SUMMARY

- Emerging Monetary Divergence

- When It Comes To Debt, How Long is Too Long?

- “Soft” Data versus “Hard” Data

Over the last decade, a combination of unprecedented global financial integration and unconventional monetary policy in global financial centers created new challenges for central banks in emerging markets (EM). Faced with the ebbs and flows of capital that followed changes in the monetary stance at the U.S. Federal Reserve, EM monetary policy makers were forced to align their stances with the U.S. to avoid violent currency moves or financial instability.

Often, this defensive posture ran counter to the needs of their domestic economies. This was acutely visible during the so-called “taper tantrum” during the summer of 2013, when Federal Reserve Chairman Ben Bernanke hinted at reductions in the Fed’s asset purchases. The remarks prompted an outflow of capital from EMs. Central banks from India to Brazil reacted by tightening monetary conditions to stem the flight of capital, despite fairly tepid domestic economic activity.

So as the Fed promises to reduce its balance sheet and deliver a total of 3-4 interest hikes this year, and speculation continues about tapering asset purchases by the European Central Bank, one might have expected EM central banks to follow suit and become more restrictive. But they haven’t—and they won’t. Times have changed.

Among major EMs, many are either expected to cut policy rates (Russia, Brazil, Chile and Colombia) or hold steady (including South Africa, India and Korea). Exceptions are Hungary, Malaysia, Turkey and Mexico, where either inflation remains high or politics are weighing on the currency.

A number of factors are driving the divergence in monetary policy between developed and developing nations.

-

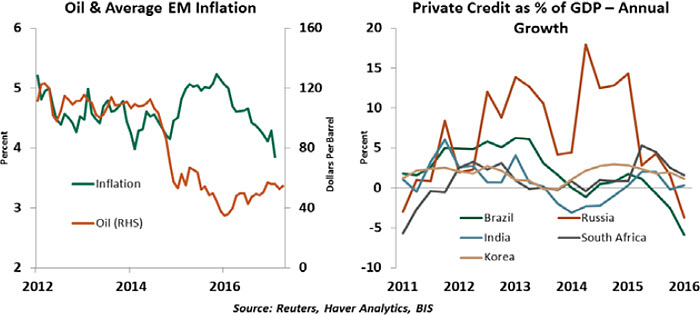

- Oil is expected to trade in a fairly narrow band of $45-$55 per barrel in the near future, comparable to its price a year ago. (During the taper tantrum era, oil was on its way up from $80 per barrel to $110 per barrel.) This keeps price pressures in check through both the direct impact on energy costs and the second order effect on core prices. More importantly, it keeps current account and fiscal balances in check in oil importing EMs, and economic activity subdued in oil exporting EMs. All of these allow central banks to keep policy accommodative or neutral.

-

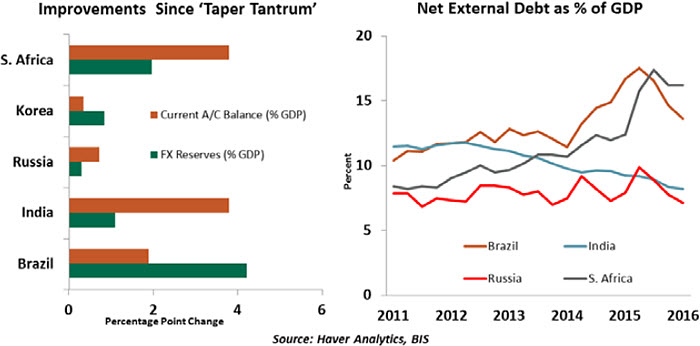

- The taper tantrum was in large part a reaction to an unanticipated shift in the Fed’s tone. It prompted the unwinding of excesses that had built up in the global financial system since the financial crisis and forced EM central banks to hike rates to halt capital flight. However, as we noted last year, the global economy has been in the process of self-correction and rebalancing since then. Current account deficits are narrower, external buffers are more robust and policy stances are typically much more prudent. Furthermore, the Fed has taken great care over the last year to move with care and preview its intentions carefully.

-

- One of the key transmission channels of U.S. monetary conditions to the rest of the world is the value of the dollar, which impacts the ability of EMs to service their external obligations and leaves them vulnerable to capital flight. The so-called “reflation” trade, predicated on prospects for U.S. tax cuts and infrastructure investment, and the unfolding Fed tightening cycle strengthened the U.S. dollar between the election and the inauguration.

Yet most EMs withstood the dollar's strength fairly painlessly. Since then, legislative wrangles in the U.S. have taken the steam out of the refation trade. We do not expect EM central banks to have to tighten policy to ensure the proper alignment of their local currency.

-

- The Bank for International Settlements has been flagging the risk of unprecedented external debt buildup in EMs and their vulnerability to Fed policy normalization for some time now. But it is important to keep in mind that, in most cases, external debt remains low as a percentage of gross domestic product (GDP), and is often hedged. Sudden stops like the taper tantrum can create short term challenges with rolling over selected issues, but the risk must not be overstated.

-

- Recent political developments in the eurozone, the U.K. and the U.S. mean that EMs yields look attractive on a relative risk adjusted basis, as is evident by a surge in capital inflows to EMs despite narrowing yield gap. EMs that are plagued by political or policy risk — namely South Africa, Turkey and Mexico — have suffered outflows and significant currency depreciation for idiosyncratic reasons. With these exceptions, EM assets are offering a positive real yield and appear cheap on a relative basis, making them less susceptible to outflows.

-

- Domestic economic conditions are far from overheated in the EM universe. For example, annual corporate credit growth (as a percentage of GDP) is in fact negative or barely positive in most of the EM universe.

For all of these reasons, many EMs that were challenged four years ago appear much more resilient now. This frees their central bank to pursue policy that is most responsive to domestic considerations, as opposed to international investors. Our main point is not that EMs will not hike rates in the medium term, but that their central banks are now able to reassert their policy independence.

The key risks to this relative stability are from a sharp upswing in oil; a global risk aversion prompted probably by a trade war; or a localized deterioration. We do expect any of these to materialize. EMs that remain dedicated to discipline will prosper; those plagued by poor governance will lag.

A worry since the financial crisis was that the Policy Trilemma had become a Dilemma – i.e. the free cross border flow of capital meant a loss of monetary policy independence. This would have dire consequences for EMs. At least for now, however, it appears those worries were overdone.

A Distant HorizonJohn Maynard Keynes did not believe economies always self-correct over time. Keynes, who ultimately lent his name to the doctrine of government intervention during times of distress, famously said,

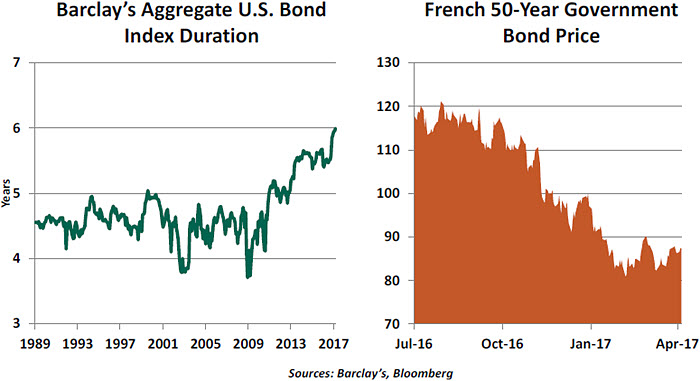

“(The) long run is a misleading guide to current affairs. In the long run we are all dead. Economists set themselves too easy, too useless a task if in tempestuous seasons then can only tell us that when the storm is long past the ocean is flat again.” During the past few years, the fixed income markets have been stretching the boundary of the long-term. For issuers, offering debt that matures far off into the future has locked in low financing costs for a very long time. But the holders of that debt may be in for some buyer’s remorse.

Interest rates in developed markets have spent the post-crisis years at very low (or even negative) levels. Central banks set the tone with accommodative monetary policy, which in many cases included the purchase of the long-term government bonds. The yields on sovereign debt, in turn, serve as benchmarks for other issues.

To lock in low carrying costs, borrowers at all levels have been seeking to lengthen the maturity of their debt. For American households, 40-year mortgages and ten-year automobile loans are now commonly offered, even though those terms extend well beyond the average length of ownership. Corporations have rushed to market with ever-longer bond issues; by some measures, the current duration of corporate debt is the highest on record.

Governments across the globe have also gotten into the act. The U.K., Spain, France and Canada (among others) have offered bonds with maturities of 45 years or more. Belgium went even further, floating a 100-year issue last June.

The attraction to debtors is clear: they have more time to pay off principal, which is friendly to their budgets. For individuals, extending terms can help them qualify for credit that might otherwise be beyond their reach. For corporations, the tenure of financing matches well with long-term investments that they might want to make. And for sovereigns, low interest payments for long periods help them meet annual deficit targets.

What is considerably less clear is the allure to the owners of long-term credit. Banks and finance companies extending loan terms may be attracting more marginal borrowers and taking on more credit risk. Owners of corporate and sovereign debt with very long maturities accept a heightened level of price risk; the value of a 50-year bond will decline by roughly four times more than the value of a 10-year bond for a given move in market interest rates.

Economic performance in the developed world has improved over the past year, and inflation is higher. Central banks are closer to curtailing their quantitative easing programs. (And as evidenced by their minutes of this week, the Federal Reserve is contemplating an outright reduction of its holdings.) This has led interest rates upward and diminished the value of funds holding long-term assets.

Of course, if one holds a bond until maturity, intermediate changes in price don’t matter much. Unless a default occurs, the bond will ultimately be worth its face amount. But maturities of 50 or 100 years are well beyond the time horizons of even the most farsighted owners (including pension funds). There is, therefore, a good possibility that generating needed cash flow will require liquidating holdings prior to maturity. And this could generate some meaningful losses.

Some have misinterpreted Keynes’ statement about the long run, suggesting that he was unconcerned with the accumulation of debt and deficits. Such was not the case. If he were alive today, Keynes would undoubtedly have something pithy to say about 50-year debt—and it might not be entirely flattering.

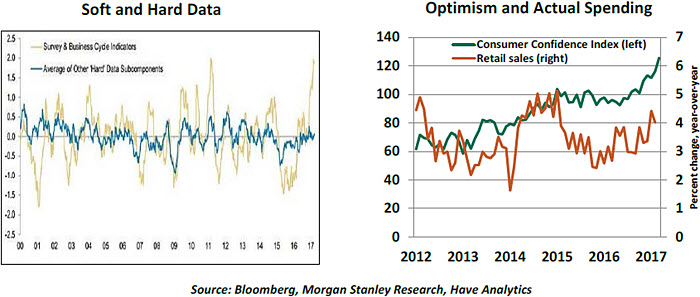

Sentiment versus RealityEaster baskets will be here soon. Some will rifle through the fake grass and the colored eggs in the hope of finding soft candy, while others will be looking for hard candy. In another arena, economists are presently puzzling over “soft data” and “hard data” to figure out the underlying momentum of the economy.

The term “soft data” refers to qualitative responses from U.S. business and consumer surveys. Hard data are counts of people employed, retail sales, orders of aircraft and prices of different goods and services. At present, there is a divergence in the message emanating from these two classes of information. The question is which one reflects reality.

A majority of soft data series paints a rosy picture of the economy. The latest U.S. consumer confidence index posted a 17-year high. The National Federation of Independent Business’s Small Business Optimism Index is the highest since 2004. The Institute for Supply Management’s factory composite index is the best in nearly seven years. The recent significant increases in these composite indices of soft data imply robust economic conditions ahead.

Employment, housing starts, retail sales, home sales and orders for durable goods – these and other “hard data” point to a more muted increase. Historically, soft and hard data track well directionally and are largely coincident, but soft data tend to overshoot in both directions.

Soft data from surveys are useful because they are available well before actual economic reports are published. But a part of the reason for the gap between soft and hard data is that components of soft data contain expectations that leave room for exaggeration. Interestingly, the two Fed sources of “nowcasts,” which track growth in the current quarter, are signaling different things because one uses soft data much more prominently.

Hard and soft data rarely diverge for long. If the positive post-election assessment of the policy environment in the U.S. exceeds what Congress can deliver, a reconciliation will be close at hand. And this could take the form of a “hard” landing.

northerntrust.comInformation is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

©

2017 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit

northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust