Rick shares two reasons why we see abundant fixed income opportunities.

Skeptics of the active approach often cite this argument: With information more and more readily available, markets are becoming ever more efficient and true alpha (or active return) is increasingly difficult to find.

We don’t believe that this is true today in fixed income markets. Indeed, we see abundant opportunities for active bond investors for two reasons. The crosscurrents different market participants create, alongside the nooks and crannies formed by a disparate investment universe, open up meaningful opportunities for harvesting alpha from the market, in our view.

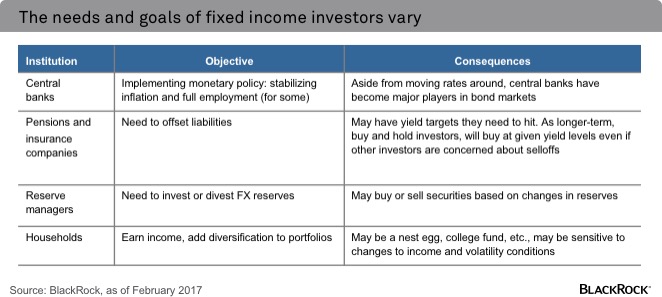

The fixed income market is incredibly diverse, with market participants who come to the table with a multitude of objectives.

Central banks, reserve managers and liability-driven investors are all major participants in bond markets, but they are not all looking simply to maximize income and returns.

European Central Bank President Mario Draghi made this clear when he discussed the central bank’s asset purchase program in December 2016, noting “there is going to be a loss, but our mandate is to pursue price stability. It’s not to maximize central banks’ profits.” He suggested that the central bank seeks monetary policy, not profit, goals when operating in the bond market.

Other institutions may not eschew returns as overtly, but bond market participants such as pension funds and reserve managers do also look to the bond markets with a different angle than traditional bond fund investors. See some examples in the table below.

We believe these different objectives mean that greater-than-zero-sum opportunities can in fact be available, i.e., we can have transactions that further the objectives of the participants on both sides of a trade. Consider a price-sensitive investor selling a long-dated bond to a liability manager in a rising rate environment. The rate-sensitive investor reduces risk, while the liability manager finds an asset that meets future obligations.

The market is built from a diverse array of securities, many exhibiting differing characteristics from one to another.

Alpha opportunities are also created by the diversity of instruments that constitute the investment universe, in our view. Take the complexity of the corporate bond market relative to the equity market, for instance. Our analysis shows the 10 largest companies in the S&P 500 Index make up 18.1% of that index’s aggregate market capitalization; the bonds issued by those same corporations, however, only make up 1.2% of the Bloomberg Barclays Global Aggregate Index. At the same time, these 10 companies have issued 362 individual securities that are held in the Global Aggregate, and there are a dizzying array of factors that determine the relative value of each of these bonds, including currency, maturity, coupon, liquidity, and structure, just to list a few. This means an investor who does rigorous analysis of the market can discover relative value opportunities.

The corporate bond market is only a small portion of a very diverse bond universe, but other corners also offer a potential stream of alpha opportunities. Take the securitized market. This asset class is spread across a large number of securities, like the corporate bond market, though there are a number of risk factors that are unique to the sector. An investor needs to consider prepayment risk, underlying collateral performance, subordination, and a number of other risks when investing in this space. As with corporate bonds, the securitized market is far from simple, but this complexity potentially opens up opportunities.

So how can investors potentially harvest these sources of active return potential within the fixed income market?

We advocate considering a flexible and diversified approach that looks for opportunities across a wide set of strategies, asset classes and markets without the limitations imposed by a broad market benchmark. Such an approach can use a combination of alpha, beta, carry and dynamic strategies, or what we like to call the ABCDs of active investing. Alpha strategies focus on micro-level mispricing opportunities. One example: a corporate bond relative value strategy that examines the capital structure of a particular issuer and discovers that short-term credit spreads are too high relative to long-term credit spreads.

Beta strategies are designed to capture broad market exposure, while carry involves manufacturing return opportunities by carefully underwriting specific trades that offer attractive risk and reward characteristics. Finally, dynamic, or macro, strategies aim to derive returns from the crosscurrents and waves created by actions from investors with different mandates.

With a combination of these diversified strategies, a flexible active approach aims to find fixed income return opportunities in all corners of the market, even during times of greater volatility or rising interest rates.

Rick Rieder, Managing Director, is BlackRock’s Chief Investment Officer of Global Fixed Income and is a regular contributor to The Blog.

© BlackRock

© BlackRock

Read more commentaries by BlackRock