Let’s Talk About Tax, Baby

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

This week I had the pleasure of attending Evercore ISI’s Energy Policy & Geopolitics Conference in Washington, D.C., where I visited with senior staff responsible for infrastructure and energy decision-making. The meetings were encouraging and highly instructive, and they opened my eyes up to some of the lesser-known inner workings of the government. Among them is the reconciliation process, whereby Congress instructs a number of committees to report on any budgetary changes a new bill or spending package might trigger. For example, if President Donald Trump truly wishes to build a wall on the southern border, he’ll need to acquire the capital from other areas of the government’s budget. In other words, “the wall” must turn out to be revenue- and distribution-neutral. It’s a highly complex process—all matters of policy are entwined in and affect various departments, after all—which partly explains why Congress often seems to have such difficulty getting anything accomplished, including repealing Obamacare.

As President Donald Trump admitted to Reuters this week: “[Governing] is more work than in my previous life. I thought it would be easier.”

The Environmental Protection Agency (EPA), part of the reconciliation process, is one such entity that’s notorious for standing in the way of infrastructure and energy projects. The agency has traditionally held the attitude that the best development is no development. However, the Trump administration has an ace up its sleeve: the Fixing America’s Surface Transportation (FAST) Act, signed into law in December 2015. According to the official website, FAST-41, as it’s known, “was designed to improve the timeliness, predictability and transparency of the Federal environmental review and authorization process for covered infrastructure projects.” Project delays, therefore, can be combatted with transparency and accountability.

|

I also had the opportunity to visit the Treasury Department. I was pleased to hear that its senior analyst, who reports directly to Secretary Steven Mnuchin, closely monitors the purchasing manager’s index (PMI) and China, as we do, and keeps an eye on both oil and gold, which the department views as a currency. He seemed genuinely concerned about how federal rules and regulations might affect the work of professional brokers and traders. Specifically, he worries about impairing liquidity in capital markets, which makes price discovery exceedingly challenging. Having served in both the Obama and Trump administrations, I found the analyst very insightful, articulate and balanced in his views. Not once did he have an explicitly negative thing to say about either president, and I got the sense that he cared deeply about the execution of his job, which was highly encouraging.

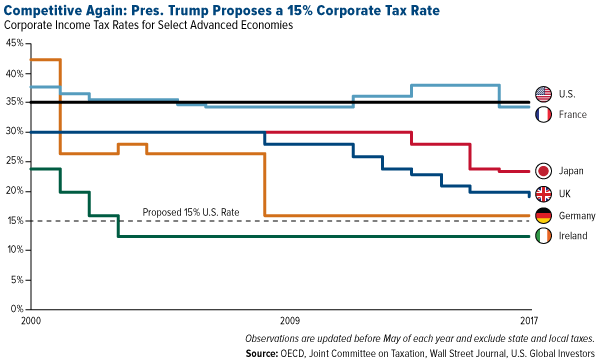

We stand on the doorstep of Trump’s 100th day in office, and as promised, the president unveiled his long-awaited U.S. tax reform proposal Wednesday, exciting many investors who might have begun to doubt his resolve following a number of significant setbacks. Most of the stock market gains actually occurred in anticipation of the announcement, with the Dow Jones Industrial Average and S&P 500 Index slightly losing ground on Wednesday, despite both indices logging positive monthly gains in five of the last six months. The small-cap Russell 2000 Index closed at an all-time high Wednesday, presumably because smaller domestic companies have the most to gain from Trump’s plan to lower the corporate tax rate from 35 percent, in effect since 1993, to a much more competitive 15 percent.

If Trump gets his way—and let’s be clear, it’s going to be an uphill fight—U.S. corporate taxes will decline from being the highest among fellow Organization for Economic Cooperation and Development (OECD) economies to just a few degrees north of Ireland’s highly favorable 12.5 percent.

Not only would this be the most meaningful overhaul of our tax code in more than 30 years, but it would also put the U.S. in very good company. If you recall from a September Frank Talk, I shared with you some of the accolades the Republic of Ireland has received partly as a result of its low tax rate, including being named “the most effective country in the EU in which to pay business taxes” by PricewaterhouseCoopers (PwC). It also ranks seventh in world competitiveness, according to Switzerland’s International Institute for Management Development (IMD), and is the fastest-growing European economy.

In the final quarter of 2016, Ireland expanded an impressive 7.2 percent year-over-year. Compare that to America’s sluggish start to 2017 with growth at 0.7 percent, the slowest quarterly rate in three years. Analysts had expected 1.2 percent. Gold, long considered a safe haven asset, closed up nearly 0.3 percent.

Obviously, there’s more to Ireland’s success than low corporate taxes, and we can’t expect the U.S. to enjoy the same momentum overnight after adopting a 15 percent tax rate. But it’s a start. As I said earlier this week, there’s still much more work that needs to be done, including streamlining burdensome financial regulations.

Can’t Please All of the People All of the Time

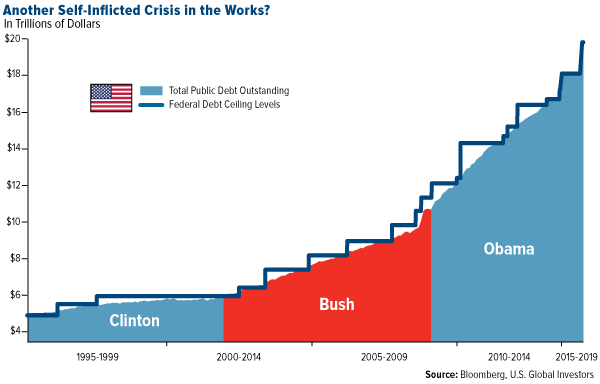

Not everyone is entirely on board with Trump’s idea, however. Many Democrats claim the plan—which includes both corporate and income tax reform—favors only the top earners, while fiscal conservatives worry the tax cuts could dig the U.S. deeper into deficit spending and add to the already-mountainous national debt, requiring another showdown over raising the debt ceiling.

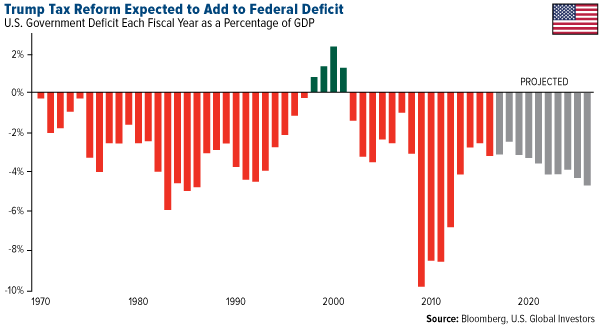

The bipartisan, Washington, D.C.-based Committee for a Responsible Federal Budget (CRFB) estimates that Trump’s plan could add between $3 trillion and $7 trillion to the federal debt over the next decade, stating emphatically that “America can’t afford” it. In addition, Bloomberg analysts see increased deficit spending over the next several years, provided everything else remains the same.

Others aren’t as negative. According to the highly-respected Tax Foundation, the oldest tax think tank in the country, an additional 1 percent growth in GDP would need to occur every year for the next 10 years to offset the cost of Trump’s plan. Although this doesn’t sound so out-of-reach, the report’s author, Alan Cole, makes it clear that this 1 percent growth must go “above and beyond” analysts’ top forecasts.

As expected, among the most enthusiastic cheerleaders of the reform are members of Trump’s inner circle, including economic adviser Gary Cohn and Treasury Secretary Steven Mnuchin, who insists that the economic growth that results from the tax cuts will sufficiently self-finance the costs of the tax cut.

I’m inclined to agree, with reservations.

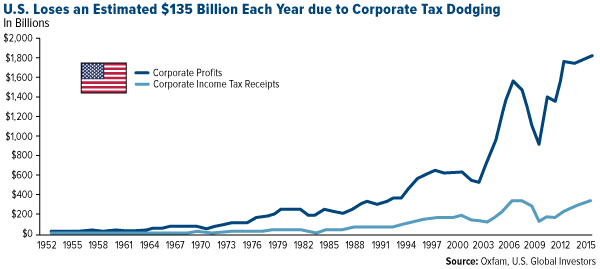

According to Oxfam, the U.S. loses out on approximately $135 billion each year as multinational companies continue to move operations overseas, presumably to avoid the astronomical tax and burdensome regulatory environment. In 1953, an estimated $1 out of every $3 of federal revenue was collected in corporate taxes. Today it’s closer to $1 out of $9, even as profits have surged dramatically since the 1950s. In 2015, the 50 largest U.S. corporations stashed as much as $1.6 trillion overseas, according to Oxfam.

Provided Trump can also deliver on his campaign promise to streamline corporate and financial regulations, I’m confident that a large percentage of this cash can be repatriated back into the U.S.

But what if there was another way? In a recent article in National Review, the conservative news magazine founded by William F. Buckley in 1955, columnist Kevin D. Williamson takes a hardline stance, arguing that Trump’s 15 percent tax is “about 15 points too high.” The corporate tax, Williamson says, leads to double taxation, as income is taxed once at the corporate rate and again as a salary or dividend.

Scrapping the corporate tax, Bahamas- or Cayman Islands-style, “would not represent a tax-free windfall to a bunch of pinstriped boardroom schmucks and Wall Street types and corporate shareholders.” Instead, he writes, it would unleash economic growth for the rich and poor alike, such as we’ve never seen. Imagine:

But if [businesses] pay [the saved 39 percent] out in salaries and bonuses, whether to fat-cat executives or ordinary line workers, those people pay the individual income tax on that money. If they pay it out to shareholders in the form of dividends, the shareholders pay the capital-gains tax on that money. If it is distributed through other capital gains, the same thing applies. If it is used to acquire facilities or equipment, then that money becomes income for another company, which has the same choices about how to dispose of it. The money still gets taxed, but not until it hits someone’s bank account.

Unrealistic? Probably. But Williamson’s idea is interesting food for thought regardles.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.91 percent. The S&P 500 Stock Index rose 1.51 percent, while the Nasdaq Composite climbed 2.32 percent. The Russell 2000 small capitalization index gained 1.49 percent this week.

- The Hang Seng Composite gained 2.38 percent this week; while Taiwan was up 1.59 percent and the KOSPI rose 1.87 percent.

- The 10-year Treasury bond yield rose 3 basis points to 2.28 percent.

Domestic Equity Market

Strengths

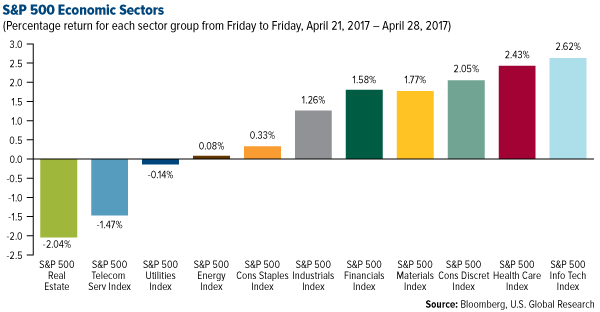

- Information technology was the best performing sector of the week, increasing by 2.62 percent versus an overall increase of 1.51 percent for the S&P 500.

- CR Bard was the best performing stock for the week, increasing 21.50 percent.

- The Nasdaq topped 6,000 for the first time. The tech-heavy index put in its first close above the 6,000 level on Tuesday, and it is now up more than 10 percent in 2017.

Weaknesses

- Real estate was the worst performing sector for the week, falling 2.04 percent versus an overall increase of 1.51 percent for the S&P 500.

- Synchrony Financial was the worst performing stock for the week, falling16.72 percent.

- U.S. Steel tanked after reporting an unexpected loss. Shares were down by 17 percent before the opening bell after the company reported an adjusted loss of $0.83 a share versus the Wall Street expectation of a gain of $0.35. Revenue was also light, coming in at $2.73 billion versus expectations of $2.95 billion.

Opportunities

- Netflix entered a licensing deal in China. The streaming video giant is teaming up with Baidu’s iQiyi to bring its content to mainland China.

- Weight Watchers has a new CEO. Mindy Grossman, current chief executive of HSN, has been named CEO, Reuters says. Shares of Weight Watchers spiked as much as 13 percent in after-hours trade on Wednesday following the announcement.

- The owner of Ugg boots is up for sale. Decker Outdoors announced it is exploring strategic alternatives, including a sale, that have the "potential to unlock further value" for shareholders.

Threats

- One of the biggest middlemen in the drug industry lost its biggest customer. Express Scripts, one of the largest pharmacy benefit managers in the U.S., said Anthem, which is responsible for about 18 percent of its revenue, will not renew its contract with the company.

- Synchrony Financial’s above-peer loan growth, wide loan margins and relatively low expense ratio haven’t offset a recent surge in credit costs, raising risk for its earnings outlook. The company raised its loss-rate forecast twice in three quarters, third quarter 2016 and first quarter 2017, and expects large reserve increases to continue through 2017 as a result.

- In its latest quarterly report, Seagate Technology’s revenue gains of just 3 percent were far weaker than those following the stock had wanted to see, and Seagate said that sales could remain weak this quarter as well. Component shortages are posing an obstacle to Seagate's growth, even though overall, demand appears to be staying fairly stable.

The Economy and Bond Market

Strengths

- April’s Chicago PMI came in at 58.3, better than March’s 57.7 level and consensus for 56.4. The release noted that optimism has risen for three consecutive months, as has demand with new orders nearing a three-year high.

- German business confidence is booming. Germany's Ifo Business Climate, an assessment of current conditions, jumped to 112.9 in April from 112.4 in March.

- Policymakers in China are bullish. Speaking at a G-20 summit in Washington, finance minister Xiao Jie said numerous positive signs were emerging from the Chinese economy, Reuters reports.

Weaknesses

- U.S. first quarter GDP increased 0.7 percent, worse than consensus for around 1 percent expansion and the slowest in three years.

- U.S. consumption increased just 0.3 percent following a 3.5 percent expansion in the fourth quarter, the worst performance since 2009. Consensus was for 0.9 percent.

- The final University of Michigan consumer sentiment reading came in at 97.0, below the prior reading of 98.0, which was also the consensus.

Opportunities

- Next week in U.S. data it will be a face-off between soft and hard data. Representing the former, the April manufacturing and non-manufacturing ISM surveys are scheduled for Monday and Wednesday, respectively. The all-important nonfarm payrolls report on Friday will be the key hard data release. A rebound in employment growth after a weak showing last month is expected. The FOMC will keep interest rates unchanged on Wednesday. Investors will be looking for any forward guidance from the Fed on the timing of the next hike.

- Although light on details, Trump’s initial plan for tax reform is out. Key details from the plan include lowering the corporate tax rate to 15 percent and reducing the number of personal income tax brackets from seven to three with rates of 35 percent, 25 percent and 10 percent, respectively.

- According to BCA, its global Leading Economic Indicator remains in a solid uptrend. In the U.S., burgeoning animal spirits are powering a recovery in business spending, as evidenced by the jump in factory orders and capex intentions. Consumer confidence is also soaring. If history is any guide, this will translate into stronger consumption growth in the months ahead. Further, the lagged effects from the easing in financial conditions over the past 12 months should help support activity. The current message from BCA’s U.S. Financial Conditions index, which leads the business cycle by 6-9 months, is that U.S. growth will stay sturdy for the remainder of 2017.

Threats

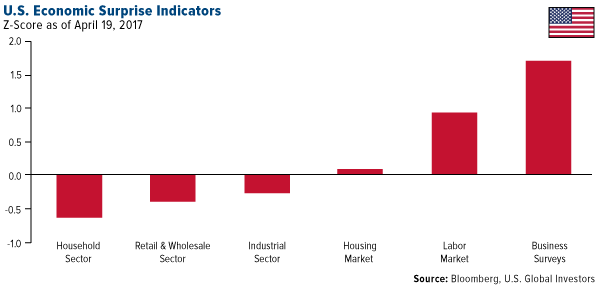

- While the household, retail & wholesale, and industrial sectors are experiencing moderate downside surprises in recent monthly indicator releases, the real estate sector, labor market and Fed surveys of regional economic activity are reporting upside surprises. To the extent that the labor market and business and household surveys provide reliable guides to the economic outlook, these large upside surprises suggest an environment for higher U.S. bond yields.

- Small business confidence soared following last November's election on hopes of corporate tax cuts and deregulation. The optimism is now being scaled back. The NFIB survey shows a significant inflection lower in expected sales. Expansion and hiring plans also look to have peaked.

- According to BCA, bond market positioning is no longer at a bearish extreme and the U.S. economy is approaching full employment. As such, they expect Treasury yields will soon break through the upside of their post-election trading range. BCA’s advice is to maintain below-benchmark duration.

This week spot gold closed at $1,268.29, down $15.81 per ounce, or 1.23 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 5.69 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index off just 2.20 percent. The U.S. Trade-Weighted Dollar Index finished the week lower by 0.95 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Apr-25 |

Hong Kong Exports YoY |

10.4% |

16.9% |

18.2% |

|

Apr-25 |

U.S. New Home Sales |

584k |

621k |

587k |

|

Apr-25 |

Conf. Board Consumer Confidence |

122.5 |

120.3 |

124.9 |

|

Apr-27 |

ECB Main Refinancing Rate |

0.000% |

0.000% |

0.000% |

|

Apr-27 |

Germany CPI YoY |

1.9% |

2.0% |

1.6% |

|

Apr-27 |

U.S. Durable Goods Orders |

1.3% |

0.7% |

2.3% |

|

Apr-27 |

U.S. Initial Jobless Claims |

245k |

257k |

243k |

|

Apr-28 |

Eurozone CPI Core YoY |

1.0% |

1.2% |

0.7% |

|

Apr-28 |

U.S. GDP Annualized QoQ |

1.0% |

0.7% |

2.1% |

|

May-1 |

ISM Manufacturing |

56.5 |

-- |

57.2 |

|

May-1 |

Caixin China PMI Mfg |

51.4 |

-- |

51.2 |

|

May-3 |

ADP Employment Change |

173k |

-- |

263k |

|

May-3 |

FOMC Rate Decision (Upper Bound) |

1.00% |

-- |

1.00% |

|

May-4 |

U.S. Initial Jobless Claims |

250K |

-- |

257k |

|

May-4 |

U.S. Durable Goods Orders |

0.7% |

-- |

0.7% |

|

May-5 |

Change in Nonfarm Payrolls |

190k |

-- |

98k |

Strengths

- The best performing precious metal for the week was palladium rising 4.07 percent as Metals Focus sees a global deficit of about 680,000 ounces this year. In addition, Norilsk Nickel PJSC noted this week that their first quarter production of palladium declined 14 percent. Not to be forgotten, investors were loading up on gold through exchange-traded products, reports Bloomberg, pouring $487 million into SPDR Gold Shares on Wednesday. That was the biggest daily inflow into the world’s top bullion ETF in seven months. Escalating tensions between the U.S. and North Korea, along with noise around President Trump’s tax cut proposals, are spurring demand for safe-haven assets, the article continues. “There’s an appetite for storehouse of wealth at this point,” said Peter Sorrentino of Comerica Asset Management Group.

- Swiss gold exports increased 57 percent month-over-month in March to 140.3 tons, reports Bloomberg. Shipments to India rose to 55.6 tons from 37.9 tons in February, while exports to China also increased to 24 tons versus 22 tons the month prior. Similarly, China’s gold imports from Hong Kong jumped to the highest in 15 months, as buyers took advantage of a slump in prices in the middle of March, reports Bloomberg.

- All India Gems and Jewelry Trade Federation said in an email statement this week that it sees gold sales rising 20 to 30 percent on demand from “Akshaya Tritiya.” The festival is considered auspicious for buying the yellow metal, and beginning April 28, sales on this day are seen better than last year because of weddings and aggressive promotional campaigns offered by jewelers, reports Bloomberg.

Weaknesses

- The worst performing precious metal for the week was silver, down 4.08 percent. Money managers cut their net long positions this week which were flirting with record highs achieved in 2016. On Thursday, gold declined for the third time in four days, reports Bloomberg, as euro-area economic confidence jumps and Emmanuel Macron’s lead in French polls curbs political concerns. “It’s all about the French election, which was a worry for many investors,” said Simona Gambarini of Capital Economics in London. “After the Dutch election and the Macron first-round win, it seems the risk of a repeat of Brexit elsewhere in Europe is much lower.”

- Following increased expenses at its mines in Argentina and Nevada, Barrick Gold Corp. tumbled after missing estimates and earnings on production. Shares fell the most in 21 months and as much as 11 percent in Toronto. This is only the company’s second earnings miss in seven consecutive quarters.

- The recent seismic event at Newcrest’s Cadia mine is greater than anticipated, according to David Haughton at CIBC. The underground operations are to remain shut down, possibly into fiscal year 2018. Full-year, fiscal year 2017 production is now expected at the lower end of 2.35M ounce to 2.60M ounce guidance, Haughton writes.

- In Paradigm Capital’s research note on the gold sector this week, the group writes that its analysis “highlights two daunting trends in the global discovery for major new deposits.” First, the rate of discovery has significantly declined from 1990-1999 relative to 2010-2015 and second, the cost of a new discovery has increased more than an order of magnitude, from $11/oz to $147/oz. Paradigm also writes, “majors can acquire advanced development-stage projects for a significant discount to what it would cost to explore and discover on their own ticket.” Although the pace of acquisitions has not picked up yet, the group believes it will, noting specifically that a new up-cycle appears to be slowly taking root. They see an opportunity for investors to take advantage of the “development discount” by adding a basket of quality development-stage and advanced exploration projects as a portion of gold portfolios.

- Global Mining Research looks at senior gold returns in its note this week, writing that there have been approximately $18 billion of gold transactions by seniors since 2012 at a ratio of 2:1, divestments to acquisitions. That has seen 3.8 million ounces per year of production divested. “Clearly the best assets haven’t been sold, so in theory the underlying businesses should be more profitable,” the note continues. From 2013 to 2016 the average margins for seniors was 35.2 percent, and over 2017E to 2020E, this is expected to improve to 43.5 percent. Lastly, the average ROIC for the group over 2013 to 2016 was 6.2 percent and this is expected to improve to 9.5 percent over 2017E to 2020E.

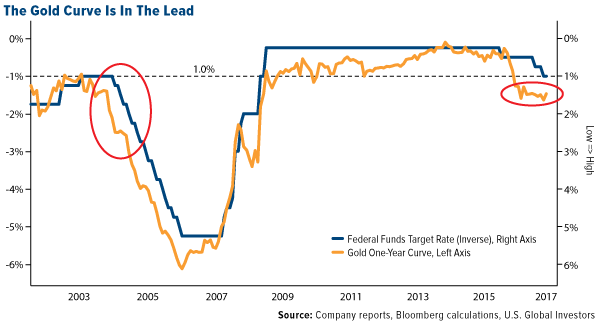

- Historically, Fed tightening cycles haven’t been sustained when both bond yields and crude oil are declining, writes Bloomberg Intelligence. And if these metrics don’t recover, the indication would be a one-and-done 2017 Fed. In a similar note, among the highest-correlated market indicators to the Fed funds rate is the shape of the gold one-year futures curve, which has stalled in 2017, reports Bloomberg. As you can see in the chart below, if the curve continues to flatten, the indication would be Fed one-and-done as mentioned above. “Since gold is a currency, its futures curve is priced off interest-rate expectations,” the article continues.

Threats

- Even with the unpredictability of President Donald Trump during his first 100 days in office, gold has yet to reclaim the surge it saw before his win in November, reports Bloomberg. In fact, some investors don’t think gold will go back up any time soon. “Without huge surprises from Trump, some investors are inclined to see more losses in gold as the U.S. economy stays strong, the Fed tightens, bond yields rise and inflation remains subdued,” the article reads. After Emmanuel Macron won the first round of the French election, Goldman predicts gold at $1,200 in the three months following.

- Because of President Trump’s tax plan and its disregard for the effect on the federal budget deficit, Bloomberg writes that this could pique the interest of a long-dormant segment of bond investors. “So-called bond vigilantes, once feared for enforcing restraint on spendthrift governments, have struggled to flex their muscles in recent years as global central banks stepped in to buy a glut of sovereign debt,” the article continues. With the Fed talking about trimming its Treasury holdings while the administration’s tax plan could spur more borrowing to cover a shortfall, now might be their time for a comeback! Those who think inflation is inevitable while the debt burden grows, tend to favor assets like gold.

- Gold buys the most silver since June, reports Bloomberg, as prices are set to cap their fourth monthly gain for the longest winning run since 2012. Silver has dropped more than 5 percent in April. According to Bloomberg, the move in the gold-silver ratio may signal a decline in gold. “I’d expect gold to play catch-up sooner rather than later,” said Jeffrey Halley of Oanda Corp. in Singapore (who also sees a break of $1,260 an ounce).

Strengths

- A note from Credit Suisse this week highlighted positive results for the Pulp and Paper Products Council (PPPC). March PPPC statistics came in stronger than expected on the back of strong demand from China benefiting Brazilian pulp producers such as Suzano, Fibria and Klabin. The data showed strong shipments well above their average at 19 percent month-over-month versus 14 percent in the same period last year, lower inventories, and a steady increase in pulp prices from China and Europe where prices have steadily risen for the past 15 weeks in a row.

- The best performing sector for the week was the BI Global Integrated Oils Valuations Peers Index. The index rose 2.1 percent along with rallying oil prices as participants are beginning to position themselves for the possibility of an extension of OPEC-led production cuts in the months to come.

- Gazprom PJSC, a large natural gas company located in Russia, was the best performing stock this week, finishing up 10.1 percent. The stock rose on the back of investors re-entering Russian equity markets and rallying energy prices this week.

Weaknesses

- Gasoline was the worst performing commodity this week losing 5.9 percent on the back of a large surprise build in inventories according to the Energy Information Administration’s (EIA) report. Gasoline inventories rose to 241,041 thousand barrels this week from 237,672 thousand barrels where inventories have maintained a consistent range over the past few weeks. As gasoline consumption accounts for almost one in every ten barrels of oil consumed globally, this could be an early signal of weakness in oil prices.

- The worst performing sector this week was the S&P/TSX Composite Gold Sub Industry Index. The index fell 5.9 percent on the back of the first round of France’s presidential election. Emmanuel Macron is on track for a win which proved positive for equity prices and negative for gold.

- The worst performing stock for the week was Barrick Gold Corporation, the largest gold mining company in the world. The company fell 12.9 percent on the back of falling gold prices.

Opportunities

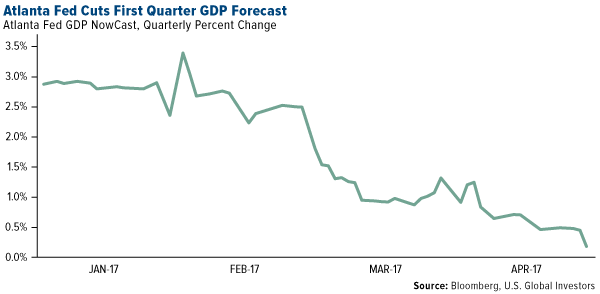

- The Atlanta Fed released its final first-quarter forecast for real GDP growth this week ay 0.17 percent, down from 3.4 percent back in February, according to Zero Hedge. Hard and soft data in the U.S. continues to collapse while other key data points such as the consumer price index (CPI), industrial production, and durable goods orders all continue to disappoint. The disappointment in U.S. macro data is not conducive to the Fed further hiking rates; however, if the dollar falls from these negative developments, this will bode positively for gold

- Big mining groups are back in the black extracting profits again according to the Financial Times this week. Over the past four years, the mining industry has had anything but an easy time as resource prices around the globe have been hit hard leaving many companies drowning in too much debt. Since 2013, the four biggest London based miners, Anglo American, BHP Billiton, Glencore, and Rio Tinto have undergone a massive cost-cutting exercise, selling off non-core assets to raise 33 billion dollars while laying off 200,000 employees to boost productivity. Coupled with higher than expected commodity prices last year, these four mining giants brought in roughly 15 billion dollars in profits last year versus 20 billion in losses a year earlier.

- U.S. crude oil stocks retreated for the third week in a row, the longest streak of inventory declines since December. Inventories of U.S. crude fell by a larger than expected 3.6 million barrels in the week of April 21, compared to expectations of a 1.14 million barrel draw, according to the weekly report released by the Energy Information Administration (EIA). Coupled with a softer greenback, crude oil prices are could potentially gain further strength in the near term.

Threats

- Key U.S. economic data points came in this week weaker than expected according to Zero Hedge. Initial jobless claims jumped the most in five months rising to 257,000, the biggest two-week rise since Thanksgiving of last year, while core durable goods orders fell at a rapid clip of 0.2 percent, the biggest drop since June 2016. The picture painted from these two indicators is fairly negative for raw materials, as both are bell weathers to productivity and demand.

- A top iron ore forecaster says iron ore prices will fall back below $50 a tonne according to an article in Bloomberg this week. Justin Smirk, senior economist of Westpac Banking Corp, states that as supply continues to build up and prices at mills continue to come off, users of the commodity will begin to question holding inventory which will add more negative pressure and momentum to the downside.

- In a research note released by Goldman Sachs this week, the bank forecasts the price of gold may come under pressure in the months ahead, targeting the shiny metal at $1,200 an ounce. The bank cites that a rally in real rates as a result of President Trump’s tax policies, a faster reduction of quantitative easing, and further economic growth around the globe as catalysts surrounding their bearish thesis towards the commodity.

Strengths

- China’s jobless rate fell to a 14-year low of 3.97 percent in the first quarter, reports Bloomberg. The Asian nation created 3.34 million jobs, on pace to exceed the government’s 11 million target for this year.

- South Korea’s GDP grew faster than expected in the first quarter, coming in at 2.7 percent versus 2.6 percent, reports Bloomberg. The country’s manufacturing sector and exports expanded even as it faced economic fallout from rising geopolitical tensions in the region, writes the Financial Times.

- The benchmark FTSE Bursa Malaysia KLCI Index was up over 2 percent for the week, reports Bloomberg. According to a note on Nasdaq.com, the KLCI finished slightly higher earlier in the week following gains from the financial shares, plantation stocks and industrial issues.

Weaknesses

- Some of China’s biggest energy producers are struggling with first quarter production, reports Bloomberg. However, oil’s recovery is helping ease the pain of shrinking outputs. “Higher capital spending may help output in 2018 or 2019, but no rebound is expected to show up for 2017,” said Laban Yu with Jefferies in Hong Kong. “Obviously higher oil prices did all of them a big favor and helped lift their earnings out of the disaster they experienced a year ago.”

- Twenty-six executives of a Chinese online peer-to-peer lender stood trial in Beijing on Wednesday and Thursday, reports ChinaDaily.com, after allegedly cheating the public out of a huge amount of money. Operators and executives of P2P lender Ezubao were charged with fundraising fraud, while some defendants were also charged with smuggling precious metals, illegal possession of guns and border-crossing.

- According to Reuters, Chinese banks are missing out on the “fee bonanza” offered by Chinese companies hunting for deals in the U.S., as scores of investment bankers profit. So what is holding Chinese banks back from the hundreds of millions of dollars that Wall St. banks and their European rivals earn advising Chinese companies on acquisitions and share and debt sales? The way Beijing controls the top lenders to manage the supply of credit to the Chinese economy, the article explains. U.S. rules require the controlling shareholder to seek Federal Reserve clearance for investment banking operations.

Opportunities

- The text of a 16-nation free trade agreement, the Regional Comprehensive Economic Partnership (RCEP), is likely to come out next year, according to Trade Secretary Ramon Lopez. Asian economic ministers will get a clearer picture of major trade parameters after meeting later this year, reports Bloomberg.

- According to Bloomberg, cruise operators, convenience stores and cosmetic makers are all emerging as sectors that could stand to benefit from an again China (a demographic consequence from the now-abandoned one-child policy). Deutsche Bank is betting on cruise-operating companies to play the shift in spending and travel, the article continues. In fact, Asian cruise passengers have tripled in 2015 from 2012.

- President Trump told Reuters that having good ties with China is more important than dealing with Taiwan, the latest sign that he is abandoning his combative China rhetoric in favor of a more cooperative approach.

Threats

- “There is a chance that we could end up having major, major conflict with North Korea,” said President Trump, warning of the ramifications should diplomatic solutions fail with the Asian nation. Senator John McCain followed up by stating that the U.S. leader understands that military action was a last resort.

- U.S. forces began installing a missile-defense system in South Korea, reports Bloomberg, sparking protests from local residents and complaints from China as tensions mount over North Korea’s nuclear program. The Terminal High Altitude Area Defense System (Thaad) should be operational by the end of the year, according to South Korea’s defense ministry. The introduction of Thaad has angered China, and has now become a campaign issue ahead of South Korea’s May 9 presidential election, the article continues.

- The crisis over North Korea’s nuclear program dominated talks in Moscow between Russian President Vladimir Putin and Japanese Prime Minister Shinzo Abe, reports Bloomberg. The situation has “seriously deteriorated,” according to the two leaders. “We call on all states involved in the region’s affairs to refrain from military rhetoric and seek peaceful, constructive dialogue,” Putin said on Thursday following the meeting.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 6 percent. Banks gained 20 percent on expectations that an agreement between Greece and its international creditors will take place by the end of May. The next Eurogroup meeting is scheduled for May 22.

- The Polish zloty was the best performing currency this week, gaining 2.5 percent against the U.S. dollar. Investors’ risk appetite increased and the zloty advanced the most among emerging market currencies after Emmanuel Macron won in the first round of the French elections on April 23.

- The industrial sector was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 5 basis points. The EU Commission has launched legal action against Hungary following a new education law which it claims is incompatible with the freedoms of the internal market. The new law in Hungary places restrictions on foreign-registered universities, and could lead to the closure of Hungary’s Central European University. Budapest has one month to respond.

- The Russian ruble was the worst performing currency this week, losing 82 basis points against the U.S. dollar. The central bank of Russia cut its key rate by 50 basis points to 9.25 percent, above market expectations of 25 basis points. This is the second rate cut this year and follows the 25 basis points cut at the previous meeting in March as inflation continues to decelerate toward the central bank’s 4 percent target.

- The consumer staples sector was the worst performing sector among eastern European markets this week.

Opportunities

- Centrist independent Emmanuel Macron won 23.8 percent of votes in the first round of France’s presidential election on Sunday, while Marine Le Pen head of the anti-immigrant National Front far-right party took 21.5 percent. Mr. Macron was current President Francois Hollande's economy minister but quit to create his own party, En Marche, which has a liberal, pro-EU agenda. The market reacted positively to his victory in the first round of elections, and most expect him to take the majority of the votes on May 7.

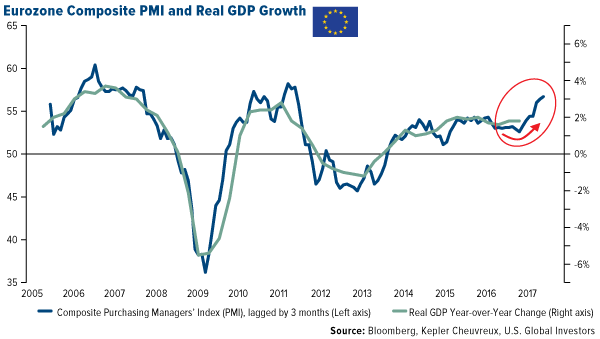

- Kepler Ceuvreux in European Investment notes wrote that economic indicators currently suggest that GDP growth in the euro area through the first half of the year will be close to 2 percent at an annual rate, thanks to improvements in both external and domestic demand. In fact, the general economic context in the eurozone at this time would seem to be the most favorable since the beginning of the decade.

- Turkish banks are set to benefit from a raft of incentives brought by President Erdogan’s administration that has led to a surge in lending, boosting banks’ revenue. Deutsche Bank AG expects first quarter profit at Turkey’s six largest banks to jump by an average 46 percent from a year earlier, as lenders are among the biggest beneficiaries from tax breaks and looser banking regulations.

Threats

- A recent report by Credit Suisse has shown that Russia is the most unequal of all the major economies, with the richest 10 percent of the population owning 87 percent of all the country’s wealth. This compares to 76 percent in the U.S. and 66 percent in China. VTB, a Russian bank, recently showed that 1 percent of the Russian population holds 46 percent of the country’s personal bank deposits. Many Russians believe this is at least in part due to corruption. Russians have historically tolerated government corruption, but things may be changing, as we saw in last month’s anti-corruption protests.

- Legislators in Europe voted 113 to 45 to reopen monitoring procedures in Turkey on strong concern over the functioning of democratic institutions after constitutional amendments were approved this month in a national referendum. Turkey rapporteur Marianne Mikko said the amendments, which significantly expand the powers of the president, “do not comply with our fundamental and common understanding of democracy.” This could be a formal deterioration in Turkey-EU relations.

- Deutsche Bank’s emerging Europe equity research team forecasts the ruble strengthening towards 54 rubles per dollar on average in 2018 versus 58 rubles per dollar in 2017. Their long-standing view has been that Russian energy stocks may lag in the recovering crude oil price environment due to the effect of ruble appreciation and a progressive tax system.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All