America’s New Emphasis on Fiscal Policy

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsFor the third time in two years, the Federal Reserve lifted interest rates 0.25 percent this week following last week’s phenomenal jobs report. The move was seen as more dovish than many market analysts had anticipated. BCA Research went so far as to call it an “unhike,” citing a number of factors, including forecasts of only three rate hikes in 2017 instead of four.

Immediately following the announcement, the dollar lost ground, clearing the way for gold to climb more than $20 an ounce.

During her press coverage, Fed Chair Janet Yellen expressed doubt that the U.S. economy can grow much faster than 2 percent annually over the next couple of years, placing her squarely at odds with President Donald Trump, who campaigned on a pledge to boost GDP growth as much as 4 percent.

Since Trump’s inauguration more than 55 days ago, we’ve seen a steady power shift from the monetary side to the fiscal side. I believe this will only continue to accelerate. As I mentioned last week, the eight-year stock market rally under President Barack Obama was, in many investors’ eyes, driven not by fundamentals but the Fed’s low-rate policy. Now, however, investor exuberance is being supported by proposed fiscal policy such as lower corporate taxes, deregulation and historically large budget cuts to help finance the rebuilding of the nation’s infrastructure and military.

Not everyone is confident Trump can deliver on his infrastructure promise, however. Earlier this week, I shared with you that the American Society of Civil Engineers (ASCE) just gave our nation’s infrastructure a dismal grade of D+, adding that we face a huge funding gap of nearly $3 trillion between now and 2025.

Yesterday, after Trump unveiled his proposed budget for fiscal year 2018, ASCE president Norma Jean Mattei issued a discouraging note, writing that the president’s budget “would eliminate funding for many of the programs designed to improve our nation’s infrastructure.” Although the $1 trillion could be raised at a later time, “that is not the way to effectively invest in, modernize and maintain our aging and underperforming infrastructure,” Mattei said.

Law of Unintended Consequences

Some investors see additional headwinds in White House policy. Near the end of January, the commercial airline industry was disrupted when Trump signed his initial executive travel ban from seven Muslim-majority countries. Between January 28 and February 4, bookings issued by those countries fell 80 percent compared to the same period in 2016, according to travel research firm ForwardKeys.

What might surprise some readers is that the ban’s effects went well beyond the Middle East, reaching most major world markets. Net international bookings to the U.S. cooled 6.5 percent during the period when the travel ban was in effect.

Among the other unintended consequences was news that customs agents were detaining a number of U.S. citizens who might not have had Western-sounding names. Sidd Bikkannavar, a U.S.-born engineer, was not only detained on his way back home to Los Angeles but also asked to turn over his work-issued phone and provide the access PIN to unlock it, potentially compromising sensitive material and contacts related to his work at the NASA Jet Propulsion Laboratory. Muhammad Ali Jr., son of the celebrated heavyweight boxer, was also stopped at least twice while flying in recent weeks.

Trump’s second travel ban, which was also struck down by a federal judge, was opposed by nearly 60 U.S. technology companies—including Airbnb, Pinterest, Lyft and Warby Parker—which filed a brief in support of Hawaii’s lawsuit to block the executive order. Tech companies “and thousands of other businesses throughout the American economy have prospered and grown through the hard work, innovation and genius of immigrants and refugees,” the brief read.

I bring this up only to show once again that regulations, in whatever form, often emerge out of the best of intentions—in the travel ban’s case, public safety—but they sometimes carry negative consequences that act as friction in our economy. Government policy is a precursor to change, as I like to say, and it’s important for us as investors to recognize their cause, effect and possible ramifications.

A couple of weeks ago I attended a Young Presidents’ Organization (YPO) meeting in Vancouver, where the theme was disruption. “Disrupt, or get disrupted,” John Chambers, executive chairman and CEO of tech firm Cisco, told us during his presentation.

One of the most promising upcoming disruptive technologies is autonomous, self-driving automobiles. This tech has the potential to change every industry, including mining, as I told Mining Journal chief editor Richard Roberts this week. So ubiquitous are self-driving cars expected to become, “it seems likely that eventually many people will no longer feel the need to own a car or even know how to drive,” according to management consulting firm Bain & Company. Bain sees the global value of this market, including software, hardware and services, reaching between $22 and $26 billion a year by 2025, with annual growth between 12 percent and 14 percent.

Brian Krzanich, CEO of chip-maker Intel, sees it closer to $70 billion by 2030.

As you might have heard, Intel just finalized its deal to purchase Israel-based Mobileye, maker of sensors and cameras for driverless vehicles, for $15.3 billion. It’s the second-largest acquisition Intel has ever made, following last year’s purchase of Altera for $16.7 billion.

Mobileye stock immediately jumped more than $10 a share.

Although Intel’s business deals haven’t always been profitable in the past, I believe this is a smart move. With sales of desktop computers stagnating, it’s essential for the company to expand its presence and become more competitive in the burgeoning field of internet of things, which will affect as many as 500 billion devices, including vehicles, in the next 10 to 15 years, according to Chambers.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.06 percent. The S&P 500 Stock Index rose 0.24 percent, while the Nasdaq Composite climbed 0.67 percent. The Russell 2000 small capitalization index gained 1.92 percent this week.

- The Hang Seng Composite gained 3.42 percent this week; while Taiwan was up 2.92 percent and the KOSPI rose 3.21 percent.

- The 10-year Treasury bond yield fell 7 basis points to 2.50 percent.

Domestic Equity Market

Strengths

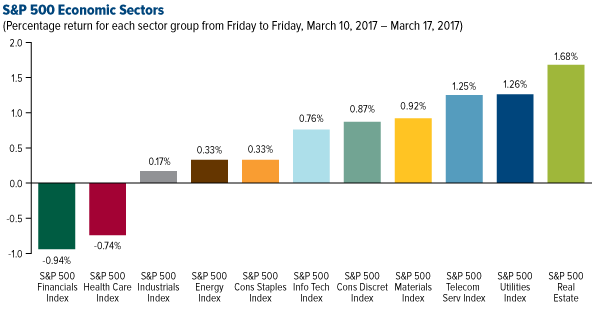

- Real estate was the best performing sector of the week, increasing by 1.68 percent versus an overall increase of 0.32 percent for the S&P 500.

- Wynn Resorts was the best performing stock for the week, increasing 10.69 percent.

- Oracle's cloud business had a huge quarter. The business-software maker announced better-than-expected adjusted revenue and profit, helped by sales at its cloud business surging 62 percent to $1.19 billion, Reuters reports.

Weaknesses

- Financials was the worst performing sector for the week, falling -0.94 percent versus an overall increase of 0.32 percent for the S&P 500.

- United Continental Holdings was the worst performing stock for the week, falling -7.67 percent.

- Bill Ackman folds on Valeant. Ackman's Pershing Square will sell its entire 27.2-million-share stake in Valeant, saying in a statement: "At its current market value, the Valeant position represented 1.5 percent to 3 percent of the various Pershing Square funds; however, the investment required a disproportionately large amount of time and resources. As a result, we elected to sell our investment and realize a large tax loss which will enable us to dedicate more time to our other portfolio companies and new investment opportunities." Shares of Valeant were down nearly 14 percent ahead of the opening bell.

Opportunities

- Intel is reportedly buying Mobileye. Shares of Mobileye are up 30 percent before the opening bell following a report from the Israeli newspaper Haaretz, citing sources that suggest Intel has agreed to buy it for $15 billion. The acquisition provides Intel a big opportunity to enter the driverless car and artificial intelligence markets.

- Canada Goose prices its IPO. The winter-apparel maker known for its coyote-fur-lined coats priced its initial public offering at 17 Canadian dollars ($12.78) a share, above the range of 14 to 16 Canadian dollars that Wall Street was expecting. Shares will trade under the ticker GOOS.

- Walgreens plans to sell more assets to win approval for its takeover of Rite Aid. The pharmacy chain is in talks to sell more assets to the Tennessee-based discount chain Fred's to win regulatory approval for its proposed takeover of Rite Aid, Bloomberg reports.

- GoPro announced more layoffs. The action camera maker announced it was eliminating 270 jobs in a second round of layoffs in three months. "We now expect to deliver revenue in the upper end of our guidance range of between $190 million and $210 million," CEO Nick Woodman said in a statement. The company continues to face competitive pressures.

- An early Twitter investor hates the stock. Venture capitalist Chris Sacca, who was one of Twitter's first investors, said he would defend the stock like one of his children, but he now says he loves the service but hates the stock. Sacca tweeted that his fund sold most of its shares after Jack Dorsey was brought back as CEO in October 2015 and that he sold his personal shares in the fall of last year.

- Toshiba missed its earnings deadline — again. Shares of Toshiba slid 8 percent after the company missed the deadline to report its third-quarter earnings. It was granted a one-month extension, however, as it continues to iron out the problems at its U.S. nuclear unit, Reuters reports.

March 15, 2017America’s Infrastructure Shortfall Could Be an Investor’s Best Friend |

March 13, 2017The Bull Market Just Turned Eight. What Now? |

March 9, 2017(VIDEO) What Drives the Price of Gold? |

The Economy and Bond Market

Strengths

- U.S. homebuilding jumped in February as unseasonably warm weather boosted the construction of single-family houses to near a nine-and-a-half-year high, suggesting the economy remained on solid ground despite an apparent slowdown in the first quarter. Housing starts increased 3.0 percent to a seasonally adjusted annualized rate of 1.29 million units last month, the Commerce Department said. Homebuilding was up 6.2 percent compared to February 2016, suggesting housing would contribute to growth this year.

- Retail sales increased in line with expectations. Retail sales in the U.S. rose by 0.1 percent for the month of February and core retails sales, which exclude automobile sales and gasoline, rose 0.2 percent, also in line with expectations.

- CPI inflation ticked up to its highest level in five years. The headline index moved up to 2.7 percent year-on-year for the month of February. Core CPI, which strips out the volatile food and energy categories, was up 2.2 percent year-on-year. This is a sign the economy is picking up momentum.

Weaknesses

- The U.S. economy is on track to grow at a 0.8 percent annualized pace in the first quarter following the latest jobs and retail sales data, the Atlanta Federal Reserve's GDP Now forecast model showed on Wednesday. However, the latest first-quarter gross domestic product estimate was lower than the 1.2 percent growth rate calculated on March 8, the Atlanta Fed said on its website.

- Industrial production for February came in flat, missing economist expectations of a 0.2 percent gain.

- Construction in the eurozone dipped markedly in January, falling by 2.3 percent compared with the month before, according to the European Commission. The year-on-year decline was even greater, at 6.2 percent.

Opportunities

- Global flash purchasing managers' indices will be released next Friday. Positive readings would buoy confidence in the pace of global growth.

- Federal Reserve Chair Janet Yellen sought to reassure investors that the central bank’s latest interest-rate increase wasn’t a paradigm shift to a trigger-happy policy driven by fears of faster inflation. Speaking to reporters after the Fed’s quarter percentage-point move on Wednesday, Yellen said the central bank was willing to tolerate inflation temporarily overshooting its 2 percent goal and that it intended to keep its policy accommodative for “some time.”

- U.S. Treasury Secretary Steven Mnuchin is set to meet with his G20 counterparts for the first time this weekend in Germany. Trade and currency issues will no doubt be at the top of the agenda. Mnuchin met with German finance minister Wolfgang Schaeuble on Thursday, with Mnuchin vowing to avoid trade wars while seeking to secure reciprocal trading arrangements.

Threats

- Reacting to President Donald Trump's new spending plan, House Minority Whip Steny Hoyer told CNBC on Thursday he doubts even Republican budgeteers think the White House budget blueprint "could" or "should be accomplished." The president's budget framework calls for boosts in defense spending by 9 percent or $54 billion to bolster readiness, and homeland security spending by nearly 7 percent or $2.8 billion to help start building his promised U.S.-Mexico border wall. The White House proposal also calls for funding cuts of 28 percent or nearly $10.1 billion at the State Department, about 31 percent or $5.7 billion at the Environmental Protection Agency, and 18 percent or $5.8 billion at the National Institutes of Health. "It's probably the most irresponsible budget that I've seen and the most unrealistic budget that I've seen," Rep. Hoyer said.

- When the Fed voted to hike interest rates, the market reaction saw stocks rise, bond yields fall and the U.S. dollar decline against its global peers. That, according to Goldman Sachs, was pretty much precisely the wrong reaction. After all, the U.S. central bank, by increasing its benchmark rate, was trying to tighten up things at least a little. Instead, a measure Goldman uses to gauge financial conditions actually loosened afterward. As a result, Goldman believes investors may be underestimating how quickly the Fed will move in the future.

- President Donald Trump’s economic optimism has been a big part of his appeal. On the campaign trail, he promised a return to 3 percent GDP growth. And now in the White House, one of his first announcements was a commitment to return to a 4 percent growth rate. The trouble is that although it’s admittedly very early in the Trump administration and despite strong measures of business, consumer and investor confidence, the real economy isn’t playing along, with GDP growth estimates lagging behind the administration’s promises.

This week spot gold closed at $1,229.14, up $24.41 per ounce, or 2.03 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 4.54 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index rose just 1.43 percent. The U.S. Trade-Weighted Dollar Index finished the week lower by 0.88 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Mar-14 |

Germany CPI YoY |

2.2% |

2.2% |

2.2% |

|

Mar-14 |

Germany ZEW Survey Current Situation |

78.0 |

77.3 |

76.4 |

|

Mar-14 |

Germany ZEW Survey Expectations |

13.0 |

12.8 |

10.4 |

|

Mar-14 |

U.S. PPI Final Demand YoY |

1.9% |

2.2% |

1.6% |

|

Mar-15 |

U.S. CPI YoY |

2.7% |

2.7% |

2.5% |

|

Mar-15 |

FOMC Rate Decision (upper bound) |

1.00% |

1.00% |

0.75% |

|

Mar-16 |

Eurozone CPI Core YoY |

0.9% |

0.9% |

0.9% |

|

Mar-16 |

U.S. Housing Starts |

1264k |

1288k |

1251k |

|

Mar-16 |

U.S. Initial Jobless Claims |

240k |

241k |

243k |

|

Mar-23 |

U.S. Initial Jobless Claims |

240k |

-- |

241k |

|

Mar-23 |

U.S. New Home Sales |

560k |

-- |

555k |

|

Mar-24 |

U.S. Durable Goods Orders |

1.0% |

-- |

2.0% |

Strengths

- The best performing precious metal for the week was palladium, up 3.96 percent. In a note this week Richard Hatch at RBC Capital Markets outlined his preference for palladium over platinum as government policy is shifting to smaller, gas-powered vehicles versus the use of diesel engines. China earlier this year extended its tax incentive scheme to get buyers to favor smaller, gas-powered vehicles in the world’s fastest growing market for cars.

- Following the Fed’s anticipated 25 basis point rate hike on Wednesday, gold bounced over $20, reflecting that the decision was already baked into the price, reports Joni Teves at UBS. Federal Reserve Chair Janet Yellen says the Fed intends to keep its monetary policy accommodative for “some time,” reports Bloomberg.

- Bargain hunters had their eye on gold after its biggest weekly slump in almost four months, writes Bloomberg. On Monday, investors poured nearly $264 million into SPDR Gold Shares, the most since February 7. In a note from Adrian Day this week, more positive news came out of this year’s PDAC conference. Day says that many exploration companies noted that the senior companies seemed more interested in doing deals than they had been the last few years. Lastly, a comment from OceanaGold CEO Mick Wilkes, “It feels like the gold price goes down reluctantly. Every chance it gets, it pops up again.”

Weaknesses

- The worst performing precious metal for the week was a tie, with both gold and silver up 2.03 percent. Even after two straight months of gains, gold’s shine could be dimming due to equities, reports Bloomberg. “There’s little need for gold as a diversifier when the stock market goes up with such high velocity,” Bloomberg Intelligence strategist Mike McGlone said. “Gold is unlikely to go up until the stock market goes down.”

- The outlook for mining in the Philippines remains uncertain as lawmakers deferred a decision on Tuesday about whether to confirm or reject Regina Lopez as the country’s resources minister, according to ScotiaBank. Last month Lopez ordered the closure of more than half the nation’s mines to protect watersheds.

- Chile’s Supreme Court revoked a temporary closure permit this week for Barrick Gold’s Pascua Lama project, reports Bloomberg. The permit, granted by the country’s mining regulator, meant that Barrick didn’t have to make annual payments of $3 million. The project has been shuttered since 2013 when it was court ordered to halt construction due to environmental concerns, the article continues.

Opportunities

- According to Wayne Gordon, executive director for commodities and forex at UBS, gold will rise after Fed Chair Janet Yellen indicated she is going to stick to three interest rate hikes this year and three next year. “That means real interest rates go deeper into negative territory in the U.S., that means a weaker U.S. dollar and it means a better gold price,” Gordon said. In addition, Joni Teves of UBS writes that the risk of a pullback in equities could also boost the yellow metal.

- In a note from Macquarie Research this week, David Doyle writes that lower equilibrium yields mean a flattening yield curve. “Our view on lower potential output growth underpin our estimate for the end-cycle neutral fed funds rate of 1.5 to 1.75 percent range (current FOMC estimate is 3 percent,” the article explains. The group continues that over time as the capacity constraints on the economy intensify, it believes the neutral policy rate will decline modestly rather than rise. Lastly, Doyle writes that the group sees the 10-year treasury yield finding a “fair value” at 2.3 percent, well below the consensus of 3.5 percent.

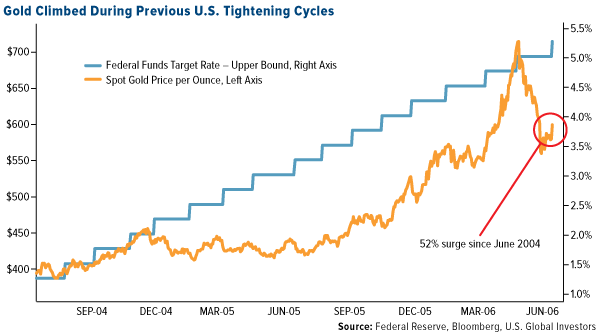

- Those expecting gold to falter following the Federal Reserve’s rate hike, should take a closer look at history, reports Bloomberg. As you can see in the chart below, gold fared well in earlier rounds of rate increases, rising 52 percent in the June 2004 to June 2006 tightening cycle, and 5 percent from the June 1999 to the May 2000 cycle. One reason for this, the article continues, is the Fed tightens monetary policy when it’s concerned about inflation, and that’s good for gold.

- According to Senate Democrats on Monday, Republicans should be wary of attempting to take funding away from Planned Parenthood or pay for President Trump’s border wall in a spending bill that must be passed by April 28, reports Bloomberg. Otherwise, a partial government shutdown would begin on April 29. The threat from Senate Minority Leader Chuck Schumer sets up a climactic first showdown with the president where he would need 60 votes in the senate, the article continues.

- The European Parliament has approved legislation to hold smelters and refiners that import mineral and concentrates to follow a due-diligence process regarding sourcing ores from conflict zones around the world. The law seeks to ensure that the metals produces are sourced responsibly.

- Construction economist Ed Zarenski, who teaches at the Worcester Polytechnic Institute, writes that any economists or investors who are talking seriously about $100 billion in new infrastructure spending each year for a decade are dreaming. An article from Bloomberg recaps Zarenski’s reasoning – he notes that only three times in history has the entire construction industry ever seen a $100 billion increase in a year. Zarenski estimates there is perhaps room for an additional $26 billion per year in infrastructure spending. He notes that industry capacity, not the money itself, is the big constraint on the president’s ambitious budgetary plans.

Energy and Natural Resources Market

Strengths

- Copper prices rose 3.6 percent this week on the back of constricted global supply and a weakening U.S. dollar, according to the Wall Street Journal. Supply concerns linger in the copper market as workers continue to strike at BHP Billiton’s Escondida copper mine, the largest copper mine in the world, based in Chile. To add further tension to the already tight copper market, Freeport-McMoRan faces problems at two of its key mines, where workers in Peru have started to strike and, in Indonesia, the company is locked in a dispute with the government over export licensing. All of this has helped boost copper prices higher, which is a positive read-through for copper.

- The best-performing sector for the week was the FTSE 350 Mining index. The index rose on the back of rising metal prices as the U.S. dollar fell in value as a result of the Federal Reserve’s 25 basis point rate hike.

- Antofagasta, a copper mining company based in Chile, was the best-performing stock this week, finishing up 16.1 percent. The stock rose on the back of a surge in earnings on lower operating costs and better prices, due to rallying copper prices in the fourth quarter of 2016.

Weaknesses

- Iron ore was the worst-performing commodity this week, dropping 5.4 percent. The mineral experienced a volatile week as stockpiles rose in all of China’s major shipping ports and investors expressed concerns over a potentially oversupplied market.

- The worst-performing sector this week was the Alerian MLP Index. The index fell 0.9 percent on the back of poor earnings releases from select members of the group.

- The worst-performing stock for the week was Petrobras, one of the world’s largest energy companies located in Brazil. The company fell 5.6 percent on the back of falling natural gas prices which has significantly hampered profit margins in the company’s natural gas unit.

Opportunities

- Organization for Economic Cooperation and Development (OECD) oil inventories suggest the glut is easing, according to a research report published by RBC Capital Markets this week. Despite U.S. oil inventories sitting near all-time highs, elsewhere the glut appears to be dissipating with OECD inventories dropping well off of last year’s peak. In addition, the Baker Hughes Rig Count increased this week by 14 for the ninth straight week as global demand for oil begins to pick up.

- Net long positions declined in gold but not by much, according to UBS this week. Despite the Fed’s rate hike of 25 basis points on Wednesday, gold prices rallied to a two-week high on the back of a weakening U.S. dollar. Additionally, physical demand in both India and China has been on the rise as price differentials in these regions have been ticking higher.

- Steel demand in China’s construction sector is looking strong, according to a note released by UBS’s research team this week. The bank’s steel analysts toured a handful of steel mills and construction sites in China this week and discovered that order books of steelmakers in the coming months are looking fairly strong. Although many factors affect the price of steel, this is a positive read-through for steel prices from the world’s largest consumer of the metal.

Threats

- After a brief jump in December, U.S. industrial production was unchanged last month, according to Zero Hedge. February saw industrial production unchanged against expectations of a 0.2 percent month-over-month rise. It’s worth noting that U.S. industrial production peaked in November 2014 and has yet to recover.

- Asia remains awash in fuel, according to an article by Reuters this week. As we are three months into OPEC’s announced cuts to reduce crude production to 1.8 million barrels per day (bdp), oil flows to Asia, the world’s biggest and fastest growing market, have risen to near-record highs. The surplus from Asia will add further pressure to global oil prices and weigh on the budgets of major oil producing countries.

- The U.S. government is predicting warmer-than-average weather in the coming months, according to Reuters. Warm weather in April favors the planting of corn, the first of the primary exported crops sown by the U.S. However, as the world is working through an oversupply of corn stocks, specifically in Asia, more corn entering global inventories could potentially further damage already depressed prices of the commodity.

Strengths

- China’s industrial production increased faster than expected in the first two months of the year. Industrial output rose 6.3 percent in January and February combined, and fixed-asset investment also jumped 8.9 percent; both measurements beat estimates.

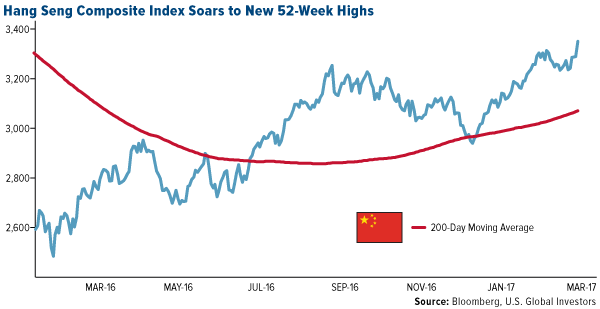

- Chinese stocks in Hong Kong rose the most in more than nine months, reports Bloomberg news, as the Federal Reserve signaled that it is in no rush to raise rates. As you can see in the chart below, the Hang Seng Composite Index soared to new highs this week.

- In Southeast Asia credit-default swaps on the bonds of every Asian emerging market except South Korea have tumbled this year, outperforming debt risk for developed economies like the U.K. and France. According to John Woods, Credit Suisse’s APAC CIO, the reflation story remains attractive and default risk is low.

Weaknesses

- Despite robust growth in China’s economy at the start of the year, retail sales rose less than expected in the first two months of 2017. With slowing car sales, retail sales came in up only 9.5 percent, cooling from 10.9 percent in December.

- Indonesia’s exports and imports expanded at a slower pace in February than a month earlier, reports Reuters. Data from the statistics bureau show that exports rose 11.2 percent year-on-year in February, missing estimates for a 16.2 percent increase, while imports were up 10.6 percent year-on-year. In February, Indonesia’s trade surplus stood at $1.3 billion.

- Cathay Pacific Airways reported its first loss in eight years, writes Bloomberg, also scrapping plans for a second-half dividend. According to the article, competition from Chinese airlines and losses from fuel hedging dented earnings. Shares declined on the news.

Opportunities

- Premier Li Keqiang struck an optimistic tone on China’s relations with the U.S., writes Bloomberg. Following the close of the National People’s Congress this week, Li said that diplomats are discussing a potential meeting between leaders Xi Jinping and President Donald Trump. “We don’t want to see a trade war,” he added.

- Thanks to continued evidence of strength throughout the Chinese economy, Goldman Sachs has become the latest brokerage to upgrade the market, reports Bloomberg. The bank’s strategists are now overweight Chinese stocks, the article continues, with its 12-month forecast for the MSCI China Index boosted to 73 points from 68.

- According to people with knowledge of the matter, China is in talks with Saudi Arabia regarding a potential investment from China’s sovereign wealth fund and its largest energy company in the IPO of the Middle East nation’s state oil producer. The principle investor in the planned flotation by Saudi Arabian Oil Co. would be China Investment Corp. China National Petroleum Corp. may also invest in the IPO, reports Bloomberg.

Threats

- In an attempt to offset the growing might of China, Taiwan plans to boost military spending by about 50 percent next year, reports Bloomberg. Defense expenditures are targeted to rise to 3 percent of GDP next year, up from 2 percent this year, said the Minister of National Defense Feng Shih-kuan.

- Rodrigo Duterte faces an impeachment complaint from a Philippine lawmaker, reports the Wall St Journal, making this the highest-profile challenge yet to the populist president. On Thursday, Congressman Gary Alejano filed the complaint accusing Duterte of corruption, violating the constitution, betraying public trust and other high crimes. Alejano said the leader must be made accountable for a “state policy of killings.” Duterte’s spokesman denied the Philippine leader committed any impeachable offense.

- According to Reuters, Japan plans to dispatch its largest warship on a three-month tour through the South China Sea beginning in May. This would be Japan’s biggest show of naval force in the region since World War II, the article notes.

Emerging Europe

Strengths

- Poland was the best performing country this week, gaining 3.64 percent. Consumer prices in Poland rose faster than expected last month to hit a fresh four- year high. Inflation reached 2.2 percent in February compared to the same time a year ago, up from expectations of 2.1 percent and higher than January’s 1.8 percent. Despite the recent pickup in inflation, Polish inflation has long been below the central bank’s inflation target of 2.5 percent.

- The Turkish lira was the best performing currency this week, gaining 3.19 percent against the dollar. The Turkish central bank held its three key rates unchanged and hiked the late liquidity rate by 75 basis points.

- The material sector was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 59 basis points. Greece is working on its second review with its creditors, and most likely the final agreement will not happen March 20 but sometime in April or late May.

- The Romanian leu was the worst relative performing currency this week, gaining 51 basis points against the dollar. Demand for local Romanian bonds is low. The last two local bond auctions were cancelled because of insufficient demand and external pressure on yield. Government officials commented that it is temporary and circumstantial, driven mostly by the U.S. Federal Reserve’s effect on investment sentiment.

- The real estate sector was the worst performing sector among eastern European markets this week.

Opportunities

- Preliminary results show that Dutch Prime Minister Mark Rutte’s center-right People’s Party for Freedom and Democracy won the election in Netherlands. The premier’s party is on track to win 33 seats out of the 150 seats, while the Party for Freedom led by Geert Wilders who wants to halt Muslim immigration and leave the European union, secured 20 seats.

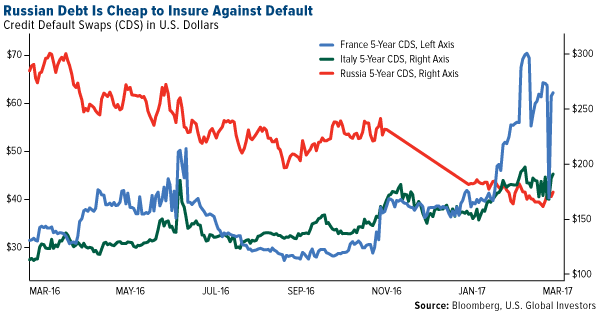

- According to Natasha Doff Bloomberg publication, political turmoil in the eurozone is making Russia look like a safe bet to bondholders. The nation’s debt is cheaper to insure against default in Italy or France. After dropping more than 100 basis points in the past year, Russian five-year credit default swaps trade at a low level, below France and Italy.

- The German ZEW survey rebounded in March to 77.3, after falling slightly to 76.4 in February. Almost three months into 2017, the German economy appears to be growing at least as fast as the previous quarter. Bloomberg economists expect the German economy to expand by 0.4 percent again in the first quarter of the year. Strong growth in Germany will support growth in eastern Europe.

Threats

- With eurozone inflation now above the European Central Bank’s (ECB) target, most economists expect the ECB will announce an exit from easy money policy. According to the headline of an article by Tom Fairless in the Wall Street Journal, “ECB walks fine line as it prepares to signal possible end to stimulus.” An announcement of policy change could rock markets and upset the eurozone’s recovery.

- Turkey announced a list of political sanctions against the Netherlands following the refusal to allow two Turkish ministers to campaign for the upcoming referendum on the executive presidency. Turkey stopped all high level political relations with the Netherlands, barred Dutch ambassadors to enter Turkey, closed Turkish airspace to Dutch diplomats and advised Parliament to withdraw from a Dutch-Turkish friendship group. Netherlands is an important source of foreign financing for Turkey. The country is one of Turkey’s top 20 trade partners, having accounted for 2.5 percent of total exports and 1.5 percent imports last year.

- Unemployment in Turkey rose to its highest level since 2010, reaching 12.7 percent in December from 12.1 percent in November. Turkey also suffers from the worst economic slump since 2008, with growth shrinking by 1.8 percent in the third quarter. The Turkish lira has also been the worst performing emerging market currency of 2017.Turkey has been hit by political and security fears that put pressure on sectors from tourism to banking. The executive presidency referendum is scheduled for April 16.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits