suggesting traders should tread carefully. The latest is coming from the bond market. As the stock market heats up, so too are the expectations that the Fed will hike rates. World Interest Rate Probability data provided by Bloomberg suggests a 90 percent chance the Fed will raise its benchmark interest rate at its upcoming meeting on March 14/15. And as rate hike expectations rise, traders are dumping Treasuries. That selling is causing a bearish flattening of the yield curve, meaning that yields on shorter-term debt are rising faster than yields on long-term debt. While the yield curve isn't yet inverted, often times a sign that a recession is coming, the spread is the tightest it's been since 2007.

- Caterpillar facilities in Illinois were searched by law enforcement authorities with a warrant. The Peoria Journal Star newspaper reported that people with Internal Revenue Service jackets were seen entering the headquarters. Caterpillar shares fell 4 percent on the news.

- Costco same-store sales miss. The warehouse club retailer reported that same-store sales rose by 3 percent in its second quarter, missing the 3.2 percent gain that analysts were forecasting. The company also announced that it planned to raise membership fees as of June 1. Target missed on sales, earnings and guidance. Earnings came in at $1.45 a share against expectations of $1.51 per share. Additionally, the retailer said sales fell by 1.5 percent for the quarter, below analyst projections of 1.3 percent.

March 1, 2017The Diversification Benefits of Gold |

February 27, 2017This Natural Gas Opportunity Is Years in the Making |

February 23, 20175 Charts That Show 2017 Could Be a Banner Year for Retailers |

Strengths

- Global manufacturing is making a comeback. Global manufacturers posted their best month in almost six years in February as the JPMorgan-IHS Markit Global Manufacturing Purchasing Managers Index rose by 0.2 points to 52.9, making for the best reading in 69 months.

- Consumer confidence jumped to a 15-year high. The Conference Board's measure of consumer confidence increased to 114.8 for February, the highest since July 2001.

- Europe is growing at its fastest pace since 2011. Markit's final February composite reading for the eurozone came in at 56, well ahead of the 54.4 result from January. "Growth of eurozone economic output accelerated to a near six-year record in February," IHS Markit said in a release.

Weaknesses

- GDP missed again. The measure of the overall state of the U.S. economy missed in its second print for the fourth quarter, according to the Bureau of Economic Analysis. The reading came in at 1.9 percent growth, lower than the 2.1 percent expected by economists. Personal consumption growth increased to 3.0 percent from the initial print of 2.5 percent, but mostly on the back of increased medical spending.

- U.S. pending home sales unexpectedly fell by 2.8 percent in January. "The significant shortage of listings last month along with deteriorating affordability as the result of higher home prices and mortgage rates kept many would-be buyers at bay," said Lawrence Yun, the chief economist.

- Personal spending missed, but personal income beat. For the month of January, personal income rose by 0.4 percent and personal spending came in at 0.2 percent. Economists had forecast that both personal income and spending would rise by 0.3 percent.

Opportunities

- Federal Reserve Chair Janet Yellen capped a week of rising expectations about an imminent interest-rate increase by explicitly supporting a hike in mid-March if U.S. economic progress persists. Markets see a better than 90 percent chance of a rate hike this month, up from just 40 percent a week ago, after top Fed officials including New York Fed President William Dudley and Governor Lael Brainard signaled they’re willing to lift rates soon. Inflation and employment data have been meeting policy makers’ expectations, and growth abroad is either stable or slowly improving, clearing the way for gradual increases.

- Trump says he is committed to rebuilding the roads and bridges in America. "We spend $6 trillion in the Middle East and we have potholes all over our highways and our roads," he said.

- Fourth-quarter eurozone GDP will be released next Tuesday. That could confirm the recent economic momentum in the region.

Threats

- Treasuries got smashed as sellers piled on after Trump's speech. Selling pushed yields up more than 7 basis points in the intermediate part of the curve with the 10-year back up at a two-week high.

- The U.S. February employment report will be released next Friday. Any disappointment in the expected pace of job growth could cause major turmoil in the market, given high expectations of a March rate hike.

- A miss on the final release of January durable goods orders on Monday would create concern about the recent strength in manufacturing.

Gold Market

This week spot gold closed at $1,234.55, down $22.60 per ounce, or 1.80 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower though by 7.88 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index slipped just 2.13 percent. The U.S. Trade-Weighted Dollar Index finished the week up by 0.26 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Feb-27 |

Hong Kong Exports YoY |

7.8% | -1.2% | 10.1% |

| Feb-27 |

U.S. Durable Goods Orders |

1.6% | 1.8% | -0.8% |

| Feb-28 |

U.S. GDP Annualized QoQ |

2.1% | 1.9% | 1.9% |

| Feb-28 |

U.S. Conf. Board Consumer Confidence |

111.0 | 114.8 | 111.6 |

| Feb-28 |

Caixin China PMI Mfg |

50.8 | 51.7 | 51.0 |

| Mar-1 |

Germany CPI YoY |

2.1% | 2.2% | 1.9% |

| Mar-1 |

U.S. ISM Manufacturing |

56.2 | 57.7 | 56.0 |

| Mar-2 |

Eurozone CPI Core YoY |

0.9% | 0.9% | 0.9% |

| Mar-2 |

U.S. Initial Jobless Claims |

245k | 223k | 242k |

| Mar-6 |

U.S. Durable Goods Orders |

1.0% | -- | 1.8% |

| Mar-8 |

U.S. ADP Employment Change |

1.0% | -- | 1.8% |

| Mar-9 |

ECB Main Refinancing Rate |

0.000% | -- | 0.000% |

| Mar-9 |

U.S. Initial Jobless Claims |

238k | -- | 223k |

| Mar-10 |

U.S. Change in Nonfarm Payrolls |

185k | -- | 227k |

- The best performing precious metal for the week was palladium up 0.39 percent. Friday’s Commitments of Traders Report showed money managers increased their bullish positions over the past week. On Thursday the European Union reported consumer prices were 2 percent higher in February than a year earlier, reports MarketWatch. This is the highest rate of inflation in four years, and a pickup from 1.8 percent in January 2017. Europeans have been significant buyers of gold in recent months.

- Provisional data from consultancy firm GFMS shows that India’s gold imports in February surged to 50 tonnes, reports Reuters. This is up more than 82 percent from a year ago, and should support global prices that are trading near their highest level in three-and-a-half months. “Pent-up demand on the ease of the cash crunch and wedding related demand lifted imports in February,” said Sudheesh Nambiath with GFMS.

- Australia saw its highest gold production levels in more than 17 years, reports Kitco News, totaling 298 tonnes according to data compiled by mining consultancy firm Surbirton Associates. Production is up around 3.5 percent compared to last year and is the highest since 1999. Australia has seen renewed interest in gold exploration and production as labor and other input costs have dropped in recent years.

Weaknesses

- The worst performing precious metal for the week was platinum, falling 3.03 percent. A story in Business Day reported mid-week that a new study indicated that South Africa should reconsider public ownership of the mining industry. Gold is headed for its biggest weekly drop since November, declining for the fourth time in five days, reports Bloomberg. Gold prices fell as the U.S. dollar rallied following the Federal Reserve’s increased expectation for a March interest rate hike. New York Fed President William Dudley said earlier this week that the case for tightening had become a lot more compelling, while John Williams of the San Francisco Fed said he sees serious consideration for a rise at the March 14-15 meeting.

- Sales of U.S. Mint American Eagle gold coins fell to a 14-month low, reports Reuters, while silver coin sales were also sharply lower last month. The U.S. Mint sold 27,500 ounces of the gold coins in February, down 67 percent from last year. Despite analysts expecting nervousness ahead of elections in the Netherlands, France and Germany to help the gold price this year, new expectations for higher U.S. interest rates could provide a source of pressure, the article continues.

- Chinese gold imports from Hong Kong slid in January, reports Platts.com. January gold imports totaled 32 metric tons (mt), down 40 percent from December and reaching a two-year low. Combined imports for January stand at 50 mt, down 35 percent year-over-year.

Opportunities

- Mark Bristow, Chief Executive of Randgold Resources, announced during the company’s annual results presentation that more cash would be returned to shareholders over the next few years. At a gold price of $1,200 an ounce, the company expects to generate as much as $1.7 billion by year-end 2021, reports Moneyweb, which could be returned to shareholders. “This would represent a step change in the quantum of dividends paid.”

- INTL FCStone Inc.’s London-based subsidiary has unveiled its physical trading platform for the global bullion market called PMXecute+, reports BankingTech.com. “It’s simply automating our interaction with our customers – improving market access and efficiency – through one platform,” said Barry Canham, global head of precious metals at INTL. Suppliers can anonymously create firm or indicative offers on the platform for all customers to view, the article continues. And if they like what they see, the customers can trade on these, thus seamlessly securing gold at a price and a location they want the bullion to be stored at.

- Gold ETFs are either too optimistic, or in it for the long-term, reports Bloomberg. Gold ETF holdings are almost 8 percent above the four-year average, despite the underlying metal being right at the average. Bloomberg adds that silver ETFs are increasingly utilized for longer-term buy-and-hold vehicles since they are less widely traded and more efficient to store. Silver ETF holdings remain near 2013’s record high of 646 billion ounces. In addition, according to UBS, white metals tend to benefit from positive growth and risk given their links to economic activity via industrial demand. Silver has been outperforming gold so far this year, with the gold/silver ratio gently drifting lower, UBS continues.

Threats

- As you can see in the chart below, a slump in the price of gold is due to “a firmer U.S. dollar and significantly higher rate hike expectations in the U.S.,” said Eugen Weinberg of Commerzbank AG. New York Fed President William Dudley said the case for tightening monetary policy has become “a lot more compelling.” However, one question remains. Will the Fed really choose to hike interest rates around key European elections that have the potential to cause significant moves in the euro?

- In quite the Donald Trump fashion, Tanzania has banned the export of unprocessed metals and ordered mining companies to begin smelting or refining their production to help boost state revenue and create jobs, reports Bloomberg. “The ban intends to make sure that mineral value-addition activities are carried out within Tanzania,” the ministry said. Acacia Mining, which produces all of its gold from three mines in the country, dropped as much as 20 percent on the news, the most since March 2014.

- Franco-Nevada’s David Harquail thinks that gold miners are running to stand still, reports Bloomberg. “In my mind, the industry is ex-growth,” said Harquail. He believes that producers will be faced with options that are unlikely to boost global gold production or lower the sector’s overall costs. Franco-Nevada currently has 94 percent of its holdings in precious metals, but Harquail says the company plans to do more deals in the non-precious metals space, with a particular focus on oil and gas, the article continues, perhaps with fewer royalty contracts being available to the mining sector.

Energy and Natural Resources Market

Strengths

- Manufacturing in the U.S. expanded at its fastest pace since August 2014. The Institute for Supply Managements Index (also known as the ISM Survey) climbed to 57.7, beating forecasts of 56.2, and advancing for the sixth month in a row. Bradley Holcomb, chairman of the ISM survey committee shared with Bloomberg earlier this week that he doesn’t foresee any roadblocks in the way of U.S. manufacturing in the months ahead. As manufacturing is a key input to raw material demand, this is a positive read-through for commodities.

- The best-performing sector for the week was the S&P 1500 Super Composite Construction and Materials Sub Industry Index. The index rose 3.41 percent on the back of positive economic data from the U.S. and around the world.

- South32, a base metal and coal mining company based in Australia, was the best-performing stock this week, finishing up 8.11 percent. The stock rallied on the back of a strong buy rating from Goldman Sachs.

Weaknesses

- Silver was the worst-performing commodity this week, falling 2.88 percent. The drop in the price of the white metal was driven by falling gold prices as the two metals are strongly correlated. Both of the metals were hurt this week as investors positioned themselves in anticipation of the Federal Reserve’s upcoming rate hike.

- The worst-performing sector this week was the S&P/TSX Composite Diversified Gold Sub Industry Index. The index fell 7.99 percent on the back of falling gold prices as the Federal Reserve takes center stage of the financial system this month.

- The worst-performing stock for the week was Newcrest Mining, an Australia-based gold and copper mining company. The company fell 11.6 percent on the back of falling gold prices.

Opportunities

- On Wednesday, China’s air pollution control officially came into effect, according to Reuters. The air pollution control regulation will force aluminum smelters in four provinces surrounding Beijing to cut output by 30 percent over the winter heating season that runs from November to March. As China is the world’s largest producer of aluminum, this will impact the global aluminum supply chain, potentially moving prices higher.

- U.S. drillers added oil rigs for the seventh week in a row, according to Baker Hughes, one of the world’s largest oil field services companies. Drillers added an additional seven oil rigs this week, bringing the total rig count up to 609, the most since October 2015. This marks the 10th month of recovery for energy companies.

- Chinese iron ore miners plot their return as prices surge, according to Reuters. Chinese producers are looking to reopen old mines that were hit hard in the sector downturn over the last few years. As Beijing is expected to boost infrastructure spending in the coming months, producers are working hard to bring more supply online to service future demand.

Threats

- U.S. dollar appreciation and upcoming rate hikes stand as a mild threat to commodity prices, according to Macquarie Bank, a leader in commodity research and banking. After a rocky start to 2017, the dollar is beginning to push higher once again. The relationship holds that a stronger dollar is a negative factor for commodity prices. Although the bank does not view this as a major threat to the current rally in commodities, it views this as a threat nonetheless.

- Gold suffered its largest daily decline of 2017, according to the Wall Street Journal. The yellow metal was hit hard on Thursday this week, falling 1.4 percent in a day as the Federal Reserve took the stage at the prospect of raising rates later this month. Lael Brainard, Fed governor, stated that economic risks are as close to balance as they have been in some time, paving a clear runway for the Fed to potential raise rates.

- U.S. crude oil stocks built to record highs this week, according to the Energy Information Administration (EIA). Stockpiles rose 1.5 million barrels last week, touching a record of 520.2 million barrels after eight straight weekly builds, forcing oil prices to trade range-bound.

Strengths

- The FTSE Bursa Malaysia Kuala Lumpur Composite Index finished the week as a top performer for the region, rising 0.73 percent in a quiet week of trading.

- China ZhengTong Auto Services Hdgs. Ltd. (1728 HK) soared more than 30 percent this week as Bocom International analyst Angus Chan sees margins potentially climbing on new BMW models.

- Utilities were the winner for the week amongst HSCI sectors: the sector rose 1.58 percent in a down week for the broader index.

Weaknesses

- The Hang Seng Composite Index finished the week as the weakest performer in the region, falling 1.32 percent.

- Energy constitutes the worst-performing sector in the HSCI for the week. HSCI energy stocks fell 2.43 percent in the last five trading days.

- Nikkei Taiwan manufacturing PMI dropped to 54.5 from last month’s print of 55.6, while the Nikkei Indonesia manufacturing PMI actually fell to a contractionary 49.3, down from 50.4.

Opportunities

- While there has been a lot of talk about infrastructure in the United States, the Asian Development Bank (ADB) suggested in a new report released this week that Emerging Asia may require some $22.6 trillion dollars (!) in infrastructure spending by 2030.

- This week we got quite a bit of PMI data from a number of spots in the region. Official China manufacturing PMI came in at a solid 51.6, above expectations for a 51.2 print, and was matched by a solid Caixin China manufacturing PMI print of 51.7, well ahead of expectations for a 50.8 print. Investors will watch carefully China’s upcoming National People’s Congress (NPC) for more clarity and color on directions in China in the future. China’s good PMI print had company as well: Nikkei Malaysia PMI rose this month, still a contractionary 49.4 but up from last month’s 48.6, while the Nikkei Vietnam PMI jumped to 54.2 from the prior month’s 51.9 print.

- There seem to be fewer reasons to label China as a currency manipulator at the moment. The Economist points out in an article this week that China meets only some criteria considered to identify currency manipulation, namely, that China runs a large bilateral trade surplus with the U.S. By Economist metrics, indeed, other countries aside from China appear to be guiltier of currency manipulation. For the time being, perhaps, it seems that U.S.-China trade relations may well “keep calm and carry on.”

Threats

- Bloomberg News reports that China’s top diplomat Yang Jiechi met this week with U.S. president Donald Trump to discuss several things, among them North Korea and recent tensions exacerbated by South Korean company Lotte Group’s agreement to provide land for the Terminal High-Altitude Area Defense system. Some South Korean tourism stocks have already taken a hit following a report that China has ordered its travel agents to halt sales of holiday packages to South Korea.

- While it remains somewhat unlikely that China’s carefully crafted NPC would offer any damaging spin or headlines from Chinese authorities, there remains an element of headline risk from the high profile event if the market interprets authorities’ statements and policies in a negative fashion.

- Nickel jumped as the Philippines indicates it may “bar shipments of unprocessed ores,” according to Bloomberg News, which compounds ongoing supply concerns. The Philippines suggests a period of assessment to “consider” banning mineral-ore exports in order to develop high value-added processing, somewhat similar to Indonesia’s approach. Incidentally, Tanzania also made a recent announcement: Friday the country stated all exports of nickel, gold, silver and copper concentrates have been halted, effective immediately.

Strengths

- Turkey was the best performing country this week, gaining 1.7 percent. February manufacturing data was reported at 49.7, higher than January’s 48.7, but still below the 50 level that separates expansion from contraction. The inflation rate was 10.13 percent in February, the highest level since April 2012.

- The Polish zloty was the best performing currency this week, gaining 80 basis points against the U.S. dollar. The zloty’s appreciation is supported by strong economic data. The economy grew at 2.7 percent last year, the deflation period ended, unemployment has been declining, wages are increasing, and retail sales are improving.

- The consumer discretionary sector was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 1.7 percent. Russia's February manufacturing PMI ended its six-month rise and retreated to 52.5, down from January's 54.7 and hitting a four-month low. The price of Brent crude oil declined by 30 basis points and closed at 55.81 after the U.S. reported record high oil inventories.

- The Turkish lira was the worst performing currency this week, losing 2.6 percent against the U.S. dollar. By Bloomberg’s calculation, there is now an 82 percent chance the Fed will hike interest rates in two weeks; such a move will put pressure on the lira as Turkey borrows heavily in dollars.

- The energy sector was the worst performing sector among eastern European markets this week.

Opportunities

- The February eurozone manufacturing PMI ticked down from a flash reading of 55.5 to 55.4, but is still better than the 55.2 January reading, and is the highest since the series began in early 2014. Strong manufacturing data was reported in Eastern Europe. In Hungary, the PMI surged to a record 59.5, from the revised 57 read in January. The Czech PMI topped forecasts and rose to 57.6, the highest reading since April 2011. And in Poland, the PMI was little changed at 54.2, compared with the 54.8 read a month earlier. An improving outlook in Western Europe, the main destination for exports, is positive for the EU’s former communist east.

- The annual rate of inflation in the eurozone rose above the European Central Bank’s target for the first time in four years in February, reaching 2 percent from the prior reading of 1.8 percent in January. Some may argue that the recent pickup in inflation will prompt the ECB to change its policy, but policymakers want to see if the current rate of inflation will be sustained when the rise in energy prices comes to a halt.

- Poland’s government is predicting the U.K.’s departure from the European Union will bring as many as 200,000 Poles back to its hot job market. With the unemployment rate at 5.5 percent, the lowest reading since the data series started in 1992, the labor market is tight and in need of skilled workers. In 2015 more than 800,000 Poles resided in the U.K., according to the Office of National Statistics.

Threats

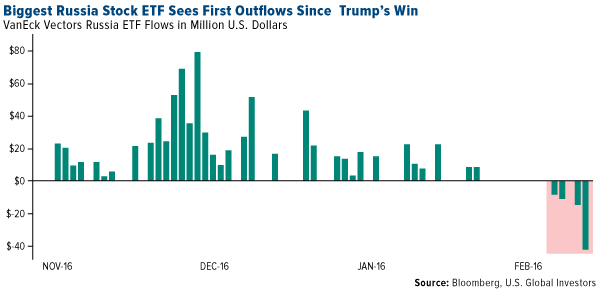

- The world’s biggest exchange traded fund that tracks Russian equities, last week logged its largest outflows in nine months. Russian investors may be losing optimism over prospects for an easing of sanctions under President Trump. “There is room for a correction after the market rallied a lot last year,” said Maarten-Jan Bakkum, a senior strategist at NN Investment Partners in The Hague.

- The Turkish lira continues to stabilize, but its stability is very fragile, Win Thin from Brown Brothers Harriman wrote this week. Purges of the nation’s institutions continue, tension with the military may be intensifying, regional tension remains high, and the referendum on the executive presidency will take place on April 16. If Turks vote in favor of it, the Prime Minister post will be eliminated, and will allow the president to issue an executive decree, declare emergency rule, appoint ministers and top state officials, and dissolve parliament.

- President Donald Trump may name Fiona Hill as his top Russian advisor. Hill was a national intelligence officer for Russia and Eurasia at the National Intelligence Council, serving under both George W. Bush and Barack Obama, and she advocates keeping sanctions on Russia and rejected the idea of a “grand bargain” with Putin. Optimism in Moscow is fading that Trump’s presidency will make a new area of cooperation.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits