SUMMARY

- Global Supply Chains Contain Inflation

- Avoid the Debt Ceiling Drama

- Analysis of the Proposed Health Care Law Carries Valuable Lessons

Globalization has profoundly affected politics, society and economic performance. Among its most significant results has been persistent downward pressure on prices. As governments across the world consider their participation in free trade, they should appreciate that withdrawal could come at a high cost.

Among the most prominent developments of the last generation has been the taming of inflation in major markets. Monetary policy has often been credited for this; restrictions in money growth and the anchoring of expectations have been widely cited as bringing about this end. But the dominant driver of this outcome may instead have been the integration of national markets into a global marketplace.

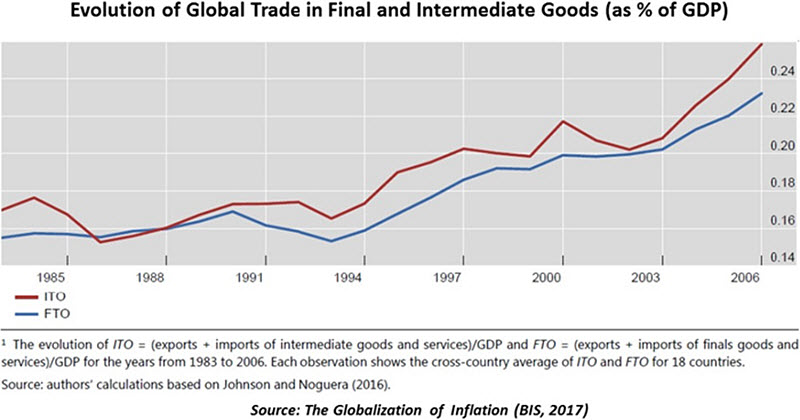

A direct and easily measured example comes from trade in goods. Price movements for goods in an exporting nation are echoed in price movements of finished and intermediate goods in an importing nation. This is especially true for globally traded raw materials, where individual countries are often price takers. The chart below shows the growth in the trade of both final and intermediate products, where the blue line represents total trade in finished goods (exports plus imports as a percentage of GDP) and the red line charts the growth of trade in intermediate goods.

Indirect effects of globalization on prices can be even more powerful. The import content of U.S. personal consumption expenditures is less than 15 percent, but the influence of trade on the prices paid is much larger. Opening an economy to trade leads to competition at a global level and pushes down prices of domestically produced goods. The “threat” of cheaper imported substitutes keeps a lid on domestic production costs. Like the cost any other factor of production, wage growth (and its impact on overall inflation) is also kept in check through this mechanism.

It works something like this: slack in the Chinese economy keeps Chinese wages, and export prices, down — a phenomenon often called “exporting deflation.” Since U.S. producers compete in the same marketplace, they must either gain efficiencies or increase the import content of their value chains to remain competitive.

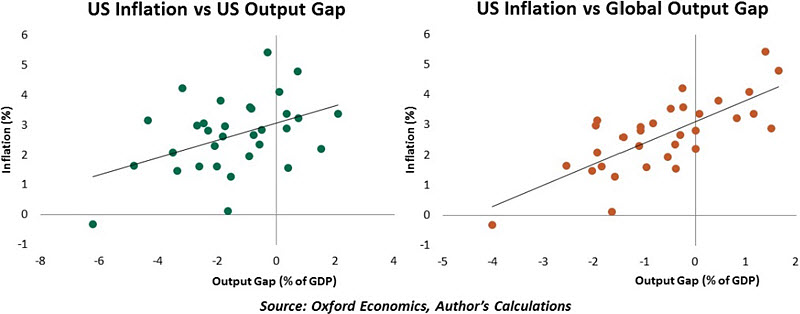

A recent paper by the Bank for International Settlements (BIS) documents the importance of global value chains in determining domestic prices. Their findings challenge the country-centric view of inflation and emphasize the need to look at the global output gap (actual output minus potential output) as a determinant of domestic inflation.

To illustrate this, the charts below plot U.S. inflation against the U.S. output gap (left) and against the global output gap (right). Each dot represents a year from the period 1985-2015. An upward sloping scatter would suggest strong positive correlation between the two variables. As we can see, the U.S. slack versus inflation scatter is quite dispersed, while the association with global slack is tighter and more positive.

To be sure, this is an asymmetric relationship, driven by both the direction of trade and the type of goods traded. Developing nations have a much larger impact on developed ones than the other way around, as the former have a competitive advantage in the production of goods.

The Federal Reserve was among the first to appreciate this. In the 1990s, Alan Greenspan cited a “new paradigm” as support for holding interest rates constant even as real growth accelerated. A later paper assessing import competition’s impact on U.S. inflation vindicated his observation. As a result of Greenspan’s prescience, the American economy entered what came to be known as the Great Moderation —an era of unprecedented price and output stability that lasted until 2008.

Success has many fathers, and there is vigorous debate over what was behind the stability of that period. Many have sought to attribute it to Paul Volcker’s war on inflation in 1980s and the subsequent adoption of de facto inflation targeting across the developed world. As central banks credibly committed to price stability, inflation expectations settled.

But the Great Moderation also coincided with the entry of developing economies, particularly China, into the global market place. Many have argued that a steady supply of cheap consumer durables from these low wage economies helped keep prices in check in places like the U.S. and Europe. It follows that central banks can sometimes have limited influence on domestic inflation in the face of external factors, and may therefore struggle to meet their inflation targets. If central banks push too hard, the excess of liquidity in the system may serve only to inflate the prices of assets, not goods.

The eurozone knows this well. European Central Bank (ECB) chief Mario Draghi

noted last year that “prices set by producers in the euro area and those set by producers in trading partner countries are indeed highly correlated.” The ECB’s struggle to lift inflation towards its 2% target has been due, in part, to the eurozone’s openness to trade.

In light of this evidence, some have suggested that policy frameworks employing the Phillips Curve, the non-accelerating inflation rate of unemployment (NAIRU) or the Taylor Rule may be of limited help in a global marketplace. These three concepts — which link unemployment, inflation and policy interest rates — are typically based only on domestic readings. For larger economies, global formulations of these metrics may be required.

The Bank of England’s Mark Carney offered a counter to this argument in a

speech at the Federal Reserve’s 2015 Jackson Hole conference. Carney noted that while global inflation rates have a much greater correlation than they did in the past, markets for key services such as shelter and medical care are more localized. Inflation retains important idiosyncratic elements between countries, and central banks are therefore justified in retaining a local focus.

The debate over the drivers of inflation and proper central bank orientation could become a moot point. The new nationalism that is spreading across continents aims to roll back globalization. Increased protectionism will end up boosting inflation–not just via higher tariffs or the substitution of expensive domestic alternatives—but also via less efficient supply chains. The subsequent loss of purchasing power would be damaging to standards of living the world over.

So the inflation narrative of the last generation has important implications for both central banks and governments as they contemplate strategy for the coming years. A proper reading of history is essential for setting policy for the future.

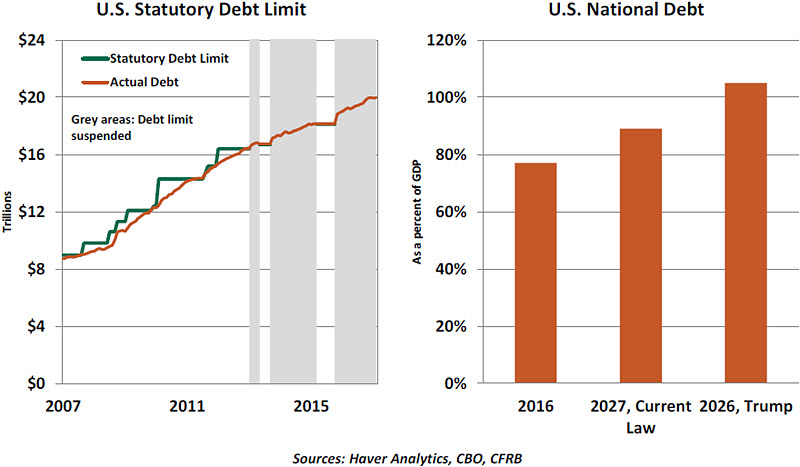

The Ceiling Comes to the FloorThe debt ceiling is back and is again making headlines in the financial pages. March 15 was the last day the U.S. Treasury could issue new debt to meet its obligations. Although this event was not followed by market turbulence, the likelihood of market volatility later in the year is a non-trivial risk to consider.

The debt limit (also referred to as debt ceiling) is the maximum debt the U.S. Treasury can issue to the public and other federal agencies. The Bipartisan Budget Act of November 2015 suspended the debt ceiling until this past Wednesday. A moratorium on Treasury debt issuance is now in force, and will not end until the debt ceiling is raised by the Congress.

In the interim, the U.S. Treasury has resorted to “extraordinary measures” to avoid breaching the debt ceiling. Treasury Secretary Steven Mnuchin has already notified Congress about the suspension of sales of State and Local Government Series securities and the postponement of investments related to the Civil Service Retirement and Disability Fund, Postal Service Retiree Health Benefits Fund, and the Federal Employees’ Retirement System.

Extraordinary measures enabled the U.S. Treasury to funds its operations before Congress decided the national debt limit in 2015. Analysts estimate a similar plan can work this time around, with funds available until the third quarter of 2017. This estimate is imprecise, as it depends on the size and timing of tax revenues and federal expenditures.

The U.S. Congressional Budget Office (CBO) estimates that, under current law, publicly held U.S. national debt will touch 89% of gross domestic product (GDP) in the next ten years. Projections from the Committee for a Responsible Federal Budget indicate that if President Trump’s campaign promises of an expansionary fiscal policy are implemented, the national debt will escalate to 105% of GDP in the next decade.

Bipartisan debt ceiling legislation is not required as Republicans control both chambers of Congress, but there are differences among Republicans that could result in debt ceiling drama later in the year. Deficit “hawks” in the U.S. House of Representatives used the debt ceiling as leverage to obtain large spending cuts in 2011, 2013, and 2014.

It will be interesting to see whether they take the same posture on proposed fiscal expansion that comes from within the Republican platform. Tax reductions and infrastructure expansion are unlikely to be deficit neutral, and the hawks in Congress could use the debt ceiling to pre-empt their advancement.

Democrats might consider blocking an increase in the debt ceiling if spending reductions are not to their liking. But they would do well to avoid another government shutdown, which tarnished the Republicans the last two times around. And the 2011 debate over the debt ceiling resulted in a rating downgrade of U.S. government debt.

President Trump has yet to share his current view on the debt ceiling, but he has been critical in the past of the willingness of Republicans to allow increases. Without leadership from the White House, an impasse may develop, which has the potential to upset financial markets.

There is no need for this kind of volatility. The United States is the only developed country with a limit on its borrowing capacity. Proponents note that the debt ceiling provides a useful checkpoint that focuses budget priorities. But since the debt ceiling has been raised 44 times since 1980, it really isn’t providing much discipline at all. We would be better off without it.

A Healthy Process Economic projections are hard to assemble. They rely on a long series of assumptions that can certainly be questioned. They are based on past patterns which may not be a good guide to future performance. They are almost always wrong. But they are also absolutely essential.

There was controversy this week when the CBO released its

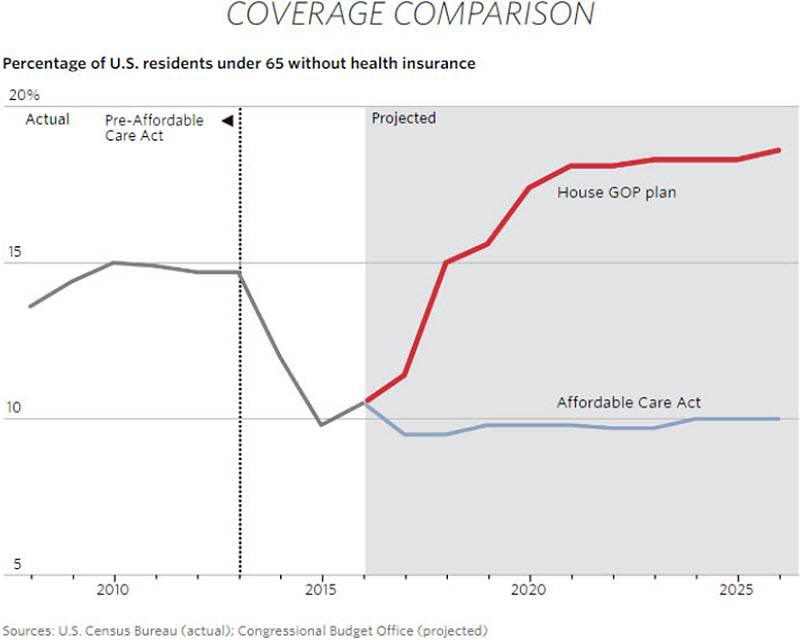

analysis of American Health Care Act (AHCA). The AHCA is designed as the “replacement” for the Affordable Care Act, the sun-setting of which was a key campaign promise of the current administration. The CBO found that the AHCA would save $337 billion over the next ten years, but would also cost 24 million people their health care coverage.

Immediately after the report was filed, it met with ridicule from supporters of the new legislation. The integrity and intelligence of the CBO were called into question. Tom Price, secretary of the Department of Health and Human Services, stated that “The CBO report’s coverage numbers defy logic.”

To economists, though, the findings are entirely logical. Eliminating the mandate that people purchase health insurance and trimming the subsidies they receive will result in lower levels of coverage. While this would save the government money, society would to pay higher health care bills for the uninsured through taxes and insurance premiums.

The CBO has a well-deserved reputation for rigor and impartiality. Evaluating programs through an economic lens (however cloudy) reveals causes and effects that can be a useful guide to possible alterations. There are signals that this process is already working as intended.

The evaluation of the AHCA is only a warm up act for the review of larger proposals that headline the administration’s fiscal plans. As we head toward the main events, support for the CBO and economic analysis must be sustained.

© Northern Trust

www.northerntrust.com

© Northern Trust

Read more commentaries by Northern Trust