Year-to-date through 6/9/17, the Russell 2000 Index advanced 5.3%. More than half of that result, however, has come during a so-far highly bullish June.

Prior to this recent burst, the small-cap index had been trading in a relatively close range, giving the impression of a market running in place since the 2016 high for the Russell 2000 on December 9th.

Through the end of May, for example, small-caps were close to their fifth consecutive month of consolidation after posting very strong returns in 2016.

It remains to be seen, then, whether June’s upswing has enough force to push small-caps out of this narrow band of returns, or if it will go the way of similar breakouts for the Russell 2000 this year in January, February, March, and April.

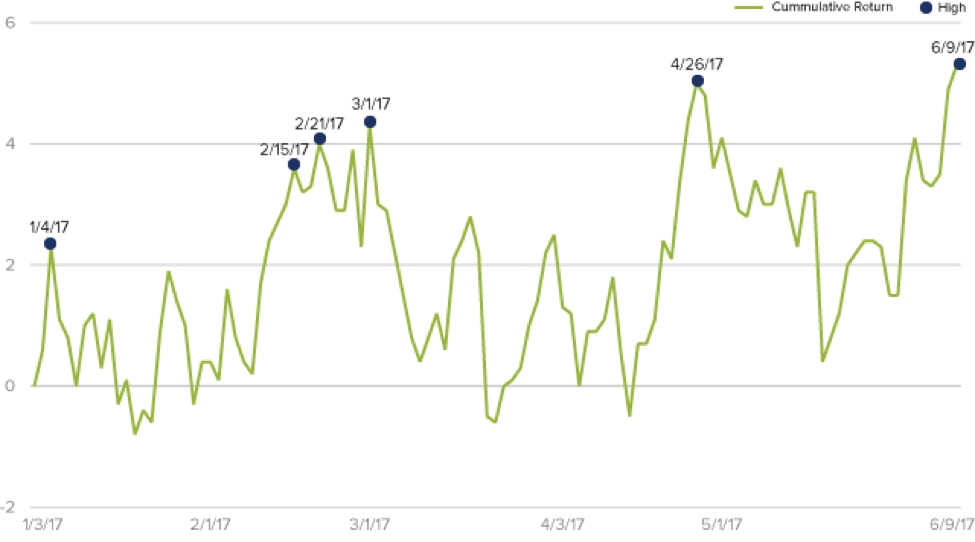

Each of the five new highs the small-cap index previously reached this year was followed by a pullback prior to the most recent. This tight and volatile range can be seen in the chart below.

Russell 2000 Year-to-Date Peaks From 12/31/16 to 6/9/17

In this consolidating context, it’s fair to ask what direction small-cap stocks may take through the rest of this year. First, we think it’s helpful to look at where they’ve been.

We are approaching the two-year anniversary of the last peak for the Russell 2000, which fell on 6/23/15. This peak marked the beginning of a broad small-cap recovery in which cyclical industries and value approaches have taken the lead.

We suspect that many investors have lost sight of two other important implications of this dramatic shift, especially against the backdrop of high-volume political noise: returns for the Russell 2000 were both strong prior to the November elections and firmly rooted in company fundamentals.

For now, small-cap returns are very concentrated, with technology driving year-to-date results for equities overall. This has led to a curious development within small-cap, with growth and lower quality stocks strong at one end and a smaller number of very high ROIC companies robust at the other.

As we go about navigating a course across this rocky investment terrain, our first action is to tune out politics and focus on fundamentals. If the pun can be forgiven, we think earnings trump policy (or the lack thereof) every time.

We also feel confident that ongoing earnings strength is more than enough to keep small-caps in the black, regardless of what happens in Washington and in spite of an uncertain market that hasn’t really established a direction so far in 2017.

According to research from our friends at Strategas, as well as our own analyses and discussions with company management teams, the sales and earnings outlook for small-caps remains promising through the end of the year.

To be sure, the combination of barbell-shaped returns, political theater, and economic uncertainty is creating what we see as fertile ground for fundamentally based, risk-conscious stock-pickers such as ourselves.

Stay tuned…

Important Disclosure Information

Mr. Gannon's thoughts and opinions concerning the stock market are solely his own and, of course, there can be no assurance with regard to future market movements. No assurance can be given that the past performance trends as outlined above will continue in the future.

The Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. The Russell 2000 Index is an unmanaged, capitalization-weighted index of domestic small-cap stocks. It measures the performance of the 2,000 smallest publicly traded U.S. companies in the Russell 3000 Index. The performance of an index does not represent exactly any particular investment, as you cannot invest directly in an index.

This material is not authorized for distribution unless preceded or accompanied by a current prospectus. Please read the prospectus carefully before investing or sending money. Investments in securities of micro-cap, small-cap, and/or mid-cap companies may involve considerably more risk than investments in securities of larger-cap companies. (Please see "Primary Risks for Fund Investors" in the prospectus.) Investments in foreign companies may be subject to different risks than investments in securities of U.S. companies, including adverse political, social, economic, or other developments that are unique to a particular country or region. (Please see "Investing in International Securities" in the prospectus.)