The U.S. Labor Market Through A Different Lens

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits- The U.S. Labor Market Through A Different Lens

- Is The Yield Curve Signaling A Recession?

The June employment report published today maintains the current status: hiring is strong and wage growth continues to linger at sub-par levels. The U.S. unemployment rate edged up one notch to 4.4% in June; payroll employment increased 222,000. Hourly earnings rose 2.5% from a year ago. Employment compensation gains have hovered around this range for four of the last six months.

This has led some economists to suggest that the Phillips curve, which represents an inverse relationship between unemployment and inflation, is dead. We touched on this briefly in our mid-year musings last week. This week, we look at employment and wage trends at state and industry levels to try and breathe life into the Phillips curve.

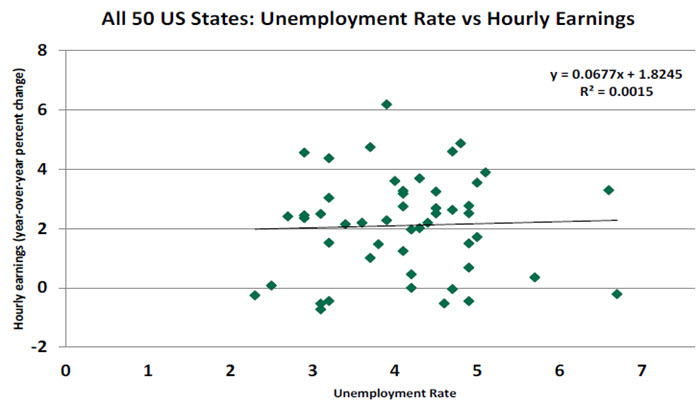

Data for national and state labor market conditions are gathered separately. State-level unemployment rates and hourly earnings do not exactly aggregate to the national readings, but they follow one another closely.

The chart below represents the unemployment rate and year-to-year change in hourly earnings for all the 50 states in the nation.

State earnings numbers usually contain larger swings than national data partly due to larger sampling and non-sampling errors. Excluding this limitation, one would typically anticipate states with low unemployment rates to show significant wage pressures. The chart on the earlier page indicates that hourly earnings numbers are different from these expectations and support for the Phillips curve is missing.

There are different reasons hiring and wage trends have failed to validate the inverse relationship between labor costs and employment conditions. In addition to the data problems mentioned earlier, which may be affecting comparisons at a given time, the nature and concentration of industries in each state is different. Differences in educational attainment of states’s populations affect labor market dynamics.

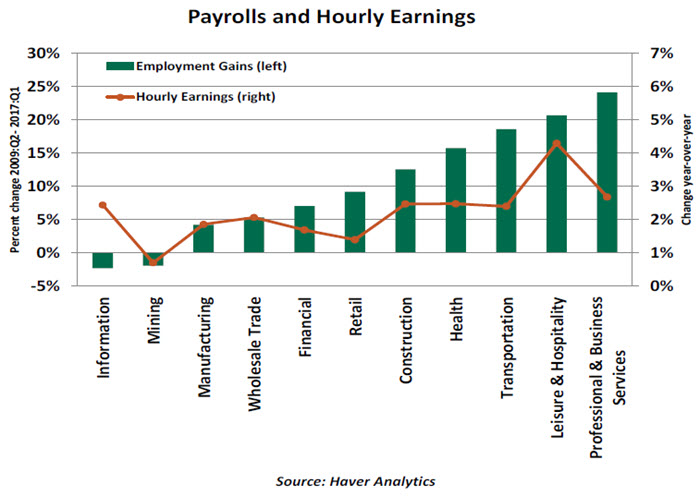

Another way of examining the Phillips curve’s performance during the current expansion is to look at experience across industries. Nearly 15 million jobs have been created during the last eight years, with some industries registering faster growth in payrolls than others.

Professional and business services, the category that covers a range of occupations, has added the most jobs since the Great Recession. The leisure and hospitality industry, which includes hotels, restaurants and tourism jobs, follows in second place with a little over 2.8 million jobs created since the second quarter of 2009.

The employment and wage dynamics of the oil industry is captured in the “mining” category. The large increase in jobs following the shale oil boom petered out as oil prices fell, and was followed in recent months by a small recovery. Growth in employment compensation has suffered following large gains during prosperous times.

Sectors associated with soft employment growth show subdued growth in earnings. Industries grouped under the “information” component are an exception. This sector includes internet publishing, telecommunications, internet service providers, the motion picture industry and publishing excluding the internet. Employment compensation moved up in this sector despite a reduction in employment, which reflects the impact of demand conditions for the products produced in this sector.

The state and industry data of employment and wages point out that the traditional relationship between hiring conditions and compensation is visible in the latter than the former. The distinctive features of states and differences in the nature of their industries could be important factors that result in atypical relationships between wages and employment. Getting a definitive read on the employment wage dynamic will be critical to the setting of U.S. interest rates. If this relationship has broken, we must understand the sources of the rupture so that they can form a conjecture on the evolution of inflation. If the dissociation is more temporary, rates will need to be raised prospectively to hold off pressure on the price level.

The modern economy, with its global and technological features, has challenged our understanding of labor market equilibrium. With key policy decisions at hand, we do not have the luxury of much time to study the question and arrive at new understandings.

Yield Curve Flattening

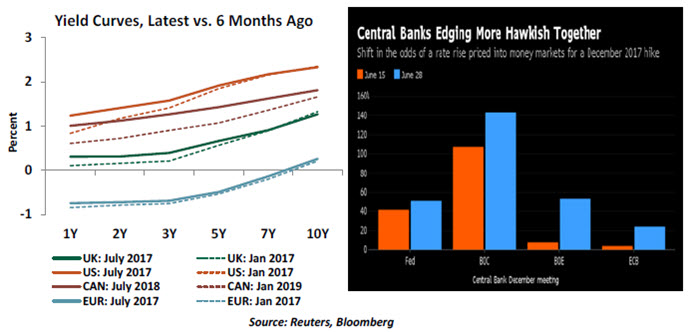

Last week, the European Central Bank’s (ECB) president, Mario Draghi, tested the waters for withdrawing monetary stimulus when he signaled a shift in “policy parameters.” However, the extreme market reaction (the euro and German bond yields posted new 2017 highs) forced the ECB to beat a hasty retreat. We are likely to see more trial balloons and false starts as the ECB contemplates an exit from extraordinary policy easing amid improving growth but weak price pressures.

Across the English Channel, the Bank of England’s policy makers continue to baffle the markets with their hawkish turn over recent weeks, despite worsening economic data and continued uncertainty around UK’s exit from the European Union.

With the conspicuous exception of the Bank of Japan, the monetary policy outlook in advanced economies has turned decidedly hawkish due to receding growth and deflation concerns; and anxiety over seemingly overstretched equity valuations and financial excesses. The U.S. Federal Reserve has already been hiking rates for a while now and will likely start balance sheet reduction this year. The Bank of Canada is likely to go ahead with a rate hike soon, while Sweden’s ultra-dovish Riksbank has dropped its easing bias. Norway, Switzerland, Australia and New Zealand are likely to join in within the next couple of quarters.

One would therefore expect bond yields to reflect the rise in the policy interest rate outlook, and they have. But what is surprising is the muted response of the long end of the yield curve. As a result, yield curves have flattened in many of these economies, i.e. short-term rates have risen more than long-term rates.

A flattening of the yield curve is typically indicates a pessimistic economic outlook. This widely held interpretation of curve flattening argues that a deteriorating economic outlook forces investors to flee to the safety of risk-free, long-term government bonds, suppressing long-term yields. This is in stark contrast with the market’s economic outlook implied by the strong performance of equity indices.

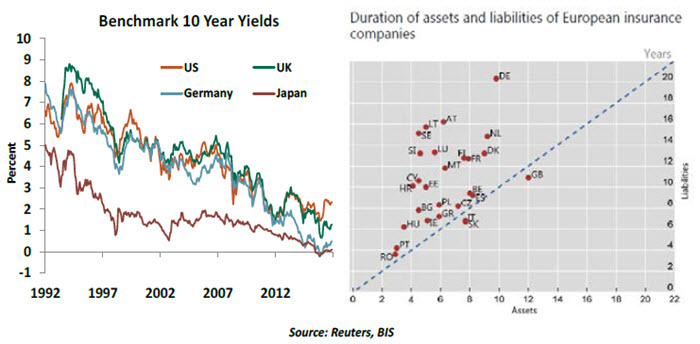

So why are long-term yields low? Any explanation for the current non-responsiveness of long yields must also account for the continued decline in long-term interest rates since the 1990s.

This question has attracted considerable attention since the great financial crisis and resulted in several prominent explanations, including lower output, weak price pressures, ultra-loose monetary policies, a global saving glut and ageing populations. For example, Rudebusch et al analyzes yields in the context of a “neutral” interest rate component and a term premium. The authors argue that low long-term inflation expectations, weak trend growth, surplus savings in export-oriented emerging markets and increasing savings on an ageing population have pushed down the neutral rate. They also highlight the role of extraordinary monetary easing and safe-haven flows to developed markets in lowering the term premium component of yields.

However, some of these explanations don’t hold water in the light of recent developments. As we have noted, global growth has improved, monetary policy has tightened and financial risk appetite has increased without causing substantial increase in yields.

But most analysts still consider long-term yields in the context of the above macroeconomic fundamentals. Perhaps unsurprisingly, yields have undershot most professional forecasts year after year over the last decade. The traditional metric of analyzing, interpreting and forecasting long-term yields is, at the very least, inadequate.

The Bank for International Settlements’ (BIS) Hyun Song Shin recently argued that “Long-dated yields… reflect very ordinary motives of individual investors that have only a limited bearing on forecasts of the distant future.” Therefore, “the market” is not a monolithic entity that sets prices according to a consensus macroeconomic view. Instead, market price action reflects the beliefs and behavior of numerous different entities with different goals, incentives and outlooks.

Ageing populations may be an important explanation for lower yields since they contribute to the increasing balance sheets of pension funds and life insurers. But more research is required to offer a complete explanation of lower-for-longer yields. For the time being, we would be well-advised to not read too much into the shape of the yield curve.

© Northern Trust

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All