SUMMARY

- Keeping a Cap on Oil Prices

- The Auto Sector May Be Leaving the Fast Lane

- Russia, Recovering from the Rubble

I grew up in the city and my wife grew up in the suburbs. We had the briefest of conversations about where we would locate after our wedding—and ended up about a mile from her family home. That story clearly illustrates who has the true power in our relationship.

The move added a degree of difficulty to my daily commute. Instead of hopping on a bus at the nearest street corner, I had to walk a mile to take a commuter train. The monthly pass cost twice as much, which challenged our meager finances. Matters got worse when the price of the ticket doubled seemingly overnight, the result of a spike in the price of fuel.

The oil markets have evolved dramatically in the generation since then. The Organization of Petroleum Exporting Countries (OPEC) has lost its grip on global production, with the United States (among others) rising to become a significant source of output. The new dynamic has been on prominent display so far this year, bringing important consequences for countries and central bankers.

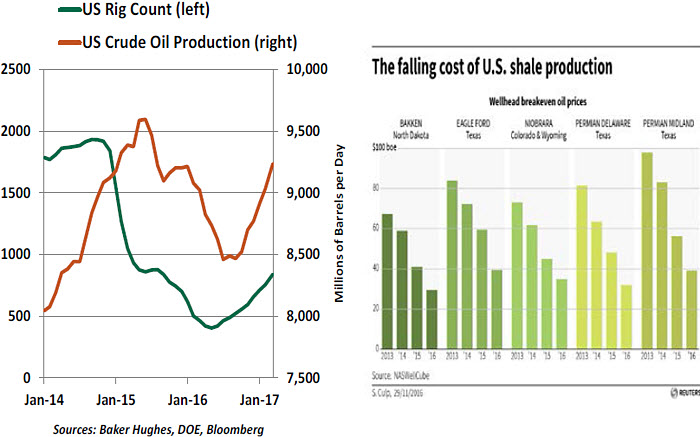

The oil “bust” that began in the summer of 2014 saw the price of crude fall from over $100 per barrel to less than $30 at the beginning of last year. The realignment was extraordinarily painful for oil producers. The number of active U.S. rigs fell by 80%, and countries overly reliant on energy revenue fell into hard times.

The drivers of the fall were many and varied, but they all come back to demand and supply. World demand for oil has grown only moderately; China’s growth is slowing, and the pace of expansion in the developed world remains modest. Energy consumption among major oil producers also slowed, as their economies were hindered by lower oil revenues.

On the supply side, OPEC no longer has a stranglehold on output: half of the top ten global producers (Russia, the U.S., China, Canada, and Brazil) are not OPEC members. Divergent agendas within OPEC have made supply restrictions hard to design and enforce.

There was widespread suspicion that Saudi Arabia, which has a huge reservoir of proven reserves, had engineered (or at least tolerated) the glut to hinder marginal producers. Falling prices made it uneconomical for some to bring crude out of the ground and hampered the fiscal health of Saudi Arabia’s rivals. Estimates suggest that most of the world’s major producers need a price of more than $60 per barrel to balance their budgets.

Low prices had the desired effect. Iran’s ascent slowed, and the U.S. shale industry endured a significant retrenchment. Investment and employment in the American energy sector diminished sharply, and some firms in the industry defaulted on their debts.

But inexpensive oil also challenged the kingdoms of the Middle East. And so last fall, OPEC crafted supply restrictions. Russia pledged its cooperation, adding credibility to the pact. Prices quickly moved above $50 per barrel, but they have not been able to advance much further.

The main reason for this is that U.S. suppliers act as a cap on the world price of oil. The challenges of last year removed marginal producers and paved the way for a considerably stronger and more nimble industry. Average extraction costs have fallen by more than half in key areas of the country.

Further, balance sheets in the U.S. energy sector are healthier. When oil prices pushed north last fall, companies took advantage by issuing equity and selling assets. Equipment is once again in high demand; it is likely that this will boost the business investment line of U.S. gross domestic product. Employment in the oil and gas sector is rising again.

Over the last six months, American production and inventories have recovered powerfully. The speed with which this occurred led some observers to term petroleum “a spigot business.”

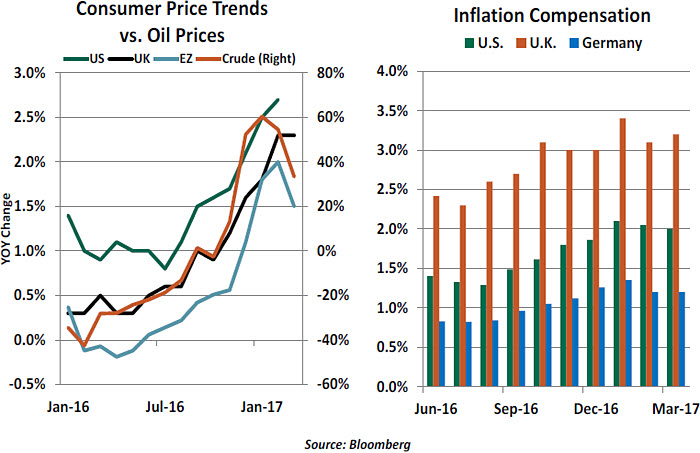

The impact of this effective limit on crude prices is significant. For countries that are net importers (which still includes the U.S.), moderating energy prices are beginning to influence inflation and inflation expectations. “Headline” price indices (which include all goods and services) had been trending up over the past twelve months, leading some to speculate that monetary policy would have to tighten sooner rather than later. With oil settling in at a new equilibrium (and, prospectively, declining), this pressure should abate. Calls for the European Central Bank and the Bank of England to move before the end of the year are fading.

Moderating inflation will also serve to raise real incomes in the developed world. There wasn’t much of an “oil dividend” derived from the 2014-2015 correction in oil prices, as many households used the savings to pay down debt. But with leverage under better control today, real consumption could be a beneficiary this time around.

On the down-side, revenue from the reserves of oil-producing nations is not likely to return to the apex seen three years ago. This could force significant budgetary compromises that would result in painful adjustments for populations. Venezuela is an unfortunate and extreme example, but others may be facing uncomfortable transitions. The Middle East, already unstable, could destabilize further. Russia, struggling with recession, may have to consider the scale of its international interventions.

Oil remains the dominant commodity of our generation, with the power to create significant changes of fortune for commuters and countries alike. But the dynamics surrounding “black gold” are quite different from thirty years ago, raising critical implications for economics and geopolitics. My anger at paying $185 per month for a train ticket seems trivial by comparison.

Bumps in the RoadOver the last seven years, aggressive lending has fueled auto sales. But the latest quarterly numbers suggest a reduced speed for the sector. If this weakness persists, it will ripple through the economy.

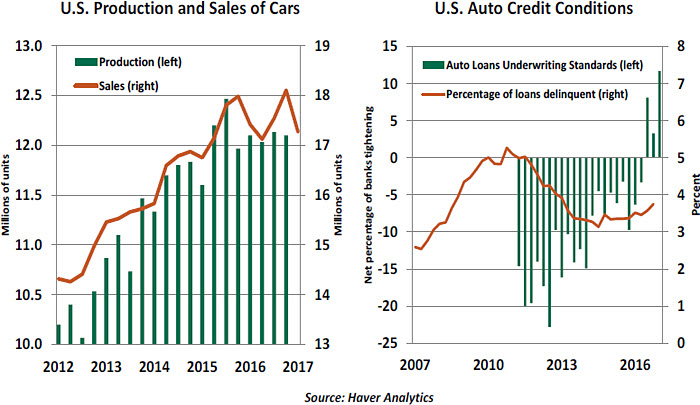

Outstanding U.S. auto loans are currently around $1.2 trillion, having risen a remarkable 65% during the current economic recovery. Underwriting standards for car loans were relaxed during most of the current business expansion. The easy lending environment encouraged sales, which rose from around 10 million cars and light trucks in 2008 to more than 18 million last year. The production of autos and the industry’s employment rate have advanced to meet the demand.

Typically, consumers have financed their cars with amortizing loans. Lenders have continuously extended the maturities of credit; the average term of an auto loan is now 68 months, half a year longer than it was six years ago. Longer maturities spread out the timeline of payments and tend to attract more marginal borrowers; the subprime sector of the auto loan market has been growing rapidly since 2009.

In addition, preferences have shifted toward leasing cars. Edmunds estimates that leases now constitute nearly a third of all cars sales, a record high. Car lease volumes have grown 91% over the past five years. Leases are popular, particularly among millennials, for their lower payments and a lower level of commitment. For financiers, however, leasing leaves the seller with residual risk if the vehicle does not hold its value as well as expected.

Unfortunately, auto loan delinquencies have been increasing, a worrisome development. About 3.1% of auto loans were past due in the third quarter of 2014, the low reading for the current business expansion. The percentage of delinquent auto loans has since moved up to 3.75% in the fourth quarter of 2016. To put things in perspective, the low for auto loan delinquency rates was 2.0% in the last business cycle, and the high was 3.1% just before the recession commenced in the fourth quarter of 2007.

Other details indicate that the contours of this market have changed for the worse. After five years of rapid growth in car leasing activity, many lease periods are now expiring, causing a large number of cars to be released into the used car market. The major outcome of this trend is that prices for used cars have fallen significantly and trimmed headline inflation numbers.

In response to more challenging conditions, the auto loan lending situation became less favorable in the second half of last year. The Federal Reserve’s Senior Loan Officer Opinion Survey on bank lending practices indicated tighter auto loan underwriting standards in the three quarters ended in March 2017, making it more difficult for some prospective car owners to afford vehicles.

Auto sales fell 17.2% in the first quarter of this year, the largest decline since the first quarter of 2009 when the “cash for clunkers” program ended. The setback in auto sales brings down overall consumer spending. If the weakness persists, production and employment will be adversely affected. Employment in the auto industry has been nearly flat in the past year.

Although car loans represent less than 10% of total household liabilities, the inability to service this debt during a long expansion with declining joblessness is a troubling sign. While unlikely to become a systemic issue, it is a bad omen for the automobile industry.

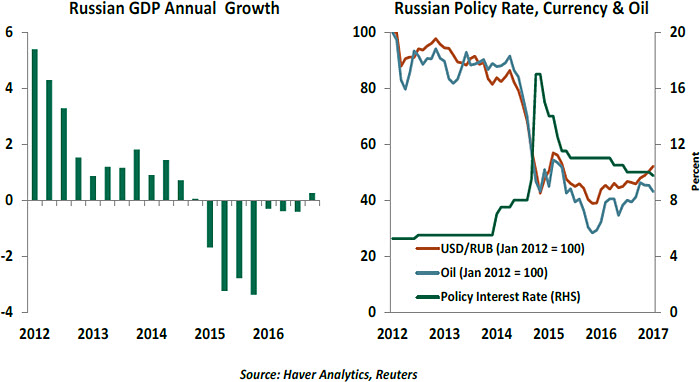

Russia, Slow and SteadyIn December of 2014, the Russian central bank ramped up its key policy rate from 9.5 percent to 17 percent to arrest the free fall of the Russian ruble. The currency had lost 60 percent of its value in the first two weeks of that month, before the emergency rate hikes reversed some of those losses. The culprit was the sharp fall in oil prices that began in the autumn of 2014.

For an economy dependent on oil for a fifth of all activity, 65% of all exports, and about half of all government revenues, the decline in oil prices has been crippling for Russia. The real gross domestic product (GDP) of the country is still lower than what it was five years ago. Sanctions by the United States since 2014 over Russia’s involvement in Ukraine haven’t helped either.

Moscow has traditionally done a fine job of macroeconomic stabilization by addressing current account and fiscal deficits, preserving currency value and controlling inflation in times of crisis. A large cache of foreign reserves (25% of GDP) and a significantly large net foreign asset position (30% of GDP) have helped Russia avoid crisis. But little progress has been made to wean the economy away from hydrocarbons or to implement other structural reforms, despite the presence of a powerful central government for almost two decades. It would not be wrong to characterize the Kremlin’s economic policy as good macro, bad micro.

Nevertheless, progress on macroeconomic stabilization, a modest recovery in oil prices, and initial hopes of rapprochement with Washington have rallied Russian markets. Strong capital inflows have encouraged the government to go on a dollar bond issuance spree, and the high interest paid on these issues has attracted international investors.

However, the enthusiasm may be short-lived. The long-term challenges of poor economic structure, reliance on oil, and a contracting population mean that growth potential for Russia remains low. To top it off, prospects of the United States lifting the sanctions seem to be fading, as relations with the U.S. have soured in a short space of time. While Russia has weathered low oil prices better than other producers, more stormy times may lie ahead.

northerntrust.comInformation is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

©

2017 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit

northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust