Small-Cap Mining Stocks, Big-Time Opportunity

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Last month I told you about the upcoming rebalance of the hugely popular VanEck Vectors Junior Gold Miners ETF (GDXJ), and how it would distress shares of junior, small-cap mining stocks. I said then that the rebalance could create some excellent opportunities for astute investors to accumulate high-quality, well-managed producers at discount prices.

That day has finally arrived, bringing with it a tsunami in the junior resource space, as I told Collin Kettell on Palisade Radio this week. It’s a buyer’s market—if you know what you’re looking for. The last time the GDXJ underwent a rebalance of this magnitude was in December 2014, so I see this as a rare event savvy investors shouldn’t miss out on.

But first a reminder of what’s been happening with the GDXJ. Basically, it had become too massive for its underlying index—composed mostly of Canadian junior gold producers—with assets rising close to $5.5 billion earlier this year, up from $1 billion only last year.

Mo Money Mo Problems

Normally this wouldn’t be such a concern. But the GDXJ was getting precariously close to owning a 20 percent share of several names in its index, which would have triggered all sorts of regulatory and tax conundrums in Canada and the U.S.

So the fund made several adjustments to its methodology, including raising the market cap threshold of allowable companies to $2.9 billion, up sharply from $1.6 billion. This means it can now hold large producers that don’t appear in its index, the MVIS Global Junior Gold Miners Index. It also means that a number of smaller constituents were down-weighted or divested altogether, giving investors less exposure to junior miners than what the fund’s name implies.

Before any of this took effect, though, many investors, hedge funds and other market participants acted on the rebalance news by indiscriminately selling down their junior mining assets. This introduced fresh volatility to underlying stocks and depreciated prices.

The selloff, I might add, was done mostly without regard for the phenomenal fundamentals and growth profiles some of these companies reported.

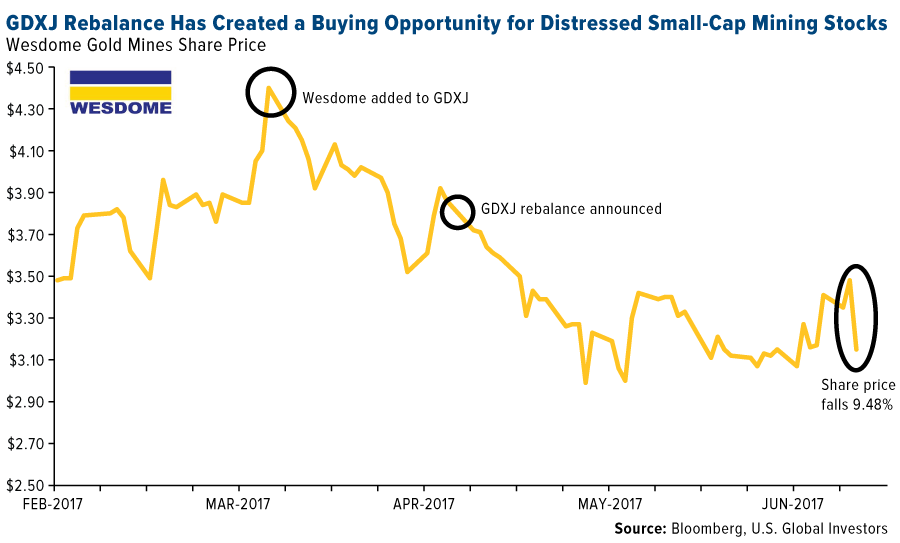

Take one of our favorite names, Wesdome Gold Mines. The Toronto-based producer has been operating in Canada for 30 straight years as of 2017 and currently carries no debt. Two of its mines, Eagle River and Mishi, are among Canada’s highest-grade gold mines. Last summer, the company made headlines when it discovered gold at its Kiena property in Quebec, sending its stock up an amazing 49 percent to $2.24 on August 25.

When Wesdome was added to the GDXJ in March, it cast newfound attention on the $417 million company. Only a month later, the rebalance was announced, and since then, its stock has eased about 19 percent.

I see this as a can’t-miss opportunity for retail and institutional investors to start nibbling on Wesdome and other junior miners that have been similarly knocked down only because of fund flows.

That includes Gran Colombia Gold, the largest gold and silver producer in Colombia, and Klondex Mines, whose Fire Creek Mine in Nevada was estimated to be the highest-grade underground gold mine in the world. (According to IntelligenceMine, Fire Creek averaged 44.1 grams per metric ton (g/t) in 2015, double the ore grade of the world’s number two project, Kirkland Lake Gold’s Macassa Mine, at 22.2 g/t.)

Gran Colombia announced this week that it produced 15,444 ounces of gold in May, representing a new monthly record for the company. This brings the total amount for the first five months of the year to 68,783 ounces, an impressive 21 percent increase over the same period last year. The Canadian-based producer has a very attractive convertible bond that pays monthly.

I’ve frequently praised Klondex for its frugality, strong revenue growth and exceptional management team. The last time I visited Vancouver, I had the opportunity to chat one-on-one with its president and CEO, Paul Andre Hurt, who has 30 years of experience in high-grade mining. Not only is Paul a highly-respected chief executive in the mining space, he’s also a devoted father of five.

The GDXJ rebalance represents a rare opportunity to accumulate high-quality junior producers at discount prices. I always recommend a 10 percent weighting in gold—5 percent in gold stocks or mutual funds, 5 percent in bars, coins and jewelry.

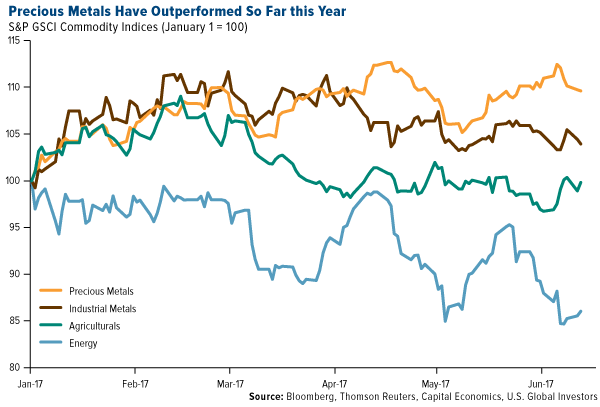

Commodity prices have lately underperformed equities mostly on subdued oil demand growth, with the S&P GSCI commodity index falling about 4 percent over the last month. If we separate the index components, however, we see that precious metals have posted positive gains year-to-date along with industrial metals.

As I mentioned last week, gold imports in China and India, the world’s top two consumers of the yellow metal, have advanced strongly this year on safe haven demand. China boosted its gold purchases from Hong Kong as much as 50 percent this year to 1,000 metric tons, the most since 2013. India’s imports rose fourfold in May compared to the same month last year as traders fear a higher tax rate on jewelry.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.53 percent. The S&P 500 Stock Index 0.06 percent, while the Nasdaq Composite fell 0.90 percent. The Russell 2000 small capitalization index lost 1.05 percent this week.

- The Hang Seng Composite lost 1.60 percent this week; while Taiwan was down 0.42 percent and the KOSPI fell 0.83 percent.

- The 10-year Treasury bond yield fell 4 basis points to 2.15 percent.

Domestic Equity Market

Strengths

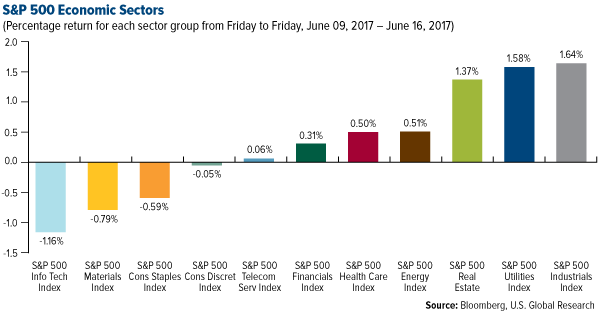

- Industrials was the best performing sector of the week, increasing by 1.64 percent versus an overall decrease of 0.06 percent for the S&P 500.

- Whole Foods Market was the best performing stock for the week, increasing 19.45 percent.

- H&R Block set a new high after fourth quarter profit beat expectations. The company reported fourth quarter earnings per share (EPS) of $3.76, up from $3.16 in the prior year period. Analysts expected EPS of $3.53.

Weaknesses

- Information technology was the worst performing sector for the week, falling 1.16 percent versus an overall decrease of 0.06 percent for the S&P 500.

- Kroger was the worst performing stock for the week, falling 27.58 percent.

- Institutional Shareholder Services is calling for Mylan investors to unseat all of the company’s incumbent board of directors. The shareholder advisory firm has cited “material failures of risk oversight,” including missteps during a pricing controversy over its EpiPen allergy shot that has dragged the company’s stock price down.

Opportunities

- Amazon.com is buying Whole Foods Market in a deal that shocked the grocery industry and set analysts speculating about the next move in a huge sector that Amazon has been trying to crack for a decade. The purchase gives the e-commerce giant, which has been experimenting with various physical grocery concepts and online food delivery, an instant footprint of 460 high-end brick-and-mortar stores across the U.S., in Canada and in the U.K.

- Apple’s latest project is to turn your iPhone into a one-stop shop for all your medical info, CNBC reports. The firm reportedly wants your iPhone to hold everything from a record of your doctor's appointments to your prescriptions. Additionally, CEO Tim Cook confirmed Apple is working on self-driving car technology. He said the company views it "as the mother of all AI projects."

- Morgan Stanley analyst Matthew Harrison reiterated his “overweight” rating on shares of Alexion after Paul Clancy leaves Biogen to fill the open CFO position. The analyst sees "Clancy as a highly credible choice that should help to remove fears around near-term Soliris stability". Paul Clancy comes to Alexion from Biogen where he had been CFO for 10 years. The analyst sees Clancy as a strong CFO who is well liked by investors and should be viewed as a stabilizing force for the company.

Threats

- A winning trade this year has been to short volatility in the market. However, JPMorgan's quant strategist warns it's not going to last, and when the shift comes, it's going to hurt bad. A big reason why shorting volatility can be dangerous is the ever-present possibility that the market will make an unexpectedly sharp move, according to Marko Kolanovic, the firm's global head of macro quantitative and derivatives strategy. The best recent example of this came on May 17, when the S&P 500 slipped 1.8 percent, only to make back most of the loss over the following week. Still, the damage to volatility bears was done, with the VIX — also known as the S&P 500 fear gauge — spiking as much as 46 percent to 15.56. He sees this happening if the VIX, which has been hovering between 10-12, spikes up to 20, near the average level for the gauge. So why is volatility so low in the first place? Kolanovic argues it's due to a series of unsustainable factors, including low correlations. With stocks moving more independently of one another, it's more difficult for them to gather momentum in a particular direction, keeping price swings subdued. However, he thinks the current low levels of volatility are not a new normal and will not last long given the amount of leverage, rising rates, and impending unwinding of the Fed’s balance sheet.

- Credit Suisse put together a list of the large-cap stocks that hedge funds are dropping. These are stocks that, in many cases, a lot of funds still own, but that saw a big reduction in the number of funds investing in them during the first quarter of this year. A large number of hedge funds selling a stock could be an indicator of a not-so-bright future for the company. The list is as follows: Targa Resources, General Motors, Gilead Sciences, United Parcel Service, Reynolds American, Time Warner, Target, General Electric, Bristol-Myers Squibb, Mead Johnson Nutrition, Qualcomm.

- Snap has been struggling since its IPO. The company is still working to court the marketing industry. A mere 7 percent of marketers said they used Snapchat in the first quarter of 2017, according to a recent Social Media Examiner survey charted for us by Statista. That leaves Snap far behind Facebook, its direct competitor, which was used by 94 percent of marketers. However, everyone tends to trail Facebook. Perhaps more tellingly, other social networks like Twitter and Pinterest also attract a greater share of marketers than Snap.

June 15, 2017One Easy Way to Invest in the “Asian Century” |

June 12, 2017Hope for the Best but Prepare for the Worst (with Gold and Munis) |

June 6, 2017In Gold We Trust |

Strengths

- China's retail sales rose 10.7 percent year-over-year in May, according to data released Wednesday by the National Bureau of Statistics. That was above the 10.6 percent that economists had anticipated. China is the world’s second largest economy.

- Manufacturing in New York state rebounded this month to the highest level since 2014, another sign of strength for America's factories. The Empire State Index only measures sentiment in New York, but economists track it because it provides an early read on factory output nationwide. The Empire State Manufacturing Index climbed to 19.8 after falling to minus-1 in May.

- The NFIB’s latest Small Business Survey was released this week, showing a continuation of the historically high levels of business confidence that emerged following the November election. The May survey came in at 104.5, unchanged from the previous month.

Weaknesses

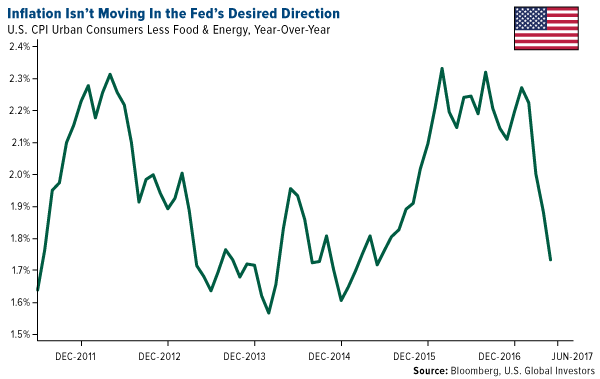

- The consumer price index (CPI) fell more than expected in May, dropping 0.1 percent and missing the forecast for a flat reading. It rose 1.9 percent year-on-year, less than the 2.2 percent expected.

- Retail sales fell 0.3 percent in May, the most in 16 months.

- The preliminary University of Michigan Sentiment Index for June came in at 94.5, below expectations of 97.0.

Opportunities

- The Federal Reserve raised its growth outlook for the U.S. economy. It now expects real GDP to rise 2.1 percent to 2.2 percent in 2017, compared to its previous outlook of 2.0 percent to 2.2 percent. It also expects the unemployment rate to fall to 4.2 to 4.3 percent this year, down from its previous projection of 4.5 percent to 4.6 percent.

- The all-important Eurozone flash purchasing manager’s index (PMI) readings will be released next Friday. Recent PMIs have been strong and consistent with over 2 percent real GDP growth for the euro area.

- The Leading Index coming out next week will be an important gauge of future expectations for the economy. The consensus is for a positive 0.4 percent, ahead of the previous 0.3 percent mark.

Threats

- The Federal Reserve raised the target range of the federal funds rate by 25 basis points to 1 percent to 1.25 percent. While it maintained its forecast for one more hike this year, it also acknowledged that "inflation has declined recently." The divide between the Fed and the bond market is getting wider by the day. Fed Chair Janet Yellen characterized the recent weakening trend in inflation as fleeting. However, bond traders think otherwise. The rally in the fixed-income markets that has pushed yields on 10-year Treasury notes down to as low as 2.10 percent on Wednesday from 2.63 percent in March suggests traders believe the slowdown in inflation is more than transitory, countering the Fed’s confidence in stronger growth and labor markets. The consumer price index data released this week was particularly meaningful, as the core reading came in 0.1 percent below forecasts, the third miss in a row. Year-over-year, the reading came in at 1.9 percent, below the expected 2.2 percent. Retail sales data released at the same time was also weak.

- Treasury Secretary Steven Mnuchin on Tuesday set up the possibility of a government shutdown. His comments echoed a lot of rhetoric coming from the Trump White House. During a hearing before the Senate Budget Committee, Mnuchin was asked by Democratic Senator Tim Kaine about a May 2 tweet from President Trump that suggested the federal government needs a "good shutdown." His response: "It’s an unfortunate outcome. At times there could be a good shutdown, at times there may not be a good shutdown. There could be reasons at various times why that is the right outcome."

- The Fed laid out its plan to unwind its $4.5 trillion balance sheet at its latest meeting. The basic idea is that the Fed will stop reinvesting the principal of Treasury securities when they mature. Once the program begins, expected to be later this year or next year, the Fed will reinvest the principal of maturities only if it gets back more than $6 billion in principal returned in a given month. The "cap" will then be increased by $6 billion every three months until it reaches $30 billion a month. This is likely to push yields up, hurting fixed-income securities and creating tighter financial conditions.

This week spot gold closed at $1,253.75, down $12.88 per ounce, or 1.02 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 4.04 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index fell only 1.93 percent. The U.S. Trade-Weighted Dollar Index finished the week slightly lower by 0.12 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jun-13 | ZEW Survey Curent Situation | 85.0 | 88.0 | 83.9 |

| Jun13 | ZEW Survey Expectations | 21.7` | 18.6 | 20.6 |

| Jun-13 | PPI Final Demand YoY | 2.3% | 2.4% | 2.5% |

| Jun-13 | China Retail Sales YoY | 10.7% | 10.7% | 10.7% |

| Jun-14 | Germany CPI YoY | 1.5% | 1.5% | 1.5% |

| Jun-14 | U.S. CPI YoY | 2.0% | 1.9% | 1.5% |

| Jun-14 | FOMC Rate Decision-Upper Bound | 1.25% | 1.25% | 1.00% |

| Jun-15 | Initial Jobless Claims | 241k | 237k | 245k |

| Jun-16 | Eurozone CPI Core YoY | 0.9% | 0.9% | 0.9% |

| Jun-16 | Housing Charts | 1220k | 1092k | 1156k |

| Jun-22 | Initial Jobless Claims | 240k | -- | 237k |

| Jun-23 | New Homes Sales | 593k | -- | 569k |

Strengths

- The best performing precious metal for the week was gold, off just 1.02 percent despite a Fed rate hike. The Fed may not be in a position to continue with multiple rate hikes. Mike McGlone, BI Commodity Strategist, points out the current situation that both crude oil futures and Treasury bond yields are falling. Since 1983, the Fed has never sustained a rate hike cycle while both crude and Treasuries are falling.

- Gold has risen from a three-week low as investors digest the latest rate hike and anticipate the probability of additional rate hikes, reports Bloomberg. Suki Cooper, an analyst with Standard Chartered, writes, “If the market starts pricing in the end to the current hiking cycle, this would remove a major headwind for gold and allow prices to breach the stubborn $1,300 threshold in a sustained move higher.”

- Bloomberg reports that public sector investors increased their net gold holdings to an estimated 31,000 tons last year, an increase of 377 tons. This is the highest level since 1999.

Weaknesses

- The worst performing precious metal for the week was silver with a loss of 2.90 percent. Money managers cut their net-long by about 10 percent this past week. For the second week in a row, gold traders and analysts surveyed by Bloomberg are bearish. This is the first time survey results have indicated two-week run of bearish outlook since December.

- Gold futures have had the longest losing streak in three months, as investors have anticipated the Fed’s actions this week. Bullion futures for August delivery closed down for the fourth straight session earlier this week.

- Palladium has declined after what some analysts see as an unjustified surge. The overall auto market, including the Chinese auto market, is a key demand driver for palladium, and that market is faltering.

Opportunities

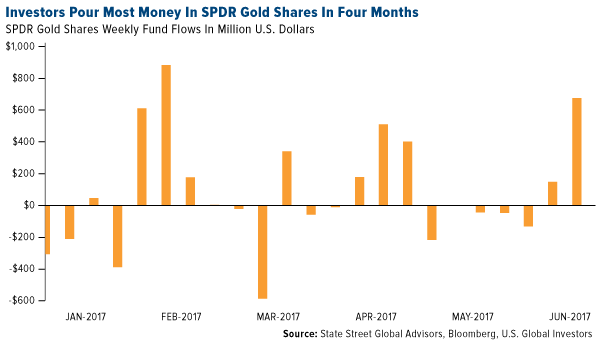

- As investors have sensed the Fed’s reluctance to continue multiple rate hikes, bullish gold investors are increasing their holdings in gold. Bloomberg reports that investors have added $675 million into the SPDR Gold Shares physical bullion ETF, taking the ETF to a six-month high. In addition, gold futures have climbed 10 percent this year on doubts that President Donald Trump’s economic agenda will make it through Congress and uncertainty around the U.K.’s Brexit plan.

- India’s gold market appears to be recovering after the demonetization scheme last fall and with efforts to improve transparency, reports Bloomberg. Some new policies under consideration include the start of a spot bullion exchange to make the supply of gold more transparent. In addition some taxes could be reduced, such as the import tax of 10 percent and a gold tax of 3 percent versus the 5 percent that some had feared.

- Barron’s reports that ANZ’s senior commodity strategist Daniel Hynes thinks gold can gold above $1,250 in the short term and break through $1,300 this year. Noting economic conditions and the signs of an improving market in China and India, Hynes goes on the say that the gold price may actually rise above $2,000 by 2025.

Threats

- Capital Economics takes the opposing view that the Fed will continue to raise rates, more so than the market seems to anticipate, and that gold will fall in the remainder of the year. The firm published a note this week stating their gold price forecast of $1,100 by the end of the year.

- Investigations into Trump are expanding to now include whether he may have attempted to obstruct justice, and exploring whether there is any evidence of financial crimes.

- The South African government’s new regulations requiring local mines to be at least 30 percent owned by black people has spurred the rand to weaken the most in more than two months. Nomura International Plc criticizes the new rule, stating that it will deter investment at a time when the country is in an economic recession. The controversy in Tanzania concerning Acacia Mining continues. Barrick Gold Corp., which owns 64 percent of Acacia, has stepped in to try to resolve the situation. Tanzanian President John Magufuli has demanded payment, and Barrick will help Tanzania build a smelter. Shares in Acacia surged on the news.

Energy and Natural Resources Market

Strengths

- Palladium was the best performing commodity this week, rallying 2.78 percent. Palladium prices are on fire this year, so much so that the metal is the top performing commodity of 2017 so far, according to the Financial Post. The metal is up 32 percent for the year on the back of favorable fundamentals where mine production hasn’t been able to keep up with usage. It is expected that supply will lag demand for the sixth straight year. Although the future is anyone’s guess in regards to palladium’s price, a deficit in supply and growing demand for the metal are positive fundamentals.

- The best performing sector this week was containers and packaging. The group rose 1.77 percent on the back of positive investor sentiment surrounding members of the index.

- Imperial Oil, a Canadian Petroleum Company, was the best performing stock this week, finishing up 5.04 percent. Despite tumbling oil prices, the stock rose on the back of being upgraded to a buy from the analyst community on Bay Street.

Weaknesses

- Copper was the worst performing commodity this week, dropping 3.07 percent. The commodity experienced its biggest weekly drop since early May of this year on the back of disappointing economic data in the U.S. this week. According to an article in the Wall Street Journal, there is increased doubt that President Donald Trump will be able to carry out planned infrastructure stimulus, which in turn will translate into weaker demand for the commodity.

- The worst performing sector this week was metals and mining. The group fell 13.03 percent on the back of disappointing economic data out of the U.S. and the Federal Reserve’s rate hike this week.

- The worst performing stock for the week was First Quantum Minerals, a mining and metals company headquartered in Vancouver. The company fell 12.9 percent on the back of falling copper prices this week.

Opportunities

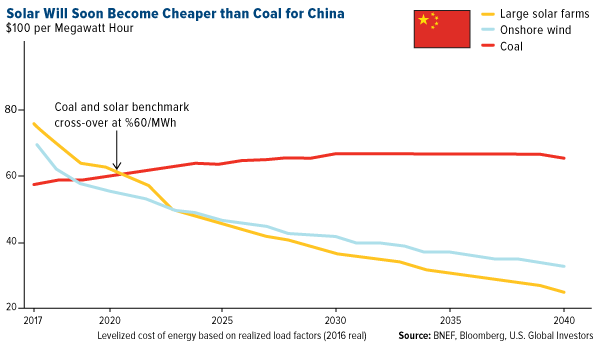

- Solar power will kill coal faster than you think, according to an article written by Bloomberg this week. Solar power energy has been plagued for years as an inefficient and costly source of energy; however, the economics of the alternative energy source are now beginning to become cheap enough to potentially push coal and even some natural-gas plants out of business faster than what was once previously forecasted. Seb Henbest, a researcher at BNEF in London, stated in the article that costs of new energy technologies are falling in a way that it’s more a matter of when than if solar power and alternative energy sources gain more market share. A boom in alternative energy projects will require materials from various commodities which is a positive read-through for raw material demand.

- Oil supply is estimated to outpace consumption in 2018, according to Reuters this week. On Wednesday, the International Energy Agency (IEA) said that growth in oil supply next year is expected to outpace an anticipated pickup in demand that will for the first time push global consumption above 100 million barrels per day (bpd). In addition, the IEA said that production outside of OPEC members may grow twice as quickly in 2018 as it will this year further increasing consumption momentum.

- Copper demand for electric cars could rise nine-fold by 2027, according to Reuters this week. As the world gears up to increase production of electric vehicles, electric or hybrid cars and buses are expected to reach 27 million by 2027, up from 3 million this year, according to a study conducted by the International Copper Association (ICA). The organization also stated in its findings that demand for electric cars could raise copper demand from 185,000 tonnes to 1.74 million in 2027.

Threats

- Crude oil chalks up its longest run of weekly losses since 2015, according to Bloomberg. This week proved to be a very challenging one for crude oil as Libya restored production this week and the surplus in U.S. inventories showed very little signs of subsiding. Bill O’Grady, chief market strategist at Confluence Investment Management, said that the current prices are an accurate reflection of fundamentals as inventory levels continue to remain stubbornly high and the factors that originally caused this trading range remain in place today.

- Decline in U.S. factory output shows manufacturing leveling off, according to Bloomberg this week. On Thursday, factory output declined 0.4 percent and industrial production came in unchanged after greatly disappointing analyst estimates of a 0.1 percent gain for factory output and 0.2 percent gain for industrial production. This is concerning, as the month of April came in at the strongest clip in three years; however, this backtrack may be signaling that the U.S. manufacturing sector may be starting to slow down.

- The dollar index rallied this week after the Federal Reserve raised interest rates, hammering all commodities. The Federal Reserve lifted its target policy rate by 25 basis points on Wednesday to a range of 1 to 1.25 percent, according to the Financial Times, which lifted the U.S. dollar. Prices of oil, copper and most importantly gold all fell as a result of rising interest rates.

China Region

Strengths

- Indonesia’s Jakarta Composite Index put on a strong showing for the week, rising 97 basis points in total return over the last five trading days; Vietnam’s Ho Chi Minh Stock Index also had a good week, rising 1.56 percent in the same time frame.

- According to a report from Citi Research, despite property controls tightening in China since mid-2016, leading indicators in the space have remained surprisingly resilient into mid-2017. For example, May 2017 floor space sales are up 10.2 percent year-over-year and floor space under construction continues to grow, up 3 percent year-to-date. Real underlying steel demand is most correlated to floor space under construction, the report continues—and despite a near-term slowdown in land sales, Citi thinks these purchases still demonstrate confidence that construction activity will remain strong in the medium-term.

- China ZhengTong Auto Services Hdgs. Ltd. (1728 HK) rose 18.39 percent for the week, the strongest performer in the HSCI. Some analysts are optimistic regarding the company’s first-half earnings potential following reports that BMW’s new 5 series pre-sales data demonstrate the model is being “well received,” according to Bloomberg News.

Weaknesses

- The Hang Seng Composite Index (HSCI) declined 1.52 percent over the last week, among the poorest performances in the region as the index fell from its 52-week highs last week.

- Esprit Hdgs. Ltd. (330 HK) fell the most in the HSCI this week, declining by 25.68 percent in that timeframe in presumed sympathy as HSBC cut its outlook for another apparel retailer, Global Brands (787 HK), which was the second worst performer in the HSCI, falling 20.87 percent.

- April year-over-year overseas remittances to the Philippines came in below expectations. Analysts were looking for a growth rate of 8.5 percent; instead, it declined by nearly 6 percent.

Opportunities

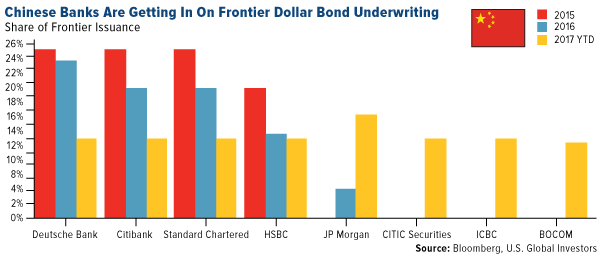

- As China continues to attempt to ramp up its image and soft power globally, the Belt and Road initiative—which includes some $80 billion in projected financing—is playing out in part in frontier-bond underwriting, as places like the Maldives, Sri Lanka, and Papua New Guinea deepen ties with Chinese banks.

- Geely Auto will be “producing locally assembled Volvo cars” in Malaysia by 2022, the Malaysia Mail Online reports, citing International Trade and Industry Minister Ong Ka Chuan. Geely recently acquired a significant stake in the Malaysian state-backed automaker Proton. • The BOK Governor Lee Ju-yeol stepped back from his talk earlier this week of tightening in Korea, reiterating that the Bank of Korea expects to maintain an accommodative policy in the near term even as the U.S. Federal Reserve raised rates.

Threats

- The government of Panama announced it is opening diplomatic relations with China this week, cutting the number of countries officially recognizing Taiwan’s government to a mere 20.

- There is a securitization boom in China, reports Reuters, as China struggles to wean its economy off of excessive debt. The Asian nation’s market in asset-backed securities (ABS) surged 50 percent in 2016 along and now exceeds a trillion yuan, the article continues. Analysts say there are signs of risks building in this market however, saying that some securitized projects have had over-optimistic cash flow projections. “It’s only a financial tool, but in recent years, ABS has been trumpeted to the sky in China, and the rapid growth of the business even shares some resemblance to the budding stage of the U.S. subprime crisis,” said Song Qinghui, a Beijing-based economist.

- And finally, Dennis Rodman is in North Korea.

Emerging Europe

Strengths

- Hungary was the best performing country this week, up 29 basis points.

- The Turkish lira was the best performing currency this week, up 94 basis points. The lira was unfazed as the nation’s central bank left rates unchanged and indicated it will maintain a tight monetary stance until the inflation outlook improves significantly.

- The health care sector was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, down 3.21 percent. Russian equities slumped to the lowest level in a year this week as several U.S. senators struck a bipartisan deal to expand existing sanctions against the nation, reducing optimism the steps would be lifted under President Donald Trump. The U.S. agreement would allow new sanctions against sectors of the Russian economy, including mining, metal, shipping and railways and would put into law penalties that were imposed by President Barack Obama’s administration, including on some Russian energy projects and on debt financing. This proposal is the latest sign that some lawmakers intend to push back on Trump’s efforts to improve relations with Moscow.

- The Russian ruble was the weakest performing currency this week, down 1.28 percent against the dollar.

- The materials sector was the worst performing sector among eastern European markets this week.

Opportunities

- Turkish economic growth unexpectedly accelerated at the start of the year to its best pace in almost two years. GDP growth hit 5 percent in the first quarter of 2017 compared to first-quarter 2016, and up from 3.5 percent at the end of 2016, when the economy bounced back after its worst quarter since the financial crisis.

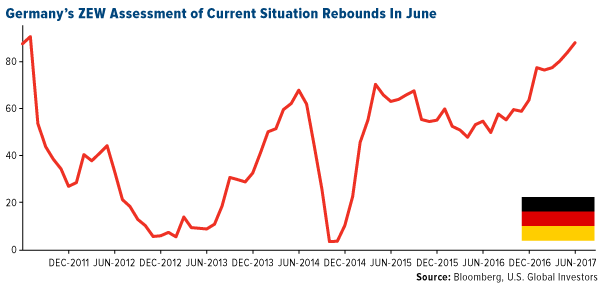

- Germany’s ZEW survey showed continued improvement in the current situation gauge, suggesting economic momentum is strengthening in the euro-area’s largest economy. The survey rose again and by more than expected in June, now standing at 88 up from 83.9 in May. The signal is probably exaggerated, but the second-quarter picture indicates the economy is continuing to enjoy strong and stable growth. The detail of the survey also show Germany’s financial industry is becoming more upbeat about France, but more worried by the U.S. and the U.K.

- According to Financial Times, nowhere in the world have expectations for growth changed so rapidly and positively as in central and Eastern Europe. The consensus forecast for economic growth in the region this year is now 2.5 percent, 0.3 percent points higher than four months ago. Expectations for 2018 are even brighter at 2.6 percent, 0.1 percentage points higher than forecast at the start of the year. Stronger-than-expected external demand in Western Europe, a tighter labor market, an attractive environment for foreign investment, government stimulus measures, easy financing conditions and the revival of EU structural funds are all supporting stronger growth in the region.

Threats

- The U.K electorate returned a hung parliament on June 8, creating further uncertainty for the economy. U.K industrial output posted a meager gain in April, which taken alongside weakness in previous months, leaves it on a weak footing at the start of the second quarter. The collapse of sterling coupled with more buoyant external demand should support the dominant manufacturing sector. But the outcome of the election has created more uncertainty about the sort of deal the U.K. will reach with the EU, which could mean the outward facing sector offers little offset to the likely slowdown in the much larger services sector this year.

- Turkish president Recep Erdogan continues to strengthen his hold on the country, firing or jailing civil servants by the tens of thousands., The number of educated, white-collar workers relocating abroad has quadrupled to almost 10,000 a month, data compiled by the CHP opposition party show. That includes an estimated 6,000 millionaires just in 2016, a six-fold annual jump, according to Johannesburg, South Africa-based research group New World Wealth.

- Brussels will sanction Czech Republic, Poland and Hungary for refusing to take part in a controversial scheme to share out refugees across the bloc. The EU introduced a plan to “relocate” up to 160,000 asylum seekers from Italy and Greece to other countries in the bloc. But so far only 20,000 have moved – with zero going to the trio of central and eastern European countries. As a result, the European Commission launched infringement proceedings – a long-winded process of sanction that could ultimately lead to fines – against Warsaw, Prague and Budapest.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All