Can Trump Dig Coal out of Its Slump?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsFlanked by coal workers, President Donald Trump signed the American Energy Independence Executive Order this week, directing the Environmental Protection Agency (EPA) to review the Clean Power Plan, former President Barack Obama’s signature environmental policy. Unveiled in August 2015, the plan is intended to reduce carbon dioxide emitted from U.S. power plants 32 percent by 2030. Because Trump cannot directly overrule this particular regulation, the EPA must come to a finding on whether it needs to be modified or repealed.

Shares of American coal mining companies jumped in response Tuesday. Kentucky-based Ramaco Resources closed up more than 13 percent, with impressive gains also made by Cloud Peak Energy and Peabody Energy

As expected, the executive order prompted criticism from environmentalist groups and acclaim from business leaders and workers in the energy sector. Among the media outlets that heaped praise on Trump was the Wall Street Journal’s editorial board, which wrote that the president “deserves credit for ending punitive policies that harmed the economy for no improvement in global CO2 emission or temperatures.”

I believe the editors make a valid point that Obama’s plan accomplished too little at too great expense. However, there are two points on which I might disagree with others

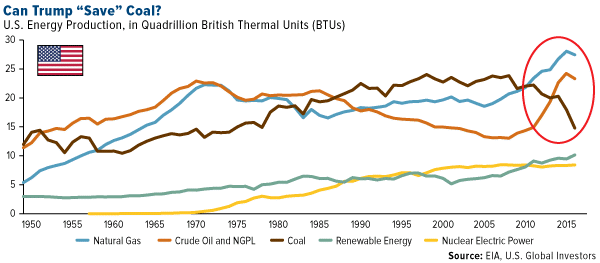

One, part of Trump’s goal here is to make America energy-independent, as the order’s name implies. Free of burdensome regulations, it’s believed, U.S. energy can be unleased, and we can become a net-exporting nation. The truth is that the U.S. has never been so energy-independent as it is now, even in the face of strict Obama-era rules and regulations. In January, the Energy Information Administration (EIA) forecasted that, even with the Clean Power Plan in place, the country would be a net energy exporter by 2026. Trump’s executive order is unlikely to move that target significantly. And remember, thanks to fracking and the recent lifting of a 40-year ban on oil exports, the U.S. is now a net petroleum exporter.

Two, Trump’s efforts are seen as benefiting the coal industry the most, but I think there are greater forces at work than regulations, as restrictive as they’ve become.

Where Have All the Coal Jobs Gone?

To be clear, I don’t think anyone sincerely believes Trump can “save” coal or coal miners’ jobs. We can probably all agree, however, that he’s at least seeking a way for the coal industry to do what it can to compete with other forms of energy, including renewables and fracking. Coal might very well continue to lose share in the U.S. even after regulations are lifted. That’s fair. But it will be the free market making the choice to retire coal, not government officials.

It’s important to recognize that coal faces several challenges that deregulation won’t be able to block. For one, the fracking boom flooded the market with cheap natural gas, compelling many U.S. power plants to make the switch from coal to gas. Thanks to fracking, gas and oil production now outpaces coal production. By 2040, natural gas will account for 40 percent of U.S. energy production, and renewables will have a larger share than coal, according to EIA estimates.

click to enlarge

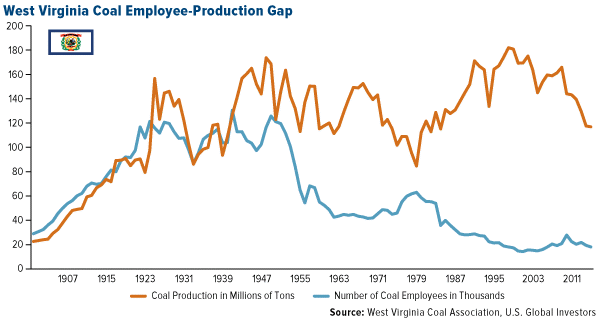

Take a look at the 114-year history of the coal industry in West Virginia, the second-largest U.S. coal producer after Wyoming. Since shortly after World War II, the number of coal mining jobs has steadily decreased. In 2014, the state industry employed a little over 18,000 people, a far cry from the 125,000 it employed in 1948.

click to enlarge

Interestingly, though, annual production levels since 1948 have remained within a 100-million-ton range. This suggests that, like fracking, better and more efficient mining tools and methods have offset the need for so many workers. More is done with less. It’s safe to say we can’t wholly blame regulations for the decline in coal jobs.

Growing Demand in Renewables

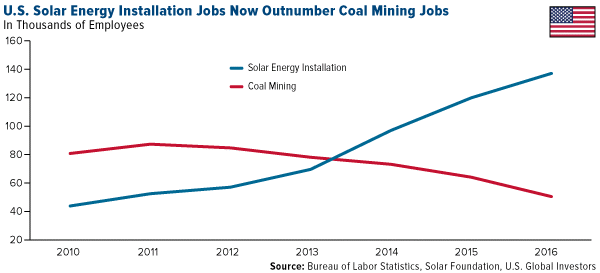

Also working against coal is the rising demand in renewable energy, specifically solar. This is reflected in the growing number of jobs in solar energy installation, to say nothing of solar manufacturing, project development, and sales and distribution. In 2016, more than 137,000 people were employed in solar installation in the U.S., compared to a little over 50,000 people in coal nationwide.

click to enlarge

According to the Solar Foundation, the industry accounted for one out of every 50 new U.S. jobs in 2016, the fourth consecutive year in which solar employment grew more than 20 percent.

As I’ve written about before, the surge in solar demand is a boon for copper, necessary for the conduction of electricity, and lithium, used in lithium-ion batteries to store the energy.

Consumers More Confident Than at Any Time Since 2000

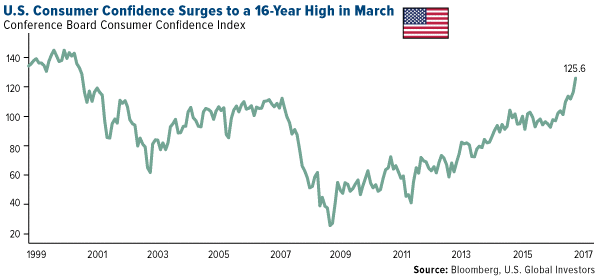

President Trump’s policies aren’t just exciting coal workers. Consumer confidence rose sharply to a 16-year high in March on an improved jobs market and the potential for robust economic growth. The Conference Board’s Consumer Confidence Index hit 125.6, its highest reading since January 2000 during President Bill Clinton’s final days in office.

click to enlarge

This comes as optimism among CEOs and business owners stands near all-time highs as well. In December, the month after the presidential election, the National Federation of Independent Business’ (NFIB) Small Business Optimism Index soared to 105.8, up from 98.4 in November, a 12-year high. Since then, the index has held above 105, indicating that, despite recent legislative and judiciary setbacks, Trump’s pro-growth agenda continues to excite small business owners.

Gold on the Mind

This upcoming Tuesday, I will be speaking at the European Gold Forum in Zurich, Europe’s most prestigious gold and silver investing conference.

In the meantime, I had the pleasure to sit down with Louisa Bojesen, anchor for “Street Signs” at CNBC International’s London location. We discussed gold’s relationship with negative real interest rates both in the U.S. and U.K., South African gold mining stocks and fiscal policy in the States, among other topics. Look for a link to the interview on our website soon!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.32 percent. The S&P 500 Stock Index rose 0.80 percent, while the Nasdaq Composite climbed 1.42 percent. The Russell 2000 small capitalization index gained 2.31 percent this week.

- The Hang Seng Composite lost 1.20 percent this week; while Taiwan was down 0.92 percent and the KOSPI fell 0.40 percent.

- The 10-year Treasury bond yield fell 3 basis points to 2.39 percent.

Domestic Equity Market

click to enlarge

Strengths

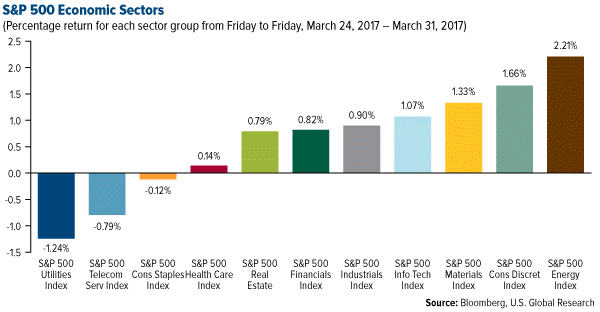

- Energy was the best performing sector of the week, increasing by 2.21 percent versus an overall increase of 0.92 percent for the S&P 500.

- Vertex Pharmaceuticals was the best performing stock for the week, increasing 21.53 percent.

- RH, formally known as Restoration Hardware, spiked on guidance. The high-end furniture retailer said it expects first-quarter net revenue of $530 million to $545 million, well ahead of $485.1 million that Wall Street was expecting. Earnings and revenue were both in line with the consensus.

Weaknesses

- Utilities was the worst performing sector for the week, falling 1.24 percent versus an overall increase of 0.92 percent for the S&P 500.

- Akamai Technologies was the worst performing stock for the week, falling 6.18 percent.

- Toshiba's nuclear unit, Westinghouse, filed for Chapter 11 bankruptcy on Wednesday as liabilities totaled $9.8 billion as of December, Reuters says.

Opportunities

- Facebook's stock price is up again this week after announcing features that mimic those of Snapchat. In another piece of good news, Barclays has named Facebook the "best pure play in consumer Internet around the secular growth in mobile advertising, full stop." Analyst Ross Sandler and his team released a note on Facebook March 29 with an "Overweight" rating and a $154 price target, implying a potential 9.5 percent increase. Sandler thinks that the next 3-5 years will be the "golden age" of mobile, with the rapid transition of all things moving from desktops and laptops to mobile devices.

- BlackRock announced a big shake-up. The asset manager is cutting dozens of jobs and reducing some fees by up to 21 percent as it looks to reorganize its stock-picking unit, Bloomberg says. Over the next 18 months, BlackRock plans to hire about the same number of employees that were let go, shifting its focus to emerging markets.

- David Einhorn's hedge fund Greenlight Capital Inc. urged General Motors Co. to split its common stock into two classes, a proposal that was swiftly rejected by the carmaker. The company's shares jumped 3.9 percent to $35.96 on Tuesday. Greenlight Capital said the move would help the carmaker improve its financial flexibility and boost the stock's value. GM rejected the plans, saying they are not in the best interests of shareholders.

Threats

- Chipotle has dominated the growth of fast-casual Mexican dining in America. According to UBS analysts, its biggest competition is from Panera Bread, the fast-casual chain that serves up sandwiches, soups and salads. Panera is outside Chipotle's cuisine niche, but it is competing with its rivals by using fresh, additive-free ingredients. More important, consumers who are looking for alternatives to Chipotle — perhaps because of lingering concerns from the 2015 E. coli saga — are likely to find a Panera nearby.

- Lululemon collapsed after earnings. Shares of Lululemon fell by as much as 16 percent in after-hours trade on Wednesday after the company said it expected sales at stores open for at least one year to decline in the first quarter in the "low-single digits" on a constant dollar basis.

- Darden Restaurants, the owner of popular chains such as Olive Garden and Longhorn Steakhouse, announced on Monday that it is buying Texas-based restaurant chain Cheddar's Scratch Kitchen for $780 million. In a note sent out to clients on Tuesday, a team of Morgan Stanley analysts said that the deal is bad news for small cap restaurants looking for a buyout. "The acquisition of a privately held brand is probably a modest negative for other small cap public casual diners, as they are now effectively ruled out as DRI targets in the short-term."

The Economy and Bond Market

Strengths

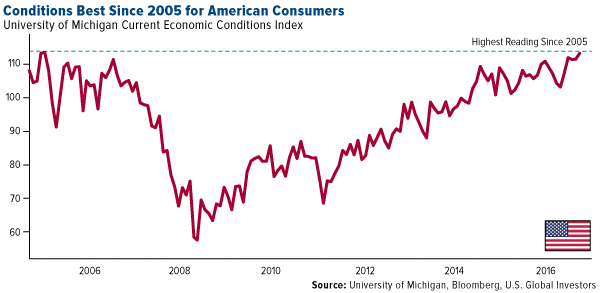

- Consumer sentiment rose in March as Americans registered sunnier views about the state of their finances. The University of Michigan current conditions gauge increased to 113.2 from 111.5 the prior month, an 11 year high.

click to enlarge

- Pending home sales jumped 5.5 percent in February, the most since April 2010, according to the National Association of Realtors. Some prospective homebuyers are speeding up the process in anticipation of higher interest rates.

- Global trade is growing at its fastest pace in 7 years. Global trade in goods increased 2.4 percent in volume terms during the three months that ended in January, making for the fastest growth since August 2010, the Financial Times reports, citing figures from the CPB Netherlands Bureau for Economic Policy Analysis.

Weaknesses

- Eurozone inflation slows down. Consumer prices in the eurozone rose 1.5 percent in March, down from 2.0 percent in February, data released Friday by Eurostat showed. The reading marked the first time consumer price growth in the eurozone had slowed since April 2016.

- Personal spending for February came in at 0.1 percent, below the forecast 0.2 percent.

- Initial jobless claims for the past week were 258,000, higher than the expected 247,000.

Opportunities

- Following the health care debacle, Trump is planning to move up the timetable on large-scale infrastructure spending to this year, reported Jonathan Swan at the news website Axios.

- China's economy is picking up. Data released by the National Bureau of Statistics on Friday showed that the Chinese government’s official manufacturing Purchasing Managers' Index rose to 51.8 in March, its highest level since April 2012. PMIs tend to be a leading indicator of economic activity.

- The European Union (EU) published its plan for Brexit talks. The EU says discussions will take place in three phases: 1) The settlement of key questions regarding Britain's exit; 2) Talks about future trade deals; and 3) Negotiations for a possible transitional agreement.

Threats

- Business Insider reports that although we have a Republican president backed by a Republican majority in Congress, tax reform is not simple. The 'Trumpcare' debate showed there is little unity within the governing party itself. Also, the proposed tax policies are not simple. "Certainly tax reform, both at the individual and corporate levels, is every bit as complicated as health care,” said Mark Hamrick, senior economic analyst at Bankrate.com. "The looming unpopular issue of the border adjustment tax is just one of the complicated policy wild cards. History reminds us that it has been decades since significant tax reform has passed in Washington because it is not easy.”

- The commercial real estate market is showing cracks and will peak this year, Morgan Stanley analysts forecast. The big risk for the market is that the growth of net operating income could slow down, they said. Commercial real-estate prices have recovered above the peaks they set before the housing crisis a decade ago. However, the revenue generated by rents face two growing challenges. "To keep CRE prices afloat, NOI growth needs to accelerate to overcome dual headwinds of rising rates and tighter lending standards," Morgan Stanley wrote. "However, the reality is that it is decelerating, which is different than prior rate hike cycles. We therefore believe valuations can decline even without a recession, which was a necessary condition for the past two declines in CRE prices in the early 1990s and 2008."

- According to Raoul Pal, a former hedge fund manager who retired at the age of 36 and is now CEO and cofounder of RealVision, "The market narrative is reflation. Trump. Amazing. However, the actual stuff is that everything is going to weaken dramatically, and I think the Atlanta Fed is starting to capture this." The latest GDPNow reading from the Atlanta Fed released on March 24 shows real gross domestic product is tracking at just 1 percent for the current quarter, well below the 3 percent target that has been touted by the Trump administration. "Now this is going to catch the markets offside," Pal said. "The speculative positioning in bonds up until about a week and a half ago, two weeks ago, was the largest ever short position in the history of the bond markets."

Gold Market

This week spot gold closed at $1,243.45, up $4.80 per ounce, or 0.39 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.80 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index rose 1.51 percent. The U.S. Trade-Weighted Dollar Index finished the week higher by 0.90 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Mar-27 |

H.K. Exports YoY |

15.7% |

18.2% |

-1.2% |

|

Mar-28 |

U.S. Conf. Board Consumer Confidence |

114.0 |

125.6 |

116.1 |

|

Mar-30 |

Germany CPI YoY |

1.8% |

1.6% |

2.2% |

|

Mar-30 |

U.S. GDP Annualized QoQ |

2.0% |

2.1% |

1.9% |

|

Mar-30 |

U.S. Initial Jobless Claims |

247k |

258k |

261K |

|

Mar-31 |

Eurozone CPI Core YoY |

0.8% |

0.7% |

0.9% |

|

Apr-2 |

Caxin China PMI Mfg |

51.7 |

-- |

51.7 |

|

Apr-3 |

U.S. ISM Manufacturing |

57.0 |

-- |

57.7 |

|

Apr-4 |

U.S. Durable Goods Orders |

-- |

-- |

1.7% |

|

Apr-5 |

U.S. ADP Employment Change |

180k |

-- |

298k |

|

Apr-6 |

U.S. Initial Jobless Claims |

245k |

-- |

258K |

|

Apr-7 |

U.S. Change in Nonfarm Payrolls |

174k |

-- |

235k |

Strengths

- The best performing precious metal for the week was silver, up 2.61 percent, as investors keep pushing money into commodities in search of investments that keep up with faster inflation. Gold rose nearly 9 percent this quarter, its best performance in a year. Gold has risen on the perceived inability of President Donald Trump to advance his economic agenda after the failed health care reform plan. Traders and analysts are divided on the outlook for gold, given the uncertainty around interest rates.

- Japan’s continuing sales of U.S. debt highlight the uncertainty around fiscal and monetary policies in the U.S., making way for gold to shine. Japan holds $1.1 trillion of U.S. Treasuries, making it the largest holder of U.S. debt, surpassing China. Japanese were net sellers for three months straight through January, the longest stretch since 2013.

- Bloomberg Intelligence published a note saying that precious metals may have the most favorable reward versus risk as they appear to have bottomed following a multiyear slump. In past rate hiking cycles metals have been among the top performers.

Weaknesses

- The worst performing precious metal for the week was almost a tie between platinum and palladium, down 1.41 percent and 1.44 percent, respectively. The rand fell precipitously earlier in the week as South African president Jacob Zuma fired another cabinet member, this time finance minister Pravin Gordhan. With the fall in the rand, this reduces the costs of the South African producers to produce these metals, thus there is some worry output will increase. The country’s chamber of mines commented that this decision is “bizarre and difficult to understand.” The statement went on to say that, “The mining industry believes the changes will lead to instability and reduce investor confidence.”

- More interest rate hikes may be on the way. Boston Fed president Eric Rosengren argued that four rate increases may be needed this year, and San Francisco’s John Williams said he “would not rule out more than three increases total for this year.” Rosengren warned that the faster rate increases may be needed to balance unemployment and inflation targets.

- Gold reserves are declining in North America. TD Securities published a brief stating that reserves declined for five straight years through 2016, and large cap total reserve life is at a 10-year low. Meanwhile, a huge deposit has been reported discovered in China’s Shandong province, with reserves estimated between 382 tons and 550 tons.

Opportunities

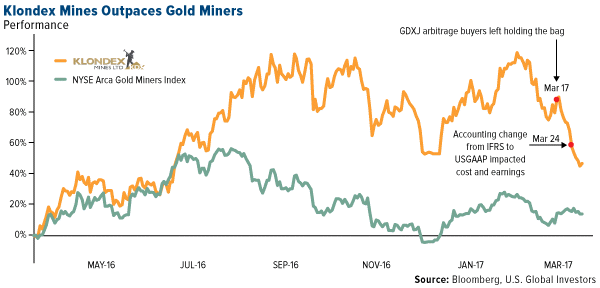

- Klondex Mines (KDX CN, KLDX US) on a trailing year basis is still up 47 percent relative to the NYSE Arca Gold Miners Index which is up almost 16 percent after two events that have transpired over the past two weeks. On March 17, the Market Vectors Junior Gold Miners ETF (GDXJ) was anticipated to sell roughly three of its largest holdings as they no longer met the criteria for the benchmark index. The proceeds generated from the expected sales were thought to be redeployed into most of the existing holdings, meaning potentially 11.5 million shares of new demand for Klondex by the GDXJ ETF. This led many index arbitragers to start accumulating shares in Klondex in anticipation they could sell the shares at a higher price into the index rebalance. However, when the index rebalance date arrived on March 17, the managers of the GDXJ ETF did not sell their largest names as expected, thus the arbitragers were left with no easy money exit from their accumulated positions. This weighed on Klondex’s share price performance as the arbitrage buyers chose to exit their positions to move on to other trades. Over the last couple of years, the share registry of U.S. holders of Klondex Mines has grown significantly, thus requiring the company to transition from IFRS accounting to U.S. GAAP reporting. Therefore, on March 24, when Klondex reported earnings for yearend 2016, analyst estimates were based on IFRS rules but the earning reported by Klondex were based on GAAP which requires more costs to be expensed. Klondex Mines has been making capital improvements to rehabilitate the True North Mine purchased out of receivership last year, but because there are no proven and probable reserves associated with the asset yet, all the capital invested in bringing the operation up to production readiness had to be expensed. In summary, Klondex has had its share price driven down by an index rebalance that did not happen and an earnings miss from a change in accounting standards, that was exacerbated by trading algorithms that immediately started selling the stock. This unusual set of events may provide investors an exceptional opportunity to establish positions in a high quality set of assets operated by strong team of operators.

click to enlarge

- Rye Patch Gold (RPM CN) received regulatory approval to start irrigation on the new South Heap Leach Pad at Florida Canyon. The project’s first gold production may come as early as April this year. Macquarie Research published positive outlook on Rye Patch Gold, putting its price target up 132 percent. President and CEO William Howald said, "It's with a great sense of accomplishment and pride that the Florida Canyon team has completed the re-start of the mine. This accomplishment launches Rye Patch as a tenacious Au producer with a bright future with its pipeline of existing resource assets and exploration upside along the Oreana trend."

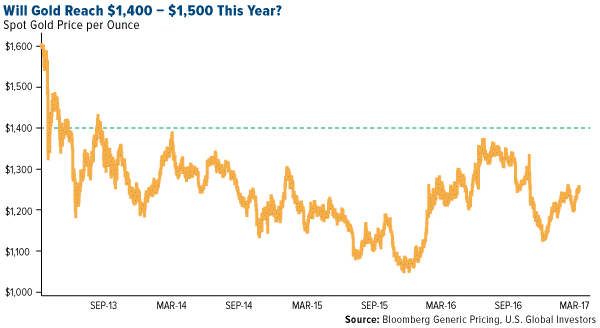

- Gold price forecasts are looking up as anticipation over Trump’s tax cuts wane and investors confront continued negative real interest rates. Jeffrey Christian of CPM Group sees the price rising to $1,300 per ounce, Metals Focus Ltd. argues the case for $1,400 gold, and Incrementum AG anticipates $1,500 prices.

click to enlarge

Threats

- Uncertainty lingers over potential Federal Reserve appointments during the Trump administration. Two spots on the Board of Governors have been unoccupied for nearly three years. A third spot will open up when Governor Daniel Tarullo steps down. Among the chairs, Janet Yellen’s term will end in 2018, as will vice chair Stanley Fischer’s. It remains to be seen who Trump could tap for these positions and what political agenda they might have.

- Lawmakers in El Salvador dealt a blow to the metals mining industry when they voted earlier this week to enact a nationwide ban on metal mining. The law does not apply to other mining activity, such as coal or salt.

- Residents of the Cajamarca municipality in Colombia voted against allowing mining activity in their area. The popular, regional vote may lead to a trend of additional popular efforts to restrict mining projects within Colombia. The vote is a blow to AngloGold Ashanti’s La Colosa gold project, located in the region.

Energy and Natural Resources Market

Strengths

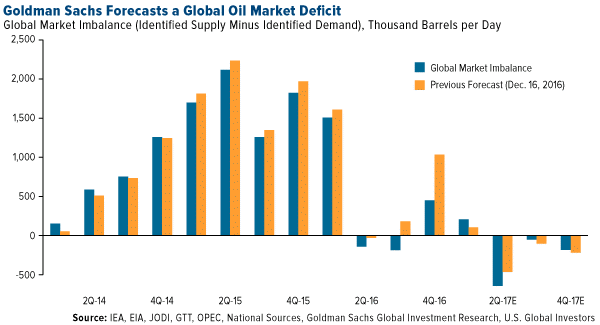

- Crude oil prices rose 5.7 percent this week on the back of renewed faith that output cuts and strong demand are ending oversupply. According to a research note released by Goldman Sachs this week, global market imbalances will continue to support a deficit in the global oil market throughout 2017. As we have mentioned in a previous piece, despite disappointing U.S. inventory releases, inventory draws across the globe, most notably in Asian regions, continue to be supportive of higher oil prices. This is positive for oil prices.

click to enlarge

- The best performing sector for the week was the S&P Super Composite Oil and Gas Exploration and Production Sub Index. The index rose 5.8 percent related to rising oil prices and rising gasoline demand in the U.S.

- ConocoPhillips Co, a multinational energy corporation based in Houston, Texas, was the best performing stock this week, finishing up 13 percent. The stock rose following a gigantic acquisition from Cenovus who pledged to purchase the company’s Canadian assets for a massive 17.7 billion dollars.

Weaknesses

- Iron ore was the worst performing commodity this week, dropping 3.4 percent. According to Reuters, China’s ports are bursting with record stockpiles of the mineral where they are going so far as to demolish abandoned buildings in attempts to create more space. The estimated inventory count is roughly 132 million tonnes at 46 Chinese ports and 40 million tonnes in overstock at steel mills, enough iron ore to build 13,000 Eiffel Towers. This is negative for the industrial commodity.

- The worst performing sector this week was the BI Global Coal Producers Top Competitive Peers. The index fell 2.5 percent on the back of power plant owners turning to natural gas in spite of President Trumps promise to put coal miners back to work.

- The worst performing stock for the week was Goldcorp Inc., one of the world’s largest gold mining companies. The company fell 8 percent on the back of falling gold prices.

Opportunities

- Jean-Sebastian Jacques, Head of Rio Tinto, is unfazed by concerns surrounding weakness in China’s economy according to the Financial Times this week. The leader of the mining giant stated that restructuring of the country’s state-owned enterprises will lead to demand for iron ore produced from Australia despite what the battered price action of iron ore currently suggests. He further supported his claim by highlighting that China’s crackdown on polluting steel furnaces will be a positive factor for the commodities demand through 2017. A positive read-through for iron ore from one of the world largest mining companies.

- U.S. GDP came in higher than expectations at 2.1 percent versus expectations of 1.8 percent according to data released by Bloomberg this week. Contributing to much of this increase came from a substantial lift in consumer spending which rose to 3.5 percent from 3 percent in the second quarter of 2016. In addition, private inventory, residential, and business investment all increased, which contributed to the percentage gains. This bodes well for raw materials.

- Private equity funds are getting ready to deploy cash reserves that have been on the sidelines in the last two years, according to oilprice.com. As oil has passed the $50 a barrel range, oil specialist private equity funds like Argus, a group of three energy-focused firms, are planning to invest over 4 billion dollars in the next three years on the back of relatively cheap assets and companies. Interval Capital expects the U.S. oil industry to boom by 2020.

Threats

- Protectionist rhetoric casts shadows over agricultural markets according to the Financial Times this week. The Financial Times Global Summit for Commodities was held this week in Lausanne, Switzerland, where key members from agricultural trading houses gathered to discuss the bleak state affairs pertaining to their operations. Carl Casale, head of CHS, a leading U.S. grain cooperative, highlighted that farm earnings are projected to fall for the fourth consecutive year coupled with a strong greenback; there is not a lot of resilience in the system to absorb trade disruptions.

- The spectacular rally in copper has come into question this week as momentum has slowed down according to Reuters. The strike at the world’s copper largest mine, Escondida in Chile, officially came to an end this week as union workers finally arrived at a deal. During the time the mine was out of production, roughly 230,000-240,000 tons of productions were lost which helped tighten supply in the short-term. However, as missed production comes back online, this gap will likely close suggesting prices may have run up too far too fast.

- For the 11th week in a row, the number of U.S. oil rigs has continued to increase. The rig count is up 10 to 662, the highest rig count since September of 2015 according to Zero Hedge. As the U.S. works through overstocked inventories, a rising rig count will only bring more supply online, prolonging the time needed to work through current over supply.

China Region

Strengths

- China’s official Manufacturing PMI came in at 51.8, just ahead of expectations of 51.7 and up from 51.6 in February. This marks the official metric’s highest reading in nearly five years.

- South Korea’s final GDP for the fourth quarter rose 0.5 percent quarter-over-quarter, beating expectations of 0.4 percent. Korea’s year-over-year reading also beat with a 2.4 percent actual growth rate versus an expected 2.3 percent.

- Singapore’s Straits Times Total Return Index gained 97 basis points for the week.

Weaknesses

- Vietnam’s first-quarter GDP came in light at 5.10 percent, shy of analysts’ expectations of 6.25 print and down from 2016’s fourth-quarter showing of 6.21 percent.

- China’s Shanghai Composite Index fell 1.8 percent for the week.

- The worst performer in the Hang Seng Composite Index for the week was mobile application software company Meitu, which fell 21.42 percent.

Opportunities

- Next week and this weekend we’ll get PMI data for a number of countries in the region, including China’s Caixin PMI.

- China Southern Airlines, Asia’s largest carrier by number of passengers, formally announced that American Airlines took a $200 million strategic stake in the company, which issued nearly 271 million H-shares to American.

- Korea Transportation Asset Management is said to be in talks to acquire AirAsia’s leasing unit stake, Reuters reported this week. AirAsia is near its 52-week highs.

Threats

- A week ahead of Chinese President Xi Jinping’s visit to the U.S., President Donald Trump took to Twitter noting the “difficult” conversations to be had with his Chinese counterpart. Trump signed executive orders today designed to strengthen trade enforcement and review U.S. trade deficits with all other countries.

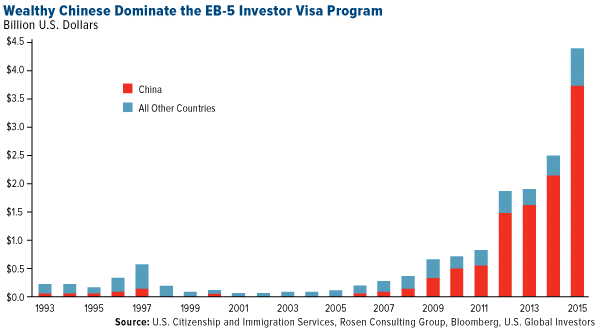

- Wealthy Chinese are scrambling to obtain a U.S. immigrant investor visa, Bloomberg reports, as members of Congress in Washington debate raising the minimum required to obtain one from $500,000 to $1.35 million. The EB-5 Immigrant Investor visa initiative channels money to high-profile U.S. real estate projects from New York to California. As you can see in the chart below, China’s wealthy continue to be the largest participants in the EB-5 program.

click to enlarge

- As expected, Carrie Lam won Hong Kong’s “election” this week for the role of Chief Executive, but she did so without wide popular support. Her public polling numbers remained well behind that of her top competitor, though she was favored by Beijing.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 4.8 percent. Banks rallied on the back of increasing hopes for an agreement between Greece and its lenders. Next Eurogroup meeting will take place on April 7.

- The Russian ruble was the best performing currency this week, gaining 1.3 percent against the dollar. The Bank of Russia revised up fourth quarter current account surplus to $10.1 billion from $7.8 billion previously. The Russian economy returned to growth at the end of 2016, when gross domestic product gained 0.3 percent from a year earlier in the fourth quarter after a decline of 0.4 percent in the previous three months.

- The health care services sector was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 2.2 percent. Despite good economic growth data, political noise weighed on the Moscow stock exchange. Mike Flynn, the former national security advisor to Donald Trump, asked for immunity from prosecution in return for being interviewed for the probe into the Trump’s campaign’s alleged contacts with Russia. He “has a story to tell and very much wants to tell it,” Flynn’s lawyer said.

- The Czech kurona was the worst relative performing currency this week, losing 1.3 percent against the dollar. The central bank of Czech Republic is preparing to remove a cap on the currency. The market reaction will be far from a repeat of the Swiss franc’s surge in January 2015, according to the chief investment officer on North Asset Management. Investors flooding into the koruna may struggle to close their trades in an economy a quarter of the size of Switzerland’s, he said.

- The real estate sector was the worst performing sector among eastern European markets this week.

Opportunities

- March PMI data will be released next week, and expectation is that once again we will see readings well above the 50 level that separate growth from contraction. In February, Hungary recorded the highest PMI of 59.5, Czech Republic 57.6, Poland 54.2, and Russia 52.

- Raffaella Tenconi from Wood & Company expects the Central Bank of Europe to extend its quantitative easing program until December 2018, which is favorable on the margins for both bonds and stocks. The conditions for ending the quantitative easing program are not in place yet, mostly because of the fragile economic and political situation in Italy, as well as the still significant slack in the labor market in the euro area.

- Easing continues in Hungary, as the central bank lowered its cap on benchmark deposits more than economists expected and has left the benchmark unchanged at a record low 0.9 percent for a tenth month. The cap on deposits, which limits the funds commercial banks can place in the central bank facility, has boosted liquidity in the economy, pushing interbank rates to a record low 0.21 percent. Hungary was able to sell bonds at negative yields for the first time last week.

Threats

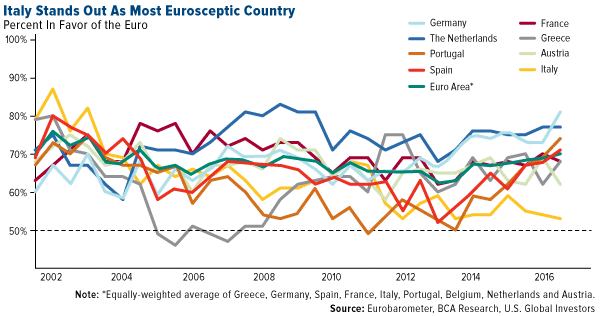

- Marko Papic, Senior Vice President at Bank Credit Analyst, predicts that the largest threat to the eurozone’s stability is Italy. Euroscepticism is the strongest in Italy. The chart below shows the percentage of people in favor of the euro, and you can see that acceptance of the euro is clearly visible among several European countries but less supported in Italy.

click to enlarge

- The U.K. on Wednesday formally began the process of exiting the European Union. Managing Britain’s exit will be a major political test for Prime Minister Theresa May, who has only a small majority in Parliament. The negotiations will also test the unity of the remaining 27 nations in the European Union.

- Deutsche Bank has been bullish on the ruble since a year ago, but last month turned neutral and recommended taking profits. Now Deutsche Bank’s currency research team is shifting from neutral to a tactically bearish view on the Russian currency. While the fundamental outlook for the ruble over the medium term is robust, recent ruble appreciation and resilience in the face of crude weakness has been excessive.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| DJIA | 20,663.22 | +66.50 | +0.32% |

| S&P 500 | 2,362.72 | +18.74 | +0.80% |

| S&P Energy | 514.01 | +11.09 | +2.21% |

| S&P Basic Materials | 328.73 | +4.33 | +1.33% |

| Nasdaq | 5,911.74 | +83.00 | +1.42% |

| Russell 2000 | 1,385.92 | +31.28 | +2.31% |

| Hang Seng Composite Index | 3,310.11 | -40.37 | -1.20% |

| Korean KOSPI Index | 2,160.23 | -8.72 | -0.40% |

| S&P/TSX Global Gold Index | 207.45 | -3.69 | -1.75% |

| XAU | 83.77 | -0.22 | -0.26% |

| Gold Futures | 1,251.20 | -0.50 | -0.04% |

| Oil Futures | 50.76 | +2.79 | +5.82% |

| Natural Gas Futures | 3.19 | +0.11 | +3.64% |

| SS&P/TSX Venture Index | 815.77 | +12.17 | +1.51% |

| 10-Yr Treasury Bond | 2.39 | -0.02 | -1.04% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| DJIA | 20,663.22 | -452.33 | -2.14% |

| S&P 500 | 2,362.72 | -33.24 | -1.39% |

| S&P Energy | 514.01 | -16.39 | -3.09% |

| S&P Basic Materials | 328.73 | -5.38 | -1.61% |

| Nasdaq | 5,911.74 | +7.71 | +0.13% |

| Russell 2000 | 1,385.92 | -27.71 | -1.96% |

| Hang Seng Composite Index | 3,310.11 | +56.43 | +1.73% |

| Korean KOSPI Index | 2,160.23 | +68.59 | +3.28% |

| S&P/TSX Global Gold Index | 207.45 | -3.16 | -1.50% |

| XAU | 83.77 | -1.26 | -1.48% |

| Gold Futures | 1,251.20 | -2.10 | -0.17% |

| Oil Futures | 50.76 | -3.07 | -5.70% |

| Natural Gas Futures | 3.19 | +0.39 | +13.90% |

| SS&P/TSX Venture Index | 815.77 | -6.29 | -0.77% |

| 10-Yr Treasury Bond | 2.39 | -0.07 | -2.69% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| DJIA | 20,663.22 | +900.62 | +4.56% |

| S&P 500 | 2,362.72 | +123.89 | +5.53% |

| S&P Energy | 514.01 | -40.49 | -7.30% |

| S&P Basic Materials | 328.73 | +16.57 | +5.31% |

| Nasdaq | 5,911.74 | +528.62 | +9.82% |

| Russell 2000 | 1,385.92 | +28.79 | +2.12% |

| Hang Seng Composite Index | 3,310.11 | +315.50 | +10.54% |

| Korean KOSPI Index | 2,160.23 | +133.77 | +6.60% |

| S&P/TSX Global Gold Index | 207.45 | +13.20 | +6.80% |

| XAU | 83.77 | +4.91 | +6.23% |

| Gold Futures | 1,251.20 | +94.10 | +8.13% |

| Oil Futures | 50.76 | -2.96 | -5.51% |

| Natural Gas Futures | 3.19 | -0.54 | -14.39% |

| SS&P/TSX Venture Index | 815.77 | +53.40 | +7.00% |

| 10-Yr Treasury Bond | 2.39 | -0.06 | -2.33% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investHoldings may change daily.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of 12/31/16:

AirAsia

American Airlines

China Southern Airlines

Klondex Mines

Rye Patch Gold

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The Consumer Confidence Index (CCI) is an indicator which measures consumer confidence in the Economy.

The National Federation of Independent Business’s (NFIB) Index of business optimism is based on responses from 1221 member firms.

The University of Michigan Confidence Index is a survey of consumer confidence conducted by the University of Michigan. The report, released on the tenth of each month, gives a snapshot of whether or not consumers are willing to spend money.

The S&P 1500 Supercomposite Oil & Gas Exploration & Production Index is a capitalization-weighted index comprised of stocks whose primary function is exploring for natural gas and oil resources on land or at sea.

The Bloomberg Intelligence (BI) Global Coal Producers Top Competitive Peer Group is an equal-weighted basket of peers.

The Straits Times Index is a modified market capitalization-weighted index comprised of the most heavily weighted and active stocks traded on the Stock Exchange of Singapore.

The Shanghai Composite Index (SSE) is an index of all stocks that trade on the Shanghai Stock Exchange.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits