Trump Bids Adieu to Paris Climate Agreement. What Does this Mean for Energy Investors?

Surprising no one, President Donald Trump announced his decision to withdraw the U.S. from the Paris climate agreement this week, highlighting the depth of his commitment to keep “America First.” Also surprising no one, the media is making much of the fact that the U.S. now joins only Nicaragua and Syria in refusing to participate in the accord.

Trump was under intense pressure from business leaders, politicians on both sides of the aisle, environmental activists, members of his Cabinet—even his own daughter Ivanka, reportedly—to stay in the agreement, but he made his decision with the American worker in mind. The Paris accord, Trump said, “is simply the latest example of Washington entering into an agreement that disadvantages the United States,” leaving American workers and taxpayers “to absorb the cost in terms of lost jobs, lower wages, shuttered factories and vastly demised economic production.”

This is the assessment of Secretary of Commerce Wilbur Ross, who went on Fox News to defend the decision. “Any time that people are taking money out of your pocket and you make them put it back in, they’re not going to be happy,” Ross said, making a similar argument to the one that prompted the Brexit referendum last year.

Just as many Brits were tired of following rules passed down from unelected officials in Brussels, many Americans have feared the encroachment of global environmentalists’ socialist agenda, which they believe threatens to usurp their freedom.

A thought-provoking article from FiveThirtyEight outlines how climate science became a partisan issue over the last 30 years in the U.S. It was the fall of the Soviet Union in the early 1990s, the article argues, that brought on a significant partisan shift in attitude, with conservative thinkers beginning to see the regulations that went along with environmentalism as the new scourge.

No, the Sky Isn’t Falling

Despite the withdrawal, I believe that the U.S. will not stop innovating and being a world leader in renewable energy—even while oil and natural gas production continues to surge. As the president himself said, we will still “be the cleanest and most environmentally friendly country on Earth.”

Last week I shared with you that we’re seeing record renewable capacity growth here in the U.S., with solar ranking as the number one source of net new electric generating capacity in 2016. In the first quarter of 2017, wind capacity grew at an impressive 385 percent over the same period last year. The “clean electricity” sector now employs more people in the U.S. than fossil fuel electricity generation, according to the 2017 Energy and Employment Report.

This was all accomplished not because of an international agreement but because independent communities, markets and corporations demanded it. Solar and wind turbine manufacturers will likely continue to perform well in the long term as renewable energy costs decline and battery technology improves.

Clearly people’s attitudes toward climate change—and its impact on business operations—are changing. This week, Exxon Mobil shareholders voted to require the company to disclose more information about how climate change and environmental regulations might affect its global oil operations. The energy giant—along with its former CEO, Secretary of State Rex Tillerson—favored staying in the climate deal.

At the same time, markets reacted positively to the exit, with the S&P 500 Index, Dow Jones Industrial Average and NASDAQ Composite Index all closing at record highs on Thursday following Trump’s announcement.

So What Does This Mean?

The question now is what investment implications, if any, the withdrawal might trigger.

The short answer is no one knows exactly what happens now. There’s already speculation that some countries might act to raise “carbon tariffs” on U.S. exports, increasing the cost of American-made goods “to offset the fact that U.S. manufacturers could make products more cheaply because they would not have to abide by Paris climate goals,” according to Politico. German chancellor candidate Martin Schulz has said that, should he be elected in September, he would refuse to “engage with the U.S. in transatlantic trade talks.” Schulz’s comments are not that far removed from those of his political rival, incumbent Angela Merkel, who called Trump’s decision “extremely regrettable.”

This has the potential to widen the rift that’s been forming between the U.S. and Germany since Trump took office. Recall that Trump refused to shake Merkel’s hand during her Washington visit in March. More recently, the president reportedly called the Germans “bad, very bad,” adding that he would stop them from selling millions of cars in the U.S.

One of the biggest winners of the withdrawal could be China. Just as the Asian giant is poised to benefit from the U.S. distancing itself from multilateral free-trade agreements such as NAFTA and the Trans-Pacific Partnership (TPP), it’s also in a position to brand itself as the world’s leader in renewable energy. Just today, Chinese Premiere Li Keqiang met with European Union (EU) officials in Brussels to discuss trade between the two world superpowers, but they also took the time to condemn the U.S. president’s actions, with European Council president Donald Tusk saying that the Paris agreement’s mission would continue, “with or without the U.S.”

|

China might be the largest carbon emitter right now—it overtook the U.S. a decade ago—but it’s also the biggest investor in renewable energy generation, with $361 billion being spent between now and 2020. The country just fired up the world’s largest floating solar power plant in what used to be a coal mine, now flooded. The plant will provide as much as 40 megawatts (MW) of power to Huainan, China, home to more than 2.3 million people.

European Manufacturers Have Strongest Jobs Growth in 20 Years

On the same day President Trump shared his decision, new purchasing manager’s index (PMI) data was released, and just like last month, European manufacturers were the big surprise. The EU manufacturing sector strengthened its expansion for the ninth straight month in May, reaching a 73-month high of 57, right in line with expectations. Jobs growth grew to an incredible 20-year high.

Germany led the group with a PMI of 59.5. Of the eight EU countries that are monitored, only Greece fell short of expansion.

The U.S., meanwhile, slipped from 52.8 in April to 52.7 in May, posting the weakest improvement in business conditions in eight months, before the election. China fared even worse, falling from 50.3 to 49.6, signaling a slight deterioration in its manufacturing sector for the first time in almost a year.

In Gold We Trust

With the U.S. dollar taking another hit today on a weaker-than-expected jobs report, gold closed up 1.12 percent today. A Bloomberg gauge of 72 junior miners, however, has lost 15 percent since the end of January, and the rebalance of the VanEck Vectors Junior Gold Miner ETF (GDXJ), which I previously wrote about, is also having a depressing effect on many gold names.

This was a major concern among investors at the International Metal Writers Conference in Vancouver, which I presented at earlier this week. Despite gold gaining 9 percent so far this year, junior gold miners have not followed through with those gains as the GDXJ is set to cut in half its exposure to the junior mining space on June 16.

Other investors aren’t so pessimistic. Every year for the past 11 years, Liechtenstein-based investment firm Incrementum has issued its closely-read “In Gold We Trust” report. The 2017 edition, released yesterday, raises a number of interesting observations that add some shine to gold’s investment case.

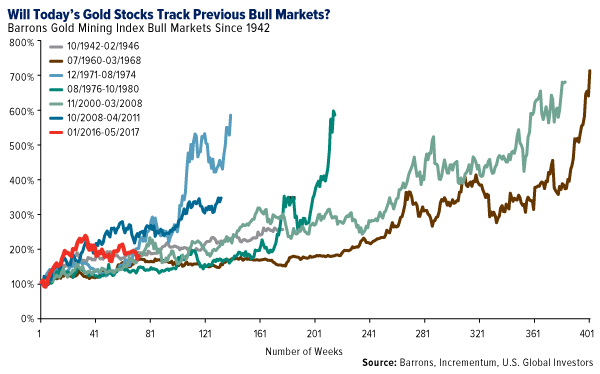

For one, its analysts firmly believe that gold’s price turnaround last year “marked the end of the cyclical bear market,” adding that “the rally in the precious metals sector has probably only just begun.” To illustrate this, the group tracked the performance of every gold stock bull market going back to 1942, using the Barron’s Gold Mining Index. The bull market that began last year, highlighted in red below, does indeed look as if it has much more room to run.

Among the reasons why “prudent investors” should consider accumulating gold and gold stocks now, according to Incrementum, are excessive global debt, the “gradual reduction of the U.S. dollar’s importance as a global reserve currency” and what the group sees as a high probability that the U.S. is close to entering a recession. Interestingly, the investment firm shows that nearly every U.S. recession, going back 100 years, was preceded by an increase in interest rates.

“The historical evidence is overwhelming,” Incrementum writes. “In the past 100 years, 16 out of 19 rate hike cycles were followed by recessions. Only three cases turned out to be exceptions to the rule”—one in the 1960s, one in the early 80s, the last in the mid-90s.

The U.S., of course, is currently at the start of a new cycle, though the ho-hum jobs report for May—138,000 jobs added, versus expectations for 185,000—casts doubt on a rate hike this month. Nevertheless, Incrementum’s research makes a compelling case that a recession could be imminent, making gold even more attractive as a store of value.

As for gold stocks, Incrementum favors “conservatively managed companies which are not merely pursuing an agenda of growth at any price, but are instead prioritizing shareholder interest.”

This is an apt description of the kinds of gold companies we prefer—frugal, small- to mid-cap names such as Klondex, Wesdome Gold Mines, Kirkland Lake and many others.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.60 percent. The S&P 500 Stock Index rose 0.96 percent, while the Nasdaq Composite climbed 1.54 percent. The Russell 2000 small capitalization index gained 1.67 percent this week.

- The Hang Seng Composite gained 0.97 percent this week; while Taiwan was up 0.50 percent and the KOSPI rose 0.70 percent.

- The 10-year Treasury bond yield fell 9 basis points to 2.15 percent.

Domestic Equity Market

Strengths

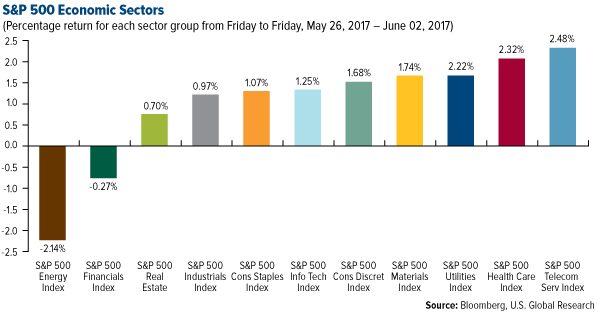

- Telecommunications was the best performing sector of the week, increasing by 2.14 percent versus an overall increase of 0.93 percent for the S&P 500 Index.

- Cooper Companies was the best performing stock for the week, increasing 9.54 percent.

- Cooper Companies reported higher profits than estimated and raised future analyst expectations by boosting its earnings forecast for the next year. Shares are at the highest level in the past 52 weeks and trading volume picked up confirming the recent price advance.

Weaknesses

- Energy was the worst performing sector of the week, declining 2.38 percent versus an overall increase of 0.90 percent for the S&P 500.

- Michael Kors was the worst performing stock for the week, declining 10.07 percent.

- Online shopping has maintained recent pressure on apparel makers like Michael Kors. The company has decided to reduce the amount of product they sell in the wholesale channel to prevent discounts and maintain current margins. Additionally, the company plans to close approximately 100 stores during the next 24 months, decreasing revenue by nearly 5 percent.

Opportunities

- Wage growth continues to climb and is currently just below 3 percent year–over-year.

- The ISM manufacturing composite index ticked a little higher since last month and, if this is a precursor for the Composite purchasing managers’ index numbers, we can probably expect an uptick there too.

- The 30-Year fixed mortgage rate fell to 3.94 percent. Consumers still have time to lock in mortgage rates before the next Fed rate hike.

- Student loan balances are a lot smaller than people thought. Media reports love to quote the $1.3 trillion of total student loan debt, but when analysts dive into the data, the debt load is not as bad as it seems. According to Deutsche Bank, 66 percent of student loans are smaller than $25,000, much less than the bears on Wall Street would like investors to believe.

Threats

- For the month of April U.S. construction spending fell 1.4 percent and residential home improvement declined 2.9 percent. If the Fed continues to raise rates we may see some investors take profits on housing and home improvement stocks.

- The Atlantic hurricane season officially began Thursday, and forecasters are expecting an above-average number of named storms this year. In 2017 the insurance industry had large losses due to tornados and hail so it will be interesting to see what Mother Nature has in store for us.

- According to the fed funds futures, there is a 90 percent chance that the Fed hikes interest rates a quarter of a percentage point later this month.

The Economy and Bond Market

Strengths

- American factories are settling back into a solid pace of expansion after a post-election run up that saw the ISM manufacturing gauge hit an almost three-year high. The purchasing managers’ index (PMI) came in at 54.9 in May, up from 54.8 in April. A reading above 50 indicates growth. ISM’s gauge of new orders increased to 59.5 from 57.5. Stronger orders growth represents resilient sales that will keep manufacturing pushing forward.

- Euro-area manufacturers are hiring at a record pace as growing export and domestic demand push output to the highest level in six years. PMI rose to 57 in May from 56.7 the previous month, IHS Markit said this week, confirming a May 23 flash estimate. Euro-area employment jumped the most in the survey’s 20-year history and expanded in all countries covered for the first time since November.

- Italy’s GDP grew 0.4 percent in the first quarter, twice as fast as initially estimated and the fastest pace since the final quarter of 2010. The better-than-expected figures came as the European Commission announced it reached an agreement with Italian officials on a draft plan allowing for Italy’s largest bank Banca Monte dei Paschi di Siena SpA to receive a state recapitalization. Italy’s main parties are also edging closer to a deal on a new electoral law which paves the way for snap elections as early as the second half of September (instead of the scheduled end of the legislature in early 2018).

Weaknesses

- A qualitative assessment of the economic anecdotes provided in the latest Beige Book suggests that U.S. growth is hovering around 2 percent or so. Most Federal Reserve districts said that "their economies continued to expand at a modest or moderate pace." Manufacturing, nonfinancial services and construction all reported "modest to moderate" growth. One area of softness was the consumer. It was noted that household spending "softened with many districts noting little or no change in non-auto retail sales, while auto sales have edged down from last year's record highs." The next retail sales report will need to be watched for hard evidence of sluggish consumer spending.

- A private gauge of Chinese manufacturing fell back into contractionary territory in May, adding to recent evidence that the economy’s strong start to 2017 is leveling off. The Caixin and Markit Economics PMI fell to 49.6 from 50.3 in April, the lowest reading since June 2016 and below the 50.1 median estimate.

- Moody’s lowered China’s rating to A1 from Aa3 on Wednesday, citing a worsening debt outlook.

Opportunities

- Stocks near a record high, sustained strength in the labor market and steadily rising wages are making Americans feel better about their financial well-being and the economy. Americans are the most upbeat about their finances in a decade, which will probably help consumer spending, contribute more to the U.S. economy in the second quarter, Bloomberg Consumer Comfort Index figures showed Thursday. The overall gauge jumped to 51.2, the second-strongest reading since 2001, from 50.9.

- According to the Wall St. Journal, the era of stubbornly weak wage growth could be coming to an end as the economy slowly shifts toward better paying jobs from low wage work at restaurants and stores. Since the U.S. started consistently adding jobs in 2010, employment in three low-wage categories (leisure and hospitality, retail, and temporary help) had grown at a faster rate than overall private-sector payrolls until this year. Growth in other private-sector industries has outpaced gains in the three largest low-wage categories since February. It’s the first time such a shift has occurred during the expansion. And it could be a precursor to better wage growth as stronger job gains in fields that pay above-average wages lift the broader pay measure.

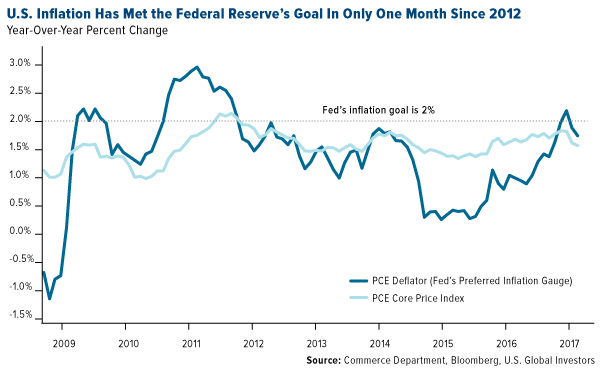

- Commerce Department data on Tuesday show that the Fed’s preferred price measure rose 1.7 percent in April from a year ago, down from 1.9 percent in March and 2.1 percent in February. Core inflation -- which strips out volatile oil and food costs -- also slowed to the weakest annual pace since 2015. A rebound anytime soon looks unlikely, with prices kept in check by an ongoing oil glut, an overstocked auto market and a rising supply of apartments to rent. Inflation looks likely to end the year shy of the Fed’s forecast. While the shortfall isn’t expected to prevent central bankers from raising interest rates in the next policy meeting, a sustained stall would make it more difficult for Chair Janet Yellen and her colleagues to follow through with another hike later in the year, as their March projections indicated.

Threats

- Headline consumer confidence drifted off of its post-recession peak (124.9), logged in March. At 117.9 in May versus 119.4 prior, confidence remains in healthy territory, to be sure, but it also runs consistent with the narrative that consumers’ faith in significant economic-policy reform is starting to fade. There is a mild tug-of-war occurring between consumers’ expectations of the future versus their reaction to healthy economic conditions at present, which is largely attributable to low interest rates and a healthy labor market. Consumers’ expectations for the future slipped to 102.6 from 105.4 prior, down from a peak of 112.3 in March. Their assessment of present conditions actually improved ever-so-slightly in May to 140.7 versus 140.3 prior. Future expectations are off nearly 10 points since March, while present conditions are down just three points.

- The spread between corporate bonds and Treasuries currently is around 113 basis points, according to Bloomberg Barclay’s index data. And it will likely narrow further as demand continues to outpace supply, Bank of America Merrill Lynch strategists led by Hans Mikkelsen wrote in a note to clients Tuesday. Inflows to high-grade debt mutual funds and exchange-traded funds are at a record $130 billion year-to-date, up roughly $85 billion year-over-year, and supply for the first five months of the year stands at $650 billion, just $25 billion above the same period last year, according to Mikkelsen. While this scenario would seem to encourage risk taking and a chase for yield, credit investors have been careful because of the political unease surrounding President Donald Trump’s agenda. Tight credit spreads and uncertainty about the Trump administration’s economic policy has money managers bracing for low returns on their corporate bond portfolios this year.

- President Donald Trump announced Thursday he is withdrawing the U.S. from the Paris climate accord. Corporate leaders have warned of long-term economic consequences, arguing that a withdrawal would put the U.S. at a disadvantage in the global race to develop and deploy clean-energy technology. They argued a U.S. exit also risks a backlash against American products, raising the specter of consumer boycotts or carbon tariffs from the European Union, China and other nations.

Gold Market

This week spot gold closed at $1,278.45, up $11.55 per ounce, or 0.91 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.72 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index fell 0.94 percent. The U.S. Trade-Weighted Dollar Index finished the week lower by 0.77 percent

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

May-30 |

Germany CPI YoY |

1.6% |

1.5% |

2.0% |

|

May-30 |

Conf. Board Consumer Confidence |

119.5 |

117.9 |

119.4 |

|

May-31 |

Eurozone CPI Core YoY |

1.0% |

0.9% |

1.2% |

|

May-31 |

Caxiin China PMI Mfg |

50.1 |

49.6 |

50.3 |

|

Jun-1 |

ADP Employment Change |

180k |

253k |

174k |

|

Jun-1 |

Initial Jobless Claims |

238k |

248k |

235k |

|

Jun-1 |

ISM Manufacturing |

54.8 |

54.9 |

54.8 |

|

Jun-2 |

Change in Nonfarm Payrolls |

182k |

138k |

174k |

|

Jun-5 |

Durable Goods Orders |

-0.3% |

-- |

-0.7% |

|

Jun-8 |

ECB Main Refinancing Rate |

0.000% |

-- |

0.000% |

|

Jun-8 |

Initial Jobless Claims |

239k |

-- |

248k |

Strengths

- The best performing precious metal for the week was palladium, up 6.17 percent. Consumer demand is rising for gasoline- versus diesel-engine powered vehicles, yet automobile sales have started to relax in recent months. According to Bloomberg, gold bulls outnumber gold bears this week as Trump probes are boosting safe-haven demand for the yellow metal. In fact, gold advanced to the highest level in nearly a month as Trump’s administration “grapples with revelations of mounting scrutiny into son-in-law Jared Kushner’s outreach to Russian officials,” Bloomberg continues. In related news, Fed’s Brainard says that soft inflation data may warrant a rethink on interest rates. Inflation in the Euro-area slowed more than economists forecast.

- The Indian rupee posted its first monthly loss since November, reports Bloomberg. The positive side of this is the decline came amid increasing demand for dollars to pay for imports of items such as gold. The Perth Mint reported its gold coin and minted bar sales for the month of May, coming in at 29, 679 ounces. This is compared with April’s sales of 10,490 ounces.

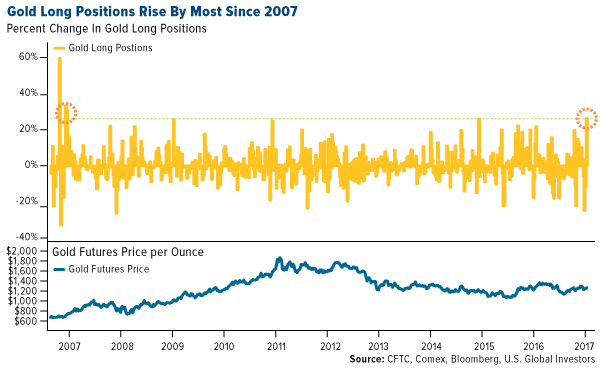

- Data from the Commodity Futures Trading Commission shows that money managers boosted their long positions in U.S. gold futures by the most in almost a decade in the week ending May 23, reports Bloomberg. As you can see in the chart below, hedge funds are jumping back into the yellow metal.

Weaknesses

- Platinum bore the brunt of the palladium move this week with a loss of 0.61 percent. Shares of junior gold miners headed for the longest stretch of monthly losses in more than two years, reports Bloomberg, citing investor concern that “flagging momentum in this year’s bullion rally will dent the outlook for profits.” A Bloomberg gauge of 72 junior miners has lost 15 percent since the end of January and the rebalance of the VanEck Vectors Junior Gold Miner ETF (GDXJ) is also having a depressing effect on many gold names. Despite gold gaining 9 percent this year with a drop in the dollar, junior gold miners have not followed through with those gains as the GDXJ is set to cut in half its exposure to the junior mining space on June 16.

- “Inflation has been below target for five years and has moved up only slowly toward 2 percent, which argues for continued patience,” said Fed Governor Jerome Powell in a statement this week. Powell is calling for gradual interest rate increases and a start to balance-sheet reductions later this year if the economy stays on track, reports Bloomberg, though he is keeping an eye on a recent slowdown in inflation. Based on prices in federal funds futures contracts, investors see the probability of a rate hike at around 85 percent when the FOMC meets June 13-14, the article continues.

- Asanko Gold is set to release an expanded Mine Feasibility Report in response to a Muddy Waters short report that detailed negative assertions regarding the company and its operations, reports Bloomberg. Asanko said in a statement that there is no merit to the Muddy Waters report, while detailing that it maintains production guidance of 230,000 to 240,000 ounces for 2017. Asanko also said it sees no impact on production or safety resulting from a partial failure on the western wall of the Nkran pit, nor does it see a need for a $115 million pushback expense (as speculated by Muddy Waters). The short report was likely timed to force Asanko’s market capitalization below the lower threshold limit for staying in the GDX index, thus triggering an additional 10.6 million shares to be sold.

Opportunities

- Friday’s jobs report came in lower by 4.3 percent, and although the three-month moving average of 121,000 net new jobs is positive, the pace has slowed dramatically, writes Bloomberg. And if the Fed continues to raise rates, it will slow even further. Economists have three major risks they are worried about, according to the article: 1) slumping U.S. auto sales, 2) weaker Chinese manufacturing and 3) the potential for U.S. fiscal policy disappointment. “Anticipating a rate-hike endgame or more increases in rising inflation, gold is poised to continue to perform well,” explains another Bloomberg article. “In the current tightening cycle, spot gold and the S&P 500 Index are neck and neck, up 19 percent to June 1.”

- In a research update from Industrial Alliance Securities, the group summarizes production statistics released by Rye Patch Gold from its Florida Canyon heap leach operation for May. Rye Patch reported 3,094 ounces of gold poured during May, up from 485 ounces in April. The mine is well on its way to achieving operating financial breakeven, the report continues. Rye Patch notes that heap leach operations tend to perform better in warmer temperatures (so notable production acceleration during the Nevada summer would not be a surprise) as well as the company’s extra cash in hand to fund further exploration. Similarly, Richmont Mines reported strong results from the Island Gold Mine Expansion Case Preliminary Assessment. It confirmed an increase in underground mine and mill productivity to 1,100 tonnes per day, supporting growth of 22 percent over an eight-year period, reports Bloomberg.

- More company-specific news comes from Lundin Gold this week, which announced a $400-$450 million project financing package for Fruta Del Norte in Ecuador. The package comes with support from Orion Mine Finance and Blackstone Tactical Opportunities. Another announcement comes from AuRico Metals, noting a positive Preliminary Economic Assessment for the Kemess East Gold-Copper Project. Pre-production capital costs are C$327 million, reports Bloomberg.

Threats

- As Jared Kushner, Donald Trump’s son-in-law and most trusted adviser, is sucked into an FBI probe, the President’s goals are increasingly at risk, reports Bloomberg. The probe could undermine policy priorities and hinder behind-the-scene communications with business leaders and foreign governments. “Kushner tried to establish a secret back channel between the president-elect and Kremlin after Trump’s election, and is reported to have held multiple undisclosed meetings with Russian officials during the campaign and transition,” the article states.

- The AOMA Argentine union has threatened to restart a strike at Barrick Gold’s Veladero gold operation in the country next month if talks with management fail to resolve a contractual feud, reports Bloomberg. Barrick and the AOMA union were set for a third round of talks late Monday, with the dispute over contracts for outsourced workers being about three-quarters of the way resolved, said AOMA Secretary General Hector Oscar Laplace.

- According to Wood Mackenzie, deep-water drilling costs are coming down as producers streamline operations and prioritize drilling in core wells. This means that oil at $50 per barrel could sustain some deep-water projects by 2018, reports Bloomberg. The tumbling costs present a challenge for the Organization of Petroleum Exporting Countries (OPEC), which is currently curbing output to shrink a glut, the article continues. Falling energy prices could dampen inflation expectations and be a headwind to gold prices.

Energy and Natural Resources Market

Strengths

- Gold rallied 0.9 percent this week. The shiny metal was up after the U.S. economy added fewer jobs than expected for the month of May where payrolls missed analyst expectations of 182,000 (advancing to only 138,000), according to Bloomberg. As the job market cools down, the prospect of aggressively increasing interest rates strongly weakens, which in turn could help gold prices further. A positive read-through for gold this week.

- The best performing sector this week was the Bloomberg Americas Auto Parts & Equipment Index. The index rose 2.9 percent on the back of long-term positioning into the sector as companies like Magna International begin to talk about pivoting toward “cars of the future.”

- Fresnillo PLC, a precious metal mining company based in Mexico, was the best performing stock this week finishing up 5.1 percent. The stock rose on the back of positive investor sentiment as the company released news that it is on track to meet production targets in the months ahead.

Weaknesses

- Natural gas was the worst performing commodity this week dropping 6 percent. The commodity fell substantially as data released from the U.S. Energy Information Administration (EIA) indicated that domestic supplies rose by 81 billion cubic feet. A negative read-through for natural gas prices going into the summer months.

- The worst performing sector this week was the S&P/TSX Diversified Metals and Mining Sub Industry Index. The index fell 7 percent on the back of falling base metal prices as investors fret over falling PMI’s and weakening growth prospects in the U.S. and Asia.

- The worst performing stock for the week was First Quantum Minerals Ltd., a metals and mining company based in Vancouver. The company fell 9.9 percent on the back of falling base metal prices.

Opportunities

- Crude oil traded higher on Thursday as U.S. inventories continue to decline, reports Bloomberg. Oil rebounded from its lowest level in more than two weeks after this week’s inventory release from the International Energy Agency (IEA) which fell by 6.4 million barrels versus analyst expectations of a 2.5 million barrel decrease. Michael Lynch, president of Strategic Energy & Economic Research stated that given the average draw size, it wouldn’t be surprising to see prices back to $50 per barrel given this latest report. A positive read-through for oil this week.

- Gold locks in its longest monthly winning streak since 2010 for the month of May, reports the Financial Times. As May comes to an end, gold has marked its fifth consecutive monthly advance, bringing its total advance year-to-date to 10.6 percent thus far. The shiny metal had an incredible performance on May 17 when U.S. President Donald Trump occupied the headlines as a probe was launched into his campaign ties with Russia sending a flurry of investors rushing for safe-haven assets like gold. If geopolitical tensions continue to take hold of financial markets and investor sentiment shifts to a place of worry, this could bode very well for gold prices in the months to come.

- As the Paris climate accord wraps up this week, President Trump’s economic advisor Gary Cohn says that coal can be competitive again, reports Reuters. Cohn stated to the press that America’s withdrawal from the Paris climate accord will help keep energy markets competitive, paving the way for a potential comeback in coal prices and the U.S. coal industry. In addition, Cohn believes that despite competition from cheap natural gas options, at some point throughout the cycle coal will be competitive again. A positive read-through for coal.

Threats

- Russia warns hedge funds that they can “live forever” with $40 oil, according to Bloomberg. Russian economic minster, Maxim Oreshkin, stated to the press this week that the country is ready to live with oil at $40 (or below) per barrel forever as all macroeconomic policy around the globe is now based on the assumption of oil at $40 per barrel and is no threat to the country’s economy. Oreshkin believes the price of oil within one or two years may be much lower and hedge funds with bullish bets are taking very huge risks. A negative read-through on oil from one of the largest producers in the world. >

- Key economic data points come in weaker than expected this week in both the U.S. and China. In the U.S., manufacturing PMI dropped to an eight-month low for May coming in at 52.7, while China’s manufacturing PMI came in at its lowest level since June of 2016 on the back of weak export sales. As this symbiotic trade relationship is very important to global markets, weakness on both ends is a very negative read-through for raw material demand.

- Domestic automobile sales in the U.S. drop to their lowest level in three years despite record inventories and incentives, according to ZeroHedge. Auto sales declined again for the month of May marking the fifth-straight month of declines where domestic light vehicle sales came in at 12.6 million, the lowest sales print in more than three years. A negative read-through for raw material demand from a very important end user in the supply chain.

China Region

Strengths

- Geely Automotive (175 HK) jumped to a 23-year high this week after investors digested news on the company’s new stake in Malaysian corporation Proton Holdings Bhd. After supposedly abandoning the bidding process several weeks ago, Geely came back and closed a deal, taking a 49.9 percent stake in Proton, Malaysia’s national carmaker and the owner of British sports car brand Lotus. Geely, which acquired Swedish carmaker Volvo from Ford in 2010 (and which also controls London’s iconic black taxi cab maker London Taxi Company), gains broad access to Southeast Asia out of the Proton deal as well as a dealer network in Asia, Australia and the U.K., with a well-known sports car brand to boot. Geely, which is in the process of rolling out its own Chinese-produced luxury brand, Lynk & Co., and which has already created synergies between its Volvo brand and domestic Chinese brands, can presumably make good use of the technologies from its new acquisitions while gaining access to a larger potential export market and growth in the ASEAN region. Chinese bank CICC raised its price target on Geely—which was one of the best performers in the HSCI for the week—by 33 percent.

- The Hang Seng Composite Index (HSCI) itself constituted the strongest index in the region, rising 1.18 percent for the week to new multiyear highs.

- South Korea’s final first quarter GDP reading came in better than expected, rising to a 1.1 percent quarter-over-quarter print from last month’s 0.9 (0.9 exp.) and to a 2.9 percent year-over-year print from last month’s 2.7 percent (2.7 exp.)

Weaknesses

- While the official China Manufacturing PMI came in slightly better than expected at 51.2 (51.0 exp.), the Caixin China Manufacturing PMI slipped into theoretically contractionary territory at 49.6, down from last month’s 50.3 print and below expectations for a 50.1 showing.

- China’s Shanghai Composite finished the week down mildly, off about 13 basis points in total return, and was kept company by Thailand’s SET Index, which declined about 10 basis points in total return, and Vietnam, which finished down for the week, off some 56 basis points.

- The Nikkei Vietnam Manufacturing PMI declined to 51.6 from April’s showing of 54.1.

Opportunities

- In a somewhat counterintuitive twist, a Bloomberg News article observes that even as their ranks rise, actual “[w]ages for China’s newest college graduates are plunging.” This certainly sounds bad. However, the article observes, the situation may well “aid policy makers striving to shift the economy into higher technology industries and services” by creating an army of relatively highly-qualified workers ready to fill the ranks of the state’s desired industries.

- The Nikkei Philippines Manufacturing PMI is back on the upswing with a 54.3 print, up from April’s 53.3 number.

- China’s offshore renminbi has declined, narrowing with the onshore yuan and signaling, perhaps, that funding worries may be on the decline as well.

Threats

- While there are reportedly a number of reasons not to suspect the brutal Manila casino attack as related in any way to Islamic State—which did claim responsibility for the attack, as propagandists are wont to do—when combined with perceptions of the ongoing violence in the southern part of the Philippines and potential fears of any further attacks, there could be economic repercussions.

- Thai exports declined to a 5.9 percent year-over-year growth rate from April’s 10.8 percent, even as the baht appreciated to 52-week highs (lows).

- While there appears to be consensus among analysts that China‘s pace of growth likely peaked in the first quarter for 2017, weaker data are usually not, on the whole, particularly good things, even if they remain somewhat expected.

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 2.3 percent. A gauge of Hungary’s manufacturing activity pointed to a record pace of expansion, boosted by output, new orders and higher employment, according to index publisher MLBKT. Manufacturing PMI rose to 62.1 in May from a revised 56.2 in April.

- The Turkish lira was the best performing currency this week, gaining 1.97 percent against the dollar.

- The consumer discretionary sector was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 2.71 percent. The Moscow stock exchange corrected with lower oil prices and deepening U.S. probes into whether President Donald Trump or his associates had improper contact with Russia prior to the U.S. presidential elections.

- The Russian ruble was the worst performing currency this week, losing 19 basis points against the dollar.

- The energy sector was the worst performing sector among eastern European markets this week

Opportunities

- The economic sentiment index (ESI) jumped to its highest level in Hungary since at least 2001, and in Romania to its highest in 8.5 years, suggesting strong economic momentum. Central emerging Europe continues to benefit from fast-rising employment and solid wage gains, which help to support an increase in consumer and services confidence.

- Greek Finance Minister Euclid Tsakalotos wants the nation’s debt included in the European Central Bank’s (ECB) bond-buying program even without a final debt agreement. The next big opportunity for Greek economic growth is to have access to the bond market and end its reliance on bailout loans from European government. A decision by the ECB to buy Greek debt would greatly boost investor confidence, but the ECB previously has said it won’t add Greece to its QE program until the International Monetary Fund says Greece’s debt is sustainable.

- In Turkey tourist arrivals rose 18 percent year-over-year to just over 2 million in April, nearly a year after Turkey apologized to Russia for the jet incident. A tourism recovery is crucial for Turkey, which relies on the foreign-exchange revenue to plug part of a current-account gap predicted to reach 4.7 percent of gross domestic product this year, according to estimates compiled by Bloomberg.

Threats

- German Chancellor Angela Marker said the U.S. is no longer a reliable partner for Europe, following the G7 Summit in Taormina, Sicily on May 27. Trump said on Thursday that he would withdraw U.S. from the Paris climate accord, an agreement signed by the Obama administration on April 22, 2016 between the U.S. and 170 other countries to combat climate change. Currently, roughly 80 percent of America’s energy needs are being met through carbon-based natural resources—mainly coal, natural gas, and oil. Trump’s administration is saying that implementing U.S. regulations to conform to the Paris agreement’s ideals would cripple American carbon-based industries and drive up energy costs, harming American workers and consumers.

- Euro-area economic confidence slipped for the first time this year, dropping to 109.2 in May from a revised 109.7 in April. Consensus was for an increase to 110. Consumer confidence was confirmed at negative 3.3, versus negative 3.6 the previous month.

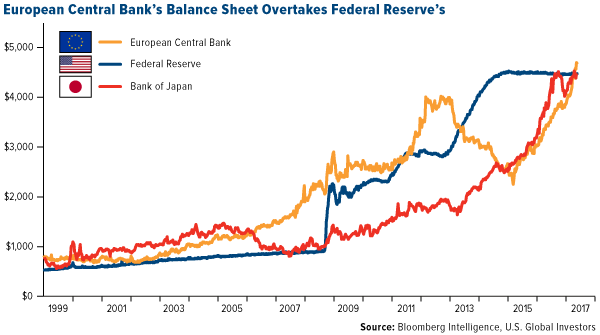

- Mario Draghi said the euro area still needs “an extraordinary amount of money policy support” to push up inflation even as growth picks up. Ongoing asset purchases by the ECB, combined with the strong euro following the French presidential election, have pushed the size of the ECB’s balance sheet above the Federal Reserve’s. The spread is expected to widen further, as the ECB is unlikely to begin tapering until January next year.

© US Global Investors