The Bull Market Just Turned Eight. What Now?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

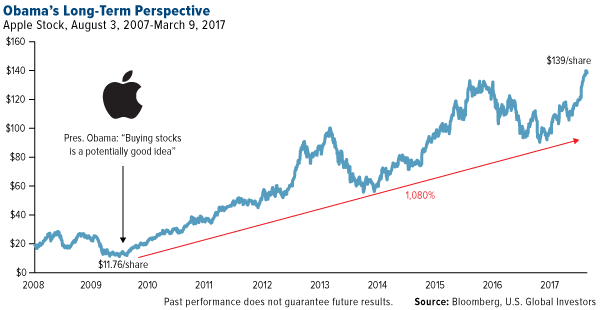

Eight years ago this week, President Barack Obama gave investors a surprisingly hot trading tip. In office less than two months, he commented that we were at “the point where buying stocks is a potentially good deal if you’ve got a long-term perspective.”

Obama couldn’t have known then how accurate his call was. The market found a bottom that very week, and investors who took the president’s advice managed to get in on the absolute ground floor.

At the time, investor sentiment was at or near record lows. The number of S&P 500 Index stocks trading below $10 a share had grown tenfold since the end of 2007. The New York Stock Exchange, in fact, had to temporarily suspend its requirement that equities trade at more than $1 a share. Giant companies such as Citigroup and General Motors—a share of which cost little more than a pocketful of spare change—were at risk of being delisted.

Today, many of those bullish investors have seen some spectacular gains. Since its low of 666 in March 2009, the S&P 500 has climbed a whopping 260 percent, with not a single year of losses. The average annual return has been over 15.7 percent, based on Bloomberg data. With dividends reinvested, it’s closer to 18 percent.

Just take a look at Apple, which has surged more than 1,080 percent as it introduced or expanded its line of got-to-have, now-ubiquitous products, from the iPhone to iPad.

To show you just how far we’ve come, I put together a few comparisons of several indices and economic factors between March 2009 and now.

| March 2009 | Most Recent Data, March 2017 | Percent Change | |

|---|---|---|---|

| S&P 500 Index | 666.79 (intraday low, March 6) | 2,400.98 (intraday high, March 1) | 260% |

| Dow Jones Industrial Average | 6,440.08 (intraday low, March 9) | 21,169.11 (intraday high, March 1) | 228% |

| University of Michigan Consumer Sentiment Index | 69.5 | 96.3 | 38% |

| U.S. ISM Manufacturing Purchasing Managers’ Index (PMI) | 35.8 | 57.7 (February) | 61% |

| Housing Starts | 505,000 | 1,290,000 | 155% |

| Light Vehicle Sales | 9,552,000 | 17,465,000 | 83% |

| Unemployment | 8.7% | 4.7% (February) | -45% |

| Gold | $885 (intraday low, March 18) | $1,248.30 (intraday high, March 1) | 41% |

| Sources: S&P Dow Jones Indices, Bureau of Economic Analysis, University of Michigan, Bureau of Labor Statistics, Census Bureau, ISM, IBA | |||

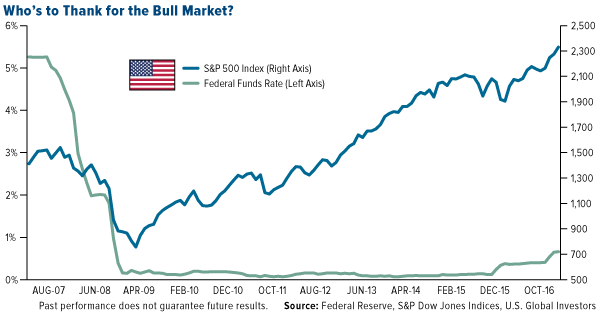

Of course, there have been market skeptics. As others have pointed out, this particular bull run—the second-longest in U.S. history—has arguably been the least loved, with many investors calling it artificial and arguing that it’s been driven not by fundamentals but the Federal Reserve’s policy of record-low interest rates.

Now there are those who wonder how much longer this bull run can last. And if it ends, will it be with a bang or a whimper?

“Trump Rally” Could Have Further Room to Grow

It’s important to keep in mind the old investing adage, “Bull markets don’t die of old age.” Bear markets have been incited by everything from geopolitical conflicts to stagflation to oil price shocks to financial crises. Although no one can say with all certainty that age is irrelevant in a market’s longevity, there are signs that the current eight-year-old run has further room to grow, at least in the short term.

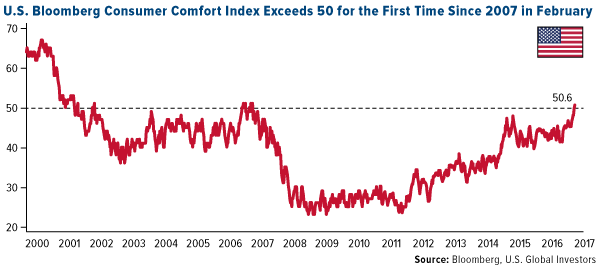

President Donald Trump’s pro-growth policy proposals, including lower corporate taxes, deregulation and infrastructure spending, have jolted many people’s “animal spirits,” with several indices already hitting near-record highs. In January, the Index of Small Business Optimism posted a reading unseen since 2004, as I shared with you earlier. More recently, the Bloomberg Consumer Comfort Index, which measures American consumers’ views on the U.S. economy and their personal finances, climbed to 50.6, the first time it’s exceeded 50 in a decade. Note how few times it’s risen above that level in the past 17 years.

And of course there’s the booming jobs market. Following the record 75 straight months of jobs creation under Obama, employers continue to ramp up their rate of hiring even more, indicating a rosy financial and economic outlook. Despite candidate Trump’s tendency to question the validity of encouraging jobs reports before the election, President Trump now has much to brag about in his first full month in office.

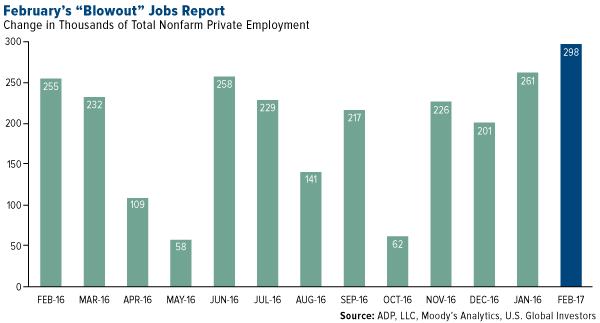

According to the Bureau of Labor Statistics (BLS), the U.S. added a phenomenal 235,000 jobs in February, with gains made in construction, manufacturing, mining, educational services and health care. The report indicated that mining added 8,000 positions during the month, 20,000 in total since a recent low in October, just before the election. This shows executives’ confidence in Trump, who pledged to revive the industry by eliminating job-killing regulations.

Another recent report was even more generous than the BLS. The ADP National Employment Report showed U.S. employment increasing by nearly 300,000 from January to February. Medium-size businesses—those with between 50 and 499 employees—expanded the most, adding 122,000 positions.

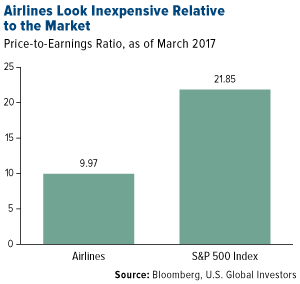

Valuations High, but Good Deals Can Still Be Found

Some investors right now might be discouraged by high stock valuations. Although it’s true certain sectors are beginning to look expensive—information technology is currently trading at more than 23 times earnings, real estate at 43 times earnings and energy at a whopping 113 times earnings—there are still some attractive deals.

|

Among them is the airlines industry, which as of today has a very reasonable price-to-earnings ratio of 9.97. At 21.85, the S&P 500 is more than twice as expensive.

This is one of the many reasons why billionaire investor Warren Buffett is bullish on airlines, which he once called a “death trap” for investors. Not only did his holding company Berkshire Hathaway purchase shares of the four big domestic carriers—American, United, Delta and Southwest—but it dramatically expanded those holdings in the fourth quarter, according to regulatory filings. Now there’s even speculation that Buffett and Berkshire Hathaway could be planning to acquire one of these four carriers outright, with Morgan Stanley’s Rajeev Lalwani writing that Southwest’s “domestic focus, robust and sustainable free cash flow, range of growth opportunities, defensible cost structure and more tenured management team” make it a logical candidate.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.49 percent. The S&P 500 Stock Index fell 0.44 percent, while the Nasdaq Composite fell 0.15 percent. The Russell 2000 small capitalization index lost 2.07 percent this week.

- The Hang Seng Composite gained 0.26 percent this week; while Taiwan was down 0.21 percent and the KOSPI rose 0.89 percent.

- The 10-year Treasury bond yield rose 9 basis points to 2.57 percent.

Domestic Equity Market

Strengths

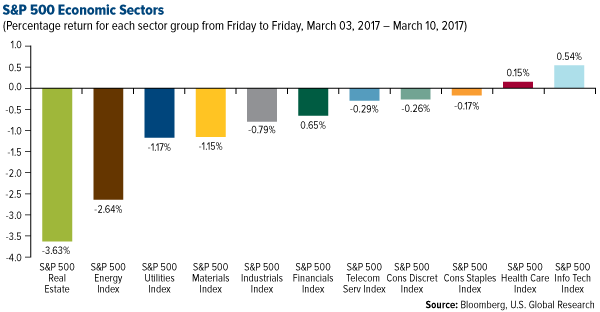

- Information technology was the best performing sector of the week, increasing by 0.54 percent versus an overall decrease of 0.43 percent for the S&P 500 Index.

- H&R Block was the best performing stock for the week, increasing 13.11 percent.

- The Nintendo Switch is Nintendo's fastest-selling console ever. Nintendo has sold more Switch consoles in its first two days than any other of its gaming systems, according to Nick Wingfield of The New York Times.

Weaknesses

- Real estate was the worst performing sector for the week, falling 3.63 percent versus an overall decrease of 0.43 percent for the S&P 500.

- Transocean was the worst performing stock for the week, falling 9.39 percent.

- Radio Shack's operator has filed for bankruptcy protection. General Wireless Operations bought Radio Shack in 2015 when it filed for bankruptcy; now it has filed for Chapter 11 reorganization, Reuters reports.

Opportunities

- General Motors is selling Opel. GM has agreed to sell its European division to Peugeot for $2.3 billion. "For GM, this represents another major step in the ongoing work that is driving our improved performance and accelerating our momentum," GM CEO Mary Barra said in a statement.

- Facebook reached a deal to stream soccer matches. Facebook, the Spanish-language broadcaster Univision, and Major League Soccer have reached an agreement in which Facebook will stream at least 22 regular-season matches, The Wall Street Journal reports.

- Hedge fund billionaire David Tepper says he bought Snap Inc. shares, sold some, and will buy again if they fall. Shares of Snap, the parent company of Snapchat, gained as much as 7 percent after Tapper's interview with CNBC and as the pace of short sales slowed.

- Caterpillar failed to comply with U.S. tax and financial reporting rules in an effort to keep its stock price high, according to a government-commissioned report reviewed by The New York Times. The Times cited a report prepared by a Dartmouth College professor that investigated the heavy-machinery maker's tax practices. Its main finding was that Caterpillar avoided reporting on billions of dollars it brought to the U.S. from its Swiss units and affiliates. The report found that Caterpillar returned an estimated $7.9 billion in funds structured as loans that it did not report for tax or accounting purposes, The Times reported.

- Urban Outfitters' shares slumped more than 8 percent after its fourth-quarter results missed analyst estimates. "Like housing, that bubble has now burst," CEO Richard Hayne said during the earnings call, referring to retail square-foot capacity.

- Snap is in a bear market. Shares of the newly public social-media company plunged 10 percent on Tuesday, and they are now 27 percent below Friday's high print of $29.44 a share. Snap's opening trade was at $24 after pricing its initial public offering at $17 last Thursday.

March 9, 2017(VIDEO) What Drives the Price of Gold? |

March 8, 2017Why Commodities Could Be on the Verge of a Massive Surge |

March 6, 2017Disrupt... Or Get Disrupted |

Strengths

- Employers added 235,000 workers to their payrolls in February, the government reported on Friday, a hefty gain that clears the path for the Federal Reserve to raise its benchmark interest rate when it meets next week. World Interest Rate Probability data provided by Bloomberg shows a 100 percent chance the Federal Reserve will raise its key interest rate by 25 basis points to a range of 0.75 percent to 1.00 percent at the conclusion of its March 14-15 meeting.

- Gallup's measure of U.S. economic confidence jumped to a record high. The U.S. Economic Confidence Index increased by seven points to +16 from February 27 to March 5, marking the highest weekly average in the index's nine-year trend.

- An indicator of the health of the global economy grew at its fastest pace in six years. Data released by the International Air Transport Association showed that revenue passenger kilometers grew by 9.6 percent compared with a year earlier, making for the fastest growth since April 2011.

Weaknesses

- The U.S. trade deficit jumped in January to a five-year high. The Commerce Department said the trade deficit in January rose 9.6 percent to $48.5 billion. This underscored the challenges facing President Donald Trump in fulfilling a campaign pledge to reduce deficits.

- According to the Conference Board’s latest Economic Forecast for the U.S. economy, U.S. economic growth was downgraded in the first quarter from 2.2 percent (annualized) to only 1.6 percent. The data suggests weaker than expected consumer and government construction spending along with a drop in exports of capital goods, resulting in a surge in the trade deficit.

- Initial jobless claims rose by 20,000 to 243,000 last week, more than expected.

Opportunities

- U.S. retail sales for February are released on Wednesday and economists will be on the lookout for strength in consumption.

- The U.S. reports industrial production data on Friday, which is likely to follow suit from this week’s strong factory orders report.

- The Leading Index for February will be released next Friday and investors are optimistic about a strong print given the recent positive economic surprises.

Threats

- Societe Generale strategist Albert Edwards says higher interest rates will trigger a 1994-style "bloodbath" in the bond market. Edwards recalled that before 1994 markets were expecting interest rates to increase, much as they are today. After the Fed initially raised rates, the two-year note yield, which moves inversely to its price, jumped by about 50 basis points.

- President Donald Trump told conservative groups that if the GOP leadership's American Health Care Act did not pass, he would allow Obamacare to collapse and blame its failure on Democrats. Conservative groups contend that the AHCA's tax credits that allow people to purchase insurance are a "Republican entitlement" and the whole bill is simply "Obamacare Lite" or "Obamacare 2.0."

- Peter Navarro, the head of the Trump administration National Trade Council, wrote an op-ed in The Wall Street Journal. Business Insider reports that Navarro laid out why he thinks the U.S. is losing its grip on the economy. He shared his views on GDP growth, trade deficits, and how the U.S. national security depend on keeping American assets in American hands. However, Business Insider states that Navarro doesn’t seem to understand how our economy works.

This week spot gold closed at $1,204.55, down $30.00 per ounce, or 2.43 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower though by 2.50 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index slipped just 2.35 percent. The U.S. Trade-Weighted Dollar Index finished the week down by 0.16 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Mar-6 |

U.S. Durable Goods Orders |

1.0% | 2.0% | 1.8% |

| Mar-8 |

U.S. ADP Employment Change |

187k | 298k | 261k |

| Mar-9 |

ECB Main Refinancing Rate |

0.000% | 0.000% | 0.000% |

| Mar-9 |

U.S. Initial Jobless Claims |

238k | 243k | 223k |

| Mar-10 |

U.S. Change in Nonfarm Payrolls |

200k | 235k | 238k |

| Mar-14 |

Germany CPI YoY |

2.2% | -- | 2.2% |

| Mar-14 |

Germany ZEW Survey Current Situation |

77.3 | -- | 76.4 |

| Mar-14 |

Germany ZEW Survey Expectations |

13.0 | -- | 10.4 |

| Mar-14 |

U.S. PPI Final Demand YoY |

1.9% | -- | 1.6% |

| Mar-15 |

U.S. CPI YoY |

2.7% | -- | 2.5% |

| Mar-15 |

FOMC Rate Decision |

1.00% | -- | 0.75% |

| Mar-16 |

Eurozone CPI Core YoY |

0.9% | -- | 0.9% |

| Mar-16 |

U.S. Housing Starts |

1262k | -- | 1246k |

| Mar-16 |

U.S. Initial Jobless Claims |

245k | -- | 243k |

Strengths

- The best performing precious metal for the week was gold, down 2.43 percent, but still leading its precious metals peers. Gold imports by India are said to have risen nearly three-fold in February from a year earlier, reports Bloomberg, jumping 175 percent. Jewelers are restocking for the upcoming festival and wedding period that starts next month.

- The U.S. saw its largest trade deficit since March of 2012, reports Bloomberg, as a jump in merchandise imports in January exceeded a smaller gain in shipments overseas. “The wider deficit indicates trade, which subtracted 1.7 percent from fourth-quarter growth, will weigh on the economy in early 2017,” the article continues. A stronger dollar has made exports less competitive and could be hindrance to boosting manufacturing jobs in the U.S. as President Trump promised.

- Joni Teves, strategist at UBS, writes that the research group expects underlying positive sentiment toward gold to remain broadly intact as uncertainty lingers. In its Global Precious Metals Comment, Teves outlines that despite the recent increase in positioning, gold market length remains relatively subdued with net positions in Comex accounting for about 50 percent of the record. Similarly, UBS writes “there really isn’t much expectation of an aggressive selloff in gold – this has been a common theme among our conversations with market participants in different regions.”

Weaknesses

- The worst performing precious metal for the week was platinum, down 5.72 percent. Silver was not far behind with a loss of 5.22 percent.

- According to a weekly Bloomberg survey, nearly half of gold traders and analysts are bearish on gold as the dollar strengthens amid expectations of a Fed rate hike next week. Overseas, the People’s Bank of China reports gold holdings unchanged for a fourth-straight month, coming in at 59.24 million ounces by the end of February. Similarly, Bullionvault’s Gold Investor Index, which measures the balance of client buyers against sellers, fell to the lowest level since July.

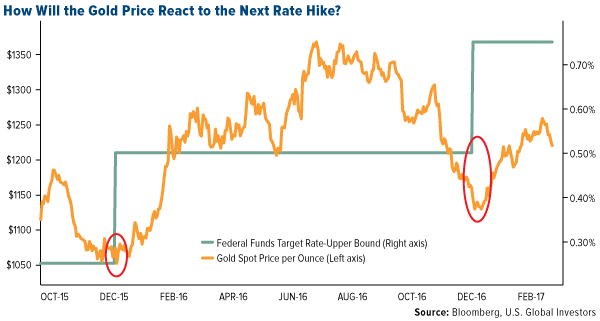

- Gold fell below $1,200 an ounce this week, the longest losing streak since October, on better-than-expected U.S. private jobs data – adding to positive economic talk that boosted the dollar. “Three weeks ago the possibility of a rate hike in March was very small, but now it’s 100 percent,” said Bob Takai, CEO and president of Sumitomo Corp. So where exactly does the Fed see rates headed? The chart below gives a quick comparison between the Fed Funds Target versus where the Taylor Rule Estimate, estimating close to 4 percent. The sudden shift to raise rates in March may reflect that the Fed is behind the curve again.

- Hedge funds are bracing themselves for tough times ahead this year, reports Bloomberg. Managers have stopped loading up on bullish positioning, becoming less reliant on U.S. stocks and selling economically sensitive bank shares and materials like copper, the article continues. Now they are buying gold. Quants from UBS and Goldman Sachs are also seeing opportunity for the yellow metal, using different modeling techniques they conclude that the dollar is perhaps 30 percent overvalued. And despite gold being under pressure leading up to the next rate hike, Bank of America still sees prices rallying by around $200 by the end of the year.

- Mike McGlone, a BI Commodity Strategist, writes this week that commodities often prevail in tightening cycles, perhaps now more than ever. For example, bullion gained 52 percent in the June 2004 to June 2006 tightening cycle and 5 percent from the June 1999 to May 2000 tightening cycle. “The Fed is only tightening when they are concerned about inflation,” McGlone said. “That is good for gold.” In fact, the yellow metal bottomed a day after the past two tightenings and rallied thereafter.

- After four years of restraint, Bloomberg reports that mining investment bankers say deal-making is starting to flow again. Paul Knight of Barclays Plc says this is the busiest it’s been in his four years with the company. “If our experience here is any indication of what’s happening around the street, you may well see more M&A activity at the end of this year than we’ve seen in the last three or four years,” Knight commented. China Gold, the nation’s largest government-owned gold producer is even back on the acquisition hunt after bulking up mines, reports Bloomberg.

Threats

- Morgan Stanley points out that a revised draft of South Africa’s mining charter could still contain very disadvantageous requirements for mining companies that are not reflected in the share prices. One of the key concerns around the potential draft includes the fact that the once empowered, always empowered rule no longer applies and companies have to empower back to 26 percent if they are below the threshold.

- Steven Mnuchin’s picks for the top ranks of the U.S. Treasury are being stalled due to resistance from the White House, reports Bloomberg. More specifically, questions about loyalty to Trump have played a role in at least two cases – including one recruit whose Twitter account was scrutinized for potential criticism of the president. On the flip side, David Nason, who is a leading candidate to be named the Fed’s bank supervision chief, told the White House he is no longer interested in the job. Nason plans to pursue opportunities at GE instead. And if you thought Russian hacking in the U.S. has pulled back since the election, you would be wrong. Liberal think tanks, critical of President Trump, around the U.S. are finding that their firewalls have been breached by Cozy Bear and they are being asked to pay ransoms in bitcoin to prevent sensitive data from potentially being leaked.

- According to a study by consultant Roland Berger GmbH, the proposed U.S. border tax would make most automakers unprofitable, reports Bloomberg, along with strain consumers and lead to job losses rather than gains. “The planned charge would increase the average cost of a car by $3,300, prompting a drop in demand and forcing manufacturers to react by shrinking their U.S. workforce,” the firm said in a presentation on Wednesday.

Energy and Natural Resources Market

Strengths

- Natural gas prices rose 7.4 percent this week as colder-than-average weather across the eastern seaborne is clearing stockpiles in the U.S. According to the U.S. Energy Information Administration, U.S. stockpiles shrank by 68 billion cubic feet (BCF) this week where 64 BCF came from consumers pulling gas from storage, compared to analyst estimates of 61 BCF. A positive read-through for natural gas prices.

- The best performing sector for the week was the S&P Super Composite Package Foods Sub Industry index. All sectors fell in value this week; however, the index decreased the least at -0.07 percent as cyclical investors moved into defensive names.

- Israel Chemicals Ltd, a multi-national manufacturer of fertilizers and chemicals based in Israel, was the best performing stock this week, finishing up 4.7 percent. The stock rose on the back of beating analysts’ profit and revenue forecast estimates for the fourth-quarter of 2016.

Weaknesses

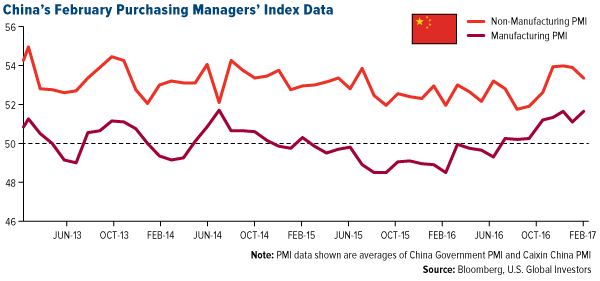

- Iron ore was the worst performing commodity this week dropping 10.85 percent. The mineral experienced its worst week in nearly three months as stockpiles in China rose to the most in 13 years and investors worry over the trajectory of China’s economy in the year ahead. A negative read-through for iron ore.

- The worst performing sector this week was the FTSE 350 Mining Index. The index fell 7.4 percent on the back of falling metal prices across the complex and concerns surrounding global growth.

- The worst performing stock for the week was First Quantum Minerals Ltd, a Vancouver-based mining and metals company. The company fell 11.2 percent on the back of falling copper prices.

Opportunities

- Oil prices have gone down too far, too fast according to a note by the famed research house Evercore ISI. The commodity has been hit hard with a 6 percent decline this week as negative inventory reports have forced investors to exit positions; however, Evercore ISI believes that investors are missing the bigger picture. A key driver of oil prices resides in manufacturing strength which is at its highest reading since August 2014 at 57.7. Evercore is taking a contrarian view to the recent negative developments in oil, initiating an overweight position to its model portfolio. A positive read-through for oil prices in light of negative developments.

- Steel prices are looking strong and robust in China, according to a note released by UBS earlier this week. The materials team at UBS met with several steel mills this week on a field trip to the country and reported back a very optimistic outlook on the metal’s price in the short term. The steel mills that the team visited reported that capacity is currently running on full due to strong demand where order books are indicating demand has potential to remain strong in the coming months. A positive read-through for steel prices.

- The IEA predicts that oil will face a supply shortage within the next three years, according to an article written by the Financial Post. Investment to various projects globally has stalled in the last few years as crude oil prices crashed, making it harder for producers to operate profitably. However, this backlog in investment is estimated by the IEA to lead to a price spike in the coming years. A positive read-through for oil prices.

- China’s consumer price index (CPI) and producer price index (PPI) data diverged this week raising concerns over the validity of the global reflation trade, according to Zerohedge. PPI, a measure of the prices producers pay was 7.8 higher this month while CPI, a measure of the prices consumers pay, was only 2.5 percent higher, suggesting that demand for raw materials in the country might actually be more overstated than what was reported. A negative read-through for raw materials from the world’s largest price setter.

- OECD warns the global recovery is far too fragile and markets have lost touch with reality, according to the Financial Post. While pickup in growth around the world is expected to reach 3.3 percent this year by many forecasters, the OECD believes that the pace is still too slow and warns that factors such as trade barriers, overvalued stock markets, and volatile currencies could potentially derail the world’s current trajectory of growth.

- China is confronting issues surrounding excess corn stocks, reports the Financial Times this week. As the country works in attempts to rid itself of unwanted stocks of corn built up in recent years, struggling farmers are seeking additional financial aid from Beijing to help with low prices and bulging inventories. Chen Xiwen, a leading agricultural policy advisor, stated that such large stocks will need alternative means of consumption as the country will need a few years to work through current stock. A negative read-through for corn prices.

China Region

Strengths

- The best-performing market in the region this week was South Korea, up 0.89 percent. South Korea’s currency was up 27 basis points for the week.

- China’s foreign-currency reserves posted their first gain since June in February, climbing above $3 trillion. Zhao Yang, the Hong-Kong-based chief China economist at Nomura Holdings, Inc., said, “Strict capital controls have taken effect, as it has reduced outflows and helped market sentiment on the yuan.” The tighter controls on capital outflows and a rally in the yuan prompted the reversal of the seven-month losing streak.

- China announced plans to reduce air pollution through lowering production of several resources including aluminum, steel and coal. The price of aluminum has risen.

Weaknesses

- Thailand was the worst-performing market this week, down 1.68 percent, and the Thai baht currency was down 81 basis points.

- The automotive company Zhejiang Geely Holding Group Co. will no longer pursue the Malaysian carmaker Proton Holdings Bhd. Geely’s chairman, billionaire Li Shufu, said he’s pulling out of the big because Proton “keeps changing its plan and doesn’t know what it wants.” Proton needs a foreign partner as part of the conditions for a loan it received last year.

- Chinese tensions are increasing against South Korea and the U.S. over the Terminal High Altitude Area Defense (THAAD) missile system. China has forced the closing of multiple stores owned by Lotte, a South Korean family-run conglomerate that turned over a parcel of land in South Korea for the THAAD system.

Opportunities

- According to a report from the Asian Development Bank, the cost to modernize the Asian region’s infrastructure will be between $22.6 trillion and $26 trillion from 2016 to 2030. Only part of this spending would come from governments, leaving a massive gap for global investors. The infrastructure need covers projects ranging from power and water, to sanitation, transportation, telecommunications, and more.

- China’s National People’s Congress began last weekend, with an announcement of the government’s economic target. Premier Li Keqiang stated the goal is “around 6.5 percent, or higher if possible.” The Chinese market has been transitioning toward the service sector, away from manufacturing and exports. The government also announced that it won’t devalue its currency in an effort to boost exports growth.

- Leaders in China will strive to improve the quality and efficiency of the economy, said President Xi Jinping regarding the annual National People’s Congress. Legislators concluded that China must better deal with certain state owned enterprises (SOEs), sometimes called “zombie companies.” The government is exploring the possibility of integrating assets owned by SOEs in overseas markets.

- China is facing a shortage in its labor market over the coming decades. Due to China’s long-held one-child policy, the working-age population has been shrinking. About one in three Chinese will be older than 60 by 2050, compared with about one in seven now. Although China reversed the one-child policy in 2015, the government is now considering financial incentives to boost the birth rate.

- Philippine president Rodrigo Duterte may be guilty of crimes against humanity, according to the group Human Rights Watch and others. Under Duterte’s antidrug campaign, thousands of people have been killed, and police have allegedly ordered the extrajudicial killings of drug dealers and users. Although the Philippines is a member of the International Criminal Court, it is unlikely that Duterte would face domestic prosecution while president.

- Tensions between South Korea and China over a U.S. missile defense system are impacting air travel and tourism in the area. Some South Korean and Chinese airline carriers have temporarily suspended certain flights. Goldman Sachs estimates that the economic impact of fewer mainland Chinese taking trips to South Korea will come in at $5 billion.

Emerging Europe

Strengths

- Turkey was the best relative performing country this week, losing 12 basis points. In Moscow, President Erdogan signed a deal to create a Russia-Turkey Investment fund worth $1 billion that could strengthen bilateral economic ties and increase investment flows between both countries.

- The euro was the best performing currency this week, gaining 61 basis points against the U.S. dollar. Hawkish comments out of the European Central Bank (ECB) supported the eurozone bloc currency.

- The consumer discretionary sector was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 4 percent. The Moscow stock exchange is highly correlated with the price of Brent crude oil, which fell to $51.33 per barrel from $55.90 in the past five days, or 8.4 percent. U.S. crude oil inventories surged to another record high.

- The Russian ruble was the worst performing currency this week, losing 1.3 percent against the U.S. dollar. The currency slumped in response to oil’s plunge. According to Bloomberg, the ruble’s 30-day correlation to oil rose to 0.5 from as low as 0.13 on February 20.

- The material sector was the worst performing sector among eastern European markets this week.

Opportunities

- The ECB left its policy unchanged and Mario Draghi said further stimulus measures are less likely as the threats to recovery have become less severe. Inflation spiked in last months and ECB’s economist raised their growth forecast for this year to 1.8 percent from 1.7 percent. The central bank is due to lower its monthly bond purchase program in April to 60 billion euros from 80 billion. The program is set to run until the end of the year.

- Czech Republic’s inflation accelerated to 2.5 percent in February from 2.2 percent in December, the fastest pace since November 2012. The spike in inflation puts pressure on the central bank to exit its three-year koruna appreciation cap.

- European Union leaders re-elected Donald Tusk as the European Council president despite Poland voting against his next two-and-a-half year term. The European Council brings together the government of the 28 EU member states and jointly they set the EU’s strategic direction in key areas, such as reforms of the eurozone, the Greek debt crisis, the migrant challenge and relations with Russia. Mr. Tusk is expected to play a major role in the U.K.’s Brexit negotiations.

Threats

- Greek’s gross domestic product decreased by 1.2 percent in the October to December period on a quarterly basis, compared with a 0.4 percent contraction rate stated in a flash data released last month. The fourth quarter contraction was mainly due to as 2.1 percent decline in public consumption and weaker net exports. This negative growth data may complicate ongoing bailout talks.

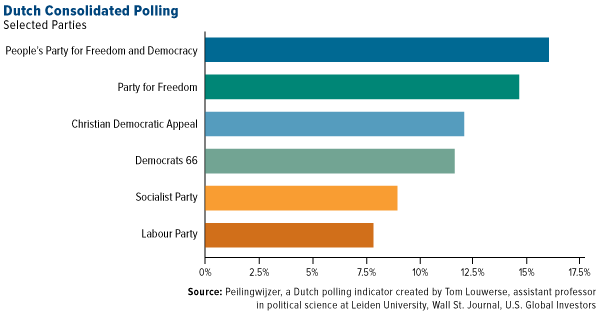

- Next week on March 15, the Netherlands will hold national elections. The People’s Party for Freedom and Democracy, led by the current prime minister Mark Rutte, is leading in the polls. The anti-European Union, anti-immigration Party for Freedom, led by Geert Wilders, is a step below in the polls. If Mr. Wilders wins, he may take the Netherlands out of the EU. And, his victory may support presidential candidate Marine Le Pen in France, from the far right Front National party, who has vowed to pull France out of the euro, potentially bringing an end to the common currency project.

- The Russian MICEX Index closed below its 200-day moving average for the first time in more than a year on Tuesday, a bearish sign to some investors. Investors pulled the most cash from Russia’s biggest exchange-traded fund in more than three years last week. The downtrend may continue with falling oil prices and optimism over sanctions removal fading.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All