The Federal Reserve spent a good portion of last year talking tough about raising rates, only to back away at several turns when intimidated by international uncertainty. The Federal Open Market Committee (FOMC) seems to be starting this year off on a more confident note.

As expected, the range for overnight rates was increased by 25 basis points (the upper and lower bounds are now 0.75% and 1%). This action had been previewed by an exaggerated parade of speeches earlier this month, designed to prepare markets. The foreshadowing seems to have worked, as asset prices were little changed after the release. There was one dissenter to the decision, Neel Kashkari of Minneapolis, who wished rates to remain stable.

Market actors were more intently focused on what the Fed offered as a guide to potential future courses of action. To this end, we noted the following:

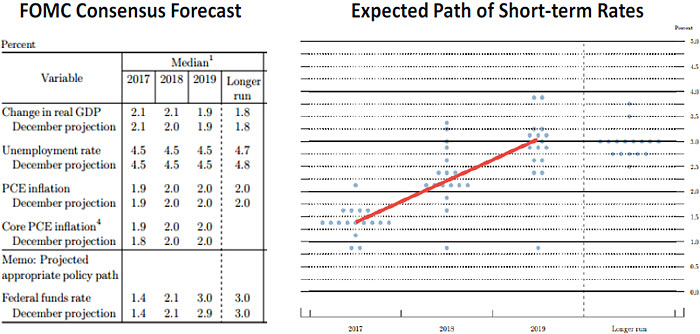

- The Fed’s collective forecast for the next three years was virtually unchanged from its position of last December. If the central bank is expecting a big fiscal package, it is not evident in its projections. (Chair Janet Yellen suggested that the FOMC had not spent time discussing scenarios for fiscal policy or the Fed’s prospective reaction to them.) The outlook also does not seem to give much credit to the “animal spirits” view, which holds that rising levels of optimism will carry over into increased levels of real activity. This suggests a slow and gradual pace of policy normalization.

- The FOMC consensus calls for two further interest rate increases this year, and three next year. This is consistent with the projection that inflation will reach the Fed’s 2% target late this year or early in 2018.

The dispersion of expectations for interest rates is fairly pronounced, even though the dispersion of economic forecasts is not. Risk factors around the outlook and their reflection in asset prices are likely contributing to this broad spectrum of opinion. Overall, the committee described the risks to the outlook as “balanced.”

In her press conference following the committee meeting, Yellen did offer that the FOMC had a conversation centering on the proper size of its balance sheet. At times in the past, Fed officials have suggested that holdings of securities acquired through the quantitative easing (QE) program would be allowed to diminish once the process of interest rate normalization was “well underway.”

It isn’t clear that three interest rate changes spread over 15 months qualifies as a process that is “well underway.” But our sense is that many at the Fed would like to see the portfolio start running off later this year. Yellen noted the uncertainty that will surround this process; while the Fed has a reasonable understanding of how the economy reacts to changes in short-term rates, there is no guide to how activity will respond to a reversal of QE.

Yellen was careful in discussing the level of asset prices, offering that while strong equity prices and narrow bond spreads represented looser financial conditions, higher long-term interest rates had the opposite effect. She did not betray any collective concern about market excesses.

This weekend, Yellen and Treasury Secretary Steven Mnuchin will be Europe for a meeting of G-20 finance officials. The transition is fitting, as events in Europe during the coming months may play into the timing of the Fed’s next move. At present, markets are assigning a 42% probability to another rate hike in June; but given the pending declaration of Brexit and the French election in April, our current guess is that the Fed may wait until September. But a lot could transpire between now and then.

northerntrust.com

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2017 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit

northerntrust.com/disclosures

© Northern Trust

Read more commentaries by Northern Trust