Soft Data for the First Quarter, Firming Thereafter

U.S. political issues have dominated the economic headlines for the past month. The failure of the Republican-led House of Representatives to repeal and replace the Affordable Care Act delays consideration of tax reform and infrastructure spending. Following this legislative battle, there is more uncertainty now about when and if Congress can deliver changes to fiscal policy this year.

Consumer and business sentiment surveys present an upbeat assessment of the economy. Actual “hard” economic data present a less sanguine picture. The recent step-back in consumer spending should be reversed soon. A pickup in real gross domestic product (GDP) growth is predicted for the second quarter after a slow performance in the first quarter.

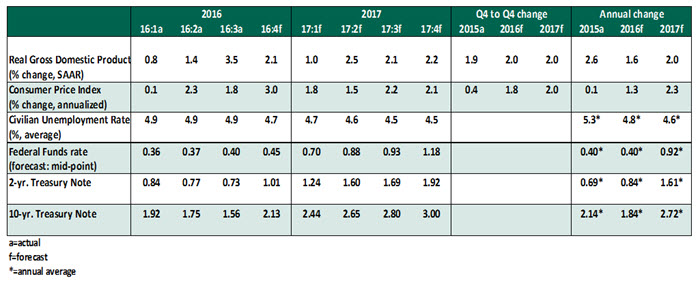

Key Economic Indicators

Key Elements of the Forecast

-

- Consumer spending fell 0.1% and 0.2% in February and January, respectively. One-off factors influenced these numbers. Auto sales shot up in December (18.4 million units) to their highest level in more than a decade, and a partial payback occurred in the first quarter. Warm weather in the first two months of the year reduced spending on utilities. Looking ahead, the factors that underpin consumer spending remain supportive of a recovery.

-

- The current U.S unemployment rate (4.5% in March and 4.7% on average in the first quarter) points to full employment conditions. Monthly gains in payrolls slowed in March (+98,000) following solid increases in the prior two months. Bad weather in some parts of the country explains a part of the weakness. Hourly earnings increased 2.7% in March, representing a small deceleration from the prior month. Employment compensation should match hiring strength in the months ahead, which should boost consumer spending.

-

- Developments in the housing sector are largely positive. Single-family housing starts advanced in January and February, while the volatile multi-family starts component fell. Sales of new single-family homes have risen since December, while purchases of existing single-family homes have been flat. Actual residential construction spending in the first two months of the year implies strong growth in residential investment expenditures during the first quarter.

-

- The Institute for Supply Management’s (ISM) factory survey in the first quarter recorded the highest reading in six years. Quarter-to-date, shipments of non-defense capital goods (an input for the business equipment spending in the GDP report) suggest a stronger gain compared with the fourth quarter. In other words, hard data are pointing to continued growth in business equipment spending that is more muted than the more upbeat message from soft survey data.