Hedge Fund Managers Pour SALT on U.S. Stocks, Look to Europe

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Europe is back on the map. That was one of the main takeaways this week from the SkyBridge Alternatives (SALT) hedge fund conference in Las Vegas, where $3 trillion in assets was represented. Speaker after speaker touted European equities for their attractive valuations and as a means to diversify away from the volatile American market in light of rising U.S. geopolitical risk. France’s election of centrist Emmanuel Macron over far-right nationalist Marine Le Pen this month has especially eased investors’ fears that antiestablishment forces would challenge the integrity of the European Union (EU).

Economic growth is finally picking up in Europe—“solid and broad,” as European Central Bank (ECB) president Mario Draghi recently put it—and many countries’ purchasing managers’ indexes (PMIs) are at five- and six-year highs. Export orders and hiring have accelerated. Labor participation is improving. European commodity sectors, including energy and metals, look cheap and oversold, meaning it might be time to start accumulating.

Trading at around 17 times earnings, European companies are priced to move compared to American firms, which are trading at 22 times earnings.

|

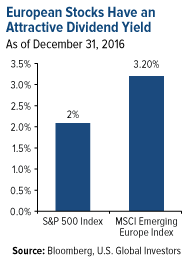

Dividend yields also look attractive relative to U.S. stocks. The MSCI Emerging Europe Index, which is most heavily weighted in Russian, Polish and Turkish stocks, currently yields 3.2 percent. The S&P 500 Index, by comparison, yields 2 percent.

A recent Barron’s article, “Europe on Sale: Time to Buy Foreign Stocks,” makes the same bullish case as many of the SALT presenters. Its author, Vito J. Racanelli, suggests that the eight-year bull run in the U.S. could be coming to an end, and that the baton is being passed to Europe. Overseas markets have already attracted more fund flows so far this year than the U.S. market, with a whopping $6.1 billion being plowed into European equity funds in the week ended May 10.

“Given attractive valuations, diminished political risk, low interest rates and a pickup in global growth, international markets, and Europe in particular, could finally start to outperform,” Racanelli writes.

Talking Geopolitics

Before moving on, I want to share a few other takeaways from SALT. One of the highlights was hearing billionaire investor Dan Loeb, who manages the $16 billion hedge fund firm Third Point. Loeb said that serious investors should closely monitor geopolitics as a backdrop or overlay when making investment decisions because government policy can have the fastest and most significant impact on your portfolio.

|

That was flattering to hear. Not only do I spend a lot of time discussing and analyzing geopolitics, both here in the weekly commentary and my CEO blog Frank Talk, but it’s baked right into U.S. Global Investors’ methodology: Our investment process clearly asserts that “government policy is a precursor to change.” Loeb’s comments, I felt, validated our emphasis on geopolitics.

Many conferences I attend can often get bogged down in partisan politics, but SALT was refreshingly balanced. Joe Biden was as welcome on-stage as Jeb Bush. No one came out entirely in favor of or against President Donald Trump or his policies. Instead, presenters discussed the inherent risks and opportunities in an intelligent, even-handed manner. I aspire to do the same.

One of the speakers was John Brennan, the former CIA director, who’s scheduled to testify before the House Intelligence Committee later this month as part of its investigation into Russia’s alleged involvement with the 2016 election. Brennan, who told lawmakers as far back ago as August that the agency had information pointing to possible collusion between Russia and the Trump campaign, shed some much-needed light on allegations that Trump shared sensitive intelligence with Russian officials this month—a “serious mistake,” he said—explaining that such leaks to the media are potentially just as damaging to national security as the president’s actions.

Also notable was former Federal Reserve Chair Ben Bernanke’s thoughts on Washington’s little-known power dynamics. He said there are really three parties jockeying for control in the capital—Republicans, Democrats… and the “beltway party.” It’s this last group, composed of deeply entrenched lobbyists and career bureaucrats, that gives Washington outsiders such as Trump the hardest time and actively tries to sabotage agendas that shake up the status quo.

|

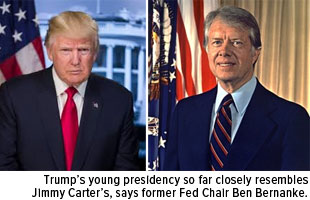

In this regard, Bernanke said, the presidency Trump’s tenure so far resembles the most is not Richard Nixon’s, as some have suggested. It’s not even Andrew Jackson’s, which Trump himself expressly would like to emulate. Instead, it’s Jimmy Carter’s.

This might seem counterintuitive, but think about it: Both men were Washington outsiders. Both men arrived in the beltway with aspirations to transform the capital’s insular culture and “drain the swamp.” Both men had the great fortune of working with a party majority in both chambers of Congress. But because they exuded an “I alone” attitude and often picked fights with members of their own party, both men faced unusual difficulties in getting key components of their agendas passed. And just as Carter had little success in his first 100 days—in his entire four-year term, in fact—Trump’s young presidency has similarly been unable to make significant strides so far in getting much accomplished.

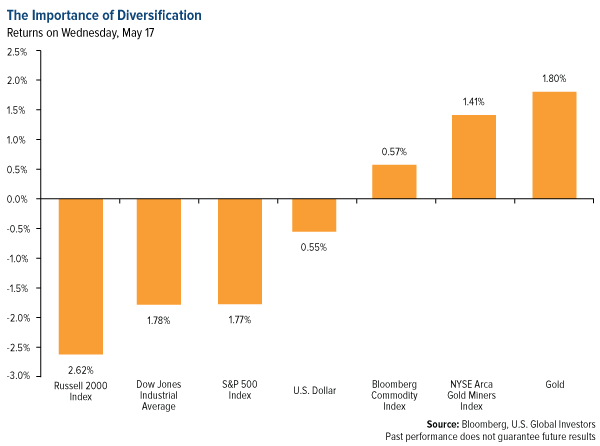

This is precisely what markets were reacting to on Wednesday, the worst week for major U.S. indices in months. Investors, fearing Trump’s pro-growth agenda could be threatened by troubling news and allegations coming out of the White House, punished small-cap stocks in particular, sending the Russell 2000 Index down 2.62 percent, its sharpest one-day loss since March. Recall that it was small caps that saw the strongest surge following the election, as investors bet on domestic growth stemming from the then-president-elect’s “American first” proposals.

Now, however, some are wondering if Trump, embroiled in numerous scandals, will finish out his term. A few SALT presenters even uttered the “i” word. Jim Chanos, founder and investment manager of Kynikos Associates in New York, told the packed auditorium that he believes the market hopes Vice President Mike Pence will become president. Investors are seeking deregulation and tax cuts, plain and simple, Chanos said, and the “more stable” Pence is seen as having a better shot at delivering. This squares with reports from British gambling and betting company Ladbrokes, which announced this week that Trump is now odds-on, or highly likely, to face impeachment by the end of his first term, with bookies having to cut the price from 11/10 to 4/5.

Banks, which stand to benefit from Trump’s plan to loosen financial regulations, were Wednesday’s biggest losers. JPMorgan was down 3.81 percent, or $3.34 a share. Goldman Sachs fell 5.27 percent, or $11.88 a share.

Apple finished the day down 3.36 percent, wiping away some $20 billion in market value. The smartphone giant, which recently became the first company ever to be worth more than $800 billion, could also benefit from Treasury Secretary Steven Mnuchin’s efforts to make it easier for multinationals to repatriate cash that’s held overseas. And if that describes any company today, it would be Apple: The iPhone-maker holds nearly $250 billion in cash and securities in offshore accounts.

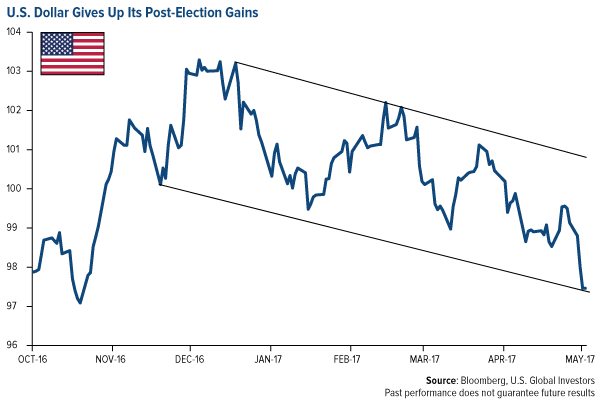

Dollar Weakness Gives a Boost to Gold

More so than equities, the U.S. dollar is highly sensitive to geopolitical drama. This week, the greenback tumbled to its lowest level since the November election compared to other major currencies.

This helped gold, miners and commodities end the week in positive territory. Gold gained 2 percent, gold miners 0.57 percent and commodities 1.36 percent. The S&P 500, meanwhile, finished the week down 0.8 percent.

For diversification benefits, I always recommend around a 10 percent weighting in gold and gold stocks, and this week proved yet again that this strategy could help mitigate the losses in risk assets.

Unsure what else drives the price of gold? Find out!

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.44 percent. The S&P 500 Stock Index fell 0.38 percent, while the Nasdaq Composite fell 0.61 percent. The Russell 2000 small capitalization index lost 1.12 percent this week.

- The Hang Seng rose 0.12 percent this week; while Taiwan was down 0.39 percent and the KOSPI rose 0.11percent.

- The 10-year Treasury bond yield fell 9 basis points to 2.23 percent.

Domestic Equity Market

Strengths

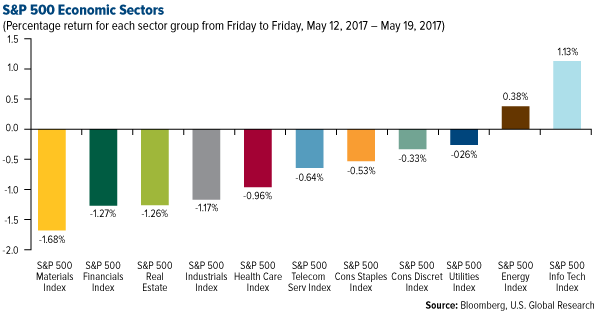

- Real estate was the best performing sector for the week, increasing by 1.23 percent versus an overall decrease of 0.45 percent for the S&P 500.

- Autodesk was the best performing stock for the week, increasing 15.22 percent.

- Salesforce beat across the board and raised its outlook. The company earned an adjusted $0.28 a share on revenue of $2.39 billion and raised its full-year GAAP earnings per share (EPS) to a range of $0.06 to $0.08 on sales of $10.25 billion to $10.3 billion.

Weaknesses

- Financials was the worst performing sector for the week, falling 1.01 percent versus an overall decrease of 0.45 percent for the S&P 500.

- Foot Locker was the worst performing stock for the week, falling 21.58 percent.

- The S&P 500 closed down by 1.7 percent on Wednesday, making for its biggest drop in eight months, after reports surfaced that President Donald Trump in February had asked James Comey to end the FBI's investigation into former national security adviser Michael Flynn. Trump fired Comey as FBI Director last week. The selling spilled over into Asia, where Japan's Nikkei (down1.3 percent) paced the decline, and then Europe, where Britain's FTSE (down 1.3 percent) led the losses.

Opportunities

- The Trump administration gave Wall Street some great news. Testifying in front of the Senate banking committee on Thursday, Treasury Secretary Steven Mnuchin said the Trump administration did not support the separation of investment banks and commercial banks.

- Gap continues to fend off the retail apocalypse. The retailer beat on both the top and bottom lines and said same-store sales climbed by 2 percent, well ahead of the 0.2 percent contraction that Wall Street was anticipating.

- Walmart beat on earnings as online sales surge. America's largest brick-and-mortar retailer said gross merchandise volume in its e-commerce unit — the value of everything sold online — jumped by 69 percent compared with the same period last year. This validates its recent push into the e-commerce space in order to compete with Amazon.

Threats

- Apparently, talk of a potential impeachment of Trump — after his reported strong-arming and then firing of FBI Director, James Comey — has gotten investors' attention. To be clear, it's not that investors are necessarily taking an impeachment as likely, it is that the challenge to Trump's political power has reached a level that means his economic agenda is off the rails.

- Since the election, the sectors of the U.S. stock market most closely linked to President Donald Trump's proposed economic policies have shown remarkable resilience. Until now. No area of the so-called Trump trade has been hit harder than banks. An index tracking the sector, which had been seen as benefiting from Trump's call for looser regulatory oversight, slipped by 3.5 percent on Wednesday, headed for its biggest drop in almost two months. Companies that pay the most taxes also incurred the wrath of stock traders. Viewed as best positioned to benefit from a tax cut, the high-tax group lost 1.2 percent on Wednesday, the largest single-day decline since March 21. Industrial companies were also unable to escape unscathed, falling by 1.4 percent, also the biggest drop since late March. Boosted by expectations of $1 trillion in infrastructure spending, the sector was the second-best performer in the months following the election, trailing only financials.

- Elon Musk admitted that Tesla's stock is out of control. "I do believe this market cap is higher than we have any right to deserve," he said in an interview with The Guardian, pointing out his company produces just 1 percent of GM’s total output. "We’re a money losing company," Musk said. Additionally, a major Tesla bull downgraded the stock to "equal weight" from "overweight." Morgan Stanley's lead auto analyst, Adam Jonas, said he thought Tesla would struggle to deliver its Model 3 mass-market vehicle in 2017.

The Economy and Bond Market

Strengths

- U.S. homebuilder sentiment was stronger than expected. The National Association of Homebuilders' Index rose to 70 from 68, and its gauge of future sales conditions hit its highest level since June 2005.

- U.S. industrial production for April grew 1 percent month-over-month, more than the 0.4 percent growth expected by economists.

- Japan logged its longest stretch of growth in over a decade. The Japanese economy grew at a 0.5 percent clip in the first quarter, making for the fifth consecutive quarterly increase. That hasn't happened since 2006.

Weaknesses

- U.S. new housing construction unexpectedly declined in April. Housing starts fell 2.6 percent to a seasonally adjusted annual rate of 1.17 million units, the Commerce Department said. Some of the drop in starts, especially in the Northeast, could be weather-related after a snowstorm in March.

- The U.S. Leading Index for April came in at 0.3 percent, below the expected 0.4 percent.

- China's industrial production slowed. Data released by China's National Bureau of Statistics showed that industrial production grew by 6.5 percent year-over-year in April. That was below both March's 7.6 percent print and the 7.1 percent that economists had forecast.

Opportunities

- The German Ifo and euro-area flash PMIs for May will be released on Tuesday. These should provide a timely update on the European economy. Recent PMIs have been pointing to strong GDP growth.

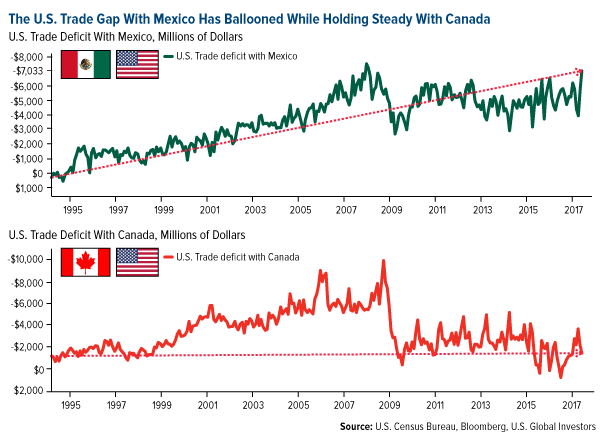

- President Donald Trump’s administration took its first formal step toward renegotiating the North American Free Trade Agreement, setting the stage for talks that could influence more than $1.2 trillion in annual trade and shake up corporate supply chains. U.S. Trade Representative Robert Lighthizer gave official notice to Congress on Thursday of the government’s intention to renegotiate the 23-year-old accord with Mexico and Canada. Over the next 90 days, Lighthizer will consult with lawmakers on the position the U.S. will take in negotiations, which could begin as early as August 16. The U.S. administration hopes to wrap up negotiations this year before a final deal is presented to Congress for approval. The administration has made reducing the trade deficit a priority, and Lighthizer suggested Thursday the U.S. will seek to lure back firms that have moved production to Mexico. The U.S. had a $62-billion trade deficit with Mexico last year.

- A bipartisan group of senators is moving ahead with their own infrastructure spending bill as Congress awaits details from the White House about President Trump’s rebuilding proposal. The new legislative effort would leverage money from the private sector through a newly created investment bank to help upgrade U.S. infrastructure.

Threats

- U.S. first quarter GDP revisions and April durables goods orders are scheduled for Friday. Any disappointment in these items would cast doubt on the Federal Reserve’s ability to raise rates in June, especially in light of the latest political and market turmoil.

- A new Hoover Institution report on public pensions, found that as of 2015, governments’ reported unfunded liabilities were $1.38 trillion under recently implemented governmental accounting standards. However, using market valuation techniques, the true unfunded liability owed to workers based on their current service and salaries would be $3.85 trillion.

- Connecticut was downgraded for the third time in less than a week, after plummeting income-tax collections opened a wider budget deficit, forcing the governor and legislature to redraw spending plans. S&P Global Ratings lowered the state’s general obligation bond rating to A+ from AA-. Both Moody’s and Fitch lowered the state’s rating to the same level in the last five days.

Gold Market

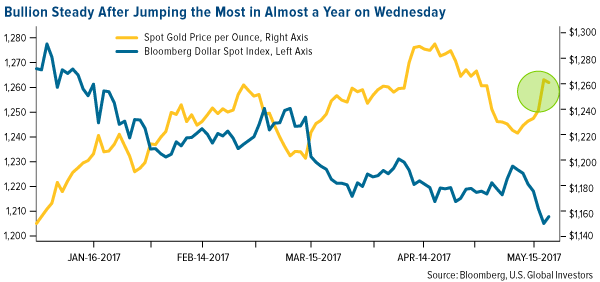

This week spot gold closed at $1,255.65, up $27.52 per ounce, or 2.24 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by just 0.75 percent in what was disappointing performance relative to the move in gold. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index climbed 1.67 percent. The U.S. Trade-Weighted Dollar Index finished the week down 2.16 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| May-14 | China Retail Sales YoY | 10.8% | 10.7% | 10.9% |

| May-16 | Germany ZEW Survey Current Situation | 80.2 | 83.9 | 80.1 |

| May-16 | Germany ZEW Survey Expectations | 22.0 | 20.6 | 19.5 |

| May-16 | U.S. Housing Starts | 1260k | 1172k | 1203k |

| May-17 | U.S. CPI Core YoY | 1.2% | 1.2% | 1.2% |

| May-18 | Initial Jobless Claims | 240k | 232k | 236k |

| May-23 | U.S. New Home Sales | 620k | -- | 621k |

| May-25 | Hong Kong Export YoY | 11.0% | -- | 16.9% |

| May-25 | Initial Jobless Claims | -- | 238k | 232k |

| May-26 | U.S. GDP Annualized QoQ | 0.9% | -- | 0.7% |

| May-26 | U.S. Durable Goods Orders | -1.5% | -- | 0.9% |

Strengths

- The best performing precious metal for the week was silver, climbing 2.36 percent and just beating out gold’s price performance as softer economic data emerged.

- Gold traders and analysts are split on their outlook for gold, reports Bloomberg, with 12 bearish, three bullish and four neutral this week. On May 16 the yellow metal advanced for a fourth day, with Kotak Commodities Services saying gold is supported by “mixed U.S. economic data, weakness in the U.S. dollar, geopolitical tensions and uncertainty about Trump’s policy actions.” On the prior Friday, consumer prices (excluding food and energy) rose 1.9 percent year-over-year for April, the least since 2015, while retail sales were also weaker, reports Bloomberg.

- Eldorado Gold will “gain an operating foothold in its own country with a deal to take full control of Integra Gold Corp,” reports Bloomberg, offering the equivalent of C$1.2125 for each Integra share. That is a 52 percent premium to Integra’s closing price on May 12, according to a statement on Monday from Eldorado. The proposed acquisition provides Eldorado with its first operating mine in Canada, offering G&A and income tax benefits, along with exposure to a lower political risk project, notes a Viii Capital report.

Weaknesses

- The worst performing metal for the week was palladium, down 5.87 percent. UBS noted that electric cars will be brought to the market sooner than consensus expectations and that platinum group metals are expected to lose market demand on this technology adoption.

- Barrick Gold reached an agreement with the Dominican Republic government (where it operates its Pueblo Viejo mine), outlining new financial terms and tax rates, reports Bloomberg. The new terms show the government is projected to receive an additional $181 million from Barrick between 2017 and 2019, according to a statement from the Dominican President’s office. The new terms are based on a gold price of $1,275 per ounce.

- Sibanye Gold Ltd. announced it will sell around $1 billion of shares at a 60-percent discount to partly fund its purchase of Stillwater Mining. The statement soon sent the stock plummeting the most in five months before rebounding after, reports Bloomberg. “The South African miner dropped as much as 11 percent in Johannesburg, the most since December 9, before paring losses to trade 2.4 percent lower,” the article continues.

- Frankfurt-based Commerzbank AG is exiting its physical precious-metals trading and services business, reports Bloomberg. The bank’s physical services include trading of physical precious metals, refining services, vaulting and transportation. Commerzbank does plan to continue its other bullion banking operations.

Opportunities

- Author and investor Mark Faber says that for the first time in a long time he is more heavily weighted in Europe than in the U.S. Faber cites “good opportunities in European stocks” at the present time along with his belief that the euro will continue to strengthen against the dollar. In a Bloomberg phone interview, he continues by stating, “In my opinion in the U.S. they will launch QE4 at the end of the year. The economy in the U.S. is weakening.” He also noted that gold mining shares are “inexpensive” and Amazon is “expensive.”

- Since President Trump’s comments about the dollar being “too strong” back in April, the greenback has since dropped – the Bloomberg Dollar Spot Index has fallen 3.1 percent, reports Bloomberg. Citigroup, the world’s biggest currency trading firm, believes continued erosions for policy changes in D.C. will only lead to further weakening of the currency, the article continues. Even Westpac Banking Corp., the second most-accurate currency forecaster in Bloomberg’s recent rankings, is advising clients to sell the dollar, with Macquarie Bank expecting the greenback to decline as well. Gold traded near a two-week high this week, with equities in retreat “and in

- Bullion markets are staging a tentative recovery, reports Bloomberg, with the number of holes drilled at gold deposits steadily rising for more than a year, according to S&P Global Market Intelligence. For example, exploration has jumped around 50 percent in parts of Argentina for lithium mainly, but also for gold. “When prices fell, exploration budgets were slashed, which means the industry had limited scope to grow,” said Goldcorp CEO David Garofalo. In a similar note from Bloomberg, mining companies lured back to Ecuador after a ban on large projects was overturned, “will welcome news that the incumbent mining minister is set to continue in the role under President-elect Lenin Moreno.”

Threats

- Despite the world’s largest gold-mining companies posting their best profit margins in four years, the biggest ETF linked to producers (the VanEck Vectors Gold Miners ETF) has seen net withdrawals this month of $617 million, reports Bloomberg. During 2016, investors poured record amounts into the ETF, but now it seems the gold rally has faded, with prices lower by 10 percent from 2016 highs. “Some companies are finding it more difficult to tighten their belts further, diminishing prospects for increased cash flow,” the article continues.

- Staff was evacuated and production was suspended at one of the two Banro Corp. gold mines in eastern Democratic Republic of Congo on Thursday, reports Bloomberg. A gunman left three people dead, making this the fourth assault on the company’s operations in eight months. Namoya is the company’s second mine in eastern Congo, beginning production back in January of 2016.

- Acacia Mining will start its three-year process of closing down its Buzwagi mine in Tanzania, reports Bloomberg. According to an emailed statement from the company’s communication manager, the mine will be shut down by 2020, leading to as many as 100 job cuts. At current gold prices, Acacia is not able to increase the life of the mine past the year 2020. Back in March, the Tanzanian government issued a ban on concentrate exports that Acacia said cost the company over $1M a day.

Energy and Natural Resources Market

Strengths

- Iron ore was the best performing commodity this week, rallying 7.4 percent. According to a research note released by Credit Suisse, analysts believe that this rebound may be sustained in the months ahead on the back of solid demand coming from Chinese infrastructure projects, record iron ore consumption, and a positive backdrop from the macro environment. A positive read-through for iron ore prices.

- The best performing sector this week was the FTSE 350 Index. The index rose 6 percent on the back of rallying iron ore and base metal prices which helped lift index members such as Rio Tinto, Glencore, and BHP Billiton.

- OCI NV, a producer and distributor of natural gas-based fertilizers and industrial chemicals based in the Netherlands, was the best performing stock this week, finishing up 17.2 percent. The stock rose on the back of positive investor sentiment and rallying natural gas prices.

Weaknesses

- Lumber was the worst performing commodity this week dropping 3.14 percent. The commodity fell to its lowest level in two months as Canada and the U.S. proved unlikely to strike a deal on a dispute over lumber exports by the time talks of renewing NAFTA start in mid-August, reports Reuters. A negative read-through for lumber prices.

- The worst performing sector this week was the S&P Super Composite Paper & Forest Products Industry Index. The index fell 3 percent on the back of falling lumber prices.

- The worst performing stock for the week was Petrobras, one of the largest energy companies in the world located in Brazil. The company fell 12.4 percent on the back of negative news surrounding the company’s corporate governance this week.

Opportunities

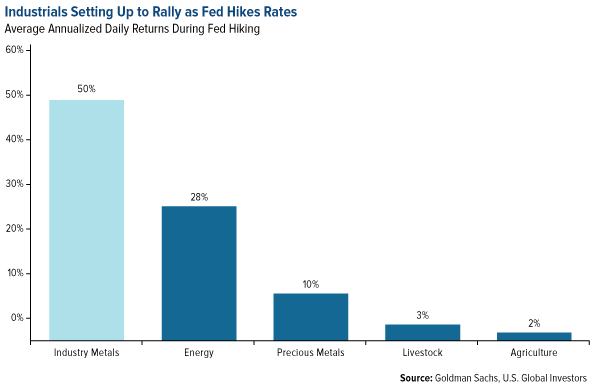

- Industrial metals outperform other metals and commodities during Fed rate hikes, according to a research note released by Goldman Sachs. In the piece, the bank highlights that when the level of output is high, otherwise known as the expansion phase in the business cycle, commodities perform best. Industrial metals take center stage of findings in the research piece as these metals tend to have the highest correlation with economic cycles due to their use cases for economic growth and expansion, returning on average 50 percent during these phases while precious metals return on average only 10 percent. A positive read-through for industrial metals as the Fed enters a hiking cycle.

- Russia and Saudi Arabia back the extension of oil output cuts by pledging to do “whatever it takes” to reduce global stockpiles, according to the Financial Times. Saudi Arabia (the world’s largest exporter of oil) and Russia (the largest producer) have been forced into the driver seat to take further action on global oil markets after prices erased all of their gains since the output deal originally came into effect in January of this year. Both nations have emphasized that they are committed to stabilizing the oil market, reducing volatility, and ensuring the balance of supply and demand are met in both the near- and long-term. A positive read-through for global oil markets.

- China jitters are unlikely to trigger another commodity price rout, according to Glencore in an article by the Financial Times. Ivan Glasenberg, CEO of the commodity giant, stated at an industry conference in Barcelona this week that Beijing’s new emphasis on financial stability would not lead to a repeat of the extreme weakness that was seen in 2015, when mining companies were forced to fight for survival while frantically slashing debt. In addition, he stated that infrastructure contractor order data indicates positive demand momentum in Asia through the rest of 2017. A positive read-through from one of the largest commodity traders in the world.

Threats

- China has flipped from bull driver of metals pricing to bear drive, according to Reuters. As divergence continues in the metals complex, the demand side of the fundamental equation has put China in the spotlight. Having been caught by the strength of policy stimulus last year, industrial metals are now responding negatively to the tightening in policy (where the country has become net sellers instead of net buyers in recent months). Until infrastructure demand picks up steam, this dynamic will continue to put pressure on global metal pricing.

- Political tension in Indonesia and the Philippines continues to keep the price of nickel volatile, according to the Financial Times. After banning nickel ore exports in January 2014 to encourage domestic investment, the government reversed its actions at the start of this year forcing prices to tumble with no action in sight of when policies may change. Wood Mackenzie, a global leader in commodities research, forecasts that prices will remain low for the rest of the year and into 2018. At current levels, about 25 to 30 percent of global nickel production will operate at a loss. A negative read-through for nickel and nickel miners.

- U.S. mortgage applications tumbled the most since 2016 according to weak housing starts and permits data on Tuesday. Mortgage applications fell by 4.1 percent while purchases fell by 2.7 percent. As housing is a key input to raw material demand, this is a negative development.

Strengths

- Indonesia’s Jakarta Composite Index soared to new record highs this week, finishing up 2.12 percent in the last five trading days. S&P raised Indonesia’s credit rating to investment grade, in line with the other two major ratings agencies.

- Malaysia’s first quarter year-over-year GDP beat expectations, coming in up 5.6 percent and well ahead of estimates for a gain of only 4.8 percent. Quarter-over-quarter GDP came in up 1.8 percent, ahead of expectations for a gain of only 1.2 percent.

- Late last week Hong Kong released its first-quarter GDP, which came in up 4.3 percent year-over-year, well ahead of expectations for a gain of only 3.2 percent.

Weaknesses

- Singapore’s Straits Times Total Return Index declined 1.12 percent for the week, among the worst performers in the region in that time frame.

- China’s year-over-year retail sales, FAI, and industrial production all came in weaker than expected at 10.7, 8.9 and 6.5 percent, respectively (and behind respective estimates of 10.8, 9.1 and 7.0).

- China’s April auto sales declined 1.8 percent year-over-year, the lowest level since mid-2015.

Opportunities

- China’s inaugural One Belt, One Road conference in Beijing earlier this week concluded with pledges from China for some 78 billion dollars in financing as well as closing statements from President Xi Jinping on the benefits of multilateral trade as a force for peace in a globalized world. Earlier this week the Chinese authorities also formally announced the creation of a bond link between Hong Kong and the Chinese mainland, designed to give foreign investors an opportunity to purchase onshore securities.

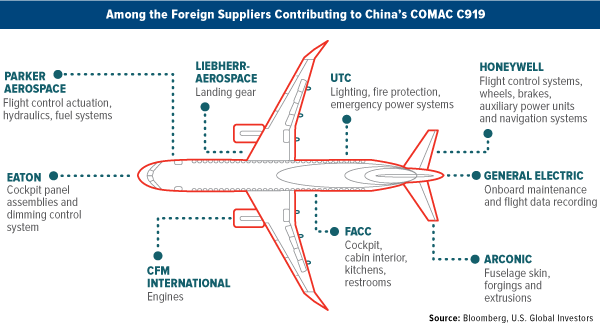

- As mentioned previously, China’s new single-aisle C919 jet—designed and manufactured by the Commercial Aircraft Corp. of China, or Comac—took its maiden voyage this month. The Comac C919 signals a turning point for China, and while there are clear intentions eventually to produce more components domestically, at present the new airliner is the portrait of globalization, including a variety of finished components produced outside of China (some of which are partly made up of subcomponents produced in China).

- China’s surge in home prices has moderated somewhat following stricter restrictions on property purchases: prices still rose, but only in 58 of the 70 major cities tracked each month, down from 62 in March.

Threats

- China was among the countries hardest hit by this week’s viral Ransomware attack, with Chinese companies, government agencies and universities running what is expected to be, according to Bloomberg News, a relatively high percentage of machines and networks dependent upon or operating unlicensed Windows software.

- The U.S. Navy is reported to have moved a second aircraft carrier near North Korea, even as China has stepped up criticism of its neighboring state.

- U.S. interest rate policies and/or political drama may continue to wield outsized influence in the region as markets assess near-term U.S. political and economic prospects.

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 1.2 percent. OTP Bank was the best performing equity trading on the Budapest stock exchange, gaining 5 percent. The bank reported strong first-quarter results and analysts’ ratings were revised up. Morgan Stanley improved ratings to overweight from equal weight and Citi revised its recommendation to buy from neutral.

- The Hungarian forint was the best performing currency this week, gaining 1.3 percent against the dollar. Investors who wish to keep their exposure to emerging-market assets may shift capital from Brazil to Central and Eastern Europe, where local assets offer attractive valuations supported by fairly robust growth, Rabobank’s EM FX strategist Piotr Matys wrote in a note on Friday.

- The health care sector was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 1.6 percent. Despite oil price recovery this week, Russian equites underperformed. The International Monetary Fund (IMF) said that Russian medium-term growth outlook is capped at about 1.5 percent because of structural issues, including demographics and technology, as well as lingering effects from sanctions.

- The Turkish lira was the worst performing currency this week, losing 11 basis points against the dollar. Turkish President Recep Tayyip Erdogan and Donald Trump met at the White House this week. Turkey and the United States are long-standing allies, but the relationship has been rocky in recent years.

- The utility sector was the worst performing sector among eastern European markets this week.

Opportunities

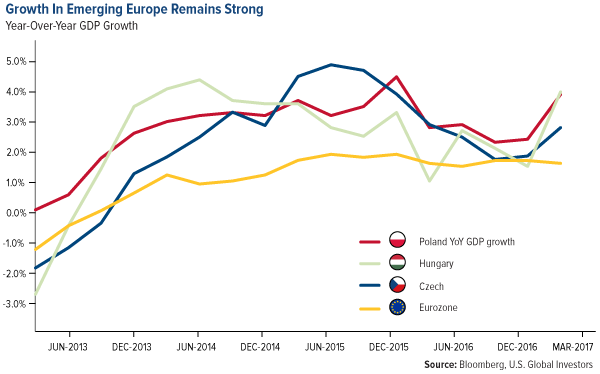

- Post-communist emerging European countries continue to grow at a much higher rate than the eurozone. Hungary’s first-quarter gross domestic product rose 4.1 percent year-over-year, Poland grew 4 percent and Czech Republic 2.9 percent. The eurozone grew at 1.7 percent during the same period.

- Oil production cuts could be extended at the next OEPC meeting on May 25. Steady demand growth and extended production cuts will drain global oil inventories, even as U.S. shale output continues to grow. BCA’s commodity team sees crude oil prices ending the year closer to $60 per barrel. Higher oil prices should benefit Russia, as its mains source of revenue comes from the sale of oil.

- Yields on Greek 10-year government bonds are heading toward levels last seen before 2009. The second review seems to be a done deal, with disbursement of the next tranche in the middle of June. The focus has turned to debt relief discussions and possible inclusion of Greek debt in a quantitative easing program.

- Poland’s sovereign credit rating was left at A2, the sixth-highest investment grade, and credit outlook was lifted to stable from negative by Moody’s Investors Service. The rating agency said that economic strength is offsetting risks stemming from increased government spending. Moody’s forecasts Poland’s 2017 and 2018 real gross domestic growth at 3.2 percent and 3.1 percent.

Threats

- The Trump campaign including Michael Flynn and other advisers had at least 18 undisclosed contacts with Russian officials and others close to the Kremlin in the last seven months of the U.S. presidential race, Reuters reported, citing former and current U.S. officials. Former FBI director, Robert Mueller, will run the probe into alleged Russian meddling in the elections.

- Turkish lawmakers elected seven members to a reshaped judicial authority on Wednesday, part of a constitutional overhaul backed by a referendum last month that considerably expanded the powers of President Erdogan. Erdogan says that the changes are needed to ensure stability in Turkey, while opposition parties and human rights groups say the reforms threaten judicial independence and push Turkey toward one-man rule.

- Russian economic growth remains weak after the recession ended last year. Gross domestic product had 0.5 percent gain last quarter after increasing 0.3 percent in the last quarter in the prior year. The central bank of Russia forecasts growth of 1.5 percent this year, assuming oil at $50 per barrel.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits