Five Things You Need to Know from this Week (Look What Gold Just Did!)

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

It’s been a whirlwind week. After attending two big conferences, I landed in Vancouver today where I’ll be presenting at the International Metal Writers Conference. Markets continue to close at record highs, even as political uncertainty remains and the threat of terrorism looms large over Western nations. On Monday, gold flashed a bullish signal we haven’t seen in over a year.

There’s much to talk about! Below are five things you need to know from the week now behind us.

1. Quants Now Control Wall Street

A special report by the Wall Street Journal this week confirmed what I’ve been saying for a while: Wall Street is now run by the quantitative analysts, or quants. Numbered are the days when traders and fund managers picked stocks on gut instinct. Today, a decision is made only after whole oceans of data have been processed using sophisticated algorithms.

And yet quants’ role has even further room to expand. As the WSJ reports, quant hedge funds now represent 27 percent of all U.S. stock trades by investors, up from 14 percent in 2013.

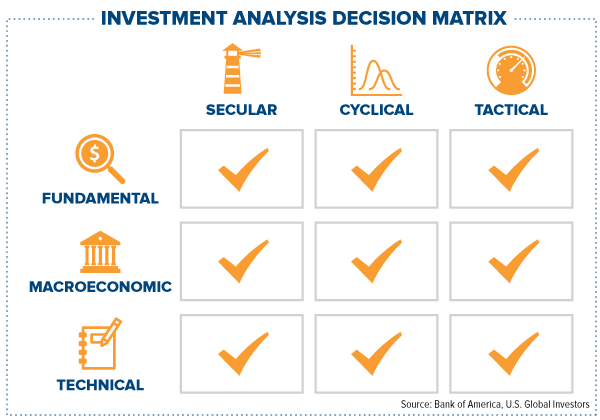

To get some idea of the type of analysis quants conduct, take a look at the matrix below. Of course, their methods are far more sophisticated, their data crunched in a matter of nanoseconds, but it’s helpful to see how they might codify many points of data.

We aspire to conduct the same sort of analysis, from technical to tactical, to make better, more strategic investment decisions.

2. Paul Singer Says It’s Time to Build Up Some Dry Powder

|

This week at a Chief Executives Organization (CEO) event, I had the privilege of hearing billionaire hedge fund manager Paul Singer speak. His firm, Elliott Management, has one of the most impressive long-term track records, generating a compound annual growth rate (CAGR) of 13.5 percent since its inception in 1977, with only two down years.

Elliott Management currently manages close to $33 billion—not including the $5 billion it raised this month in as little as 24 hours. Yes, billion with a b. Singer, suggesting a potential investment opportunity in distressed stocks could soon open up, recently called on investors to commit a fresh infusion of cash. The resultant $5 billion in dry powder, the most ever raised in the firm’s history, is expected to be deployed at some later date.

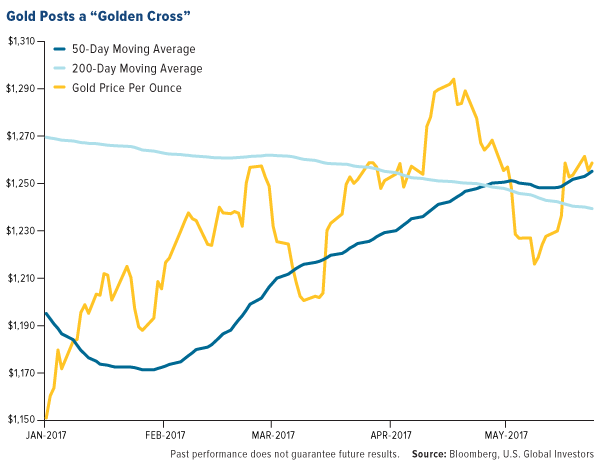

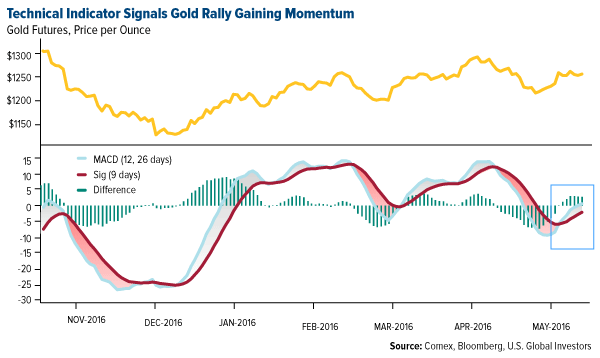

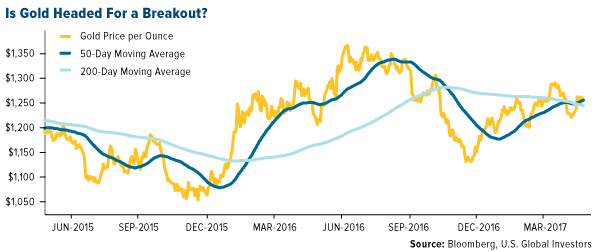

Gold posted a “golden cross” this week, which is what happens when the 50-day moving average climbs above the 200-day moving average, often seen as a bullish move.

The metal is up about 10 percent year-to-date on a weaker U.S. dollar, which has declined more than 5.5 percent over the same period.

3. BBH: Just Say No to Overdiversification

Diversification can sometimes help minimize volatility, but too much of it can lead to mediocre returns. That was the main theme of another speaker at the CEO event, this one from Brown Brothers Harriman (BBH), one of the largest private banks in the U.S. BBH research shows that, if your investment goal is to get rich, a highly-concentrated portfolio is the surest way to achieve it. An S&P 500 Index fund, while possibly delivering positive returns, is unlikely to make anyone a millionaire.

This is good to know, but the problem is that most investors can’t stomach the volatility inherent in a portfolio that holds only a few assets. With minimal diversification, daily swings can be dizzying. Professional money managers and investment banks such as BBH know how to use this volatility to their advantage, but for everyone else, it’s prudent to be diversified in gold, municipal bonds and other assets often seen as havens.

For more on how to deal with market volatility, download my whitepaper, “Managing Expectations.”

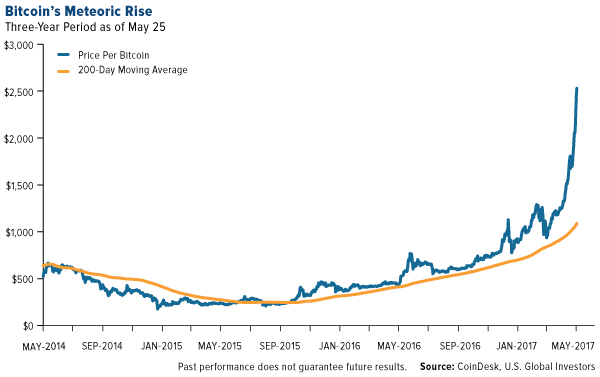

4. Want Volatility? Look No Further Than Bitcoin

Markets watched in amazement this week as bitcoin, the online-only currency, soared to a fresh high of $2,740, more than twice the value of an ounce of gold. On Thursday alone, it traded within a $510 range, underscoring the nearly 10-year-old cryptocurrency’s high levels of volatility and speculation.

Some bitcoin analysts forecast even higher gains, while others see the formation of a bubble they liken to the dotcom crash of the late 1990s and early 2000s. Since only March, when it surpassed gold, the digital currency has doubled in value.

These were among some of the discussions at Consensus, a bitcoin technology conference, which I also attended this week in New York. One of the highlights of the conference was hearing from Fidelity CEO Abigail Johnson, who surprised many attendees by embracing the digital currency and supporting its growth. I admire Johnson, head of a traditional financial firm, for recognizing the fact that bitcoin is already disrupting our industry and will likely continue to do so for some time. Not only does Fidelity now allow its workers to buy their lunches using bitcoin, but there are also plans to make it possible for clients to see and manage their bitcoin assets.

|

Fidelity isn’t the only firm trying to position itself as a bitcoin pioneer. Both Nasdaq and the Chicago Mercantile Exchange (CME) were sponsors of the conference, indicating cryptocurrencies’ gradual shift from fringe curiosity to legitimate speculative asset.

I was shocked to learn that there are now somewhere in the neighborhood of 700 cryptocurrencies, all of them locked in a race to see which ones will come out on top. They’re collectively up more than 400 percent so far this year, the market having risen from $17.6 million in January to $88 million today, according to cryptocurrency and blockchain technology news site CoinDesk.

To “mint” a new cryptocurrency, I learned, speculators raise capital not through conventional means but through crowdfunding, like a 21st century Gold Rush. All regulatory oversight and governance is therefore bypassed. The currency is then issued in an initial coin offering (ICO), after which it can be “mined” using powerful, energy-hogging computers. Naturally, the cheaper the electricity, the better. The hunt for the world’s cheapest kilowatt hour has taken “miners” all over the globe, from parts of Russia to Iceland to Finland to rural China.

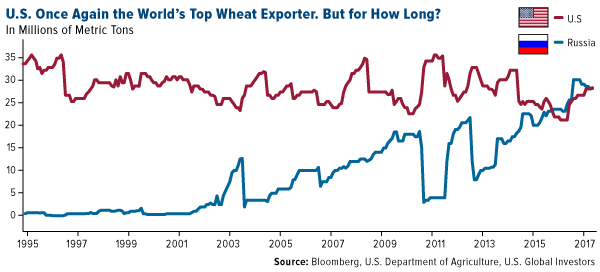

5. Make American Wheat Great Again

It looks as if wheat exporters are great again. After being displaced by Russia in August 2016, the U.S. has regained its title as the world’s top exporter of the grain—for now. Interestingly enough, the investigation into possible collusion between Donald Trump’s campaign and Russia has driven the U.S. dollar’s devaluation since the start of the year, which in turn has made U.S. exports cheaper for overseas buyers. Egypt, Algeria, Mexico and Japan all reportedly increased their purchase amounts of American wheat.

Two years ago, it was the Russian ruble’s weakness—prompted by the dramatic decline in oil prices and international sanctions following Russia’s occupation of Ukraine—that gave Russian exporters an edge. Coupled with a bumper crop, the country outpaced both the U.S. and European Union, then the leader.

As I said earlier, the dollar has declined 5.5 percent year-to-date, helping to give American exporters an edge. According to Bloomberg, the U.S. is expected to ship more than 28 million tons of wheat this season, an increase of 34 percent compared to the same time last year.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.32 percent. The S&P 500 Stock Index rose 1.43 percent, while the Nasdaq Composite climbed 2.08 percent. The Russell 2000 small capitalization index gained 1.09 percent this week.

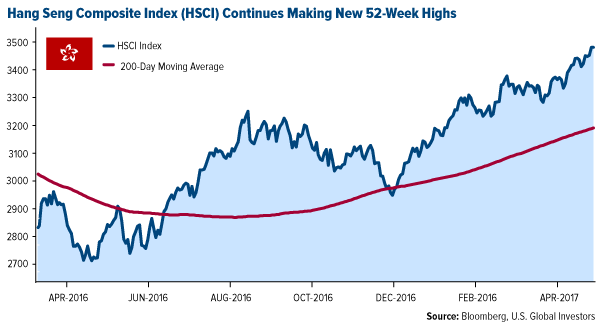

- The Hang Seng Composite gained 1.81 percent this week; while Taiwan was up 1.55 percent and the KOSPI rose 2.92 percent.

- The 10-year Treasury bond yield rose 1basis point to 2.25 percent.

Domestic Equity Market

Strengths

- Utilities was the best performing sector of the week, increasing by 2.48 percent versus an overall increase of 1.43 percent for the S&P 500 Index.

- Best Buy was the best performing stock for the week, increasing 14.88 percent.

- Best Buy beat on earnings. Comparable sales for the retailer climbed 1.6 percent, exceeding consensus forecasts of a 1.5 percent contraction. The firm reported first-quarter profit of $0.60 per share, above the average estimate of $0.40 per share and beating even the most optimistic forecast.

Weaknesses

- Energy was the worst performing sector for the week, falling 2.14 percent versus an overall increase of 1.43 percent for the S&P 500.

- Signet Jewelers was the worst performing stock for the week, falling 15.92 percent.

- Shares of Alexion Pharmaceuticals had a terrible week after the company announced a series of changes to its management team. Investors, it seems, worry that the decision to replace much of Alexion's management could be a sign that more trouble is on its way.

Opportunities

- Business Insider reports that corporate capital expenditure is picking up. According to a report from Strategas Research Partners, fixed asset investment is up 3.1 percent year-over-year. Strategas states that capital expenditures are more important than consumer spending, and that industrial and technology companies make up about one-third of the S&P 500. Nicholas Bohnsack, co-founder and head of quantitative research at Strategas, notes that industril capex has room to expand.

- Costco same-store sales crushed estimates. Sales at stores open at least one year rose by 5 percent excluding the impact of gasoline prices and foreign exchange, easily beating the 3.7 percent gain that was expected.

- Softbank is taking a big stake in Nvidia. The Japanese tech giant has invested $4 billion in the chipmaker, good for about a 4.9 percent stake, Bloomberg says.

Threats

- Billionaire Paul Singer's Elliott Management raised $5 billion in less than 24 hours earlier this month, says it has been building up its cash reserve to deploy during future market turmoil, reports Business Insider. The hedge fund’s recent letter states that the firm is anticipating volatility, and that “all hell will break loose,” and that “The only way to take advantage of those opportunities is to have read access to capital.”

- Mallinckrodt Pharmaceuticals is facing a probe, after Senator Claire McCaskill (D-MO) sent a letter to the company, Business Insider reports. The company acquired the pain medication Ofimerv when it purchased Cadence Pharmaceutical in 2014. Mallinckrodt Pharmaceuticals immediately doubled the price of the drug at the time, negatively impacting hospitals.

- A team of analysts from Morgan Stanley on Thursday published an updated list of the bank's "Shared Autonomous 30" reports Business Insider. Morgan Stanley’s lists 30 companies they believe “will influence a big transition from a world in which vehicles are sold to a world in which more emphasis is placed on how much vehicles are driven." Of conventional carmakers, Tesla makes the list. Other companies on the list include tech firms such as Microsoft, Google and Facebook.

The Economy and Bond Market

Strengths

- The second print of first quarter GDP beat. The U.S. economy grew 1.2 percent in the first quarter, better than initially reported. Economists had estimated that gross domestic product rose by 0.9 percent, improved from the advance estimate of 0.7 percent. The final revision for the quarter will arrive in Ju

- Eurozone growth holds at a six-year high. The flash, or preliminary, eurozone PMI held at a six-year high of 56.8 in May, with IHS Markit saying, "Job creation also perked up to one of the strongest recorded over the past decade amid improved optimism about future prospects."

- The preliminary Markit U.S. Services PMI for May came in at 54, stronger than the expected 53.3.

Weaknesses

- U.S. durable goods orders whiffed. The measure of purchases of goods designed to last dropped in April for the first time in five months. Durable goods orders fell 0.7 percent in April after rising 2.3 percent in March. The downturn was the first since durable goods orders fell 4.6 percent in November.

- Moody's downgraded China’s debt for the first time since 1989. The ratings agency cut its China rating to A1 from Aa3, saying it "expects that economy-wide leverage will increase further over the coming years."

- The Congressional Budget Office (CBO) score for the GOP healthcare bill is out. The American Health Care Act (AHCA) would reportedly leave 23 million more Americans uninsured than projected under the Affordable Care Act (ACA) and undermine protections for people with preexisting conditions, according to the updated estimate.

Opportunities

- The Federal Reserve seems determined to raise the overnight federal funds rate it controls. Many believe that two or three more 25 basis-point increases this year are all but certain, unless the economy suddenly weakens appreciably or a major financial or political crisis unfolds here or abroad. The prospect of steady rate increases is a worry to many market participants, with the taper tantrum of May and June 2013 still a vivid memory. The question now is: How much effect do changes in the fed funds rate have on longer-term Treasury yields? According to Gary Shilling, president of A. Gary Shilling & Co., a 100 basis-point increase in the fed fund rate results in a 46 basis-point increase in 10-year Treasury yields, on average. In other words, about half the change in the fed fund rate spills over to Treasury yields. So the influence is far less than one-to-one. As you’d expect, the spillover from fed funds changes to 30-year Treasury yields is even smaller. A 100 basis-point rise in the fed funds rate results in only a 35 basis-point rise in yields. Further, the influence of changes in the fed funds rate on Treasury yields may be even less today than in the past. Thirty-year yields are lower, not higher, than when the Fed first raised its reference rate by 25 basis points in December 2015 and then made further quarter-point increases in December 2016 and in March of this year.

- Tuesday's focus will be on the household sector with personal income, spending and consumer confidence data due. A rebound in April spending would support the Fed's view that the first-quarter weakness in consumer spending was "transitory."

- The all-important monthly employment report will be published on Friday. A strong report would further propel the Fed’s ability to raise rates during its June meeting.

Threats

- Some economists are concerned that President Donald Trump’s agenda could possibly deepen the income disparity that divides many parts of the U.S. and that helped propel Trump into the White House. Speaking to Business Insider this week, Emmanuel Saez, professor of economics at the University of California, Berkeley, said about Trump’s tax policies, “by giving large tax cuts to the wealthy would further exacerbate inequality.”

- With less than a week left in the regular legislative session, Illinois lawmakers and Governor Bruce Rauner are still divided on how to end the worst-rated state’s nearly three-year budget impasse. After May 31, a three-fifths majority will be required to pass anything, making a deal even more difficult to reach.

- Minutes from the May Federal Open Market Committee meeting, released Wednesday, showed the Federal Reserve plans to unwind its massive balance sheet by gradually increasing limits on the dollar amounts of Treasuries and other securities that will be allowed to run off into maturity each month. Depending on the execution, it could cause turmoil in fixed-income markets.

This week spot gold closed at $1,266.91, up $11.00 per ounce, or 0.88 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.24 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index returned 0.21 percent. The U.S. Trade-Weighted Dollar Index finished the week up 0.31 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| May-23 | U.S. New Home Sales | 620k | 569k | 642k |

| May-25 | Hong Kong Export YoY | 12.5% | 7.1% | 16.9% |

| May-25 | Initial Jobless Claims | 238k | 234k | 233k |

| May-26 | U.S. GDP Annualized QoQ | 0.9% | 1.2% | 0.7% |

| May-26 | U.S. Durable Goods Orders | -1.5% | -0.7% | 2.3% |

| May-30 | Germany CPI YoY | 1.6% | -- | 2.0% |

| May-30 | Conf. Board Consumer Confidence | 119.9 | -- | 120.3 |

| May-31 | Eurozone CPI Core YoY | 1.0% | -- | 1.2% |

| May-31 | Caxiin China PMI Mfg | 50.2 | -- | 50.3 |

| Jun-1 | ADP Employment Change | 180k | -- | 177k |

| Jun-1 | Initial Jobless Claims | 239k | -- | 234k |

| Jun-1 | ISM Manufacturing | 54.9 | -- | 54.8 |

| Jun-2 | Change in Nonfarm Payrolls | 180k | -- | 211k |

Strengths

- The best-performing precious metal for the week was palladium, up 4.18 percent. Bloomberg reports that rising automobile demand may be sending palladium futures toward the steepest rally since April 20.

- Bloomberg’s weekly poll of traders and analysts show the trending heading toward bullishness, with 10 bullish, five bearish and four neutral. Analysts point to concerns over terrorism, probes into President Donald Trump’s links to Russia and doubts that the Federal Reserve will raise rates in June, as factors that may spur investors to choose gold.

- China’s gold demand in 2017 is still the strongest in four years, reports Bloomberg. Although higher prices have deterred some buyers, dropping gold purchases from 15-month highs, the World Gold Council (WGC) sees demand growing to 900 to 1,000 metric tons for the full year.

Weaknesses

- The worst-performing metal for the week was gold, albeit still positive with a gain of 0.91 percent.

- The biggest gold miner ETF, the VanEck Vectors Gold Miners ETF, saw record outflows this week. On Wednesday, investors withdrew $662 million from the fund, making it the worst daily outflow since 2006. Similarly, the VanEck Vectors Junior Gold Miners ETF has had outflows of $804 million since March 31, after record inflows last quarter prompted the fund to change its portfolio structure. Bloomberg reports that the fund is now on track for the biggest quarterly outflow since the fund’s inception in 2009.

- A handful of gold mining stocks are experiencing challenges this week. Tragically, a fatal accident occurred at Torex Gold’s construction site at the El Limon Sur pit in Mexico. The ongoing ban on exports of mineral concentrate from Tanzania could cut Barrick Gold’s gold production by up to 6 percent this year, as Barrick’s equity interest in Acacia accounts for around 10 percent of its gold production. And Freeport-McMoRan has let go about 4,000 workers after a strike at the company’s Indonesian operations.

Opportunities

- Bank of America Merrill Lynch published a report this week on the company’s global mining conference in Barcelona. BofAML reports that most gold mining companies are in better condition than last year, due in great part to the better corporate discipline, with more focus on value over risk.

- Deutsche Bank published a special report on the global gold sector, stating “we feel investors should prepare for a flight to gold” in the uncertain global climate. The report also emphasizes the importance of looking for the gold stocks that offer better value, growth or leverage. Deutsche highlights the top global gold stocks as Newmont, Evolution Mining, St. Barbara Mining, Alacer Gold and Dacian Gold.

- Dacian CEO Rohan Williams told reporters that the recent deal between Eldorado and Integra signals the beginning of a cycle of mergers and acquisitions (M&A). More optimism for gold comes from Trump’s political troubles after Republicans criticized his budget. The gold price has risen, and gold’s open interest, a tally of outstanding contracts, has climbed to the highest since April 27. The chart below shows that the MACD (the gauge of price momentum) is above the “Sig,” or signal line, which is considered a bullish indicator. Yet another bullish indicator is that gold has experienced a golden cross, which happens when the 50-day moving average crosses above the 200-day moving average.

- Sibanye Gold recent acquisition of Stillwater Mining is under review in the courts. Some Stillwater investors contend that they were shortchanged with the purchase price of $18 per share. Sibanye is the U.S.’s only producer of platinum-group metals.

- South Africa is proposing to change the minimum black ownership of mining assets from 26 percent to 30 percent. Mines Minister Mosebenzi Zwane included this proposal in a mining charter. However, senior party policy officials said there may be negative consequences from such a measure, and that it may deter investment.

- Tanzanian Mines Minister Sospeter Muhongo was fired after an audit revealed that mineral exports had been understated. Acacia Mining has been investigated by a presidential committee, showing that Acacia reported certain containers held 26,000 ounces of gold, while the committee found those containers to hold 250,000 ounces. The magnitude of the discrepancy implies that the source mines, Bulyanhulu and Buzwagi, would actually be the world’s two largest gold producers. Those familiar with the events have called for an independent review. Acacia stock tumbled around 40 percent this week.

Energy and Natural Resources Market

Strengths

- Zinc was the best performing commodity this week, rallying 5.2 percent. Zinc prices soared as inventories shrank at an alarming rate according to Bloomberg. In recent years demand for the commodity has weakened considerably, forcing mines to close, stockpiles to rise and prices to fall. As economic growth is beginning to pick up in China and India, orders for the commodity from end users are beginning to pick up and when there is a lack of supply relative to strong demand, prices tend to rally. Although it is far too early to usher in an official bull market for zinc prices, this week’s price action is positive.

- The best performing sector this week was the S&P Super Containers & Packaging Industry Index. The index rose 3 percent on the back of increased investor demand as many index members raised dividends from stellar first-quarter performance.

- Bunge Ltd, one of the largest grain traders in the world headquartered in the U.S., was the best performing stock this week, finishing up 17.9 percent. The stock rose on the back of speculation surrounding a takeover offer from commodity trading giant Glencore.

Weaknesses

- Iron ore was the worst performing commodity this week, falling 4.5 percent. The commodity fell through $60 a tonne this week, marking a key psychological trading level. Stockpiles hit a new record high in China this week, taking the already bloated inventories up to 22.05 million tonnes, surpassing last year’s inventories at 20.85 million tonnes according to mining.com, and negatively impacting iron ore prices from China.

- The worst performing sector this week was the S&P/TSX Composite Oil & Gas Exploration & Production Sub Industry Index. The index fell 4.3 percent along with falling oil prices and lack of confidence in the sentiment surrounding the oil glut.

- The worst performing stock for the week was Devon Energy, an independent natural gas and petroleum producer located in the U.S. The company fell 6.7 percent as energy prices fell.

Opportunities

- This week gold prices formed a golden cross, a technical chart pattern that famously signals bullish breakouts. A golden cross occurs when the price of an asset’s 50-day moving average crosses above the 200-day moving average. As gold is up almost 10 percent for the year and geopolitical tensions across the globe continue to increase, the conditions surrounding a breakout and upward momentum for gold are looking very positive.

- On Thursday this week, OPEC agreed to extend oil supply cuts for another nine months into 2018 in attempts to end the glut, according to the Financial Times. The agreement made in Vienna outlined that 1.8 million barrels of production will continue to be cut until the end of the first quarter of 2018. Russia, the most important producer outside of the cartel, and other non-OPEC countries have also signed on to the deal, marking cooperation from the largest oil producers around the world. A supply cut is expected to be positive for oil prices.

- Miner and trader Glencore is looking to expand its agriculture business according to Reuters this week. The trading giant attempted a tie up with grains trader Bunge Ltd which may be the start of a wave of consolidation and partnering to come in the agricultural industry. Although a concrete deal is very far and speculative at this point, the trading giant is very adamant to expand its grain division. These events are positive for agricultural commodities.

- Noble Group, the Asian commodity trading house, was hit hard this week as common shares fell by a third according to the Financial Times. On Monday of this week, Standard & Poor’s cut Noble’s credit rating into junk territory and flagged that the company faces risk of defaulting on its debt load. Noble has repaid bank loans through asset sales and bond and share issues amounting to roughly $3 billion; however, investors have yet to buy into the company’s turnaround strategy.

- Australian iron ore producer Fortescue Metals Group warns of greater volatility to come in iron ore prices according to an article in the Financial Times this week. The company wrote to the Times stating that iron ore prices may need to fall further to counter the effect of a glut in Chinese supply. Nev Power, chief executive officer of the company, believes that at the current price point additional production may start to exit; however, if this production doesn’t exit fast enough to rebalance the market, more volatility for the commodity is highly likely.

- Core durable goods new orders plunged in April according to Bloomberg. Core durable goods new orders fell 0.4 percent for the month of April, dramatically worse than expectations of increasing 0.4 percent, which marks the worst performance since June 2016. Lower durable goods orders bode poorly for raw material demand from U.S. economic data.

China Region

Strengths

- South Korea had another strong week, with the KOSPI soaring another 2.7 percent for the week, once again closing at new highs.

- Hong Kong’s Hang Seng Composite Index climbed to new 52-week highs this week, rising 1.74 percent in that timeframe.

- Singapore’s year-over-year Industrial Production rose 6.7 percent, beating expectations of 6.0 percent. Month-over-month readings also beat, with a small rise of 0.1 percent handily beating expectations for a drop of 1.3 percent in April from March levels.

Weaknesses

- Indonesia’s Jakarta Composite fell 1.17 percent this week, giving back some of the gains from its late-week surge last week following the credit upgrade.

- Taiwan’s final first-quarter GDP—similar to Singapore’s final GDP—came in right in line, although down slightly from the prior print.

- China and then Hong Kong received downgrades to their credit ratings this week by Moody’s.

Opportunities

- Next week, Asian nations release a number of purchasing manager’s index (PMI) data, and investors will be keen to see how they clock in—especially with respect to China, where survey expectations for official data are looking for 51.0, down slightly from 51.2. Expectations for the Caixin are at 50.2, down from 50.3 last month.

- Some Chinese property names got an optimistic boost this week after reports and speculation that governmental authorities may ease some tightening measures.

- South Korea’s pension fund plans to boost overseas investments to 40 percent by the end of 2022, from 27 percent in 2016, according to Bloomberg News.

Threats

- Chinese firms will likely face the threat of higher debt costs after the Moody’s downgrade.

- According to a recent article by Bloomberg News about a new World Economic Forum report, China could end up with a savings shortfall in the future. The savings shortfall could climb as much as 7 percent per year in China, where the population is aging rapidly.

- U.S. interest rate policy reverberations could continue to create potentially outsized effects within the Asia Pacific region.

Strengths

- Turkey was the best performing country this week, gaining 2.5 percent. The Turkish economic confidence index increased by 1.1 percent to 100.5 points in May. The index indicates an optimistic outlook about the general economic situation when economic confidence index is above 100, whereas it indicates a pessimistic outlook when it is below 100.

- The Russian ruble was the best performing currency this week, gaining 73 basis points against the dollar. The ruble strengthened against the dollar while the Russian stock market and oil corrected. Many analysts view the ruble as overvalued at the current level.

- The real estate sector was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 1.4 percent. The Moscow stock exchange corrected with the price of oil. Brent crude oil declined 2.7 percent after OPEC and non OPEC members extended the oil output cut by nine months. Some investors had been hoping oil producers could reach a last-minute deal to deepen the cuts or extend them further, until mid-2018.

- Euro was the worst performing currency this week, losing 30 basis points against the dollar. Eurozone inflation will be released next week, with most Bloomberg analysts predicting a drop in inflation to 1.5 percent from prior 1.9 percent. It’s an important reading for Mario Draghi to determine change in the monetary policy.

- The health care sector was the worst performing sector among eastern European markets this week.

Opportunities

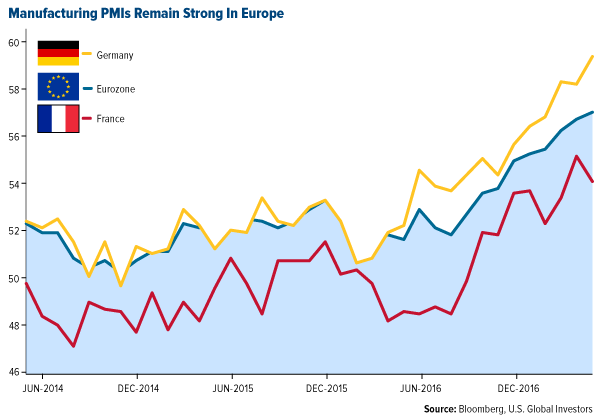

- Major European purchasing managers’ index (PMI) data in Europe is pointing to accelerating growth. PMIs remain strong above the 50 level that separates growth from contraction in the manufacturing sector. The preliminary May reading for Germany was reported at a multi-year high of 59.4, eurozone at 57 and France at 54.

- Russia’s Finance Minister is planning to offer its first 2017 Eurobonds as early as the next few weeks. The issue will be organized by Russian banks, as foreign institutions have been reluctant to participate due to sanctions imposed on Russia by the U.S. and eurozone. Russia is planning to issue $7 billion in eurobonds this year. Last year, the country sold $3 billion in two tranches. The budget deficit is expected to be 2.1 percent of gross domestic product this year, lower than the 3.2 percent seen in the beginning of the year.

- There is still optimism that an agreement will be reached within the next couple of weeks between Greece and its creditors. A leaked document from the Eurogoup came out, pointing to all the various differences that exist in the creditors, mainly in the debt front. The target for disbursement to Greece is the second half on June.

Threats

- A leaked memo from a secret meeting in Strasburg suggests that the European Commission will force all EU member countries to adopt the common euro currency by 2025. Nine of the 28 member states in the EU are currently not part of the single currency. The U.K. and Denmark are exempt, but counties like Poland, Hungary, Czech Republic, Romania, Croatia and Bulgaria all agreed to adopt the euro when they joined the bloc. Just last week, Polish finance minister Mateusz Morawiecki said it was "not in Poland’s interest" to join the eurozone. Warsaw is worried about losing its financial autonomy.

- President Donald Trump’s behavior at the NATO summit was embarrassing, the Washington Post’s Karen Attiah writes. He was the party guest who no one wants to deal with but has to because he has more money than anyone else. Trump called Germany “very bad” in a meeting with EU officials, saying the country’s manufacturers sell too many cars to the U.S. and he is going to stop it.

- Polish unemployment was at 5.3 percent in March and February, among the lowest in the EU, and it could be a sign of worse to come. The labor market is squeezed by emigration, a low participation rate and government policies as a reduction in the retirement age that further shrink the pool of workers. The central bank estimates the unemployment rate is already below the level that puts pressure on wages.

|

© US Global Investors |

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits