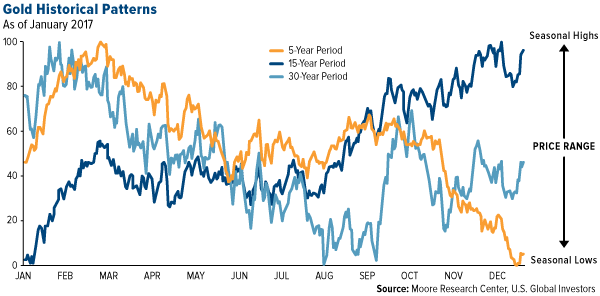

Here at the outset, I want to share with you an interesting observation we made this week of gold’s seasonal trading pattern. As you can see in the chart below, based on data provided by Moore Research Center, the five-year pattern, represented by the orange line, is diverging from the longer-term trends. Note that the index on the left measures the greatest tendency for the asset to make a seasonal high (100) or low (0) at a given time.

The data show that lows are now reached late in the year, not in January (according to the 15-year period, represented by the dark blue line) or August (according to the 30-year pattern, represented by the light blue line). Historically, September has seen the highest returns on gold as Indians make huge purchases in preparation for Diwali and the fourth-quarter wedding season, but lately we’ve seen changes. When we calculate the average monthly returns of the past five years, from January 2012 to December 2016, we find that January is the strongest month, returning 5.3 percent, following by August with 2.3 percent. September actually returns negative 1.3 percent.

There could be a number of reasons why this is, but it’s important to recognize that the five-year period captures the bear market that dragged gold from its high of $1,900 an ounce in August 2011 to a recent low of $1,050 in December 2015. The years 2013, 2014 and 2015 all saw negative returns, so it’s little wonder why the orange line trends down from February-March to December.

Inflation Props Up Gold

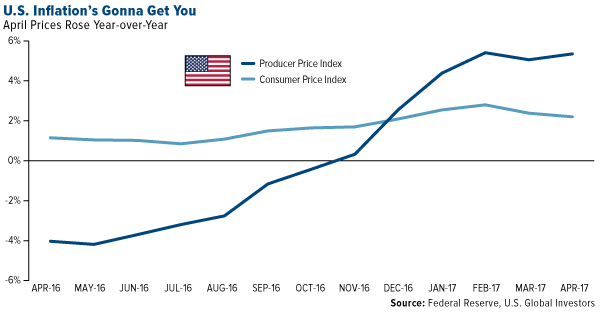

Consumer and producer prices rose in April compared to the same time last year, favoring gold prices going forward. Consumer goods climbed 2.2 percent, down slightly from March’s 2.4 percent. Wholesale goods, meanwhile, flew up 5.3 percent, higher than economists’ expectations and the strongest year-over-year increase in nearly six years.

On numerous occasions I’ve shown that higher inflation supports demand for gold, which has often been seen as a safe haven investment. The money you have sitting in the bank right now is guaranteed to lose value over time. The five-year Treasury bond is currently yielding a negative return. Diversiying a part of your portfolio into gold and gold stocks could help mitigate the effects of inflation on your household wealth. I’ve always recommended a 10 percent weighting with annual rebalances.

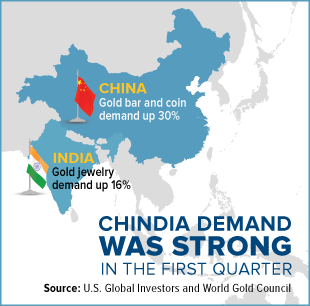

Chindia Demand Was Strong in the First Quarter

|

In India, no one questions this. Aside from property, gold is seen as the most reliable store of value, which is why it’s routinely given as a gift during weddings, graduations, births and other important life events.

Indians’ demand for gold jewelry jumped 16 percent year-over-year in the first quarter, according to the World Gold Council (WGC), as the country slowly recovers from the economic shock of Prime Minister Narendra Modi’s demonetization scheme in November.

Demand in China for gold bars and coins had an unusually strong start to the year, fueled by concerns over a weakening renminbi and uncertainty over the country’s real estate market. The first quarter has historically been a good time for Chinese demand, as that’s when the Lunar New Year falls. This year, though, demand was up an amazing 30 percent, with 105.9 metric tons (tonnes) purchased during the three-month period. According to the WGC, this was the fourth-strongest quarter on record.

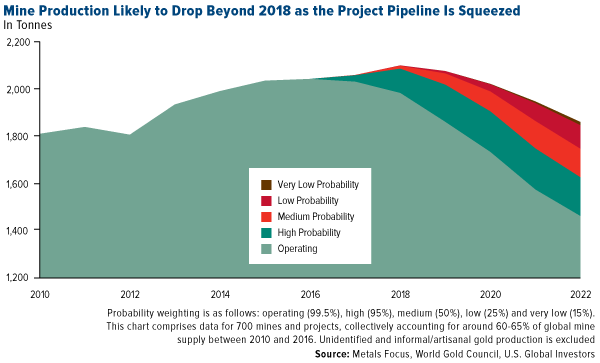

Looking ahead, gold prices could be supported by steadily declining mine production. Over the next five to 10 years, output from currently-operational mines is expected to drop off steeply as a consequence of deep spending cuts for project development as well as a lack of significant new deposit discoveries.

Between 2012 and 2016, capital expenditure for companies in the NYSE Arca Gold BUGS Index contracted 65 percent, the WGC reports. This will inevitably squeeze the supply chain and help prices firm up.

Stock Investors Have No Fear

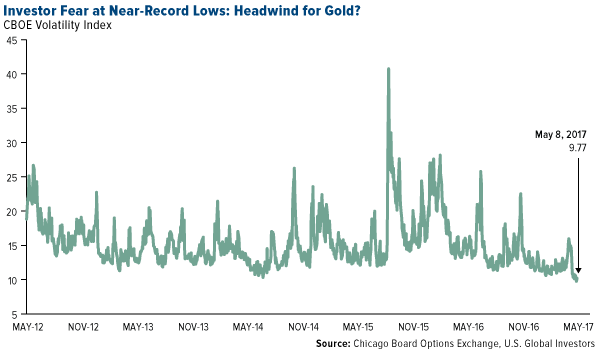

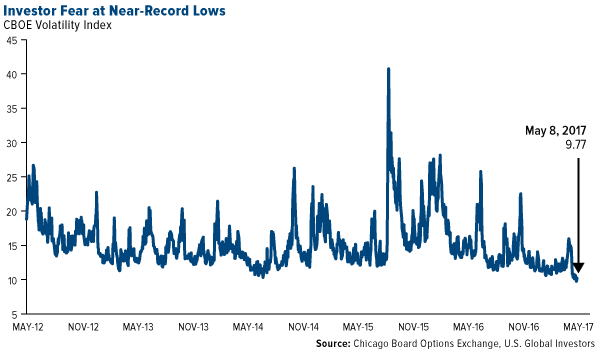

In the near term, gold faces a number of headwinds, including a strong U.S. dollar, rising nominal interest rates and a still-robust stock market. Despite recent geopolitical shockwaves such as President Donald Trump’s firing of FBI director James Comey, investors still see stocks as a good place to be, with the CBOE Volatility Index, or VIX, trading at lows last seen in 1993.

Popularly known as the “fear gauge,” the VIX measures expected volatility in the S&P 500 Index over the next month. That it’s trading so low suggests that geopolitical uncertainty doesn’t always translate into investor uncertainty. Evidently Wall Street doesn’t share the same sense of impending doom as some voters and media figures appear to have right now concerning Comey’s termination and the ongoing investigation into possible collusion between the Trump campaign and the Russian government.

This matters because gold has historically benefited in times of crisis and uncertainty, whether real or perceived. But with the VIX signaling near-record-low fear in the marketplace, some investors might see this as weakening the case for gold.

Where We See the Gold Opportunities

In this environment, we seek high-quality producers that are profitable and show improvements in revenue and cash flow. This yields junior companies such as Klondex and Wesdome, both of which have demonstrated strong fundamentals, low SG&A (selling, general and administrative expenses), cost-conscientious management and higher-grade ore.

The recent bubble in gold stocks unwound, which was harmful to some quality gold names that were affected by the issues involving the VanEck Vectors Junior Gold Miners ETF (GDXJ), which I wrote about last week. Since the GDXJ methodology update was announced, the ETF has recorded large redemptions, with assets plunging as much as 25 percent.

The GDXJ doesn’t have any smart beta attributes—instead, it relies on market cap. As portfolio manager Ralph Aldis put it, this means “we find a lot of high-quality companies being indiscriminately sold down.” We see this as an opportunity to nibble at some attractive small-cap growth names.

A Brief Comment on Ontario’s Runaway Debt

Net debt of my home province, Ontario, has been steadily expanding for years. In 2016, it actually crossed above $300 billion for the first time ever—and this is for a province of only around 14 million people, which is a little more than Pennsylvania.

|

Led by Premiere Kathleen Wynne of the socialist Liberal Party since 2013, Ontario is addicted to social spending, and its just-released 2017 budget is no exception. Free prescription drugs will now be provided for everyone aged 24 years and under. And for the first time, a guaranteed basic income, with no strings attached, will be handed out every month to people between 18 and 64 who earn less than a given amount. These programs are implemented with admirable motives, but they’re unsustainable.

To be fair, I should point out that Ontario’s 2017 budget is the first in 10 years to be “balanced.” But that doesn’t mean debt is going down any time soon. By the end of the decade, debt is projected to reach $335 billion, or about 40 percent of province GDP. Writing for the Toronto Sun, columnist James Wallace called Wynne’s undisciplined spending glut a “selfish burden on future generations.” I couldn’t agree more. As things stand now, each Ontarian owes more than $22,000 on principal alone, before interest.

We’ve seen it in Venezuela, Chicago and elsewhere—out-of-control socialism weakens economic growth and enslaves taxpayers. I’m sorry to see this happen to the great province I grew up in and still visit multiple times a year.

To show you the difference between that and a truly well-managed jurisdiction, I made the table below comparing Ontario to my present home state of Texas. It’s like night and day!

| Ontario | Texas | |

|---|---|---|

| Population, in Millions | 14 | 27.5 |

| GDP, in Trillions | $0.798 | $1.639 |

| Net Debt, in Billions | $317.9 | $49.8 |

| Debt as Percentage of GDP | 40.2% | 2.65% |

| Net Debt Per Person | $22,738 | $1,810 |

| Source: Fraser Institute, Texas Public Policy Foundation, U.S. Global Investors | ||

Happy Mother’s Day!

This Mother’s Day weekend, consumers are expected to spend a record $23.6 billion, up from $21.4 billion last year, according to the National Retail Federation (NRF). Most of the spending will be on jewelry ($5 billion), special outings ($4.2 billion) and flowers ($2.6 billion).

However you plan on celebrating the special mom(s) in your life—whether it’s your own mom, a wife, sister or daughter—make it count. It’s crucial we show gratitude to those charged with the most important task in our society. Have a blessed weekend!

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.53 percent. The S&P 500 Stock Index fell 0.35 percent, while the Nasdaq Composite climbed 0.34 percent. The Russell 2000 small capitalization index lost 1.02 percent this week.

- The Hang Seng Composite gained 2.59 percent this week; while Taiwan was up 0.88 percent and the KOSPI rose 2.00 percent.

- The 10-year Treasury bond yield rose 3 basis points to 2.325 percent.

Domestic Equity Market

Strengths

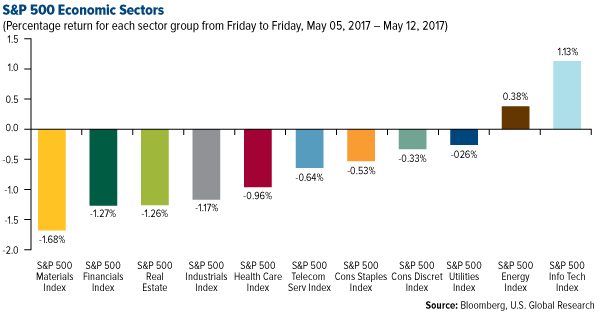

- Information technology was the best performing sector of the week, increasing by 1.13 percent versus an overall decrease of 0.43 percent for the S&P 500.

- Nvidia was the best performing stock for the week, increasing 23.14 percent.

- Nvidia spiked after its earnings beat. Shares of Nvidia spiked by more than 14 percent in extended trading Tuesday after the company reported that first-quarter revenue surged by 48.4 percent versus a year ago.

Weaknesses

- Materials was the worst performing sector for the week, falling 1.68 percent versus an overall decrease of 0.43 percent for the S&P 500.

- Macy’s was the worst performing stock for the week, falling 18.50 percent.

- Snap cratered after its first earnings report. Shares of the social-media company tumbled by as much as 25 percent following its first quarterly report as a publicly traded company. Snap lost $0.20 a share on revenue of $149.6 million. Both numbers missed Wall Street estimates.

Opportunities

- U.S. President Donald Trump has signed an executive order aimed at upgrading government cyber-defenses, Reuters reports. It builds on efforts undertaken by the Obama administration. This could be a boon to cybersecurity companies.

- With a new controller, Microsoft has taken a big shot at Facebook and Sony in the race for cheap virtual reality. It is teaming up with Acer to create a $399 virtual reality bundle. Additionally, Microsoft also has an ambitious new plan to take on Amazon's Alexa and Google Assistant. It is launching smart speakers that come with its AI assistant, Cortana, built in.

- Apple invested $200 million in a company that helped make the first iPhone. Apple's Advanced Manufacturing Fund has invested in Corning.

Threats

- Jeff Gundlach doesn't like U.S. stocks. Speaking at the Sohn Investment conference, Gundlach, the founder of DoubleLine Capital, told attendees to go long the iShares Emerging Markets ETF and short the S&P 500.

- Nordstrom's same-store sales missed. The high-end department store said comparable sales slipped 0.8 percent versus a year ago, missing the flat reading Wall Street was anticipating. All the major brick and mortar retailers have disappointed and are feeling the heat from Amazon.

- Disney sees continued weakness at ESPN. Operating income from Disney's cable networks fell by 3 percent versus a year ago to $1.8 billion. "The decrease in operating income was due to a decrease at ESPN, partially offset by increases at the Disney Channels and Freeform," Disney said.

The Economy and Bond Market

Strengths

- The University of Michigan preliminary index of consumer confidence rose to 97.7 in May (forecast was 97) from 97 in April.

- From the end of 2014, a fairly pedestrian 1.9 percent growth rate has been enough to make the euro area the world's top-performing major economy, bettering the U.S., U.K. and Japan. Moreover, growth in the eurozone is now "solid and broad," meaning that it includes all countries. The European Central Bank’s (ECB) dispersion index of value-added growth in different countries stands at a historical minimum.

- The April retail sales report points to some rebound in real consumer spending from the first quarter’s meager 0.3 percent increase. Total retail sales grew by 0.4 percent month-over-month.

Weaknesses

- Bloomberg’s U.S. Weekly Consumer Comfort Index came in at 49.7, below the previous week’s 50.9.

- U.S. import prices rose 0.5 percent in April, versus 0.2 percent expected increase. Prices increased more than expected in April amid rising costs for petroleum products and a range of other goods.

- U.S. worker productivity unexpectedly fell in the first quarter, leading to a jump in labor-related costs. Nonfarm productivity, which measures hourly output per worker, decreased at a 0.6 percent annualized rate. That was the weakest in a year.

Opportunities

- The lack of concern among U.S. equity investors can be seen in the CBOE Volatility Index, or VIX, a 30-day barometer of investor nervousness calculated using multiple S&P 500 options. The so-called fear gauge slipped last week to its lowest level since February 2007. Such a low reading is generally viewed as a bullish signal. Why such a muted response given recent major geopolitical developments? U.S. investors are simply focusing on other, more relevant market drivers — and they like what they see, according to Credit Suisse. "The principal macro factors reining in S&P short-dated implied volatility are a weaker U.S. dollar and better than expected corporate earnings," Credit Suisse derivatives strategist Mandy Xu wrote in a client note. It's been a blockbuster earnings season, which is helping drive bullishness. Results so far are showing that S&P 500 earnings grew by 13 percent in the first quarter, the index's fastest year-over-year growth since the third quarter of 2011, according to Goldman Sachs data. Further, about 50 percent of firms have beaten earnings forecasts, above the long-term average of 46 percent. Further, 41 percent of companies have exceeded revenue estimates, the most positive ratio of surprises in almost six years, according to the Goldman data.

- It will be a fairly quiet week in the U.S. on the data front. The Empire State Manufacturing Index on Monday, and Philly Federal Index on Thursday will provide a first look at the economy in May. The April Leading Economic Indicators survey on Thursday should point to firmer GDP growth ahead from the dismal performance in the first quarter.

- Emmanuel Macron won the French election. The centrist Macron defeated far-right candidate Marine Le Pen, winning 66.06 percent of the vote to her 33.94 percent, in Sunday's presidential election, according to the French Interior Ministry. "I know the divisions in our nation, which led some to vote for extremist parties," Macron said in a victory speech at his campaign headquarters. I respect them. I will work to recreate the link between Europe and its peoples, between Europe and citizens."

Threats

- Warren Buffett and Bill Gates don't think Trump's tax cut will help business. In an interview with CNBC on Monday, both Gates and Buffett downplayed the benefits of Trump's proposed tax cut for businesses and said the promised higher growth from the cut was overplayed.

- Jamie Dimon is sounding the alarm. The chairman and CEO of JPMorgan Chase has taken the opportunity on a number of occasions in recent weeks to highlight problems in America, including its failing education system, stifling bureaucracy, and high levels of incarceration and opioid deaths.

- According to BCA, emerging market currencies will depreciate more than their carry over the next 6-12 months. Thus, investors in local currency emerging market bonds should consider hedging the foreign exchange risk.

Gold Market

This week spot gold closed at $1,228.38, up $6.78 per ounce, or 0.56 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 5.72 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index climbed just 1.52 percent. The U.S. Trade-Weighted Dollar Index finished the week up 0.54 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| May-11 |

PPI Final Demand YoY |

2.2% | 2.5% | 2.3% |

| May-11 |

Initial Jobless Claims |

245k | 236k | 238k |

| May-12 |

Germany CPI YoY |

2.0% | 2.0% | 2.0% |

| May-12 |

U.S. CPI YoY |

2.3% | 2.2% | 2.4% |

| May-14 |

China Retail Sales YoY |

10.8% | -- | 10.9% |

| May-16 |

Germany ZEW Survey Current Situation |

80.2 | -- | 80.1 |

| May-16 |

Germany ZEW Survey Expectations |

22.0 | -- | 19.5 |

| May-16 |

U.S. Housing Starts |

1260k | -- | 1215k |

| May-17 |

U.S. CPI Core YoY |

1.2% | -- | 1.2% |

| May-18 |

Initial Jobless Claims |

240k | -- | 236k |

Strengths

- The best performing precious metal for the week was nearly a tie with platinum up 0.85 percent and silver with a gain of 0.70 percent, as gold, silver and platinum began to find support towards the close of the week. A Bloomberg survey this week shows that traders are split on their outlook for gold prices, with six bullish and four bearish.

- Gold demand is rising in the world’s two biggest gold markets, India and China. In India, gold imports increased more than four-fold in April, reports Bloomberg, to 98.3 metric tons compared to 22.2 tons a year earlier, in anticipation of the wedding season. Meanwhile in China, gold demand may rise to the highest level in four years in 2017. Consumption could surpass 1,000 metric tons compared to 975 tons last year, driven by slowing property prices and tensions with North Korea.

- Bank of China International led a $29 million capital raise for an online trading platform, G-banker. G-banker allows users to buy, sell, deposit and withdraw gold on its digital platform and mobile app.

Weaknesses

- The worst performing precious metal for the week was palladium, off 1.05 percent as hedge funds cut their bullish bets the over the week. Gold is near an eight-week low amid comments from Federal Reserve Bank of Boston president Eric Rosengren. Rosengren warns that the economy may be overheating, and is calling for three more interest rate hikes this year.

- BMI has cut its gold price forecast for 2017 to $1,250 per ounce. The firm sees lower demand for gold because of Emmanuel Macron’s win in the French presidential election, moderation in foreign policy rhetoric from the Trump administration, and weaker economic growth in China.

- Investor Jim Rogers says that markets everywhere will start to correct this year, and says that he won’t buy more gold until it drops below $1,000. Rogers says that the equity markets will weaken after being strong for the past 12 months, and he expects the dollar to strengthen “no matter what Trump says.”

Opportunities

- Gold open interest, the outstanding contracts on Comex futures, fell for a 10th straight session, the longest stretch since October 5, 2011. This a positive in that we may be coming to a near-term bottom with the reduced longs allowing room for positioning to build again. U.S. government data shows that consumer prices excluding food and energy were up 1.9 percent in April, the least since 2015. The relatively low inflation rate “suggests the Fed has less impetus to be aggressive in the way they remove monetary accommodation,” says Bart Melek of TD Securities. Also Joni Teves of UBS says, “we expect bargain-hunting to emerge and physical buying to strengthen should the market test $1,200/oz, paving the way for a recovery.”

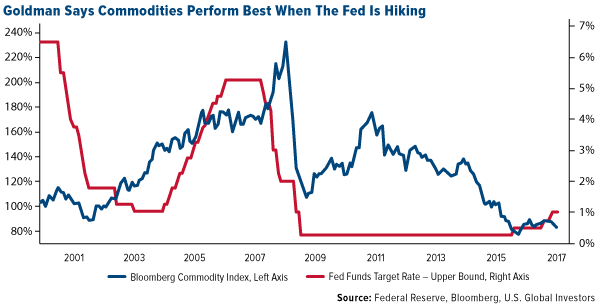

- A Goldman Sachs study concludes that it might be time to invest in commodities, during the rate hike cycle. The authors note that interest rate hiking cycles can be quantitatively measured, unlike economic cycles which require more qualitative judgement. The results of the study show that commodities outperformed during four separate rate hiking periods since 1988. During these periods, commodities were nearly double the performance of the stock market.

- Argentina Mining Secretary Daniel Meilan says that a mining accord between federal and provincial legislation is expected by the end of the year. The new standardized set of rules will be signed by provincial governors and President Mauricio Macri in the next couple of months, and then be subject to congressional approval. The new code would be a positive development for mining companies in working in Argentina.

Threats

- Bond traders are expecting the Fed to raise rates at its June meeting, placing odds of a hike at 80 percent. They are also seeing a September hike as more likely. However, looking at all 34 historical rate hikes since 1990, none occurred when five indicators were down. The five indicators, which are down this year, are crude oil prices, Treasury yields, and ratios of copper versus gold, industrial versus precious metals, and broad commodities versus Treasury prices.

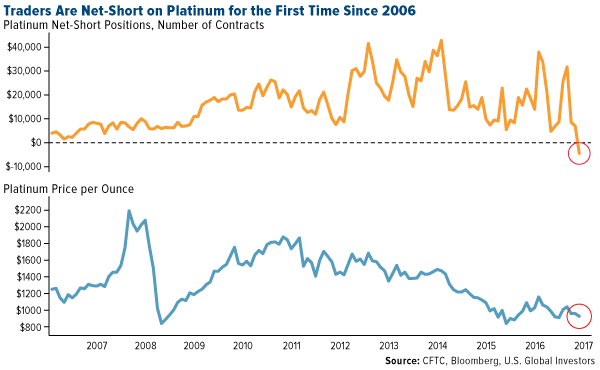

- For the first time since 2006, hedge funds and other speculators are net-short platinum. The platinum price is down 15 percent in the past 12 months, largely due to poor demand for diesel vehicles.

- Moody’s Investors Service downgraded six large Canadian banks, due to concerns about consumer debt and high housing prices. Bloomberg also reports that “A run on deposits at alternative mortgage lender Home Capital Group Inc. has sparked concern over a broader slowdown in the nation’s real estate market.” In addition, hedge funds and other speculators increased their short positions to the highest level on record in the Canadian dollar, which is the worst-performing major currency this year.

Energy and Natural Resources Market

Strengths

- Gasoline was the best performing commodity this week, rallying 4.7 percent. Gasoline prices rallied on the back of a remarkable draw posting their largest one-week drop in nearly six years, dropping 6.6 million barrels according to the Energy Information Administration (EIA) owing to strong nationwide demand in the U.S. and reduced refining output along the East Coast. This marks six consecutive weeks of falling inventory for gasoline inventories and the seventh consecutive week for distillate inventories. If the drawdowns continue in the weeks ahead, the rally in gasoline prices may gain further momentum.

- The best performing sector this week was the S&P/TSX Composite Gold Sub Industry Index. The index rose 6.1 percent on the back of political uncertainty in the U.S. which has sent investors in search of safe haven investments like gold and the Japanese yen.

- Petrobras, an energy giant located in Brazil, was the best performing stock this week, finishing up 9.5 percent. The stock rose on the back of posting its largest profit in two years.

Weaknesses

- Iron ore was the worst performing commodity this week, dropping 7.1 percent. The commodity fell to six- month lows as prices in China crashed through key levels of support on the back of concerns surrounding mine supply rising further as Chinese mills enter into a weaker period of demand and policy makers attempt to reduce leverage throughout the financial system of the country.

- The worst performing sector this week was the S&P Super Composite Steel Sub Industry Index. The index fell 5.2 percent due to falling iron ore prices and worries surrounding oversupply of the commodity.

- The worst performing stock for the week was ArcelorMittal, the largest producer of steel located in Luxembourg. The company fell 8.3 percent because of uncertainty surrounding future growth despite reporting first quarter profit that more than doubled.

Opportunities

- Goldman Sachs says Fed rate hikes and commodity gains come hand-in-hand, in according to an article in Bloomberg this week. The bank’s highly respected commodities research team conducted a research study crunching data going back to 1988, covering four hiking cycles and found that during periods of rising interest rates, raw material returns strongly surpass both equity and bond returns. This makes sense, as the Fed raises interest rates in order to cool down an economy that is beginning to show signs of overheating. As strong demand, rising wages and price inflation pick up, a rally in commodity prices might be around the corner.

- Weak oil prices create gas opportunities, according to Martin Alder, head of oil and gas at SNC-Lavalin, in an article by Reuters this week. As crude oil prices have been hit hard over the past couple of years, many oil and gas projects have been put on hold in the market downturn; however, bullish liquefied natural gas (LNG) demand growth forecasts have undermined the attractiveness of the sector in the long term. The International Energy Agency (IEA) sees LNG making up more than half of the world’s trade by 2040, up from 25 percent in 2000, as a result of favorable economics of projects and the fundamentals of the commodity. These conditions would be positive for long-term natural gas fundamentals.

- British economist Jim O’Neill, best known for coining the term BRIC, says China fears are “completely overblown,” according to Bloomberg this week. He stated in the article that China’s economy shows no signs of crisis as the country crackdowns on financial leverage. He believes, that this is completely overblown as China has demonstrated multiple times that it is very good at dealing with its cyclical challenges as its burgeoning middle class increasingly fuels growth through a wide array of services, which now account for more than half of output and consumption. These factors bode well for raw materials from one of the world’s largest consumers.

Threats

- OPEC faces a tough challenge in reducing oil inventory overhang according to the Financial Times. Higher than expected production from the U.S. and countries outside of OPEC is offsetting curbs from some of the world’s biggest producers, ultimately keeping global oil inventories persistently high and putting additional pressure on prices. OPEC’s latest monthly forecast has revised production growth upwards by 58 percent to almost 1 million additional barrels from countries outside of the cartel. This is negative for global oil markets.

- Freeport-McMoRan fights for the future of its flagship Grasberg mine, according to the Financial Times. Freeport-McMoRan is locked in a dispute with the government of Indonesia over its contract to operate in the country and has six months to turn out a deal to assure the future of the Grasberg mine, the second largest copper deposit in the world. The dispute originally led to a ban on copper exports from the mine for almost four months which hurt the company’s bottom line; however, the next six months may be pivotal to the long-term health of the company.

- Commodity trader Cargill expects a grain glut to last a long time according to Reuters this week. Bumper crops have created overstock in many inventories, dragging down prices for grains and damaging profits at grain traders including Cargill, Bunge Ltd, Archer Daniels Midland and Louis Dreyfus Co. Dave MacLennan, CEO of Cargill, has stated there are plenty of supplies in storage and Brazilian farmers are holding on to their products in hopes better prices but doesn’t see a clearing of the excess supply anytime soon.

China Region

Strengths

- The Hang Seng Composite Index rose 2.61 percent for the week, climbing to new 52-week closing highs.

- China’s April New Yuan Loans and Aggregate Financing both came in ahead of expectations. New Yuan Loans came in at 1.1 trillion, well above expectations of 815 billion, while Aggregate Financing came in at 1.390 trillion, ahead of expectations for 1.150 billion.

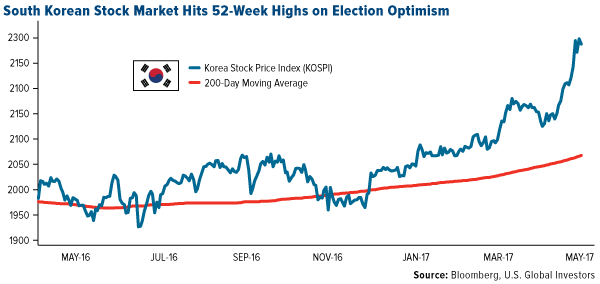

- South Korea concluded its presidential election this week, with liberal Moon Jae- cruising to an anticipated victory. The Korea Composite Stock Price Index (KOSPI), meanwhile, also cruised to new 52-week highs, rising 2 percent since trading last week in won terms and more than 3 percent in USD terms.

Weaknesses

- The Stock Exchange of Thailand (SET) Index declined 1.45 percent for the week, among the worst performers in the region in that time frame.

- China’s April Imports and Exports both came in softer than expected. Imports missed, with year-over-year gains of 11.9 percent—below expectations for an 18.0 percent gain—while year-over-year Exports rose 8.0 percent, shy of expectations for an 11.3 percent gain.

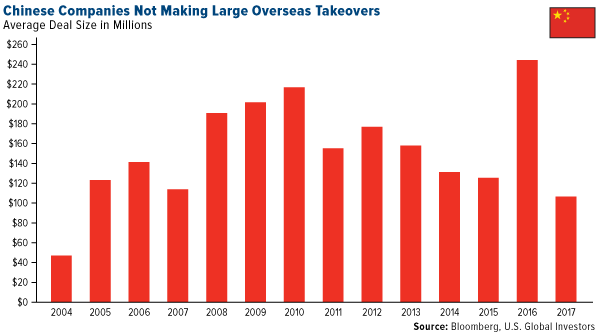

- While there is indeed some reason to consider the dramatically slower pace of outbound Chinese investment in 2017 (especially relative to a record-setting 2016) as a concern, there may be a silver lining in that aborted outbound merger and acquisition (M&A) and capital control restrictions may have served, at least short-term, to bolster the yuan, as has more stability in the FX reserve levels of late. China’s April print for its FX reserve levels came in at 3.0295 trillion, ahead of expectations for a 3.0200 trillion print.

Opportunities

- China’s first annual One Belt, One Road Forum will kick off this weekend. Beijing will host numerous world leaders to discuss President Xi Jinping’s global infrastructure buildout plan, designed to export domestic Chinese overcapacity—while simultaneously projecting soft power and building trade ties. The perceived contrast, real or not, between China’s global outreach with an “America First” policy is duly noted in media sources.

- Friday, the U.S. and China announced a trade agreement aimed at promoting “market access for American natural gas, financial services and beef,” as Bloomberg News reports, while the U.S. will allow the import of cooked poultry from China. To paraphrase U.S. Commerce Secretary Wilbur Ross, this—the Trump administration’s first negotiated trade pact—provides an opportunity to serve as a mutually beneficial platform for further negotiations on other topics in the future.

- Last week Hong Kong and Chinese regulators announced that they will formally unveil details of a program to connect foreign investors with China’s bond market by July, with expected go-live date of sometime this fall, according to Reuters.

Threats

- China’s Shanghai Composite Index has diverged significantly from a number of its fellow indices around the Asia Pacific region, as some investors fear deleveraging effects and domestic slowdowns from a better-than-expected first quarter GDP. Credit Suisse lowered its twelve-month A-share forecast slightly this week, even as the Shanghai Composite made new 2017 lows in the same timeframe.

- As South Korea’s newly-inaugurated President Moon takes the helm in Seoul, North Korea remains a hot topic within the region, as is the THAAD missile defense system—to which Mr. Moon is opposed.

- U.S. interest rate policy could continue to hold outsized significance for the broader region.

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 4.8 percent. Budapest’s stock exchange rallied after MOL, the Hungarian oil and gas company, and OTP Bank reported strong first quarter results. Shares of MOL appreciated 8 percent and OTP Bank gained 7 percent.

- The Russian ruble was the best performing currency this week, gaining 1.7 percent against the dollar. The ruble usually strengthens before and during the tax-payment deadlines as companies buy rubles to pay taxes. Profit tax estimated at 220 billion rubles is due on May 29, and individual income tax estimated at 460 billion rubles is due May 15. Also, the ruble was supported by the strengthening oil price. Brent crude oil closed above $50 per barrel on Friday, gaining 3.6 percent in the past five days.

- The utilities sector was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 40 basis points. Shares of Sistema, a large Russian conglomerate company, and Mobile TeleSystems, the telecommunication company owned by Sistema, continued their descent. Russian oil company Rosneft filed a lawsuit against Sistema last week for $1.9 billion, which is equivalent to about 66 percent of the company market capitalization.

- Turkey was the worst performing currency this week, losing 70 basis points against the dollar. Turkish authorities detained 57 former Istanbul stock exchange employees, accusing them of using the encrypted messaging app, ByLock. The government says ByLock has ties to the Gulen movement, which was responsible for last’s year failed coup.

- The real estate sector was the worst performing sector among eastern European markets this week.

Opportunities

- Emanuel Macron’s victory in France has reduced political tension in Europe and showed that Europe has resisted the populist political tide. Macron now may focus on renewing France’s relationship with Germany; to have the two biggest economies in the eurozone moving in tandem would be a powerful force.

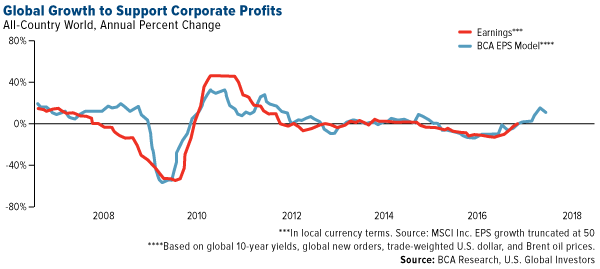

- BCA’s Daily Insights publication stated that above-trend global economic growth is helping to propel corporate earnings, pointing to particularly strong growth in the euro area. BCA's global earnings model predicts further upside for profits over the coming months.

- On Wednesday, President Donald Trump met with Russian Foreign Minister Sergei Lavrov in the White House. According to Lavrov, Russian election interference and sanctions were not discussed, but they talked about the efforts by Russia, Turkey and Iran to set up “de-escalation zones” in Syria and the ongoing violence in Ukraine. During the meeting Trump emphasized his hope for better relations between the U.S. and the Kremlin.

Threats

- Russian consumer spending on everyday items fell by 6.5 percent in April compared with the previous month, and by 4.9 percent from the same period last year, a survey published on Thursday showed, a reverse of the positive trend seen in March. The data for April, compiled by research firm Romir, cast doubt over the pace of the recovery in the Russian economy where consumer demand remains the main growth driver.

- President Trump had approved arming Kurdish forces in Syria despite objections from Turkey. A Pentagon spokesman said that the Syrian Democratic Forces, which included the Kurdish militia YPG, “are the only force on the ground that can successfully seize Raqqa in the near future.” Trump will host Turkish President Recep Erdogan at the White House on Monday, May 16, and Erdogan may relay his concern over the U.S. decision to arm Syrian Kurdish fighters.

- In the Czech Republic, the government hangs in uneasy balance as a face-off between Prime Minister Sobotka (head of CSSD party) on one side and Finance Minister Babis (head of ANO party), who appears to be supported by President Milos Zeman. Zeman’s office stated that he will decide on the resignation of the current cabinet upon his return from China on May 18. Cabinet reshuffles are not uncommon in Czech, but the market may react negatively in a short term.

© US Global Investors