Strategist: Keep Calm, Tax Reform Is On Its Way

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Stocks had their worst day in months on Tuesday. The S&P 500 Index retreated more than 1 percent for the first time since October, and the small-cap Russell 2000 Index gave back more than 2 percent for the first time since September. As of today, the Dow Jones Industrial Average has been down nine out of the past 10 days.

Throwing a monkey wrench into the Trump rally this week was fresh uncertainty House Republicans could successfully repeal and replace Obamacare, one of their headline campaign promises for seven years now. Failure to do so, it’s believed, could seriously push back tax reform. And the promise of tax reform—along with deregulation and infrastructure spending—is arguably what’s driven the Trump rally.

This uncertainty was confirmed today when President Donald Trump asked House Speaker Paul Ryan to pull the new health care bill from consideration—a stunning setback for the new president, who largely ran on his credentials as a master negotiator and closer.

The thing is, the selloff this week was a huge overreaction. That’s the opinion of Marko Papic, geopolitical strategist with BCA Research, who visited our office Thursday and briefed us on the investment implications of the domestic and European political climate. As always, Marko dazzled us with his deep intellect, quick wit and infectious enthusiasm.

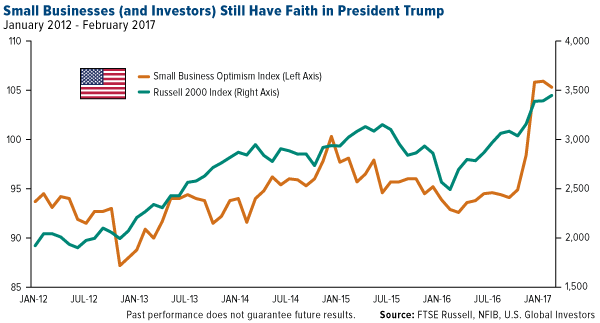

In his view, the market rally that immediately followed the election of President Donald Trump is still the “right” response. Among the companies that saw impressive returns were domestic, small-cap names, which have the most to gain (and less to lose) from Trump’s pledge to lower corporate taxes, slash regulations and raise tariffs. Small business optimism, meanwhile, posted its highest readings since 2004.

Investors, according to Marko, are making too much of the Obamacare issue. Regardless of its failure to be repealed, tax reform is on its way. Just today, Treasury Secretary Steven Mnuchin reassured Americans that we could still expect “comprehensive” tax reform by August. It’s also worth recalling that, even though he failed to reform health care during his eight years in office, President Bill Clinton still managed to tackle tax reform with the Omnibus Budget Reconciliation Act of 1993.

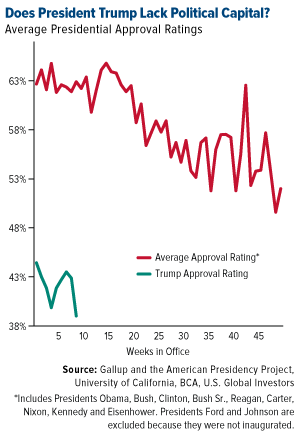

Increasing the likelihood that tax reform and infrastructure spending can be brought to light is, paradoxically, President Trump’s historically low approval rating. As you can see, he significantly trails the average rating of nine previous presidents during their same weeks in office. Congress’ job approval fares even worse at 28 percent, as of February.

What this means is the sound of the clock ticking is deafening. Midterm elections are less than 20 months away, and Trump could very well be a one-term president. According to Marko, this gives Trump tremendous political capital among those who share his vision and urgently wish to pass legislation toward that end.

Trump is seeking high growth now, not in 2020 or 2024, and I think it’s a mistake for investors to dismiss him,” Marko said, adding that the president’s goal of 4 percent GDP growth is more than attainable. But how?

Get Ready for Inflation

I’ve written about the inflationary implications of Trump’s more protectionist policies before. Over the past 30-plus years, free trade agreements (FTAs) such as NAFTA have certainly been easy on consumers’ pocketbooks. But the downside is that many U.S. companies have found it challenging, if not impossible, to compete with overseas companies whose operating expenses are a fraction of the cost, forcing them to shut down or move production out of the country.

There’s disagreement among economists and policymakers about the extent of FTAs’ impact on jobs and wages here in the U.S., but the case can be made that they’ve been negative. Certainly this is the case Trump and his supporters made during his campaign.

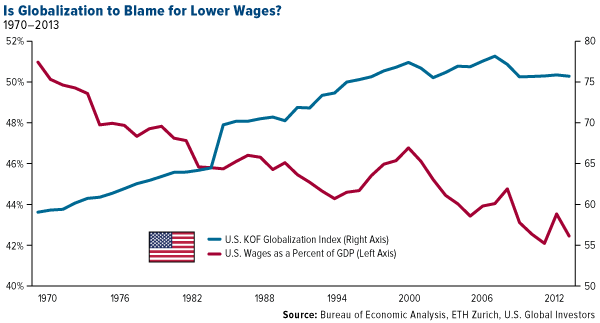

In the chart below, I compare U.S. wages as a percent of GDP between 1970 and 2013 and the KOF Globalization Index, which measures the economic, social and political dimensions of globalization on a scale from one to 100. The closer to 100, the more globalized a country is. As you can see, there’s at least a strong correlation between rising globalization and falling wages in the U.S.

With this in mind, Trump’s director of the National Trade Council, Peter Navarro, argued in January that “there is no question” the U.S. needs a border adjustment tax (BAT) to bring jobs back and grow wages:

“Would you rather have cheap subsidized… goods dumped into Walmart and not have a job and not have your wages go up in 15 years, or would you like to pay a little bit more—not much—a little bit more, and have a job and have your wages going up? I think the American people are going to make that choice.”

Whether you agree with Trump and Navarro on this point, it’s important to recognize that inflation is poised to surge in the coming years. Consumer prices rose 2.7 percent year-over-year in February, the seventh straight month they’ve advanced. And if Trump manages to restrict immigration and raise trade barriers, we can expect prices to rise even more—along with manufacturing activity, wages and ultimately GDP growth.

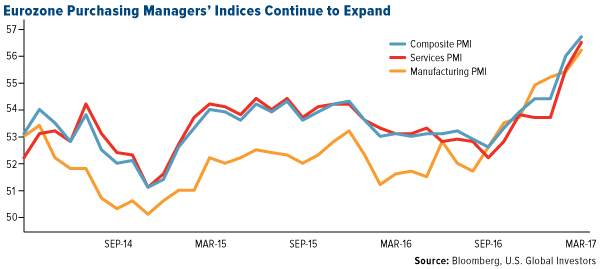

A final thought I want to share from Marko’s visit is his bullishness on Europe right now. “Forget about what you see in the news about Europe,” he said, “and look at the data.”

He has a point. For one, the Markit Flash Eurozone PMI, released today, showed the region’s manufacturing activity growing at its fastest pace in six years. For the month of February, its PMI rose to 56.7.

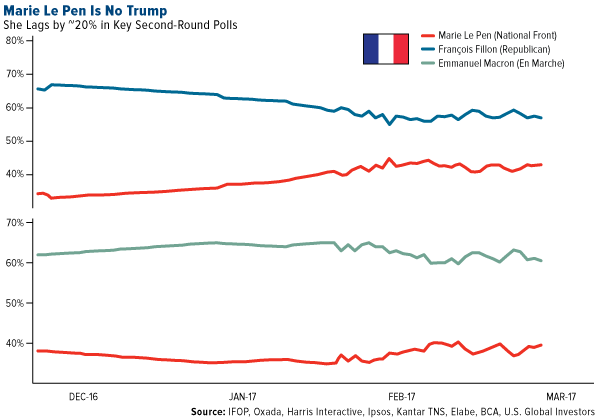

Terrorism remains a concern, as we saw in London this week, but the Syrian refugee crisis is emphatically done. Also overblown are Euroscepticism—or criticism of the European Union and its currency, the euro—secessionism and Trump-like populism. Geert Wilders’ far-right, anti-Muslim Party for Freedom (PVV) failed to secure an electoral victory in the Netherlands this week. Meanwhile, in France, the far-right Marie Le Pen still struggles to close the gap between herself and her two rivals, former prime minister of France François Fillon—currently being investigated on charges of corruption—and the socialist Emmanuel Macron.

With only one month remaining before France’s presidential election, Le Pen trails both rivals by about 20 points, throwing her candidacy into doubt. At this point in the U.S. presidential election, Trump had proven himself a very competitive candidate, trailing the much more politically experienced Hillary Clinton by single digits.

The key risk, according to Marko, is the upcoming Italian election, to be held no later than May 23. More and more, Italians are turning against the euro, and Euroscepticism is alarmingly high relative to other European Union countries. Whereas productivity is rising in Germany, France and Spain, Italy’s has stagnated since 2000.

Whatever happens, it’s important to monitor the eurozone’s PMI because, as I’ve often pointed out, it’s a precursor to commodities demand.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.52 percent. The S&P 500 Stock Index fell 1.44 percent, while the Nasdaq Composite fell 1.22 percent. The Russell 2000 small capitalization index lost 2.65 percent this week.

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.52 percent. The S&P 500 Stock Index fell 1.44 percent, while the Nasdaq Composite fell 1.22 percent. The Russell 2000 small capitalization index lost 2.65 percent this week.

- The 10-year Treasury bond yield rose 8 basis points to 2.41 percent.

Domestic Equity Market

Strengths

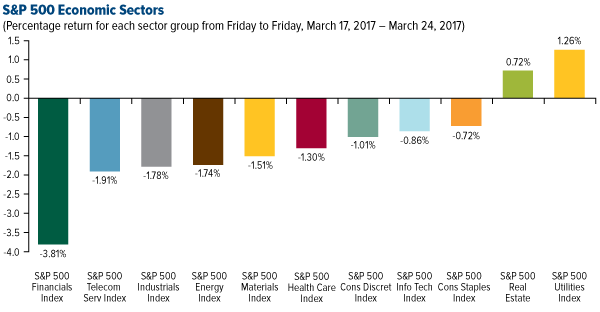

- Utilities was the best performing sector for the week, increasing by 1.26 percent versus an overall decrease of -1.44 percent for the S&P 500.

- Micron Technology was the best performing stock for the week, increasing 10.19 percent.

- Disney rallied after "Beauty and the Beast" smashed a box office record. The movie raked in a weekend box-office total of $350 million, $170 million in the U.S. and $180 million overseas.

Weaknesses

- Financials was the worst performing sector for the week, falling 3.81 percent versus an overall decrease of 1.44 percent for the S&P 500.

- Transdigm Group was the worst performing stock for the week, falling 12.50 percent.

- FedEx missed big on earnings. The courier giant earned an adjusted $2.35 a share in its third quarter, missing the $2.62 that Wall Street was expecting by a wide margin. Revenue was in line at $15 billion.

Opportunities

- Takeover activity has cooled down a bit in recent months, but there are still some big deals on the horizon. In a note to clients sent March 20, Morgan Stanley updated its Acquisition Likelihood Estimate Ranking Tool (ALERT model), a model that tracks "stock characteristics, cohort membership, and data regarding offers to forecast probabilities that stocks receive tender offers in the coming 12 months." Here's a list of the nine tech companies that Morgan Stanley says are most likely to receive takeover offers: NCR Corp, Nuance Communications, Cavium, Zebra Technologies, Coherent, Wex, Cypress Semiconductor, Teradata, Tableau Software.

- The rise of e-commerce and titanic shifts in how shoppers spend their money has hit malls and stores hard. Visits to malls declined by 50 percent between 2010 and 2013, according to the real-estate research firm Cushman & Wakefield. Amazon, in contrast, has continued to eat up market share. The company accounted for 53 percent of online sales growth in the U.S. in 2016, according to market research firm Slice Intelligence. According to equity analysts at Morgan Stanley, the retail giant has a new weapon in its war against brick-and-mortar retailers: credit cards. In January the firm renewed its credit card partnership with JPMorgan, and rolled out a new "Prime-only, 5 percent cash back incentive for purchases on Amazon." Morgan Stanley said that the firm's new card will drive more consumers to spend their money on Amazon. "Amazon's new Chase card is expected to drive more spend towards Amazon and away from retailers, as 82 percent of prospective new Amazon card owners plan to shop ‘more’ or ‘a lot more’ on Amazon than they currently do." The bank has a price target for Amazon of $900 per share, above Amazon's current share price of $849.84.

- Deutsche Bank's Chief International Economist Torsten Sløk shared a chart showing that markets are currently pricing in a less than 10 percent probability of a bear market over the next 12 months, and an even smaller probability over the next six months.

- Ford guidance disappointed. Shares of Ford Motor were down Thursday morning after the automaker reported it expects adjusted first-quarter earnings of $0.30 to $0.35 per share, well below the $0.47 that is expected by the Bloomberg consensus.

- Sears fell off a cliff. Shares of the 131-year-old company were down 13 percent after an abysmal quarterly report. The stock has lost 96 percent of its value since 2007, as the owner of Sears and Kmart stores struggled to keep pace with changing consumer tastes and online competition. In its annual report released Tuesday, Sears said "substantial doubt exists related to the company's ability to continue as a going concern."

- GameStop is shutting down stores. The video game retailer reported that comparable sales slumped 16.3 percent year-over-year in the fourth quarter and said it expected to close 2-3 percent of stores worldwide later this year. Shares were down by as much as 8 percent in Thursday's after-hour session.

The Economy and Bond Market

Strengths

- The Conference Board index of leading economic indicators, a measure of future economic activity, showed a gain of 0.6 percent for February, above the expected 0.5 percent.

- European PMIs beat again. Markit’s eurozone PMI hit 56.7 in March, its best reading in almost six years, according to IHS Markit data released Friday.

- Preliminary U.S. durable goods orders for February came in at 1.7 percent, above the 1.4 percent expectations.

Weaknesses

- Initial jobless claims rose above 250,000 for the first time in eight weeks. Claims, which count the number of people who applied for unemployment insurance for the first time in the past week, rose by 15,000 to 258,000.

- Existing home sales eased in February from a 10-year high. U.S. existing-home sales fell 3.7 percent at a seasonally adjusted annual rate of 5.48 million in February, according to the National Association of Realtors.

- The automobile loan market is showing signs of stress. U.S. auto loan and lease credit loss rates weakened in the second half of 2016, according to a new report from Fitch Ratings, which said they will continue to deteriorate.

Opportunities

- U.S. consumer confidence will be reported on Tuesday, with economists expecting a continuation of consumer optimism.

- The PCE deflator will also be released next Friday. Last month, the core PCE deflator posted an outsized 0.3 percent month-over-month increase. The CPI data points to a more moderate 0.1-0.2 percent gain for February.

- The German Ifo (Monday) and the eurozone's economic confidence survey (Thursday) should confirm that the European economy is growing well above-trend.

Threats

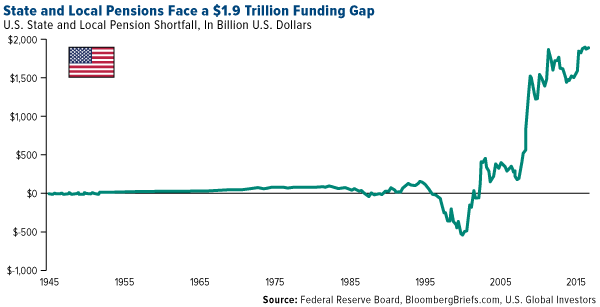

- A drop in the sale of state and local government debt this year may have a culprit other than rising interest rates. Analysts at Morgan Stanley said the rising retirement system costs have made local governments more leery of running up new debts. State and local revenues have not kept pace with growth in total liabilities that now amount to $4.97 trillion, the analysts say. Unfunded pension obligations have risen to $1.9 trillion from $292 billion since 2007, according to data compiled by Bloomberg.

- U.S. personal spending/income data will be released next Friday. Real consumer spending contracted in January and the advance retail sales report suggests that February could be another soft month.

- Bank lobbyists who opened the Trump era with great expectations for sweeping regulatory reform are privately striking an increasingly dismal tone as hopes for a quick and thorough rewrite of Dodd-Frank legislation dim. Lobbyists say they are facing the reality that bank deregulation legislation will have to wait in line behind other bigger priorities such as health care reform and taxes. Even if Congress does look to rewrite the 2010 Dodd-Frank law, it is unlikely to muster enough votes in the Senate for the strong, across-the-board overhaul industry leaders had hoped for, roughly a half dozen lobbyists told Reuters in recent interviews.

This week spot gold closed at $1,245.23, up $15.94 per ounce, or 1.30 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.27 percent. The U.S. Trade-Weighted Dollar Index finished the week lower by 0.61 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Mar-23 |

U.S. Initial Jobless Claims |

240k |

258k |

243k |

|

Mar-23 |

U.S. New Home Sales |

564k |

592k |

558k |

|

Mar-24 |

U.S. Durable Goods Orders |

1.4% |

1.7% |

2.3% |

|

Mar-27 |

H.K. Exports YoY |

15.9% |

-- |

-1.2% |

|

Mar-28 |

U.S. Conf. Board Consumer Confidence |

113.6 |

-- |

114.8 |

|

Mar-30 |

Germany CPI YoY |

1.8% |

-- |

2.2% |

|

Mar-30 |

U.S. GDP Annualized QoQ |

2.0% |

-- |

1.9% |

|

Mar-30 |

U.S. Initial Jobless Claims |

245k |

-- |

258K |

|

Mar-31 |

Eurozone CPI Core YoY |

0.8% |

-- |

0.9% |

Strengths

- The best performing precious metal for the week was palladium, up 4.22 percent on improving expectations for the automotive industry where palladium is principally used to clean gasoline emissions.

- According to ZeroHedge, a new trend is gaining popularity in China – digital gold “gifting.” Tencent’s digital gold packets, known as microgold, are backed by the country’s biggest bank and allow users to send funds that track the real-time value of gold over the WeChat platform. An ICBC document shows that during the Lunar New Year, WeChat users sent 70,000 microgold packets across the platform worth $14.5 million.

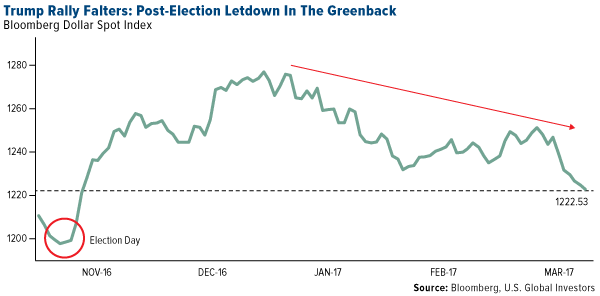

- Gold ETFs recorded inflows over the past two days totaling nearly 9 tons, reports Commerzbank, reversing more than half of outflows previously seen this month. Noting a drop in net long positions to their lowest level since the beginning of the year during the run-up to the Fed meeting, one analyst wrote that this means there is ample upside potential for gold. As seen in the chart below, we are seeing the longest losing run for the dollar since November, reports Bloomberg, as gold advanced to its highest level in three weeks on haven demand amid a global selloff in stocks.

Weaknesses

- The worst performing precious metal for the week was platinum, down 0.03 percent. Investors are not as excited about platinum versus palladium, as the former is more important in cleaning up emissions from diesel engines. In fact, diesel engines have been cited for their high level of particulate output and may face greater regulation in the future.

- The Democratic Republic of the Congo warns that proposals by the Trump administration to suspend Section 1502 of the Dodd-Frank Act will undermine both stability and security, reports Bloomberg. A roll-back in this law would encourage an “escalation in the activities of non-state armed groups,” said Mines Minister Martin Kabwelulu in a letter to the SEC dated March 13. A London-based advocacy group called Global Witness even said that suspending the law would be a “gift to warlords and corrupt businesses.”

- Robert Burgess writes for the Bloomberg Daily Prophet this week, warning investors that it may be time to prepare for the Trump “correction” and forget about the Trump trade. Prize-winning economist Robert Shiller recently said that the last time he remembers equity investors being as bullish as they are now was in 2000 and that didn’t end well. If the markets really thought Trump’s policies would juice up the economy then the dollar would be the prime beneficiary, the article continues, but instead the greenback is on an epic slump.

Opportunities

- “By most objective measures, we are deep into the longest period ever of excessively easy monetary policy,” said Stanley Druckenmiller. Bloomberg reports that Druckenmiller sees the U.S. in the biggest and longest dovish deviation from historical norms during his entire career. His solution? “Some regard it as a metal, we regard it as a currency and it remains our largest currency allocation.”

- A rebound in exploration by global miners could see spending hit $18 billion by 2025, writes David Stringer of Bloomberg. Exploration budgets are on the rise after hitting an 11-year low of around $10 billion last year when companies cut costs in the wake of a collapse in prices, according to Richard Schodde of MinEx Consulting. Ivan Glasenberg, CEO of Glencore, also notes the cut seen in gold production from mines run by majors, saying “there are no new big mines being built in the world today.” A boost in appetite for exploration could lead investors to focus more on the exploration and development companies as we go forward, as those companies will be the ones making new discoveries.

- Golden Star Resources has announced its exploration strategy for 2017 in a note this week to investors. Sam Coetzer, President and CEO, had the following to say: “During 2016 our focus was on delivering our two underground development projects, but I am pleased that we are now in a position to turn part of our focus back to exploration. I believe strongly that our assets present an exploration upside opportunity, with both Wassa Underground and Prestea Underground having the potential to expand production on an annual basis and extend their mine lives beyond the current seven and five years, respectively.”

Threats

- Detour Gold released its updated life of mine plan this week, with the main impact being lower production, a higher strip ratio and higher costs over the next five years. The company also recapped its fourth quarter 2016 financial results, noting that its adjusted loss of 3 cents was well below consensus of a 4-cent gain. Investors that are in love with Detour, or worse, married to the company, could be feeling an “Allied Nevada”-like moment if the gold price doesn’t improve.

- In its annual report, Copperbelt Energy Corp says that Zambia’s High Court is expected to rule on a three-year dispute over tariff increases to the copper mining industry. If the court rules in favor of the increases by the energy regulator, Copperbelt will owe state-owned Zesco $276 million, reports Bloomberg, with the cost being passed on to Glencore and First Quantum.

- On Tuesday, equities dropped across the globe as investors start to question President Trump’s ability to enact his pro-growth policies, reports Bloomberg, casting doubt on the so-called reflation trade.

March 23, 2017Lithium Suppliers Can’t Keep Up with Skyrocketing Demand |

March 20, 2017America’s New Emphasis on Fiscal Policy |

March 15, 2017America’s Infrastructure Shortfall Could Be an Investor’s Best Friend |

Strengths

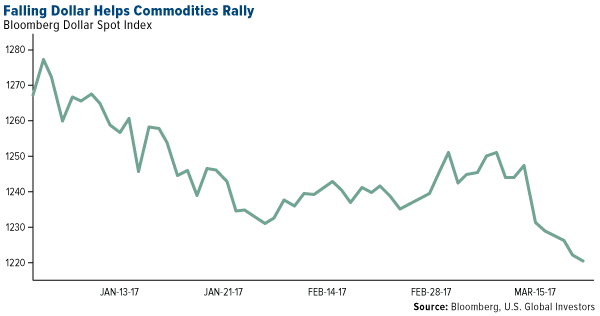

- The U.S. dollar rally comes into question this week on the back of U.S. rate policy and trade concerns, according to the Financial Times. Despite last week’s interest rate rise by the Federal Reserve, investors have interpreted the rate hike as dovish rather than hawkish, which normally helps the greenback appreciate. In addition, G20 finance ministers have yet to determine a clause to combat trade protectionism leading to uncertainty amongst global investors. However, a falling U.S. dollar helps boost commodity prices which have rallied across the globe this week. A positive read-through for commodity prices!

- The best performing sector for the week was the S&P/TSX Composite Gold Sub Industry Index. The index rose 2.14 percent on the back of gold’s spectacular performance this week setting in its best week in six weeks as the dollar fell in value.

- Goldcorp Inc., one of the world’s largest gold mining companies, was the best performing stock this week finishing up 3.57 percent. The stock rose on the back of rallying gold prices.

Weaknesses

- Iron ore was the worst performing commodity this week dropping 4.13 percent. The mineral dropped in value as investors have become skeptical about the true demand for steel in China. Investors are now concerned over the legitimacy of the minerals rally and are beginning to question whether or not the rally has reached its limits. A negative read-through for iron ore.

- The worst performing sector this week was the S&P Super Composite Steel Sub Industry Index. The index fell 7.3 percent on the back of tumbling steel and iron ore prices around the world.

- The worst performing stock for the week was Vale S.A., one of the world’s largest producers of iron ore and nickel located in Brazil. The company fell 8.1 percent on the back of falling iron ore prices.

Opportunities

- Economic data in the United States and the eurozone area came in strong this week, according to Bloomberg. Orders for U.S. durable goods increased more than forecasted, coming in at 1.7 percent versus a consensus estimate of 1.5 percent. The Purchasing Managers’ Index (PMI) in the eurozone area climbed to 56.7 from February’s print of 56. A positive read-through from the two most influential economies.

- A key railway in central Andes Peru that used to transport concentrates of copper, zinc and silver will be out of service in the coming weeks due to deadly floods and mudslides, according to Reuters. As Peru is a key exporter of these metals and minerals, constricted supply from major exporters can potentially lift prices at times if dynamics in global markets accommodate such disruption. A positive read-through for copper, zinc and silver prices.

- U.S. President Donald Trump officially gave the greenlight to TransCanada Corporation’s Keystone XL pipeline on Friday. The approval reverses a decision made by former President Barack Obama who rejected the project during his presidency. Completion of the project will lower consumer fuel prices and create roughly 28,000 jobs, according to Reuters. A positive read-through for raw materials.

Threats

- All drill and no frack is leaving thousands of wells unfinished in U.S. shale, according to Reuters. U.S shale producers are drilling at the highest rate in 18 months; however, a record number of wells have been left unfinished signaling that output may not rise as quickly as drilling activity indicates. Coupled with a glut in oil inventories across the globe, the big picture for oil may not be as bright in the near term as many analysts believe. A negative read-through for oil prices.

- After weeks of negotiations, the strike at BHP Billiton’s landmark mine, Escondida, has finally come to an end. Workers at the mine have decided to invoke a rarely used legal provision that allows union members to extend old contracts, according to Reuters. Escondida is one of the world’s largest copper mines, accounting for roughly 5 percent of the world’s copper supply. This supply coming back online may have negative consequences to copper’s rally in the weeks to come.

- U.S. PMI data came in worse than expected on Friday at 53.2 versus consensus expectations of 54.3, according to Bloomberg. The index fell to its lowest levels since before the election, suggesting the U.S. economy may be struggling to sustain momentum in growth. A negative read-through for raw materials.

Strengths

- Energy constituted the top-performing sector in the Hang Sang Composite Index (HSCI) over the last five trading days, rising 2.24 percent in that time, and edging out properties & construction and information technology, which rose 1.65 and 1.61 percent, respectively, over the same time.

- The Thai baht strengthened to new 52-week highs on Friday (lows on the chart below).

- Export orders in Taiwan came in stronger than expected. February’s year-over-year orders came in up 22 percent, well ahead of expectations for a 16.1 percent print and up from January’s 5.2 percent print.

Weaknesses

- Materials was the worst-performing sector of the HSCI for the week, falling nearly 3 percent.

- The weakest stock in the HSCI over the last week was China Huishan Dairy Holdings (6863 HK), the shares of which suddenly plummeted more than 85 percent on Friday. Noted short-seller Carson Block, who expressed surprise at the sudden drop, according to Bloomberg News, and his firm Muddy Waters had alleged last year that Huishan overstated spending and made undisclosed and questionable transfers and transactions.

- The Philippines Composite Index declined 1.03 percent for the week.

Opportunities

- Geely Automobile Holdings (175 HK), which came in with better-than-expected net income and raised its sales volume target for 2017 this week, also announced that it will be rolling out an all-electric rendition of London’s classic black taxi cab. Geely subsidiary London Taxi Co. has invested more than 300 million pounds in a new technology park from which as many as 20,000 vehicles could be produced each year. Bloomberg News reports that Carl-Peter Forster, the chairman of London Taxi Co., explained that, “The opening of our new plant sets a number of new records… the first brand new automotive manufacturing facility in Britain for over a decade, the first dedicated electric vehicle factory in the U.K., and the first major Chinese investment in U.K. automotive.” (The new factory is powered by solar panels to boot.)

- China Southern Airlines (1055 HK) is reportedly in advanced talks to sell a major stake of the company to American Airlines, says Bloomberg News, and is planning for major strategic cooperation. China Southern is Asia’s largest carrier by number of passengers.

- Next week we will begin to get the month’s PMI numbers from a number of Asian nations.

Threats

- This weekend the elite Hong Kong-ers of the Election Committee go to the polls to “elect” a new chief executive for the city. Carrie Lam, Beijing’s favored choice and thus the expected winner, is decidedly less popular than ex-Financial Secretary John Tsang, according to a recent South China Morning Post/Chinese University of Hong Kong survey. The survey’s results indicated Tsang had 46.6 percent support to Lam’s 28.2 percent. The public, however, have no direct say in the matter, as only the roughly 1,200 members of the Election Committee will cast ballots. Beijing’s role in affairs has led some to discuss the Sunday vote as a “selection” rather than an “election,” and can be considered a threat, given 2014’s so-called Umbrella Revolution that sought more autonomy and democracy in Hong Kong’s governance.

- Replacing the now-defunct Trans-Pacific Partnership may take longer than anticipated by some member countries, although Singapore and Vietnam announced in a joint statement this week that the two nations will continue to work together to find a way forward on trade.

- President Tsai Ing-wen announced that Taiwan will develop its own submarine program to counter China’s. Taiwan recently announced a 50 percent increase in its military spending, from 2 percent to 3 percent of GDP.

Strengths

- Russia was the best performing country this week, gaining 14 basis points. The central bank lowered its key rate by 25 basis points.

- The Polish zloty was the best performing currency this week, gaining 1.19 percent against the dollar. The central bank of Poland indicated a possible rate hike later this year, which should be supportive for the currency.

- The telecommunication service sector was the best performing sector among eastern European markets this week.

Weaknesses

- Poland was the worst performing country this week, losing 2.27 percent. LPP S.A. company, which designs and distributes clothing in Central and Eastern Europe, declined 7.5 percent, and PZU, the country’s biggest insurer, lost almost 5 percent after the CEO was fired without explanation.

- The Russian ruble was the worst relative performing currency this week, gaining 31 basis points against the dollar. Russian currency is highly correlated with the price of oil which declined 1.41 percent in the past five days.

- The health care sector was the worst performing sector among eastern European markets this week.

Opportunities

- Russian President Vladimir Putin told Bank of Russia Governor Elvira Nabiullina he plans to nominate her for a new five-year term. Putin appointed her to the central bank post in July 2013. A year later, the European Union (EU) and U.S. imposed sanctions on Russia over the Ukraine crisis and oil was plunging. Nabiullina first tried to stabilize the falling ruble, but later let the currency float freely, triggering a nearly 50 percent drop against the dollar. But the markets stabilized and the weak ruble helped ease the economic impact of crude’s collapse. Inflation is near a record low today. If she is re-elected in June, she could contribute to stabilize economy further.

- Eurozone Purchasing Managers’ Indices (PMIs) are at the highest level in six years, and well above the key 50 level. The Eurozone Manufacturing PMI jumped to 56.7 versus 56 for the prior month. The Services PMI rose to 56.5 versus 55.5 prior.

- Barclays equity strategists see euro-area equities as the most attractive risk-reward value in the near term. Earnings growth finally is starting to pick up, relative valuations are very low, and European inflation and interest rates are rising. Barclays increased its overweight in Europe excluding U.K. equities, and is moderately underweighting the U.K. as Article 50 is set to be triggered.

Threats

- According to Polish government officials, Poland may deliver its first increase in interest rates since 2012 this year. Faster price growth is set to help the economy’s expansion, paving the way for monetary tightening. Gross domestic product will expand an estimated 3.5 percent in 2017, after a gain of 2.7 percent last year. Inflation is picking up, but still remains below the central bank’s target of 2.5 percent.

- Sixty years ago the Treaty of Rome was signed, and as the EU celebrates the signing of the international agreement that created the European Economic Community (EEC), Therese May is preparing to trigger Article 50. On March 29, she will formally announce that the U.K. is leaving the bloc and negotiations will begin. After 60 years, this is the first time an EU member is leaving the union. There is much uncertainty surrounding U.K.’s exit process as it has never been done before.

- A former Russian lawmaker who fled Moscow for Ukraine and was critical of President Putin was shot dead in Kiev. Denis Voronenkov left Russia in 2016 to settle in Ukraine, and he was testifying against ex-Ukrainian President Viktor Yanukovych, who was toppled in deadly protests three years ago and now lives in Russia. Larysa Sargan, spokeswoman for Ukraine’s Prosecutor General, said that “it was a demonstrative execution of a witness”.

© US Global Funds

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits