We Should Be Giving More Credit to Students, Not Less

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsBoth Asha and I are celebrating graduations this month. Congratulations to Jason, Veronica, and the class of 2017!

Seniors and their families approach this milestone with a mix of pride and trepidation. Pride arises from the achievement of heightened status within the community of educated women and men. But there is trepidation about what lies ahead at the next level.

The transition anxiety is compounded by the challenge of financing higher education in America. Many of those who will be matriculating to college are soon to begin accumulating student loans. Many completing college will soon have to start paying off those loans. The amounts involved have grown substantially in the last decade, burdening young professionals.

Some have suggested that U.S. student debt is a $1.4 trillion problem that cries out for restriction and reform. But in the current environment, it is hard to argue for lower levels of investment in human capital. Financial support for students is a problem, all right—in that there isn’t enough of it.

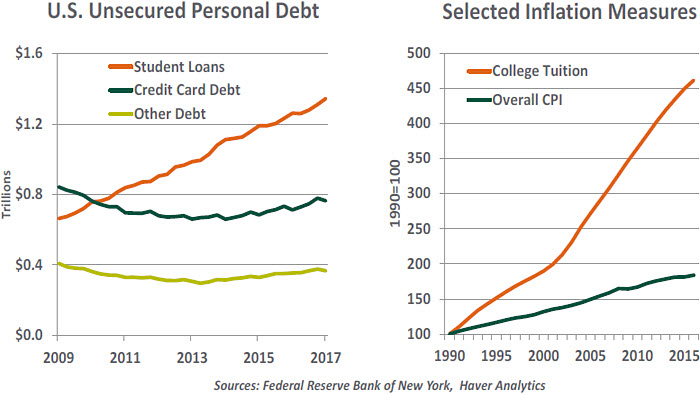

Student loans have grown by more than three times during the past decade, while overall consumer credit has moderated.

Rising college costs are the main contributor to this trend. Tuition and related expenses have grown by more than twice the rate of consumer inflation since 1990. Demand has been higher, as the children of baby boomers form the largest high school graduating classes in American history. Adding to this has been the influx of foreign students attending college in the United States, whose numbers topped one million last year. And an increasing number of adults have returned to school since the 2008 recession, seeking to improve their skill sets.

To help, private colleges have stepped forward with increased grants-in-aid, which currently cover nearly half the stated tuition. But state schools in many parts of the country have had to reduce their support of higher education because of budget challenges. Median household income in the U.S. has grown only modestly in the past decade, and many families have had to dip into their savings during that interval. This combination of circumstances has made students even more reliant on loans to cover college costs.

The vast majority of American student loans are underwritten by the Federal government through the Student Loan Marketing Administration (SLMA). Prior to the 2008 financial crisis, SLMA was increasingly becoming a guarantor of credit originated by private institutions, but reverted to its original mission to ensure the flow of credit to students would not be unduly interrupted.

The vast majority of American student loans are underwritten by the Federal government through the Student Loan Marketing Administration (SLMA). Prior to the 2008 financial crisis, SLMA was increasingly becoming a guarantor of credit originated by private institutions, but reverted to its original mission to ensure the flow of credit to students would not be unduly interrupted. Student loans differ from other forms of consumer credit in several important ways.

-

- Student debt cannot be expunged in bankruptcy proceedings. As a result there are 50- and even 60-year olds who are still carrying educational loans.

-

- Student debt offered by SLMA is not subject to a normal underwriting process. No collateral is required, and candidates actually have to show their financial means are modest, not robust.

-

- Student loans cannot be refinanced unless the borrower qualifies for a private student loan and uses the proceeds to retire the one received from SLMA. Borrowing rates within the bigger federal loan programs were fixed prior to 2013, but have been tied to Treasury rates since. Unfortunately, those who went to school prior to the switch are stuck paying rates that are several hundred basis points higher than they are today.

- Payments on student loans can be calibrated upon request to a borrower’s ability to repay (ATR). For many loan programs, candidates must provide evidence that their payments exceed 10% of their discretionary incomes, and will have their payments lowered to that level upon confirmation.

In the years since the financial crisis, American households have made considerable progress in getting their leverage under better control. Debt as a percentage of household income has dropped to a fifteen year low, and delinquencies on mortgages, credit cards, and auto loans have all fallen precipitously.

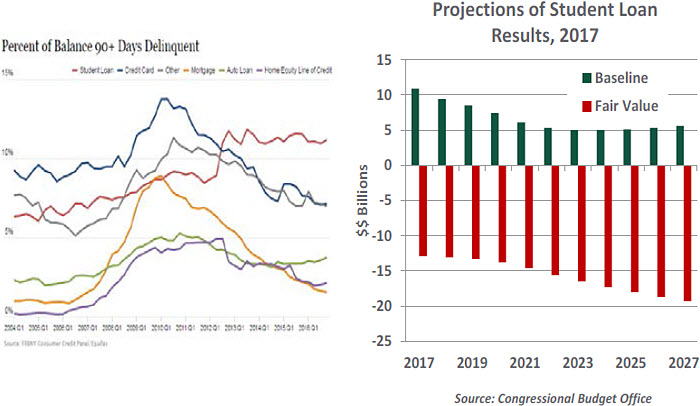

Delinquencies on student loans have been moving in the opposite direction, and now stand at 11% of credit outstanding. Further, loan defaults are rising more rapidly for recent cohorts than they ever have before.

This is, of course, a disappointing outcome for borrowers. Those who encounter trouble retiring their student loans spend less and have difficulty qualifying for other kinds of credit. They are less likely to start a business, get married and own homes. More than a third of college graduates live at home for a least a year after getting their degrees; it has only been in the past year or so that family formation (the economic term for post-college students who strike out to live on their own) has started to rise at more normal levels.

The broader financial consequences of student debt delinquency are not as severe as some might suggest. Suggesting that it will be the basis of the next systemic crisis is an exaggeration.

The cost of defaults is largely borne by the U.S. government, which owns or guarantees most student loans. Because the rates earned on these loans are significantly in excess of current borrowing costs, the Treasury earns an estimated $10 billion from the program under standard accounting. An alternative perspective that takes a more current view of defaults that may occur in the future shows losses of about $12 billion per year. Neither is a significant factor in a federal budget that totals close to $4 trillion.

The cost of defaults is largely borne by the U.S. government, which owns or guarantees most student loans. Because the rates earned on these loans are significantly in excess of current borrowing costs, the Treasury earns an estimated $10 billion from the program under standard accounting. An alternative perspective that takes a more current view of defaults that may occur in the future shows losses of about $12 billion per year. Neither is a significant factor in a federal budget that totals close to $4 trillion. There should, therefore, be plenty of fiscal room for lowering student loan payments. But government policy seems to be turning in the opposite direction. Three years ago, SLMA spun off its servicing operations into a company called Naviant. Naviant has recently come under criticism for charging excessive fees on delinquent borrowers and making the ability-to-repay application process much more difficult to complete. The Consumer Financial Protection Bureau has been called in to look at these concerns.

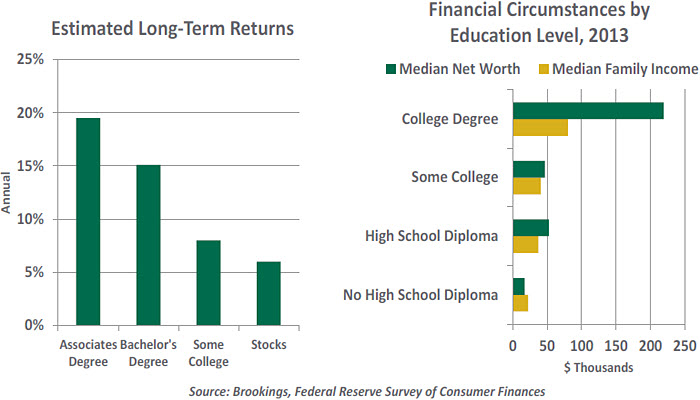

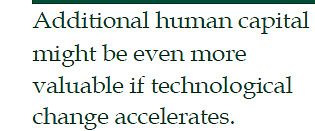

Superior Returns

The accounting results do not capture the most important outcomes of the student loan program: the returns on education. Even with rising tuition, studies have consistently demonstrated that the incremental lifetime earnings that accrue to college graduates are substantial.

Those without college degrees are significantly more likely to be unemployed, suffer from addiction or be imprisoned. The government bears the costs for people in these states, so investing in students can save both money and lives. Further, an educated citizenry adapts better to change, makes more informed decisions and is an advantage in the international competition for investment and corporate headquarters.

There are, however, concerns that the returns on education are diminishing. Studies suggest that more than half the members of recent college graduating classes are doing work that does not require a degree. And in the future, robotics and artificial intelligence are expected to make an increasing impact on the workplace. Since returns to schooling can only be measured in retrospect, it will be some time before we can formulate firm conclusions.

However, the fact that some are working at jobs beneath their education today does not mean that they will always be in that position. Higher levels of education provide both a knowledge base and a signal to employers that support a steeper career trajectory. The impact of automation on work is not new; having a well-trained mind is essential to taking advantage of the change that inevitably presents itself.

Investments in human or physical capital will have some successes and some failures. Done right, the positive outcomes should compensate for those that turn out less well. It may seem cold to apply this logic to people, but if a handful of stars take their student financing and become top innovators and entrepreneurs, they will add to national income in immense amounts. Some of that income might certainly be applied to reducing the debt burden for others.

Proposals for Reform

Observers of the student debt situation in the United States are united by one view: the current condition cannot be allowed to continue. But from there, policy paths diverge.

There are those who would allow more market forces into the student loan equation to bring about a more optimal equilibrium. Returning to a private origination system, with more traditional underwriting, is at the heart of this design. Applications could be screened based on the track record of the education institution to which the student is applying and the potential earnings improvement that the student might achieve.

Interest rates in this regime would be determined as they are for other types of credit, through the intersection of supply and demand. Subsidies for educational loans would be eliminated. (The administration’s recent budget proposal cuts $1 billion from SLMA’s budget on this front.) Moderation in the availability and cost of student debt might not necessarily reduce access to education, as institutions of higher learning might have to respond by lowering their fees.

Others would prefer that the student loan program remain in the public domain and be funded generously. The basic loan contract would be modified from a fixed rate product to one whose interest rate is always set on the borrower’s income. (Australia, Great Britain and New Zealand have implemented this idea, with good results.) This would eliminate the cost and expense of the application process for loan payment relief. Students with debt outstanding after a certain length of time would have the balance forgiven.

Debt forbearance is a touchy subject. Those who know their obligations might be expunged may not be as industrious; those who work hard to stay current might certainly feel aggrieved at this. This was at the center of the debate in the aftermath of the U.S. mortgage meltdown nine years ago. Studies consistently show that principal write-downs are a more effective path to restoring normalcy in a debt market, but most of the “help to homeowner” programs centered on lower interest payments.

Whatever is ultimately decided, we need to accumulate more higher education, not less. The potential for economic growth is based on population and productivity; maximizing educational levels makes for a better-equipped workforce. Today’s successful students become tomorrow’s inventors and entrepreneurs.

If technological disruption does come, better minds will enable the nation to take advantage. If we fail to provide an avenue to economic betterment for those communities who have fallen behind, the threat of a populist response will increase.

If technological disruption does come, better minds will enable the nation to take advantage. If we fail to provide an avenue to economic betterment for those communities who have fallen behind, the threat of a populist response will increase. And at a time when “alternative facts” are being passed off as real information and objective thinking seems to be in deficit, enhancing understanding and critical reasoning is more important than ever.

As for Asha and I, tuition bills will be arriving at our homes before long. (Long before Jason and Veronica start classes, I might add.) We’re more than happy to invest in their futures, for which we have high hopes. As a society, America needs to provide this same support to its children, so that our country can achieve its highest aspirations.

northerntrust.com

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2017 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All