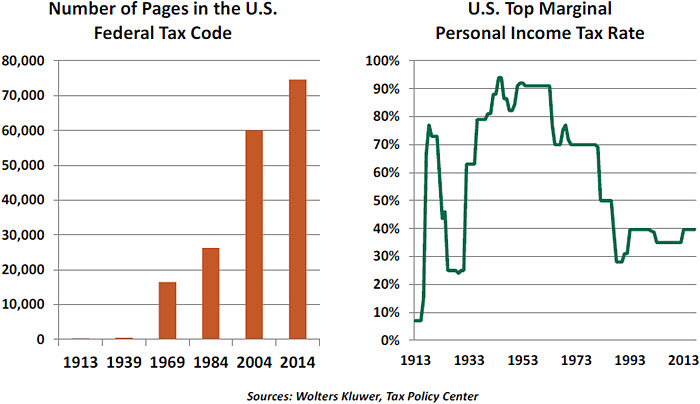

Not likely. In the 104 years since the Federal income tax was first established, the code has become much more than a revenue-generating device. It is also used to promote and discourage certain types of activity and to limit the level of economic inequality. Describing these objectives (some of which are contradictory) requires more than 70,000 pages of text.

Recipients of tax preferences appreciate them, and legislators do too. “Pork barrel” incentives curry favor with local constituents. Lobbyists earn their keep by preserving and extending the system of exceptions. Reversing this will require substantial powers of persuasion, which were not on display last week.

Eliminating tax preferences is essential to broadening the tax base, which would provide room to lower rates without sacrificing too much revenue. But the designs that have been proposed are highly unlikely to pay for themselves, and the deficit hawks in the Congress will want to be heard on this front. The border tax has been seen as a “pay-for” in the reform package, but its economics and international legality are questionable. Support for it has been waning.

75% of American companies (primarily smaller ones) ultimately pay taxes at individual rates, because they are “pass-through” entities for their owners. Unleashing entrepreneurial energy will therefore require a successful effort to reform the personal tax code. As this is looking difficult, some have suggested focusing first on the corporate income tax. This strategy would certainly be seen by some as favoring big firms at the expense of the smaller ones.

Given the advancing complexities of both the issues and the politics, the chances seem increasingly remote that substantial change will be achieved this year. And with mid-term elections on the horizon, success in 2018 is by no means assured. We continue to place very little weight on policy changes in our economic forecast, which is virtually unchanged from its standing of four months ago.

The bond markets seem to have adjusted their expectations in the wake of last week’s failure (long-term interest rates have fallen) and the currency markets have done the same (the dollar is weaker). But U.S. equity prices have held up fairly well, leading some to wonder whether a correction might be at hand.

The cherry blossom season in Washington, usually a big annual event, was curtailed this year. A mild winter invited the buds out early, but a freakish March snowstorm damaged them. The legislative season may be following that same pattern; the optimism of a Washington spring could be giving way to a big chill.

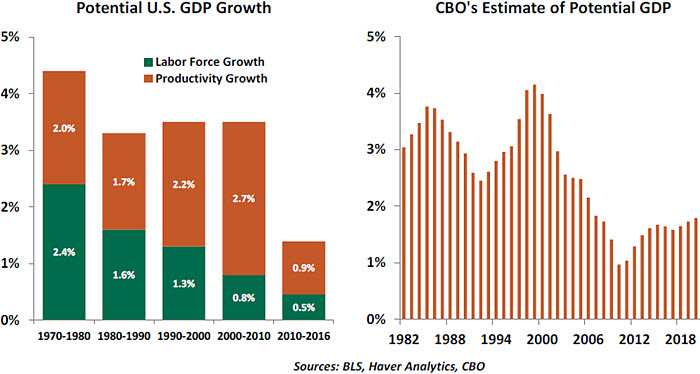

Pacing OurselvesDuring the election campaign, candidate Donald Trump promised that the U.S. would achieve 4% annual economic growth. Mr. Trump’s aides are now suggesting that this target serve as the basis for crafting the Federal budget. This would be a major miscalculation.

The administration reasons that tax reform, infrastructure spending, and reduced regulation will lift real gross domestic product (GDP) growth to twice the rate it has averaged during the current expansion. The difference between the two levels would translate into a substantial difference in the country’s standard of living and its ability to sustain debt.

Yet every country has a unique “speed limit” that bounds the pace of economic activity. This potential capacity is determined by two factors: labor force growth and productivity growth. These drivers are not static; they are shaped across time by demographic developments and investments that enhance economic efficiency.

The U.S. labor force has advanced at a weak clip in the last sixteen years, after a significantly stronger pace in the 30 years ending in 2000. The aging of the U.S. population is a major reason for this; baby boomers are presently retiring at the rate of 10,000 per day. Discouraged and disabled U.S. workers (some of whom, studies show, have been hindered by addiction to opioids) have also restricted labor force participation. Immigration can offset these limitations, but the current mood in Washington leans more toward closing borders than opening them.

Productivity growth in the current U.S. expansion pales in comparison with the experience of the 1990s and 2000s. The 1990s technology revolution was far reaching and spawned complementary effects. Business operations were transformed during this period. But since then, and especially since the 2008 crisis, productivity has been in a funk.

The reasons for this are the subject of active debate. The secular stagnation school suggests that we’ve reached natural demographic limitations that hinder demand and diminish the appetite for productive investment. Others suggest that tighter regulation has sapped business dynamism and trimmed efficiencies. Professor Robert Gordon’s research points out that educational attainment is rising slowly now compared with the past, which translates into weaker productivity growth.

Notwithstanding the incomplete understanding of the weakness in productivity growth, the fact is that efficiency gains have dwindled and are unlikely to turn around in the short term. Gains in productive capacity from the number of people working and potential increases in their output do not support 4% growth. The Congressional Budget Office’s latest projections, released this week, reflect this reality.

There are instances in history when the U.S. economy grew at a sustained pace of 3% or better. But those were different times, with different demographics and different dynamics. Expecting similar growth trends at the present stage of the business cycle is not reasonable, because the economy is already at full employment and fiscal stimulus will likely trigger inflation. The Federal Reserve would be forced to react by tightening credit, which would restrain activity.

If exaggerated productivity and GDP estimates are used as the basis for budgeting, we face the risk of a rapid escalation in national debt should economic growth fall short of expectations. To paraphrase Clint Eastwood, we’ve got to know our limitations.

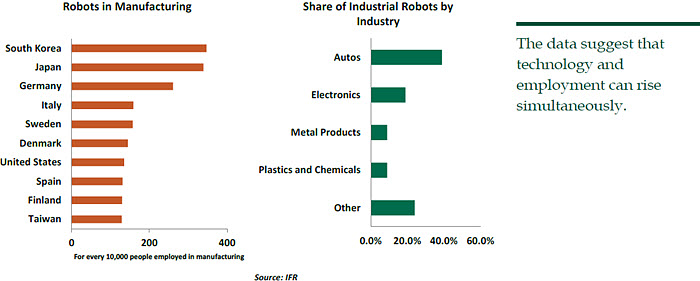

Automate ThisThe impact of technology on employment is a recurrent concern that waxes and wanes with waves of technological development. Of late, the anxiety is at a peak.

We’ve moved far beyond the application of machines in industrial applications. Computers and artificial intelligence are pervasive, and their reach will continue to expand. Driverless rigs may replace long-haul truckers, automated responders are being used to diagnose basic illnesses, and machines already direct most of the volume in the world’s financial markets. Blackrock, a global investment management company, announced this week that algorithms will replace many of its human portfolio managers.

Some studies suggest that the use of robots leads to lower employment and wages. An increase in income inequality is another outcome tied to automation. These are legitimate concerns. As the effects have spread to white collar professions, calls have risen for some kind of recompense to ease the transition for those who are displaced.

Hence the calls for taxing automation. Bill Gates, who would know a thing or two about software replacing people, has expressed support for such a measure. In theory, it would slow the pace of transition and provide funds to buffer the fates of those affected.

But history is not kind to this line of reasoning. The march of technology is somewhat inexorable, and attempts to slow it in one place would undoubtedly drive business elsewhere. Past episodes of advancing automation have been associated with

rising levels of employment on a micro and macro level. There is no reason to think that this time will be any different.

Nearly 90 years ago, John Maynard Keynes worried about technological unemployment and noted there would be 15-hour workweeks by 2030. Here we are today, still working hard even after rapid advances in technology. Robots will keep coming, and it is up to us to use these benefits they provide wisely.

northerntrust.com

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2017 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit

northerntrust.com/disclosures.

© Northern Trust

© Northern Trust

Read more commentaries by Northern Trust