The Case of the Missing U.S. Stocks

Membership required

Membership is now required to use this feature. To learn more:

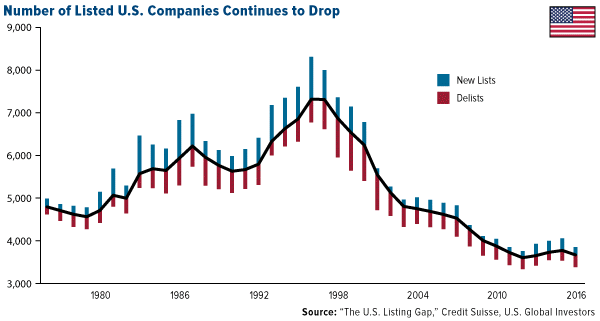

View Membership BenefitsIn the last 20 years, the U.S. stock market has undergone an alarming change that too few people are aware of or talking about. Between 1996 and 2016, the number of listed companies fell by half, from 7,300 to 3,600, according to a recent report by Credit Suisse. This occurred despite the U.S. economy growing nearly 60 percent over the same period.

click to enlarge

What’s even more flummoxing is that the U.S. seems to be the only developed country that lost so many stocks. Most other countries actually gained around 50 percent.

This matters because the U.S. stock market accounts for a little over half of the entire global equity market, meaning a huge (and growing) number of investors and fund managers now have fewer options to choose from than they did only a couple of decades ago.

So why’s the pool of publically-traded companies shrinking? We can point to a few different culprits.

For one, merger and acquisition (M&A) activity has strengthened in recent years, and when an M&A takes place, a company is consequentially delisted (if it was listed before the deal). The same thing happens, of course, when a company goes out of business.

Another reason could be the growth of private capital, which allows companies to raise funds without having to go public. Between 2013 and 2015, the amount of private money invested in tech start-ups alone tripled from $26 billion to $75 billion, according to consulting firm McKinsey. As a result, more and more software firms are managing to reach $10 billion in value before their IPO. Think wildly successful companies like Dropbox, Airbnb, Pinterest, Uber—all of which, for now, have avoided selling shares to public investors.

Unintended Consequences

My belief is that, out of all the reasons for fewer U.S. stocks and IPOs, the most impactful has been the surge in federal regulations over the last two decades. Rising costs associated with being listed on an exchange and meeting compliance standards have prohibited IPOs for all but the very largest U.S. firms. Small businesses—which, according to the American Council for Capital Formation (ACCF), account for more than half of all U.S. sales and 66 percent of all new jobs since 1970—are increasingly less competitive.

This partly explains why more and more companies are delaying going public. Back in 1980, Apple’s IPO came a mere four years after Steve Jobs, Steve Wozniak and Ronald Wayne founded the company in Jobs’ garage. Amazon waited only three years after Jeff Bezos founded it in 1994. Today that number has risen dramatically. It’s now estimated that the average age of a tech firm at the time of IPO is 11 years.

Some might disagree that regulations have had much of an effect on the U.S. equity market, but I believe the evidence is incontestable.

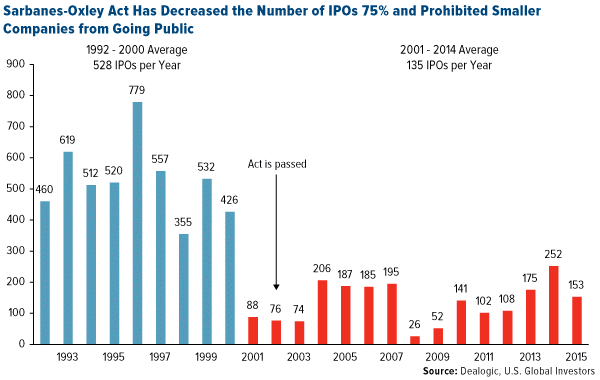

Consider the Sarbanes-Oxley Act (SOX), signed by President George W. Bush in 2002. Its goal, to prevent massive corporate fraud such as we saw from Enron and WorldCom, is an admirable one. But SOX has had several unintended consequences, as I’ve explained before. Because SOX’s requisite internal control procedures are so costly and cumbersome—necessitating additional compliance and accounting positions, not to mention hundreds of hours in compliance-driven tasks—smaller firms are inevitably at a disadvantage.

As a result, many small to mid-sized companies are delaying going public, or avoiding it altogether, to escape the regulatory burden. Before SOX, there were an average 528 IPOs a year. Since it was enacted, that number has fallen to 135, a decline of nearly 75 percent, according to Dealogic data. Last year, only 111 IPOs made it to market, a far cry from the 779 that took place in pre-SOX 1996.

click to enlarge

Other legislation has deterred even more companies from pursuing an IPO, including the Dodd-Frank Wall Street Reform Act.

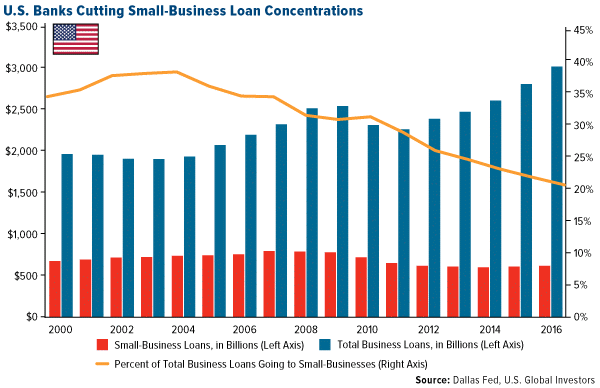

Consider also that small business loans have all but dried up for small businesses. In 2004, small business loans represented about 40 percent of commercial banks’ loan portfolio. Today, it’s closer to 20 percent, according to the Federal Reserve Bank of Dallas. This pullback in lending can be blamed on several factors, the Dallas Fed writes, “with regulatory burden among the most prominent”:

Large banks have indicated they are less likely to make small loans because the cost of processing a $100,000 loan is comparable to that of a $1 million loan. As a result, large banks have significantly reduced loans below a certain threshold, typically $250,000, or have stopped lending to businesses with revenue less than $2 million.

click to enlarge

It’s little wonder that, in an August 2016 survey conducted by the National Federation of Independent Business (NFIB), small-business owners said “unreasonable government regulations” were their second-highest concern, following “cost of health insurance.” More than 33 percent said regulations were a “critical” problem.

In another survey, this one conducted by the Center for Capital Markets Competitiveness (CCMC), nearly 80 percent of corporate treasurers, CEOs and CFOs said they had seen their business negatively affected by changes in the financial markets following the implementation of Dodd-Frank.

Relief Is Coming

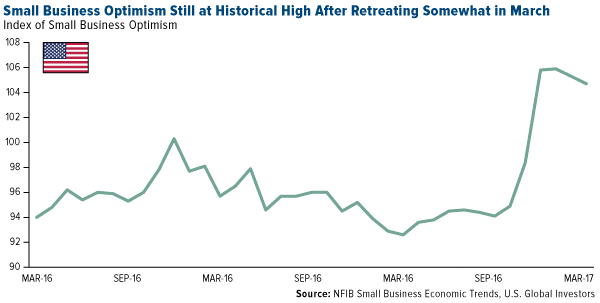

But there’s hope. President Donald Trump has pledged to roll back many of the rules that have acted like plaque build-up in the heart of smaller companies seeking to expand. Just this week, the House Financial Services Committee approved a bill to begin gutting many of the provisions in Dodd-Frank. The S&P 500 Index edged up to close at a record high Friday.

In December, a month after the election, the NFIB’s Small Business Optimism Index soared to 105.8, up from 98.4 in November, a 12-year high. Optimism fell somewhat to 104.7 in March, the most recent month of available data, but it still holds at historically high levels.

click to enlarge

Markets lately were beginning to lose faith in the president’s ability to deliver on a number of his key campaign promises. But after the House gave him a much-needed victory this week by voting to repeal Obamacare and Dodd-Frank, many small business-owners’ excitement about other Trump proposals such as deregulation and corporate tax reform is likely to be rekindled.

Until Trump can streamline regulations, however, it’s probably wise to focus on large-cap stocks, especially those that have an attractive dividend yield and are buying back their stock.

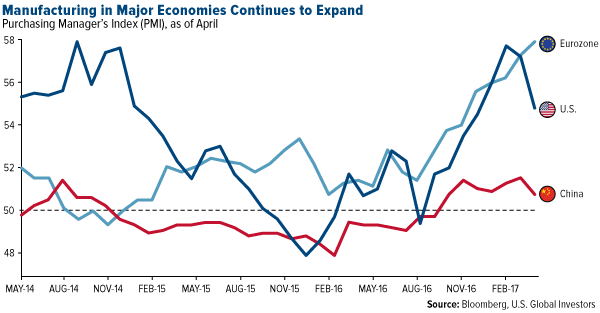

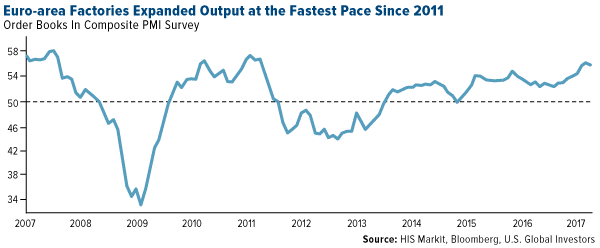

At the start of the second quarter, the eurozone’s manufacturing sector grew at its fastest pace in six years, climbing from 56.2 in March to 56.7 in April and marking the eighth straight month of expansion. Of the eight eurozone countries that IHS Markit surveys, only Greece failed to show any improvement during the month.

Growth was spurred by new orders, output and job creation, and companies are benefiting from both the historically weak euro and the European Central Bank’s ongoing stimulus, including low interest rates. Factory jobs are currently seeing one of their strongest upticks in the survey’s 20-year history.

Ahead of France’s presidential election this weekend—polls are heavily favoring 39-year-old Emmanuel Macron over far-right candidate Marine Le Pen—the country showed impressive momentum, rising from 53.3 in March to 55.1 in April. New orders grew at their sharpest pace in six years. Meanwhile, the United Kingdom’s manufacturing sector continued to expand post-Brexit, rising to a three-year high of 57.3.

click to enlarge

Both the U.S. and China continued to expand at the start of the second quarter, though at a slightly slower pace than in March. U.S. manufacturing growth relaxed a little more than 2 percent, from 57.2 to 54.8, but it still remains at a high level in the six months following the presidential election. Chinese factories pumped the brakes in April, with growth slowing to a seven-month low.

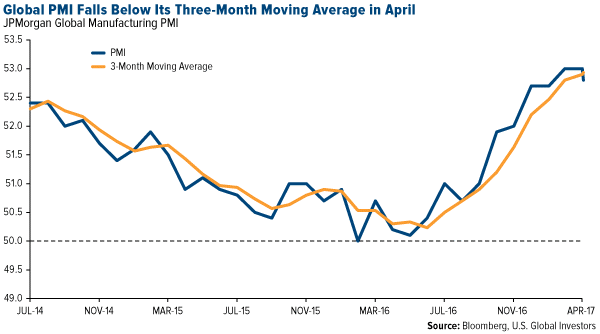

Manufacturing on a global level continued to expand as well but, like the U.S. and China, at a slower pace. The index fell from 53 in March to 52.8 in April, with the one-month reading falling below its three-month moving average for the first time since April of last year.

click to enlarge

Like clockwork, copper and oil were off this week. As I’ve shown a number of times before, the PMI can be used as a forecast tool for commodities and natural resource prices.

On Wednesday copper lost 3.5 percent, marking the largest single-day loss since September 2015. The red metal ended the week at $2.53 a pound. Oil tumbled nearly 5 percent on Thursday to close the trading day at $45.48, a level we haven’t seen since December. On Friday it finished above $46 a barrel.

SALT Conference

Later this month I’ll be in Las Vegas attending the annual SkyBridge Alternatives Conference (SALT), which normally attracts some of the biggest rock stars in the hedge fund and investing world. This year’s speaker lineup includes Ben Bernanke; Jeffrey Gundlach, CEO of DoubleLine; Eric Schmidt, executive chairman of Alphabet; Bill Ackman, CEO of Pershing Square Capital; and many more. It should be a highly enlightening conference, and I’ll likely have a few takeaways to share with you.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.32 percent. The S&P 500 Stock Index rose 0.63 percent, while the Nasdaq Composite climbed 0.88 percent. The Russell 2000 small capitalization index lost 0.25 percent this week.

- The Hang Seng Composite lost 0.94 percent this week; while Taiwan was up 0.28 percent and the KOSPI rose 1.62 percent.

- The 10-year Treasury bond yield rose 7 basis points to 2.35 percent.

Domestic Equity Market

click to enlarge

Strengths

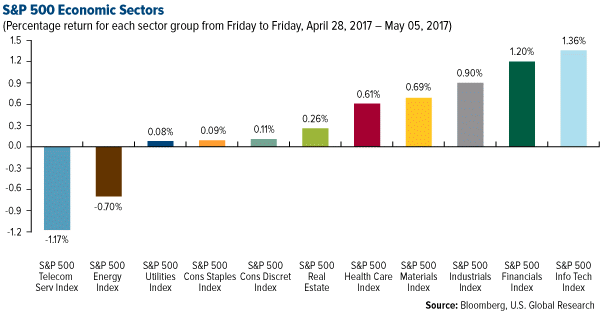

- Information technology was the best performing sector of the week, increasing by 1.36 percent versus an overall increase of 0.60 percent for the S&P 500.

- Regeneron Pharmaceuticals was the best performing stock for the week, increasing 10.43 percent.

- Facebook beat across the board. The social media giant earned $1.04 per share as revenue soared 49 percent to $8.03 billion. Both numbers were well ahead of Wall Street estimates.

Weaknesses

- Telecommunications was the worst performing sector for the week, falling 1.17 percent versus an overall increase of 0.60 percent for the S&P 500.

- Advanced Micro Devices was the worst performing stock for the week, falling 23.38 percent.

- Twilio crashed on guidance. Shares of the cloud communications company crashed 26 percent following Tuesday's closing bell after the company forecast an adjusted full-year loss of $0.27 to $0.30 on revenue of $356 million to $362 million. Both were well shy of expectations.

Opportunities

- Apple has dethroned Exxon as the world's dividend king. Apple is now the world's largest payer of dividends after increasing its quarterly payout by 10.5 percent to 63 cents a share, according to data compiled by Howard Silverblatt, senior index analyst at S&P Dow Jones Indices LLC.

- Weight Watchers posted dynamite earnings. The weight loss company earned $0.16 per share, easily beating the $0.04 that Wall Street was anticipating, and raised its full-year earnings forecast to $1.40 to $1.50 per share from $1.30 to $1.40. Shares gained as much as 11.4 percent in extended-trading on Tuesday.

- Fitbit lost less money than expected. Shares of the wearable device maker gained as much as 14 percent in extended trading on Wednesday after the company announced an adjusted loss of $0.15 during the first quarter, beating the $0.18 loss that Wall Street was anticipating.

Threats

- Etsy tanked after announcing a new CEO, flat earnings and job cuts. Shares fell by as much as 17 percent in after-hours trading on Tuesday, and were down nearly 10 percent early on Wednesday after Etsy announced that it expects to eliminate about 80 jobs, or 8 percent of its workforce.

- Shake Shack same-store sales whiffed. The burger chain said sales at stores open at least a year fell 2.5 percent, missing the 0.2 percent growth that Wall Street analysts were expecting. Shake Shack shares sank more than 7 percent in extended trading on Thursday.

- Traders are loading up on bets against the world's "most levered real estate developer." Short interest in China Evergrande Group is now $726 million, more than double the total at the start of the year, S3 Partners data show.

The Economy and Bond Market

Strengths

- U.S. jobs made a comeback in April, and the unemployment rate dropped to the lowest in a decade. The U.S. economy added 211,000 jobs following an expectedly weak March, and the unemployment rate dropped to 4.4 percent. "Businesses are certainly hiring and there's no sign that we see of any bump in the road in hiring trends," Tony Bedikian, head of global markets for Citizens Bank, told Business Insider.

- U.S. durable goods orders were stronger than expected, coming in at 0.9 percent versus the expected 0.7 percent.

- Europe's economy is doing even better than previously thought. Markit's Composite PMI reading for April came in at 56.8, ahead of the flash reading of 56.7 and up from March's 56.4.

Weaknesses

- Wage growth slowed down and the labor force participation rate ticked down. Wages grew 2.5 percent from the previous year, falling below economists' expectations of 2.7 percent and below the 2.7 percent rate in March. The labor force participation ticked down slightly to 62.9 percent from 63.0 percent in March.

- The downturn in energy prices has claimed another victim. Wyoming lost its top credit rating as it draws down reserves to cope with declining tax collections from its struggling coal industry. S&P Global Ratings lowered the state’s rating to AA+. Wyoming joins Oklahoma and Louisiana among states suffering credit rating cuts this year because of diminished tax collections tied to the energy sector.

- The U.S. ISM Manufacturing survey came in at 54.8, disappointing expectations of 56.5 and below the previous survey’s 57.2.

Opportunities

- Amid all the calls for higher inflation and continued growth in the U.S., Treasury yields have failed to meaningfully rise. Treasuries have remained attractive, keeping yields low, as investors consider a blurry growth picture in the U.S., combined with uncertainty about geopolitics and President Donald Trump's economic agenda. "I think we're more likely to go to Mars before we have a 4 percent-5 percent 10-year Treasury," David Bianco, chief investment strategist for the Americas at Deutsche Asset Management, said in an interview with Business Insider. "I think it stays near or below 3 percent through this cycle."

- The Federal Reserve held rates and said the recent slowdown in growth is likely "transitory." "The Fed’s reaction function has changed significantly from the last two years as it appears to be firmly on a policy normalization track and is not reacting to every piece of high frequency economic data," Roiana Reid of Berenberg Capital Markets said in a note. "It would take a dramatic slowdown in the economy to derail the Fed’s normalization plans."

- Eurozone manufacturing expanded at its fastest pace since 2011. Markit eurozone Manufacturing PMI printed 56.7 in April as output, new orders and employment all grew at their fastest pace in six years. PMI is often a leading indicator of the economy.

Threats

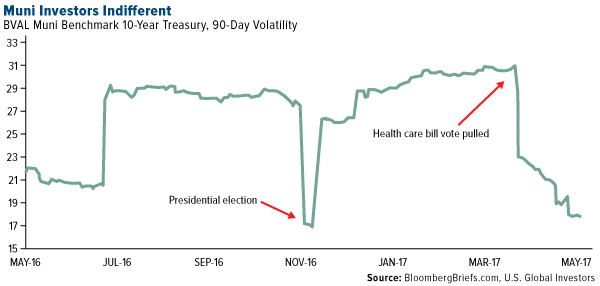

- Investors in state and local debt have weighed in on the president’s first 100 days, and the results suggest they don’t think his agenda is going anywhere soon. By the end of the week, in which the administration announced its new tax plan, trailing 90-day volatility of the benchmark 10-year municipal index fell to its lowest level since Election Day. Municipal bond interest income is exempt from federal taxes, making the bonds sensitive to changes in U.S. tax policy. While investors may believe the likelihood is low that the president’s tax plan will pass through Congress in its current form, they shouldn’t discount its success completely, according to Vikram Rai, head of municipal strategy for Citigroup Global Markets Inc. "Investors are essentially dismissing that the new corporate tax rate would be 15 percent," Rai said in a telephone interview. "The probability that that passes is not zero.” A lower corporate tax rate would likely dampen demand from institutional investors who buy municipal bonds when their tax-adjusted yields make them favorable to other investments, such as taxable investment-grade corporate bonds.

click to enlarge

- Nearly eight years after the recession, the financial recovery for U.S. states is showing signs of sputtering. The credit quality of state governments is deteriorating as spending outpaces “sluggish” growth in tax collections. Revenue growth from income and sales levies was virtually flat last year while some are drawing from their savings and facing pressure to pump more money into retirement plans. At this point in the economic recovery, reserve fund balances should be a lot higher.

- Puerto Rico has finally and officially filed for protection from its creditors in what amounts to the biggest municipal bankruptcy in U.S. history. The commonwealth is asking a federal court to force creditors to take losses on about $74 billion of debt.

Gold Market

This week spot gold closed at $1,221.60, down $46.69 per ounce, or 3.68 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 3.41 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index off just 3.10 percent. The U.S. Trade-Weighted Dollar Index finished the week lower by 0.48 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| May-1 | ISM Manufacturing | 56.5 | 54.8 | 57.2 |

| May-1 | Caixin China PMI Mfg | 51.3 | 503 | 51.2 |

| May-3 | ADP Employment Change | 175k | 177k | 255k |

| May-3 | FOMC Rate Decision (Upper Bound) | 1.00% | 1.00% | 1.00% |

| May-4 | Initial Jobless Claims | 248k | 238k | 257k |

| May-4 | Durable Goods Orders | 0.7% | 0.9% | 0.7% |

| May-5 | Change in Nonfarm Payrolls | 190k | 211k | 79k |

| May-11 | PPI Final Demand YoY | 2.2% | -- | 2.3% |

| May-11 | Initial Jobless Claims | 245k | -- | 238k |

| May-12 | Germany CPI YoY | 2.0% | -- | 2.0% |

| May-12 | U.S. CPI YoY | 2.3% | -- | 2.4% |

Strengths

- The best performing precious metal for the week was palladium, falling just 1.39 percent. Sillwater Mining’s CEO told investors that palladium prices are likely to rise further due to growing demand in China, despite auto sales declining in the U.S. Comments released by the Fed following Wednesday’s meeting, reinforcing the interest-rate hike schedule despite a slowdown in U.S. growth, left gold traders split this week. Bloomberg reports gold traders and analysts are divided on their gold price outlook with seven bullish, six bearish and three neutral. This week gold declined a bit, but Jonathan Barratt, CIO of Ayers Alliance, says these levels represent “fair value.” Similarly, BullionVault’s Gold Investor Index, measuring client buyers against sellers, fell to 52.1 versus 54.2 in March, as prices rallied during the month.

- During the first quarter of the year, China’s demand for gold bars and coins jumped 30 percent year-over-year, reports China Daily. According to the World Gold Council, this is the fourth strongest quarter on record. Overall demand in the Chinese market grew 8 percent year-over-year, making China the world’s top gold consumer. In India, gold imports jumped to the highest level since 2014, with net inbound shipments more than doubling to 270.1 metric tons.

- A Dubai technology company, OneGram, has started the first-ever currency backed by gold in an initial offering, reports Reuters and Bloomberg News, citing CEO Ibrahim Mohammed. “The token called OneGramCoin is considered an Islamic financial product, whose offering is open to all types of investors,” the article continues

Weaknesses

- The worst performing precious metal for the week was silver, trading off 5.02 percent followed closely by gold. Silver and gold fell this week as a tentative deal by U.S. Congress to avert a government shutdown curbed safe-haven demand for the precious metals, reports Bloomberg. Analysts from BOCI believe gold has a “more challenging” outlook moving forward, according to a report this week, citing two more rate hikes and the Fed’s balance sheet unwind. U.S. stocks resumed their advance this week, with optimistic earnings reports pushing the dollar back up and gold lower.

- The Perth Mint released April sales numbers this week, reporting that April gold coin and minted bar sales came in at 10,490 ounces. This is a drop from sales of 22,232 ounces in March. Silver sales also dropped in April to 468,977 ounces from 716, 283 ounces in March.

- Workers at Freeport McMoRan’s Grasberg copper and gold mine in Indonesia started to down their tools at 12am local time, reports Bloomberg. The company’s labor union and PTFI management have yet to agree on labor issues and around 8,000 employees have joined the stoppage. Workers plan to down tools until May 30 to protest job cuts, the article continues.

Opportunities

- DoubleLine Capital’s Jeffrey Gundlach believes that now is “not the time to give up on gold,” reports Bloomberg. In a Tuesday webcast, Gundlach said that gold prices are likely to head higher and also noted his secular bear view on oil prices because of improving fracking technology that cut costs. This week was a bad one for oil as it retreated to a level not seen since OPEC forged its landmark agreement to cut output last November, Bloomberg writes. “With all the shale producers coming online in the States, it’s very much taking the wind out of sails of the uptick we got from the OPEC agreement,” said James Audiss of Shaw and Partners.

- In a press release Wednesday, Red Pine Exploration reported the intersection of visible gold in new drill holes south of its Surluga Deposit. “Visible gold observed in all seven holes drilled in the southern extension of the Minto Mine shear zone,” the release notes. In separate mining news, the Commission of Appointments in the Philippines has voted not to confirm Regina Lopez as Secretary of the Department of Environment and Natural Resources, reports Argonaut. Lopez had taken a hard stance on mining with a view that the sector had negatively impacted the environment and farming communities. Now mine closures are unlikely to proceed. Over to China, gold production in the first quarter saw a significant drop with mined output falling 9.3 percent. One report notes Chinese gold miners have reduced output due to low prices.

- Klondex Mines (KDX CN, KLDX) reported financial results on Thursday after the close with the stock hitting a 52-week low that day. Klondex’s share price has been depressed by a series of events, much of which are unrelated to its operational performance. Back in March the Van Eck Vectors Junior Gold Miners ETF (GDXJ) was supposed to sell its top 3 holdings and reinvest the proceeds into existing holdings, which meant around 10 million shares would be bought by the ETF. However, the GDXJ ETF did not follow the asset mix provided by their index provider because they would have ended up owning 20 percent or more of the shares outstanding for many of their holdings, which would trigger certain Canadian stock exchange rules concerning takeovers. Next Klondex had to delay its operational reporting by one week because the shareholder base shifted to majority U.S. holders which required the company to switch from IFRS accounting to US GAAP. Klondex bought the True North Mine out of receivership and the Hollister acquisition from private owners last year. Although both properties had resources in the measured, indicated, and inferred categories there were no proven and probable reserves. Under SEC rules Klondex had to treat all the capital improvements on both properties as expenses, thus hitting the income statement, and appeared as though the company missed on its earnings. Later in mid-April, the GDXJ announced a new method for re-weighting the stocks it owns by down-weighting the existing holdings, including Klondex, and using the proceeds to buy mid-tier gold producers. The messaging on the Klondex earnings call on Friday was well received. Much of the re-positioning for the upcoming GDXJ rebalancing trade seems to be in the market now and investors now have a timely opportunity to buy Klondex Mines after touching a 52-week low, largely on issues unrelated to the operational performance of the company.

Threats

- Major bulk miners have some of the same issues seen in the gold sector. According to a report from Deutsche Bank, large miners’ “stay-in-business” (SIB) capex could increase 20 percent in 2018. “While total capex will likely remain low near-term ($30 billion in 2017, $90 billion in 2013), we will see sustaining/SIB capex increasing over the medium term as most miners catch up on the underinvestment over the past five years,” the report notes. Bottom-up analysis suggests that while truck fleet replacement will remain low, waste stripping will increase significantly, it continues.

- In November, Steven Mnuchin hinted that the Trump administration would entertain the idea of selling ultra-long bonds, reports Bloomberg, with Wall Street coming to a consensus: Don’t do it! And on Monday, the article continues, Mnuchin provided the clearest signal saying this plan “could absolutely make sense.” Jeffrey Gundlach says that DoubleLine would not buy 100-year Treasuries for its mutual funds should they become available. In fact, he said “It opens the door to burdening our great-grandchildren to a significant degree.”

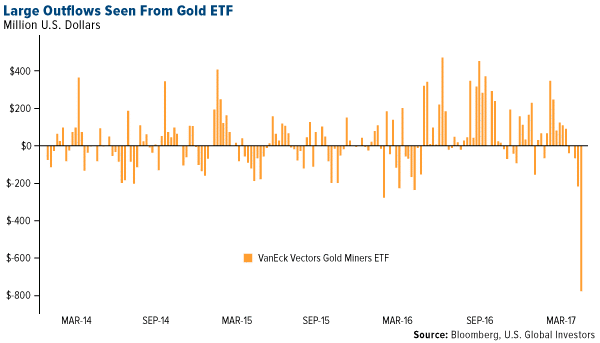

- Investors pulled $778 million dollars from the VanEck Vectors Gold Miners ETF, reports Bloomberg, the largest outflows on record. The withdrawals coincided with the outcome of the first round of the French presidential elections, the article continues. In a similar note, Jeffries reported Monday that large cap ETFs increased their assets by 1.9 percent via inflows of almost $7.4 billion, with small caps increasing assets by 4.8 percent via inflows of over $4 billion. The group also noted outflows across most of its categories being muted, with the biggest being technology and GLD, with about $216 million in withdrawals.

click to enlarge

Energy and Natural Resources Market

Strengths

- Eurozone manufacturing expanded at the fastest pace in six years according to Bloomberg this week. The Purchasing Managers Index (PMI) for the area ticked up to 56.7 for the month of April versus 56.2 for the month of March. Accompanied with a weaker euro, European companies are experiencing improved growth in key export markets and rising domestic demand. Despite political worries that plague the region, economic data is painting a much different picture and a positive one at that, where manufacturing grew in all of the eight countries in the index except for Greece. This is bullish for raw materials from the Eurozone.

click to enlarge

- The best performing sector this week was the S&P Super Composite Construction & Materials Sub Industry Index. The index rose 6.07 percent on the back of a flurry of greater than expected earnings results from index members.

- OCI N.V., a chemical company located in the Netherlands, was the best performing stock this week finishing up 6.51 percent. The stock rose on the back of being upgraded to a buy from analysts on the street as the company has announced that it will terminate negotiations to acquire all publicly held common units.

Weaknesses

- Iron ore was the worst performing commodity this week, dropping 9.17 percent. The commodity experienced greater than normal volatility on the downside this week, dropping to its lowest level in six months as investors became worrisome over China’s growth trajectory as construction and infrastructure demand has slowed down.

- The worst performing sector this week was the S&P/TSX Composite Diversified Metals & Mining Sub Industry Index. The index fell 9.45 percent on the back of falling metal prices around the world as global PMI’s on aggregate have turned down for the month of April.

- The worst performing stock for the week was The Mosaic Company, one of the world’s leading producers of potash located in the U.S. The company fell 12.96 percent due to disappointing earnings results that fell below analysts’ estimates.

Opportunities

- Crude oil fundamentals are beginning to pick up according to a research report by Macquarie Bank this week. Crude oil volatility is back in the spotlight as the commodity fell this week to its lowest levels since late November when OPEC reached an agreement to cut output. However, Macquarie has highlighted that medium-term fundamentals are looking very positive as the global oil market is on track for large deficits. These deficits, primarily in Europe and Asia, of 450,000 to 1 million barrels of oil per day in the third and fourth quarter of this year, will contribute to consistent and large drawdowns in future inventories, which is bullish for crude oil fundamentals.

- Medium-term fundamentals of gold are shaping up according to a research note by Goldman Sachs this week. The shiny metal was hit hard this week, falling from $1,288 an ounce to $1,238 an ounce; however, the bank believes that any significant further pullback in gold may present itself as a potential buying opportunity on the basis of a weak supply growth outlook, high valuations from competing asset classes, and a strong outlook for emerging market dollar savings. All of these factors could potentially support demand growth and a higher price in the medium-term.

- U.S. job gains rebounded this week while unemployment fell to pre-crisis lows according to Bloomberg. For the month of April, U.S. payrolls rebounded by more than their projected forecast, increasing to 211,000 jobs gained while the jobless rate unexpectedly fell by 4.4 percent. This positive jobs report bodes well for raw material demand.

Threats

- Chinese issuance of wealth management products slid 39 percent in the month of April from March, while trust firms distributed 35 percent fewer products, causing liquidity concerns in China according to Bloomberg. The ramifications of this development have led to increased volatility in the base metals complex this week, forcing investors to think twice about China’s growth. Iron ore futures opened limit down in China on Thursday, dropping 8 percent while copper prices approached a four-month low in conjunction with surging stockpiles.

- Massive crops and record storage signals more woes for grain merchants according to an article in Reuters. On Tuesday of this week, Archer Daniels Midland Co warned investors that it was downgrading expected return on invested capital, a key performance metric, by a full percentage point. On Wednesday, Bunge reported an 82 percent drop in first-quarter earnings and lowered its profit outlook. It is evident that agricultural commodities have been hampered over the past couple of months; however, these two giants of grain believe that the current environment may be embarking on a fundamental change where lower profits may become the new normal.

- U.S. and Chinese Purchasing Manager Index’s (PMI) both retreated for the month of April. According to research conducted by Macquarie Bank, global PMIs, which aggregate 15 countries plus the 19 country eurozone, fell 0.5 points month-over-month to 53.4, its lowest level since January of this year. However, the worst performance came from the world’s two largest economies the U.S. and China, which fell by 2.5 percent in the U.S. and 0.8 percent in China. The decline in PMIs indicate potential declines in industrial demand.

China Region

Strengths

- The strongest regional indices this week were Singapore’s Straits Times (Total Return) Index (which rose 2.18 percent to new 52 week highs); similarly, the Philippines Composite Index rose 2.36 percent, to its highest levels since last August.

- Retail sales volume in Hong Kong rose for the first time since July 2015, Bloomberg reports. Expectations were for a 1 percent decline; instead, volume rose an encouraging 2.7 percent.

- Year-over-year exports in South Korea beat expectations, coming in up 24.2 percent, well above last month’s 13.7 percent and ahead of expectations for 17.0 percent.

Weaknesses

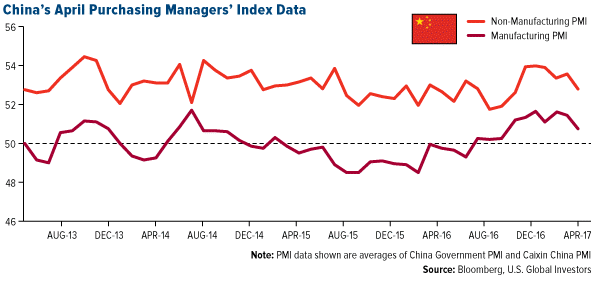

- The week’s weakest-performing regional index was the Shanghai Composite Index, which dropped 1.63 percent.

- That’s not all that dropped in China: monthly April PMI data show the official Manufacturing PMI fell to 51.2 from 51.8, missing expectations for a 51.7 print, while the Caixin China Manufacturing PMI also dropped, from 51.2 to 50.3, missing expectations for a 51.3 print. On the Services/Non-manufacturing side of things, the official Non-manufacturing PMI measurement dropped to 54.0 from 55.1; the Caixin China Services PMI came in at 51.5, down from 52.2. Notably, however, all PMI metrics remained above 50 and thus in expansionary territory.

click to enlarge

- The Nikkei Taiwan Manufacturing PMI fell as well, declining to 54.4 in April from a 56.2 March print.

Opportunities

- Airbus and Boeing, take note: Comac—shorthand for China’s state-owned Commercial Aircraft Corp. of China—this week publicized a successful test flight of its new, single-aisle, twin-engine aircraft, the 158-174 seat model C919, designed to bring eventual competition to the aerospace duopoly that is Airbus and Boeing. Though the C919 is similar in size and scale to an A320 or a 737 Max, it may yet take significant time before large-scale orders start rolling in for the China-designed product, as Comac and the C919 build a safety track record and work through kinks. According to press reports, a minimum of some 15 foreign partners worked on components and systems for the C919, an interesting representation of the globalized world, one in which a China-designed aircraft employed foreign components-makers’ products, parts of which may themselves have been made or produced in China. The Chinese government, Bloomberg reports, has referred to the ability to build and fly a large commercial aircraft as the “flower” or “pearl” of modern manufacturing, a highly desirable—and potentially competitive or even lucrative—venture.

- The Malaysian ringgit, while declining slightly in the back end of the week, continued its gains for the week and for the year, declining from just under 4.49 to present levels near 4.34 in 2017. The Nikkei Malaysia PMI rose to expansionary territory: a 50.7 print, up from March’s contractionary print of 49.5 and climbing above 50 for the first time since early 2015. Exports beat expectations this month, imports beat expectations this month, and the FTSE Bursa Malaysia Kuala Lumpur Composite Index reached new 52 week highs this week.

- Reports allege that China is preparing for a second round of state-owned enterprise (SOE) ownership reforms, with up to 10 companies readying proposals to sell stakes in their respective units and diversify ownership.

Threats

- The United States has advised the Terminal High Altitude Area Defense (THAAD) missile shield is operationally ready and deployed in South Korea, granting the hypothetical ability to intercept incoming missile threats. The THAAD shield remains controversial for relations with China and amid much saber-rattling and tough-talking about North Korea.

- A recent note by Goldman Sachs Asset Management expresses concern about alleged investor complacency about the potential impact of rising funding costs for China’s over-leveraged companies, reports Bloomberg.

- Global yuan use has lost momentum amid China’s capital controls, Fitch Ratings argues and Bloomberg reports. Swift data show global transactions in yuan have dropped to 1.78 percent from a 2015 record of 2.79 percent before the IMF approved the addition of the Chinese currency to the Special Drawing Rights (SDR) basket.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 6 percent. Greek markets are rallying following further agreements between Greece and its international creditors. Moody’s stated that the credit outlook is improving, which could lead to debt relief measures for Greece. Two-year bond yields have dropped below 10-year notes, a sign of investor confidence about the nation’s ability to repay its debts.

- The Hungarian forint was the best performing currency this week, gaining 1.4 percent against the U.S. dollar. March industrial output expanded 9.4 percent year-over-year, the biggest increase since October 2015, suggesting a strong rebound in gross domestic product in the first quarter.

- The financial sector was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing country this week, losing 80 basis points. The annual inflation reading rose to 11.87 percent in April from 11.29 percent in March. April’s PMI, which is a good indicator of economic health, was reported at 51.7 and lower than the prior reading of 52.2.

- The Russian ruble was the worst performing currency this week, losing 2 percent against the U.S. dollar. Brent crude oil fell by 5 percent after the U.S. reported crude output at the highest since August 2015. OPEC will meet May 25 in Vienna to make a decision on extending the 1.2 million barrel-a-day cut agreed to in November for six months.

- The telecommunication service sector was the worst performing sector among eastern European markets this week.

Opportunities

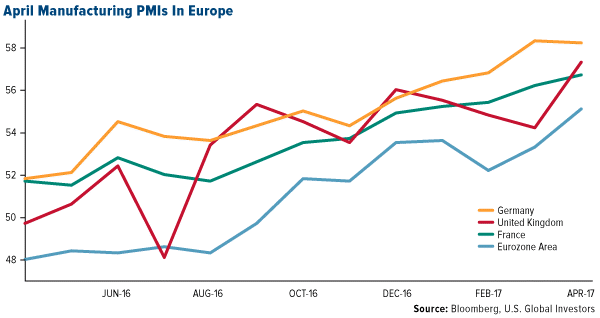

- Europe's economy is doing even better than previously thought, according to the latest PMI data. Markit's PMI reading for the eurozone jumped to 56.7 in April from March's 56.2, reaching its highest level since April 2011.United Kingdom’s PMI registered at 57.3 in April, well above the 54.0 median estimate. Germany reported PMI at 58.2, and France 56.6.

click to enlarge

- Putin and Erdogan, during their meeting in Sochi this week, agreed to lift most trade restrictions put in place after the Turkish air force shot down a Russian warplane near the Syrian border in 2015. The relationship between Turkey and Russia is turning back to normal. Erdogan said that he, and “my friend” Putin, agree on all topics except for the ban of tomato exports, that will remain in place for three to five years.

- Emmanuel Macron looks on course to become France’s next president, ending the threat of a euroskeptic at the Elysee Palace. Marine Le Pen remains 18 points behind Emmanuel Macron with just days to go before the second round of the French election on Sunday, according to one of the biggest final polls.

Threats

- German Chancellor Angela Merkel met with Vladimir Putin at Putin’s summer residence in Sochi this week. Merkel told Putin that sanctions must remain on Russia as two of the world’s most powerful long-serving leaders clashed over Ukraine, Syria and human rights.

- Czech Prime Minister Sobotka announced he is dissolving the government. The reason behind this are some questionable business practices of the Finance Minister Babis, including potential tax evasion and unexplained origin of wealth. This could be a political move ahead of the next parliamentary elections that should take place on October 20 and 21. The coalition parties will now discuss whether to regroup the current coalition and continue until October, or whether to call preliminary elections sooner.

- This week Greece finally agreed with its creditors on a package of reforms needed to unlock its next installment of bailout cash. But according to an article published in the Wall Street Journal by Simon Nixon, Greece won’t receive a cent until the International Monetary Fund is satisfied that there is a credible plan in place to put Greece’s debt on a sustainable footing. Without this, the IMF won’t lend anything to Greece—and without the IMF on board, the German government has said it won’t give Greece any more money either. The IMF and Germany need to agree on a debt relief plan for Greece next.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| DJIA | 21,006.94 | +66.43 | +0.32% |

| S&P 500 | 2,399.29 | +15.09 | +0.63% |

| S&P Energy | 495.45 | -3.50 | -0.70% |

| S&P Basic Materials | 335.48 | +2.31 | +0.69% |

| Nasdaq | 6,100.76 | +53.15 | +0.88% |

| Russell 2000 | 1,397.00 | -3.43 | -0.25% |

| Hang Seng Composite Index | 3,335.68 | -31.76 | -0.94% |

| Korean KOSPI Index | 2,241.24 | +35.80 | +1.62% |

| S&P/TSX Global Gold Index | 201.66 | -6.06 | -2.92% |

| XAU | 80.28 | -2.82 | -3.39% |

| Gold Futures | 1,229.30 | -39.00 | -3.07% |

| Oil Futures | 46.41 | -2.92 | -5.92% |

| Natural Gas Futures | 3.27 | -0.01 | -0.18% |

| SS&P/TSX Venture Index | 781.72 | -25.05 | -3.10% |

| 10-Yr Treasury Bond | 2.35 | +0.07 | +3.02% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| DJIA | 21,006.94 | +358.79 | +1.74% |

| S&P 500 | 2,399.29 | +46.34 | +1.97% |

| S&P Energy | 495.45 | -19.59 | -3.80% |

| S&P Basic Materials | 335.48 | +7.16 | +2.18% |

| Nasdaq | 6,100.76 | +236.28 | +4.03% |

| Russell 2000 | 1,397.00 | +44.85 | +3.32% |

| Hang Seng Composite Index | 3,335.68 | -21.12 | -0.63% |

| Korean KOSPI Index | 2,241.24 | +80.39 | +3.72% |

| S&P/TSX Global Gold Index | 201.66 | -13.67 | -6.35% |

| XAU | 80.28 | -6.07 | -7.03% |

| Gold Futures | 1,229.30 | -19.20 | -1.54% |

| Oil Futures | 46.41 | -4.74 | -9.27% |

| Natural Gas Futures | 3.27 | +0.00 | +0.12% |

| SS&P/TSX Venture Index | 781.72 | -38.58 | -4.70% |

| 10-Yr Treasury Bond | 2.35 | +0.01 | +0.60% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| DJIA | 21,006.94 | +935.48 | +4.66% |

| S&P 500 | 2,399.29 | +101.87 | +4.43% |

| S&P Energy | 495.45 | -42.59 | -7.92% |

| S&P Basic Materials | 335.48 | +8.28 | +2.53% |

| Nasdaq | 6,100.76 | +433.99 | +7.66% |

| Russell 2000 | 1,397.00 | +19.16 | +1.39% |

| Hang Seng Composite Index | 3,335.68 | +178.22 | +5.64% |

| Korean KOSPI Index | 2,241.24 | +168.08 | +8.11% |

| S&P/TSX Global Gold Index | 201.66 | -17.08 | -7.81% |

| XAU | 80.28 | -12.64 | -13.60% |

| Gold Futures | 1,229.30 | +5.40 | +0.44% |

| Oil Futures | 46.41 | -7.42 | -13.78% |

| Natural Gas Futures | 3.27 | +0.21 | +6.76% |

| SS&P/TSX Venture Index | 781.72 | -37.56 | -4.58% |

| 10-Yr Treasury Bond | 2.35 | -0.12 | -4.70% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investHoldings may change daily.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of 03/31/2017:

Boeing

Exxon

Klondex Mines Ltd

Red Pine Exploration Inc.

SPDR Gold Shares (GLD)

SPDR Gold Shares ETF (GLD)

Van Eck Vectors Junior Gold Miners ETF (GDXJ)

VanEck Vectors Gold Miners ETF (GDX)

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

A basis point, or bp, is a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01% (0.0001).

The National Federation of Independent Business’s (NFIB) Index of business optimism is based on responses from 1221 member firms.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time.

The BVAL Muni Benchmark 10T is the baseline curve for BVAL tax-exempt munis. It is populated with high quality US municipal bonds with an average rating of AAA from Moody’s and S&P.

The ISM manufacturing composite index is a diffusion index calculated from five of the eight sub-components of a monthly survey of purchasing managers at roughly 300 manufacturing firms from 21 industries in all 50 states.

The Straits Times Index is a modified market capitalization-weighted index comprised of the most heavily weighted and active stocks traded on the Stock Exchange of Singapore.

The Philippine Stock Exchange PSEi Index is composed of stocks representative of the industrial, properties, services, holding firms, financial and mining & oil sectors of the Philippines Stock Exchange.

The Shanghai Composite Index (SSE) is an index of all stocks that trade on the Shanghai Stock Exchange.

The Caixin China Manufacturing PMI is based on data compiled from monthly replies to questionnaires sent to purchasing executives in over 400 private manufacturing sector companies. The Caixin China Services PMI is based on data compiled from monthly replies to questionnaires sent to purchasing executives in over 400 private sector service companies.

The Kuala Lumpur Stock Exchange Composite Index (KLCI) is a broad-based capitalization-weighted index of 100 stocks designed to measure the performance of the Kuala Lumpur Stock Exchange.

The S&P Supercomposite Construction Materials Index is a capitalization-weighted index. The index is comprised of the stocks in the construction materials sub-industry.

The S&P/TSX Composite Diversified Metals & Mining Sub Industry Index is a subset of the constituents of the S&P/TSX Composite Index.

Return on Capital (or return on invested capital) is a calculation used to assess a company’s efficiency at allocating the capital under its control to profitable investments.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All