Hope for the Best but Prepare for the Worst (with Gold and Munis)

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThis week investors shrugged off even more drama coming out of Washington. Stocks continued to rally and hit record highs, even as former FBI director James Comey testified that, in his opinion, President Donald Trump fired him in an attempt to lift the “cloud” of the Russia investigation.

If true, this suggests obstruction of justice, an impeachable offense. And if impeached, or in the event of a resignation, Trump’s political agenda would obviously be derailed. The last (and only) time a U.S. president resigned, the Dow Jones Industrial Average lost up to 40 percent, as a recent article in TheStreet reminds us.

But markets paid no mind to Comey’s insinuations, underscoring investors’ confidence that tax reform and deregulation will proceed as planned. And sure enough, just hours after Comey testified, the House of Representatives voted to repeal key parts of the Dodd-Frank Wall Street Reform and Consumer Protection Act, which has contributed to an alarming number of small bank closures since its passage in 2010.

So once again, the wisdom of crowds prevails. If you remember, markets were forecasting as far back ago as last summer that Trump would win the November election.

This doesn’t mean, however, that Trump’s problems are behind him.

This week I was speaking with Mike Ward, a top publisher with Agora Financial, who compared Presidents Trump and Ronald Reagan. It was suggested that, despite Trump’s apparent affection for the 40th president, he has so far failed to live up to the Great Communicator’s memory of optimism and deep respect for the office.

Whereas Reagan wanted to “tear down this wall,” Trump wants to “put up that wall.” Whereas Reagan insisted it was “morning in America,” Trump insists it’s “American carnage.” Reagan succeeded in building coalitions and unifying our allies against the Soviet Union. Trump has already managed to destabilize those alliances.

During the 1988 vice-presidential debate, Texas Senator Lloyd Bentsen famously ribbed then-Senator of Indiana Dan Quale for comparing himself favorably to John F. Kennedy. “I served with Jack Kennedy. I knew Jack Kennedy,” Bentsen said. “Senator, you’re no Jack Kennedy.”

Similarly, many observers are of the opinion that Trump is no Reagan.

Don’t get me wrong. I remain hopeful. President Trump wants to make America great again, and it’s still well within his power to do so—if he can practice some self-restraint and not get caught up in petty feuds. Voters support his vision. They gave him not only the Executive Branch but also Congress and most states’ governorships and legislatures.

You could say I’m hoping for the best but preparing for the worst. I advise investors to do the same. No one can say what the future holds, and it’s prudent to have a portion of your portfolio in gold, gold stocks and short-term, tax-free municipal bonds, all of which have a history of performing well in volatile times.

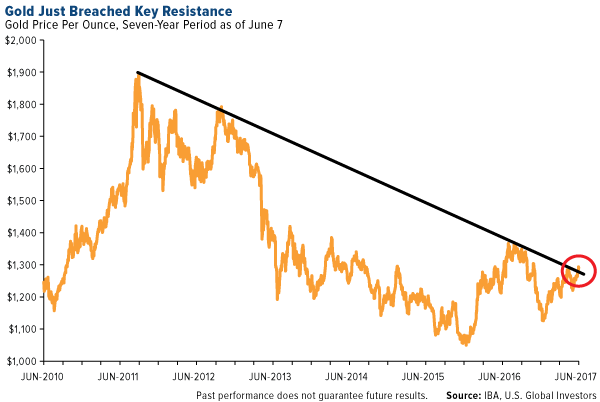

Gold Poised for a Breakout

Following bitcoin’s breathtaking ascent to fresh highs, gold rose to a seven-month high this week on safe-haven demand, stopping just short of the psychologically important $1,300 level. Supported by Fear Trade factors such as geopolitical turmoil—both in the U.S. and abroad—and low to negative government bond yields, gold’s move here can be seen as a bullish sign.

As others have pointed out, the yellow metal breached the downward trend of the past six years, possibly pointing to further gains.

click to enlarge

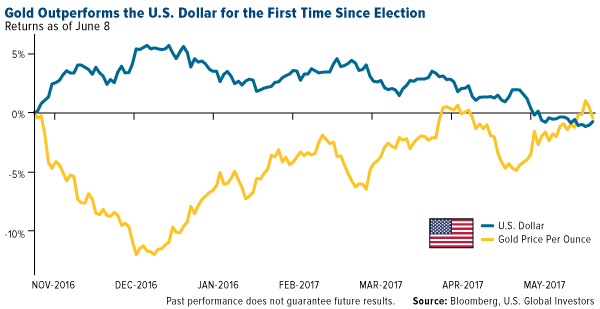

click to enlargeUnder pressure from a beleaguered White House and stalled policy reform, the U.S. dollar continued to sink this week, with gold outperforming the greenback for the first time since the November election. Because gold is priced in dollars, its value increases when the dollar contracts.

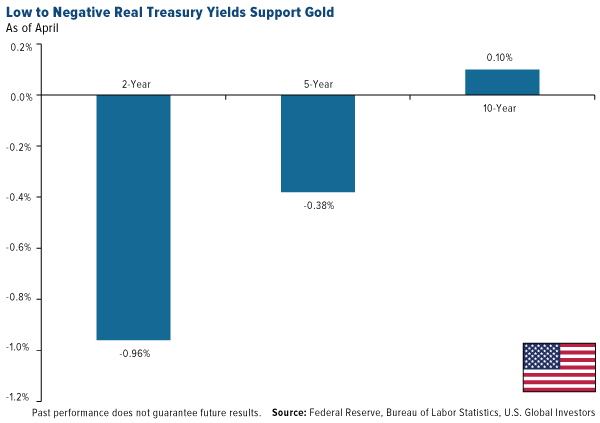

It’s also important for investors to remember that gold has often rallied when Treasuries yielded little or nothing. Why would investors knowingly lock in guaranteed losses for the next two or five years, or near-zero returns for the next 10 years? That’s precisely what Treasuries are offering, as you can see below:

Minus inflation, the two-year Treasury yielded negative 0.96 percent in April; the five-year, negative 0.38 percent; and the 10-year, a paltry 0.10 percent. (I’m using April data since May inflation data won’t be available until next week, but I expect results to look the same.)

When this happens, investors tend to shift into other safe-haven assets, including municipal bonds and gold.

Year-to-date, the yellow metal is up more than 9.7 percent, even as the stock market extends its rally. This runs counter to what we’ve seen in the past. As I’ve explained before, gold usually has a low correlation to other assets, including stocks and bonds, which is why investors all around the globe favor it as a diversifier.

So what gives?

One of the most compelling answers to this question, I believe, is that stocks appear to be overvalued right now, in turn boosting gold’s safe-haven investment case. This is the assessment of Bill Gross, the legendary bond guru who currently manages $2 billion with Janus Henderson.

Speaking at the Bloomberg Invest New York summit this week, the 73-year-old Gross said markets are now at their highest risk levels since before the 2008 financial crisis. Loose monetary policy has artificially inflated stock prices despite weak economic growth, he said, adding: “Instead of buying low and selling high, you’re buying high and crossing your fingers.”

Marc Faber, the Swiss investor often referred to as Dr. Doom, echoed Gross’ thoughts, telling CNBC this week that “everything” is in a bubble right now, similar to the days of the dotcom bust of the late 1990s. And when this bubble bursts, Marc said, investors could lose as much as half of their assets.

That stocks appear overvalued could be a driver of gold’s performance right now, with savvy investors, anticipating a possible market correction, loading up on assets that have historically held their value in times of economic crisis.

A cadre of other top money managers and analysts share Bill Gross and Marc’s less-than-rosy market view.

At the same Bloomberg event, billionaire hedge fund manager Paul Singer—whose firm, Elliott Management, recently raised $5 billion in as little as 24 hours—warned attendees that the U.S. was at risk of another debt shock.

“What we have today is a global financial system that’s just about as leveraged—and in many cases more leveraged—than before 2008, and I don’t think the financial system is more sound,” Singer said.

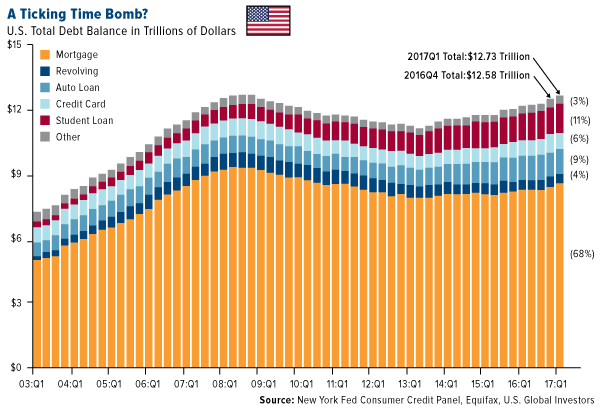

Indeed, U.S. debt levels are higher now than they’ve ever been, according to the Federal Reserve Bank of New York. In the first quarter of 2017, total U.S. household indebtedness reached a mind-boggling $12.73 trillion. That’s $150 billion more than the end of 2016 and $50 billion above the previous peak set in 2008.

Even more concerning is the fact that the number of delinquencies grew for the second straight quarter as more income-strapped Americans binged on credit. We could be headed for a massive hangover.

Cumulatively, these warnings stress the importance of hoping for the best while planning for the worst. In the past, there have been few ways as effective at preserving wealth as gold, gold stocks and tax-free, short-term munis.

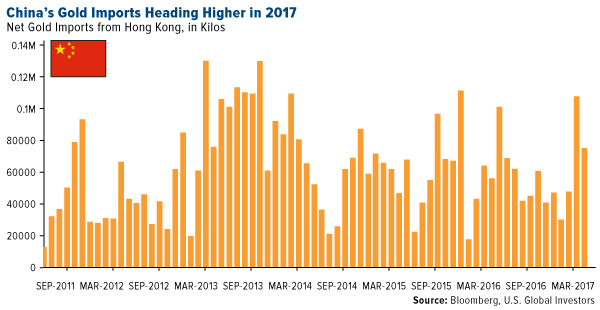

The world’s two largest consumers of gold by far, China and India, are currently importing enormous amounts of the yellow metal on safe-haven demand. Bloomberg reports that China could boost its gold purchases from Hong Kong as much as 50 percent this year over concerns of currency devaluation, a slowing real estate market and shaky stocks. Imports could advance to 1,000 metric tons, which would be the most since 2013.

Meanwhile, India—whose affection for gold goes back millennia—saw its imports of the yellow metal rise fourfold in May compared to the same month last year as traders fear a higher tax rate on jewelry. Imports climbed to 126 tons, versus 31.5 tons last May.

As impressive as this news is, there’s no sign more compelling that investors have an insatiable appetite for gold right now than the growing demand for safety-deposit boxes. According to Bloomberg, companies in Europe are scrambling to meet customers’ needs for a safe, inexpensive place to store their bullion in the face of negative interest rates and rising inflation. Two firms in particular have plans to build additional facilities capable of holding 100 million euros ($112 million) each in bars and coins.

Daniel Marburger, CEO of European coin dealer CoinInvest, told Bloomberg that he had just finished working with a German customer whose bank account was charged negative interest rates. To prevent this from happening again, the customer converted his cash into gold and silver, which he sees as a more reliable store of value.

Negative rates are “definitely a driving factor and will lead to more sales and also more storage clients,” Marburger said.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.31 percent. The S&P 500 Stock Index fell 0.39 percent, while the Nasdaq Composite fell 1.55 percent. The Russell 2000 small capitalization index gained 1.08 percent this week.

- The Hang Seng Composite gained 0.52 percent this week; while Taiwan was up 0.46 percent and the KOSPI rose 0.42 percent.

- The 10-year Treasury bond yield rose 4 basis points to 2.20 percent.

Domestic Equity Market

Strengths

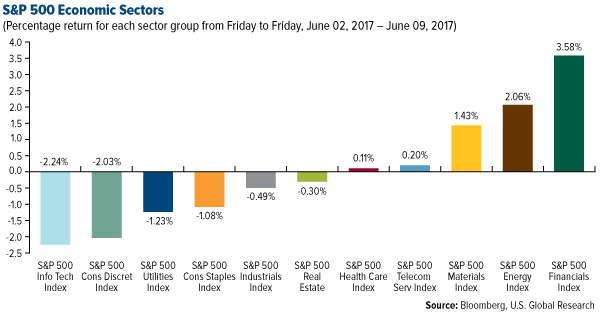

- Financials was the best performing sector of the week, increasing by 3.58 percent versus an overall decrease of 0.37 percent for the S&P 500.

- Advanced Micro Devices was the best performing stock for the week, increasing 12.66 percent.

- Companies flush in cash are outperforming. Companies with strong balance sheets are up 11 percent this year, outpacing those with weaker balance sheets by 3.5 percent, according to data compiled by Goldman Sachs and Bloomberg.

Weaknesses

- Information technology was the worst performing sector for the week, falling 2.24 percent versus an overall decrease of 0.37 percent for the S&P 500.

- Molson Coors Brewing was the worst performing stock for the week, falling 9.77 percent.

- Macy's fell to a six-year low after issuing a warning about its profit margins. The department store chain is suffering from the effects of the retail apocalypse, which is causing store closures across the country.

Opportunities

- An important stock market signal just got its most bullish reading of the year. Options traders are the most unhedged on the S&P 500 since December, showing that they're not particularly worried about the market falling, even with major indices sitting near record highs.

- Apple had its annual developer conference this week and unveiled its Amazon Echo competitor called "HomePod." The company also announced iOS 11, the latest version of its mobile operating system for iPhones and iPads. Furthermore, it launched its own augmented reality software called "ARKit." The goal is to make the iPhone "the largest AR platform in the world," according to software chief Craig Federighi.

- Amazon is targeting Walmart with cheaper Prime rates for lower income shoppers. The company announced on Tuesday that it's going to offer reduced Prime rates for U.S. shoppers who are on government assistance.

Threats

- Hedge funds are stocking up on bets against small-cap stocks, one of the Trump trade's biggest winners. Hedge funds and large speculators hold the biggest net short position in six years on the Russell 2000.

- In their latest analyst note about Snap, JP Morgan downgraded its price target and said it thinks fewer people are joining Snapchat. The bank estimates only 8 million users will join Snapchat in the second quarter of 2017, less than the 10 million that were previously expected. Further, traders are increasing their bets against the company. The put-to-call ratio in the stock has jumped to 1.7 to 1, the highest since March 17, which was the fifth day that Snap options were available to be traded.

- At its latest investor conference, Molson Coors Brewing’s management gave disappointing EBITDA guidance citing rising costs.

|

June 9, 2017 |

June 7, 2017 |

June 7, 2017 |

Strengths

- The World Bank holds its 2017 global growth forecast at 2.7 percent and says the global economy is improving, although risks remain. In its statements, the bank said, "A recovery in industrial activity has coincided with a pick-up in global trade, after two years of marked weakness."

- Europe's growth is above consensus. The euro area grew at a 0.6 percent rate in the first quarter, above the advanced reading of 0.5 percent.

- China's services sector is growing at its fastest rate since the beginning of the year. China's Caixin-IHS Markit services PMI increased 1.3 points to 52.8 in May as new orders grew at a faster pace, while order backlogs also increased.

Weaknesses

- U.S. durable goods orders for April fell 0.8 percent, more than the 0.6 percent drop that was expected.

- The Markit U.S. Services PMI for May came in at 53.6, below the consensus expectation for 54.

- Prime Minister Theresa May’s plan to improve her Brexit bargaining position by calling a snap election did exactly the opposite, increasing the uncertainty around the Brexit process as the Conservative Party lost its outright majority in the House of Commons. May’s political capital has been severely diminished and her role as party leader could be in jeopardy in the near future.

Opportunities

- BCA’s U.S. bond strategists continue to recommend positioning for a steeper yield curve by favoring the five-year bullet versus a duration-matched 2/10-year barbell. That positioning should outperform as TIPS breakevens widen and the curve steepens in the second half of the year.

- Even though U.S. economic data has disappointed this year, there is not much talk of a recession in the media. Further, BCA analysts comment that several of their models show slim chances of an economic contraction. A delay of Trumponomics should prolong the economic expansion and support the economy over the next six to12 months.

- Purchasing managers’ indices released this week show that the eurozone continues to lead other developed economies. The eurozone composite PMI came in at 56.8, unchanged from April. Meanwhile, the U.S. clocked in at 53.6 and the UK at 56.7. Japan’s composite PMI registered 52.6 and China’s 51.5. Nonetheless, all PMI’s remain above 50, a positive outlook for the world economy.

Threats

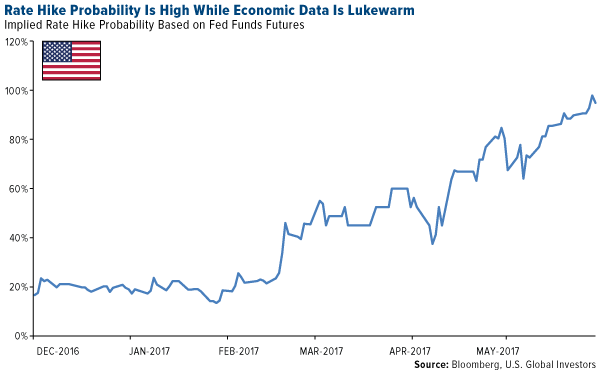

- Given May’s jobs report and sluggish wages as two of several recent signs indicating that the U.S. economy has entered a soft patch, the Federal Reserve should be cautious and refrain from increasing interest rates when the Federal Open Market Committee meets next week. However, the Fed’s monetary policy has been evolving and it is now set on a path to tighten its stance. Rate hike probabilities implied by Fed funds futures currently stand circa 95 percent and have been consistently moving upward in recent weeks.

- U.S. CPI data is announced Wednesday. Following two months of weakness, core CPI needs to show a rebound for the Fed to remain comfortable with the view that inflation will move up to its 2 percent target.

- Retail sales data will also be released Wednesday. The Fed's latest Beige Book noted that household spending "softened with many Districts noting little or no change in non-auto retail sales, while automobile sales have edged down from last year's record highs." The May retail sales report should be watched for hard evidence of sluggish consumer spending.

Gold Market

This week spot gold closed at $1,266.93, down $12.30 per ounce, or 0.96 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.01 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index fell 1.22 percent. The U.S. Trade-Weighted Dollar Index finished the week higher by 0.58 percent.

|

Date |

Event |

Survey |

Actual |

Prior |

|

Jun-5 |

Durable Goods Orders |

-0.6% |

-0.8% |

-0.7% |

|

Jun-8 |

ECB Main Refinancing Rate |

0.000% |

0.000% |

0.000% |

|

Jun-8 |

Initial Jobless Claims |

240k |

245k |

255k |

|

Jun-13 |

ZEW Survey Current Situation |

85.0 |

-- |

83.9 |

|

Jun-13 |

ZEW Survey Expectations |

21.8 |

-- |

20.6 |

|

Jun-13 |

PPI Final Demand YoY |

20.% |

-- |

2.5% |

|

Jun-13 |

China Retail Sales YoY |

10.7% |

-- |

10.7% |

|

Jun-14 |

Germany CPI YoY |

1.5% |

-- |

1.5% |

|

Jun-14 |

U.S. CPI YoY |

2.0% |

-- |

2.2% |

|

Jun-14 |

FOMC Rate Decision – Upper Bound |

1.25% |

-- |

1.00% |

|

Jun-15 |

Initial Jobless Claims |

242k |

-- |

245k |

|

Jun-16 |

Eurozone CPI Core YoY |

0.9% |

-- |

0.9% |

|

Jun-16 |

Housing Starts |

1220k |

-- |

1172k |

Strengths

- The best performing precious metal for the week was palladium, up 5.10 percent. Grant Sporre, an analyst at Deutsche Bank, noted there is a genuine physical tightness in the market, but the spike had all the hallmarks of someone being caught short and being squeezed. Bullionvault’s Gold Investor Index, which measures the balance of client buyers against sellers, rose the most in two years reaching a high of 55.3 in May versus 52.1 in April, reports Bloomberg. In India, gold imports jumped fourfold in May to 126 metric tons from 31.5 metric tons in the same month last year. In a report by the World Gold Council, consumption in India could climb dramatically this year as a “simple” nationwide Goods Services Tax will boost the economy, making the gold industry more transparent to benefit buyers, reports Bloomberg.

- Amid unease over a congressional hearing on possible links between Russia and the Trump campaign, holdings in SPDR Gold Shares (the world’s largest gold-backed ETF) climbed to the highest this year on the back of safe-haven demand, reports Bloomberg. In the two weeks through the end of May, hedge funds and other large speculators boosted their bullish bets on the precious metal by 37 percent, notes another Bloomberg article, the most since 2007 according to government data.

- Japanese investors sold a record amount of U.S. debt in April, reports Bloomberg. “Political turmoil in Washington and uncertainty about French elections pushed down Treasury yields, diminishing their attractiveness,” the article continues. Japanese investors cut holdings of U.S. debt by $33.2 billion in April, the most in data going back to 2005, according to a Ministry of Finance balance-of-payments report.

Weaknesses

- The worst performing precious metal for the week was silver, off 1.90 percent and largely in sync with the fall in gold. Data from the People’s Bank of China show that the Asian nation kept its gold reserves unchanged for the fifth straight month. Holdings stand at 59.24 million ounces for the end of May, the same level since the end of October. UBS commented on the moves in a report this week. “We maintain our base case that purchases should resume up ahead as overall official reserves stabilize, given that the diversification argument remains intact,” writes Joni Teves at UBS. “Nevertheless, we acknowledge growing risks to this view considering that the pause in buying has gone on longer than we initially expected.”

- According to an emailed statement from the Athens-based Energy Ministry, the Greek government will seek arbitration against Hellas Gold to “ensure contractual obligations of the company,” reports Bloomberg. The compliance measures are in reference to Kassandra mines in northern Greece. On the flip side of things, Eldorado Gold says is hasn’t been notified of the Greek arbitration, and says it operates in accordance with all applicable laws and regulations in jurisdictions where it conducts business.

- Employees at Freeport McMoRan’s Grasberg mine in Indonesia who stopped showing up for work in mid-April (totaling 4,000 employees and contractors), are in the process of being replaced, reports Bloomberg. Freeport CFO Kathleen Quirk said in a presentation in Chicago that all 4,000 are deemed to have resigned. The company’s top priority for the remainder of 2017 is getting a long-term extension to operating rights in Indonesia.

Opportunities

- A rush to haven assets has led to two firms saying they plan to open vaults in Europe capable of holding more than 100 million euros in gold, reports Bloomberg. This would offer customers lower costs that ETPs as well as protection from rising prices. “Inflation is a key concern for many of our clients,” said Ross Norman, CEO of Sharps Pixley. In a related note, China (the world’s biggest gold market) could boost its imports through Hong Kong by about half this year, as investors seek to protect their wealth from currency risks, reports Bloomberg. In fact, China’s gold imports are already heading higher in 2017. A slowing property market and volatile stocks also add to the safe-haven allure, according to the Chinese Gold & Silver Exchange Society.

- In its Global Precious Metals Comment this week, UBS writes that gold’s strength is justified by macro forces. “In particular, lower rates, weaker dollar and broader uncertainty provide good foundation for the market to continue its journey higher,” the report reads. The group adds that gold’s use as a portfolio diversifier has become increasingly relevant in the current environment and that despite the rally from May lows, UBS believes gold positioning is not crowded overall and there should still be room for the move to extend.

- Sean Casey, contributing analyst with Bloomberg, writes “Commodities’ negative correlation to the dollar has never been more stressed in the Bloomberg Dollar Spot Index’s 13-year history.” The note continues by stating that commodities could rally 20 percent just by catching up to the declining dollar. Over the past 26 weeks the dollar is down 6.1 percent and the Bloomberg Commodity Index is down 2.2 percent. “This unusual disparity has never happened since the dollar index’s start in 2004,” the article continues. “In the 73 weeks where the dollar ended down 5 percent or more on a 26-week basis, commodities have increased 20 percent on average.”

- Mexico’s tax agency owes Canadian mining companies over $360 million in tax rebates, reports Reuters and Bloomberg. The sum includes $230 million owed to Goldcorp and $66.5 million to Torex Gold Resources, just to name a few. “It’s damaging the ability to reinvest the dollars in assets that actually pay real tax,” said Torex chief executive Fred Stanford. The situation proves even more difficult for smaller, cash-strapped miners and explorers.

- A note from Global Mining Research this week states that wholesale electricity prices have nearly tripled over the last 18 months in Australia, primarily driven by capacity closures and higher gas costs, according to Energy Australia. Although short-term fluctuations are nothing new, “these price increases look here to stay with new generation capacity needed.” The mining industry in South Africa is also facing cost pressure. Its new mining charter will be gazetted and become law next week, Mineral Resource Minister Mosebenzi Zwane said Tuesday. The mining industry doesn’t think it has been consulted enough on these changes and is thus losing investment. Similarly, Tanzania plans to introduce a 1 percent clearing fee on the value of mineral exports in 2017/18, according to its finance minister, part of government measures aimed at getting a bigger share of revenues from tis natural resources.

- Mitsubishi Materials Corp. processed 20 percent of all electronic waste gathered globally last year to recover gold, silver and copper, reports Bloomberg. The “urban miner” plans to expand processing capacity by 14 percent to 160,000 tons next year, according to senior managing executive officer Yasunobu Suzuki. The company plans to open a facility in the Netherlands in November to collect waste in Europe for processing at its Japanese facilities and should be additive to recycled gold supply.

Energy and Natural Resources Market

Strengths

- Zinc was the best performing commodity this week, rallying 5.4 percent. After a shaky start to 2017, zinc prices are beginning to pick up steam again on the back of favorable fundamentals. As zinc inventories have been declining for the past five years and China has disappointed with weak infrastructure data, zinc has fallen out of favor. Positive data coming out of China recently may be the beginning of a change in zinc’s trajectory. According to Kitco, global demand for zinc is currently north of 14,000 tonnes per year; however, supply is just under 13,000 tonnes per year. If trade and infrastructure data out of China continue to gain momentum on the upside, zinc prices may have further room to run in the months to come.

- The best performing sector this week was the S&P/TSX Diversified Metals and Mining Sub Industry Index. The index rose 5 percent on the back of base metals rallying across the complex this week.

- Freeport-McMoran Inc, the largest copper producer in the world headquartered in Arizona, was the best performing stock this week, finishing up 9.6 percent. The stock rose on the back of rallying copper prices this week.

Weaknesses

- Crude oil was the worst performing commodity this week, dropping 3.8 percent. The commodity fell substantially this week after an unexpected increase in U.S. inventories of 3.3 million barrels according to the U.S. Energy Information Administration (EIA). Investors are beginning to fear whether or not output cuts by major producers have done much to drain a global glut, according to Reuters.

- The worst performing sector this week was the BI Global Integrated Oils Valuation Peers Index. The index fell 0.6 percent on the back of falling crude oil prices.

- The worst performing stock for the week was Fibria Celulose SA, a pulp and paper company based in Brazil. The company fell 5 percent on the back of negative investor sentiment.

Opportunities

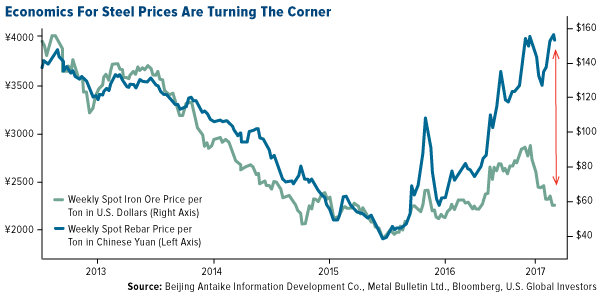

- Despite iron ore’s tumultuous price action over the last couple of months, the world’s top steelmaker, China, may have a shortage of steel according to Bloomberg this week. Months ago, stockpiles of iron ore held at ports in China acted as the catalyst for the violent drop in iron ore prices which spurred the Chinese government and group of seven policymakers to shut down outdated plants. These drastic actions have fortunately helped clean up excess supplies and put a lid on falling prices. Now steel mills may have an opportunity to increase profit margins on production in the months ahead in attempts to service the region’s current insatiable demand for rebar, which bodes well for steelmakers.

- China’s exports rose in the month of May as global trade outlook brightened, according to Bloomberg this week. A brighter global outlook is helping support China’s manufacturing machine where exports rose more than 8.7 percent in May, a more than 7.2 percent increase from economists’ forecasts. Imports also surged 14.8 percent, which was more than an 8.3 percent forecast. This marks a very positive turnaround in trade data which started the year on a negative note and may imply that domestic demand could hold up in the months to come, increasing demand and prices for raw materials.

- Electric car demand has sparked lithium supply fears according to the Financial Times this week. Concerns are beginning to mount among analysts and carmakers who believe lithium supply will not be able to keep pace with demand as the expansion of electric vehicles gains momentum. Reg Spencer, an analyst at Canaccord Genuity, cites that it took many years for iron ore supply to catch up with demand and this might be the case in battery materials if capital is not available to develop new projects. These factors may usher in a supercycle for lithium if fundamentals of the commodity line up.

Threats

- Bloomberg reports that on Wednesday, the Organisation for Economic Co-operation and Development (OECD) warned world leaders that politics surrounding protectionist policies are at risk of undermining a true recovery in investment and have instead distorted an improvement in the global economy without showing real progress. Catherine Mann, Chief Economist of the OECD, states that protectionist policies in the G-20 are creating reservations among investors and investment has been a missing element of support for global growth, trade, production and real wages. Mann further states that geopolitical shocks and trade protectionism could create snap backs in asset prices and realize downside risks through a variety of channels.

- Major investment banks, JP Morgan and Goldman Sachs, slashed their oil price targets for 2018 this week according to OilPrice.com. Both banks have cited that the largest factors affecting their forecasts are U.S. shale production that is expected to continue growing well into 2018 and OPEC’s extension deal as having no clear exit strategy or end game in sight. Of the two banks, JP Morgan is drastically cutting its price target down by 11 dollars for 2018, from 53 dollars to 42 dollars.

- European investors sell commodity ETFs as positive sentiment fades surrounding U.S. infrastructure investment and China’s growth, according to the Financial Times this week. Concerns surrounding the outlook for oil and metals from European investors have prompted the largest outflows in six months of $150 million from commodity ETFs. Chief commodities economist at Capital Economics, Caroline Bain, said that despite a massive amount of optimism coming into the year, the market has entered into a period of recalibration of what the prospects truly are.

China Region

Strengths

- China’s Shanghai Composite Index finished the week up 1.80 percent, tops in the region. Vietnam also had a strong week, with the Vietnam Ho Chi Minh Stock Index up almost 1.5 percent in the same timeframe.

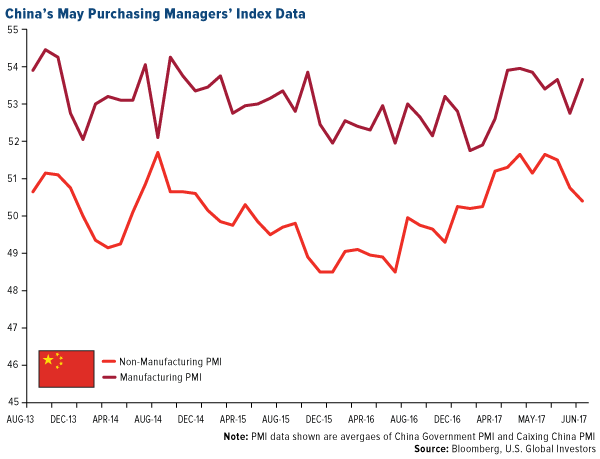

- Official Non-Manufacturing PMI for China came in at 54.5, up from April’s 54.0, and the Caixin China Services PMI reading for May came in at 52.8, up from the prior month’s reading of 51.5.

- AAC Technologies (2018 HK) soared 22.19 percent this week, the strongest gainer in the Hang Seng Composite Index. The electronics components maker reopened to investor optimism after an independent review of the company’s financials appeared to refute a negative short report. Moreover, the company reported late in the week that CITIC Bank will supply a two year, 10 billion yuan line of credit, perhaps making things more difficult for short sellers.

Weaknesses

- Indonesia’s Jakarta Composite Index fell 1.17 percent for the week, making it one of the weakest performers in the region. Cambodia’s CSX Index declined 1.43 percent, falling even more than Indonesia.

- South Korea’s won fell about 44 basis points on the week, leaving it among the region’s worst performers for the timeframe.

- Advertising and marketing company Wisdom Sports Group (1661 HK) was the worst performer in the HSCI for the week, tumbling 20.0 percent.

- Year-over-year imports rose 22.1 percent, well ahead of 16.1 percent expectations, while year-over-year exports rose 8.7 percent, up from last month’s 8.0 percent reading and ahead of analysts’ expectations for a gain of 7.2 percent.

- China’s Foreign Reserves level came in at $3.054 trillion, stable and slightly ahead of expectations for a 3.046 trillion print.

- Internet giant Alibaba Group Holding Ltd. (BABA US) reported strong earnings and a positive outlook for e-commerce on the year. Shares climbed to new record highs this week.

Threats

- North Korea launched a series of short-range missiles this week following South Korean President Moon’s promised suspension of the deployment of the THAAD shield.

- Bloomberg News reported this week that China may halt new electric car permits on concerns about a possible glut in supply.

- Some central banking policies may continue to play outsized roles for both debt and equities across the region.

Emerging Europe

Strengths

- Ukraine was the best performing country this week, up 94 basis points.

- The Ukrainian hryvnia was the best performing currency this week, up 48 basis points.

- Consumer staples was the best performing sector among eastern European markets this week.

Weaknesses

- Romania was the worst performing country this week, down 2.90 percent.

- The Polish zloty was the worst performing currency this week, losing 79 basis points against the U.S. dollar. The Polish central bank left the rate at a record low of 1.5 percent on Wednesday, in line with expectations, with governor Adam Glapinski reiterating he’d “be surprised” if rates were raised in 2018. Investors continue to watch global risk events after Poland’s central bank maintained its wait-and-see policy stance.

- Real estate was the worst performing sector among eastern European markets this week.

Opportunities

- The preliminary Euro-area composite PMI stood at 56.8 in May, unchanged from the multi-year high already reached in April. A small decline in the services PMI at 56.2 was offset by an increase in the manufacturing element at 57. Growth continues to look strong, confirming the view that the economy is enjoying positive momentum. However, the inflation outlook remains weak, and as a result, policy makers will likely stay put until September before unveiling a tapering of quantitative easing for 2018.

- Poland is one of the European nations dealing with the fallout of once-popular Swiss-franc mortgages. Their holders suffered a shock in 2015, when Switzerland ditched its peg to the euro, sending the franc 16 percent higher in a month. Poland’s banks, regulators and lawmakers have been locked in a yearlong argument over how to unwind $42 billion in foreign-currency loans without jeopardizing the economy. Duda’s legislation envisions that banks give customers part of the money they pocketed from “excess” spreads in currency-exchange transactions linked to such loans. In its current shape it would cost banks as much as 9.1 billion zloty ($2.4 billion), or 65 percent of the industry’s 2016 profit, according to estimates of the Financial Supervision Commission. Polish President Duda may modify legislation regarding FX spreads charged by lenders, currently debated by lawmakers, to ensure it doesn’t destabilize banks.

- According to Bloomberg, the European Union’s eastern members no longer need to rely solely on household spending and exports to drive its economies. A breakdown of first-quarter GDP shows investment activity is recovering across the region, following a slump in construction last year caused by weaker inflows of EU funds. The pickup accounted for almost the entire Hungarian growth in the first quarter, while in the Czech Republic, investment knocked only 0.2 percentage points off its economic expansion.

Threats

- Turkey’s annual inflation rate fell to 11.72 percent from 11.87 percent the previous month. Still, inflation remains well above the 3 to 7 percent target range and further tightening will be needed. The next central bank policy meeting is June 15, and another hike in the late liquidity window rate is possible.

- It looks like Turkey could get caught up in yet another regional conflict. A group of countries including Saudi Arabia, the United Arab Emirates and Bahrain severed diplomatic and commercial ties with Qatar earlier this week, accusing the Gulf emirate of supporting terrorist groups ranging from Shiite Iranian proxies to Sunni militants such as the Islamic State. President Erdogan has criticized the Saudi-led move to isolate Qatar, and his party has asked to fast-track approval for putting Turkish troops on the ground in Qatar. Qatar is a major investor in Turkey’s $857 billion economy, with interests in media, financial and defense companies, and Turkey is building a base in the emirate. If conflict escalates, the Turkish lira may also be pressured as some Turkish banks have Qatari ownership.

- The snap election on Thursday backfired badly on Prime Minister Theresa May, leaving no party with overall control in Parliament. The pound tumbled as the U.K.’s ruling Conservative Party lost its parliamentary majority, plunging the country into uncertainty just days before Brexit negotiations were due to start.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits