The outlook for the U.S. economy is nearly unchanged from expectations at the start of the year. Congress will address tax cuts and infrastructure spending only after passage of an updated health care law. A proposal is currently under consideration, but it faces stiff scrutiny from both sides of the aisle in Congress. Anticipated expansionary fiscal policy changes are unlikely to influence economic activity until the tail-end of 2017, at best.

Fundamentals of the U.S. economy are positive and incoming economic data do not suggest a disruption of economic activity. Real gross domestic product (GDP) is projected to grow at a 2.0% annual rate in the first quarter and at a similar pace for the rest of the year.

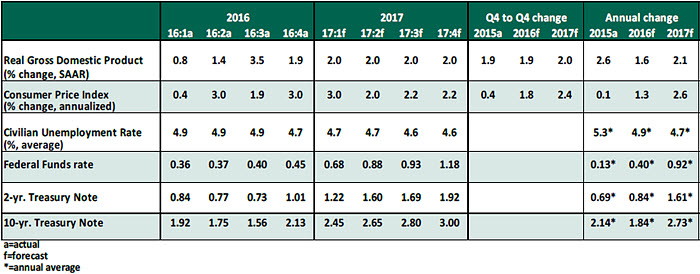

Key Economic Indicators

Key Elements of the Forecast

- Employment and income conditions are supportive of continued growth in consumer spending. Real consumer spending slipped in January, reflecting weakness in outlays for goods and services, which must be viewed with caution. The average level of auto sales was elevated for the first two months of the year (17.6 million units), but is lower than the sharply higher outlier of 18.4 million units sold in December. The weakness in services expenditures was due to warmer-than-typical weather in most of the country, which trimmed utility bills. A more stable consumer spending pattern should prevail during the rest of the year.

- Business spending grew in the fourth quarter after four consecutive quarterly declines. Shipments of non-defense capital goods, the input for business equipment expenditures in the GDP report, slipped slightly in January but the trend is firming. In addition, the Institute of Supply Management’s February survey shows a significant increase in the index tracking new orders (65.1), which is close to the cycle high (66.1) and raises expectations of an increase in factory activity.

Sales of both new and existing homes advanced in January. Construction of new homes fell in January following a strong performance in the prior month. Permit extensions for multi-family homes posted a strong gain in January, a precursor for an increase in building activity. At present, the housing market is affected by cross currents. The nearly 60 basis point increase in mortgage rates could reduce residential investment expenditures. At the same time, strong hiring conditions are a favorable offset. The low inventory of unsold existing homes places a cap on sales and could push home prices higher in the near-term.

The January and February employment reports present a bullish picture of the labor market. The unemployment rate inched down in February to 4.7% even as the labor force expanded. Widespread increases in payrolls have occurred in the past few months, taking the three-month moving average to 209,000. The quit rate and hiring rates are approaching the peaks seen in the previous expansion. Wages picked up in February; a further acceleration is likely as labor market conditions strengthen.

Actual inflation readings have risen and the Federal Reserve’s price stability target is within reach in 2017. The personal consumption expenditure price index rose 1.9% from a year ago in January; the core price index, which excludes food and energy, increased to 1.7%.

The economic environment is changing from that of low-interest rates, low inflation, and an accommodative monetary policy stance to one of higher rates, higher inflation, and a hawkish central bank. In light of this development, the 10-year Treasury note is trading around 2.60%, its highest sustained level since September 2014.

The confluence of developments described above has created the perfect “window of opportunity” for the Fed to raise the federal funds rate by 25 basis points to 0.75%-1.00% at the March 14-15 Federal Open Market Committee meeting. Markets have priced in this policy change and are looking ahead for the forward guidance, updated forecasts of the economy, and the new dot chart. Tune in later this week for our take on the outcome of the meeting.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2017 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit

northerntrust.com/disclosures

© Northern Trust

Read more commentaries by Northern Trust