Modifications to existing regulation of private mortgage market

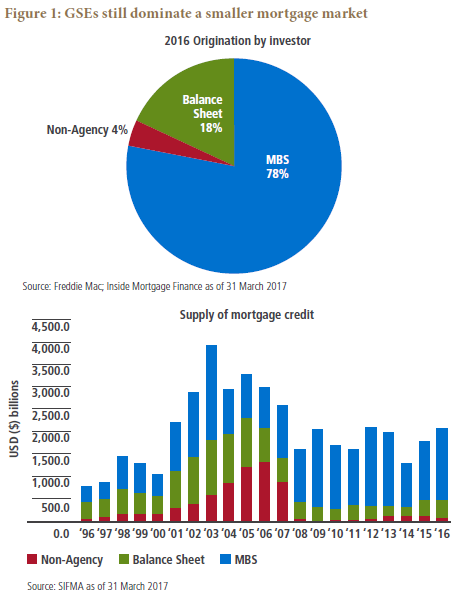

In the wake of the financial crisis, the comprehensive policy response understandably targeted the private, non-agency residential mortgage market. Remedies ranged from foreclosure prevention programs to statutory provisions and subsequent regulations that aimed to increase liability and accountability along the entire chain of non-agency mortgage production. While we believe much of this policy was reasonable in light of the financial crisis, there have been significant unintended and undesirable consequences for the private mortgage market – and as a result, for potential homeowners as well.

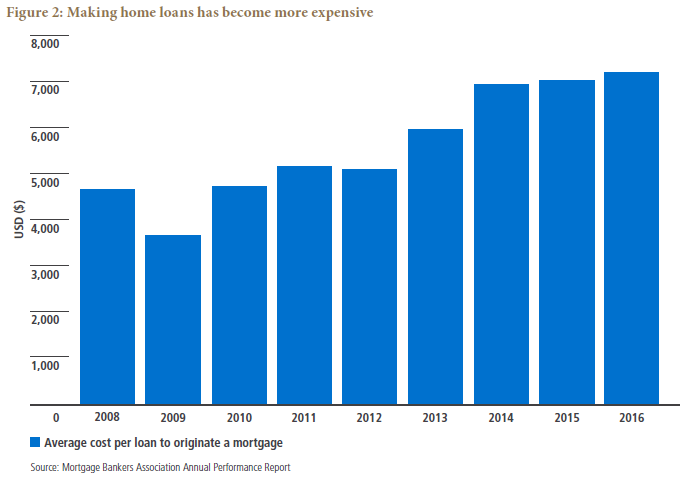

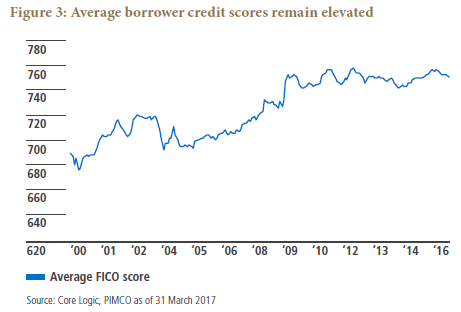

For originators and servicers, increased regulation has increased the costs of originating and servicing loans (see Figure 2), leaving financial incentive to originate and service only the most pristine, highest-quality loans (see Figure 3). From the perspective of investors such as PIMCO, the lack of investor protections and the additional legal liability and uncertainty associated with post-crisis policies represent risks that are simply too difficult to price, and as a result, we, like many others, prefer to invest our clients’ assets where legal certainty is a given. Importantly, this means that many borrowers who are qualified to purchase a home often cannot.

What can be done?

To bring capital back to the private mortgage market and ensure credit is extended to borrowers in a responsible manner, we support a few, relatively straightforward modifications to the current regulatory regime that we hope policymakers will consider.

These modifications include:

-

-

Imposing a best-interest standard on trustees and servicers in PLS (private-label securitizations) to increase investor protections. During the housing boom, mortgage originators often packaged non-agency mortgage loans into pools and sold them into mortgage-backed PLS trusts. The PLS trusts issued securities collateralized by these loans, largely to institutional investors, including PIMCO. The servicers of the loans and the trustees of these PLS trusts, however, frequently had conflicts of interest (e.g., they were owned by mortgage originators) and regularly failed to protect investors from pervasive bad practices by originators, such as poor underwriting and predatory lending. Because investors such as PIMCO did not (and still do not) have any standing to take action against the mortgage originators, they invariably had to (and still have to) bear the brunt of losses on these loans. The plethora of post-financial crisis regulation has not addressed this lack of investor protection by ensuring aligned interests in PLS trusts, and this has provento be the fundamental deterrent to investors coming back to this market.

We believe that each party involved in PLS trusts should be held fully accountable in a manner that safeguards the interests of the borrowers and the investors. To achieve this, we believe trustees and servicers need to have an explicit fiduciary duty to act in the best interest of PLS investors at all times. We maintain that this would result in higher-quality loans in PLS trusts and would greatly reduce the risk of servicers and trustees acting against the interests of PLS trusts, either through self-dealing or by inaction.

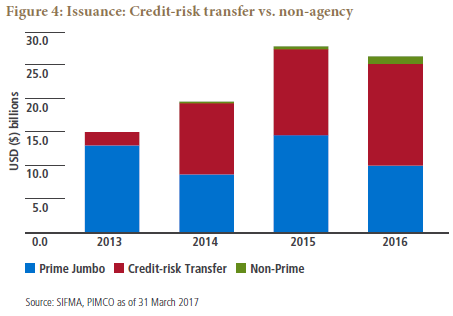

The success of the GSEs’ credit risk transfer (CRT) transactions (see Figure 4) provides a useful comparison: Although the GSEs do not have an explicit fiduciary duty to protect investor interests in the CRT transactions, they have a demonstrated history of enforcing their contracts with originators and have aligned interests with investors more broadly. Investors in CRTs therefore assume their interests will be protected. If that were not the case, it would be reasonable to infer from the lack of post-crisis PLS issuance that the CRT market would not exist given that CRT bonds typically have little to no subordination to cushion investors from losses.

-

Eliminating the expansion of assignee liability for investors under Dodd-Frank’s Ability to Repay rule: Currently under Dodd-Frank, mortgage investors are liable for mistakes made by lenders in the mortgage origination process for certain mortgage loans that are not deemed “Qualified Mortgages.” Since investors have no role or discretion in the mortgage origination process, we believe this is not only nonsensical, but also has the practical effect of discouraging investors from purchasing these loans given that such a liability is nearly impossible to price. Mortgage originators should be liable for their own underwriting practices, but investors buying these loans in the secondary market – who have no way to control the origination process – should not be.

-

Allowing for regulatory cures for numerical errors under TRID (aka, TILA-RESPA): TRID, the series of documentation and disclosures that provides borrowers more clear and concise information about their loans, represents a meaningful and necessary improvement to borrower loan disclosures. However, given how complex the regulatory requirements are, numerical errors in the documentation often occur (e.g., a mistake in the borrower’s zip code). Although these errors are typically trivial and do not result in any harm to consumers, they are nevertheless considered to be violations – for which investors can ultimately be held accountable under TRID. Since no mechanism exists to correct these errors, investors will either demand a significant discount to purchase a mortgage loan to compensate for the potential liability or walk away altogether because the liability is too difficult to price. Allowing for a mechanism to rectify these trivial errors is important in bringing back private capital to the non-agency market.

Expanding the “Qualified Mortgage” safe harbor to jumbo loans: Currently, many creditworthy jumbo loans are not considered Qualified Mortgage loans and therefore do not receive safe-harbor status from a myriad of requirements under Dodd-Frank purely because of their size. Investors who otherwise would be interested in investing in jumbo loans, which are often very high quality, do not because of the assignee liability attached to non-QM loans (discussed earlier in point 2). We believe that if a loan adheres to all other QM criteria eligible for purchase by the GSEs, it should qualify for QM status. We think this would lead to credit expansion and more liquidity in the non-agency market.

Eliminating (or scaling back) the 5% risk retention requirement in light of its redundancy with the Ability to Repay rule: The Ability to Repay rule, which is part of the Dodd-Frank Act, requires mortgage lenders to verify that mortgage borrowers can in fact pay back their loans; by contrast, in the period leading up to the financial crisis, many mortgage loans were made regardless of the ability of the borrower to pay. We believe this rule has been incredibly effective, eliminating most dubious bubble-era underwriting practices and raising underwriting standards broadly. Given the Ability to Repay rule’s success, we contend that the 5% risk retention requirement is redundant and is yet another headwind for both originators and investors from participating in the private mortgage market. We think the 5% risk retention threshold should be eliminated – or at the very least scaled back to be commensurate with the risk of the underlying collateral.

Proceeding with GSE reform only after issues in the private mortgage market are addressed

We would argue that only once a vibrant private, non-agency mortgage market returns would it be appropriate for policymakers to turn their focus to the reform of Fannie Mae and Freddie Mac. After all, if no private, alternative market exists, shrinking the GSE footprint would necessarily mean contracting the housing sector and creating a headwind to economic growth, which seems contrary to the objectives of policymakers in Washington.

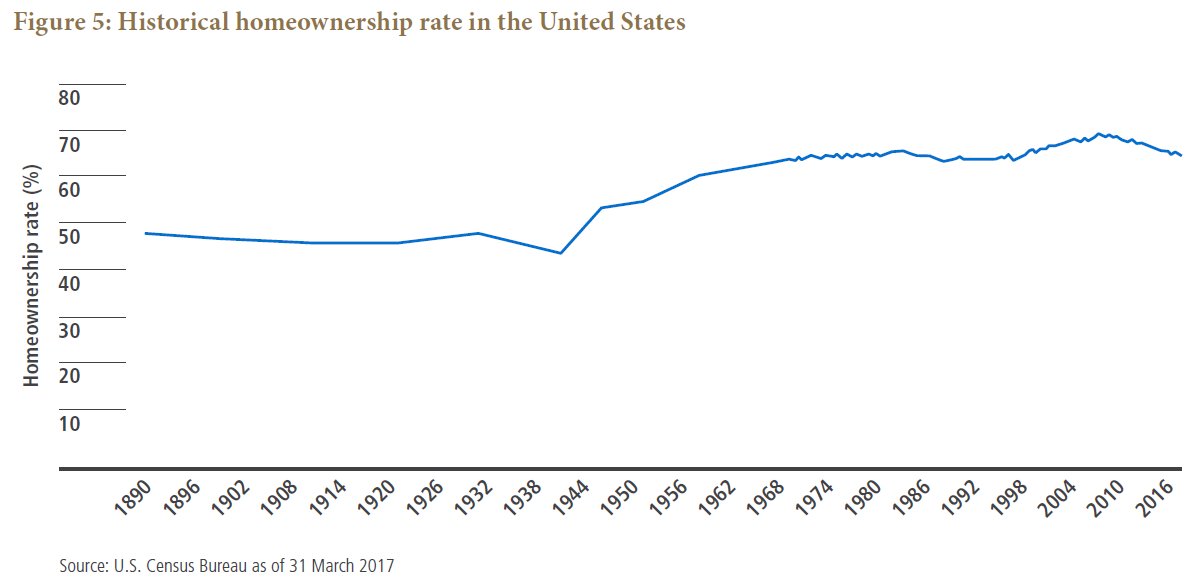

As policymakers think about reform, they need to be clear about the policy objectives reform is trying to achieve. From PIMCO’s perspective, the policy objectives outlined in the National Housing Act of 1934 that created the GSE system – including subsidizing lower- and middle-income homeowners and providing secondary loan market liquidity – are still very worthwhile and should continue. As shown in homeownership rates (see Figure 5), these policies have been incredibly successful in providing access to mortgages and promoting homeownership, which in turn has been positive in many respects. As famously attributed to former U.S. Treasury Secretary Larry Summers, “In the history of the world, no one has washed a rented car.”

Part and parcel of these objectives is the continuation of the “to be announced” (TBA) market, which helps facilitate a national mortgage rate. Without a TBA market carrying the explicit government guarantee of timely principal and interest payments, mortgage rates would be vastly disparate in places like Corona, New Mexico and Corona del Mar, California, leading to significant geographic variations in credit availability, mortgage affordability and homeownership.

Consequently, as policymakers think about removing the GSEs from conservatorship, where they have been since 2008, we are reminded of the Hippocratic Oath: “First, do no harm.” To be sure, minimizing the harm that could come from removing the GSEs from conservatorship underpins our focus on reforming the private mortgage market first.

While policy proposals for GSE reform abound, they all seem to assume too much and explain too little. For instance, why will mutually owned guarantors emerge? How will the purchase activities be funded? How politically feasible are wide geographic variations in mortgage affordability and homeownership? We will refrain from commenting on specific plans or offering our own, but as one of the largest purchasers of GSE mortgages, we can highlight provisions we think are necessary in a new system. (One exception: We believe the “recap and release” proposal would not be viable because it lacks these necessary components.)

In our view, GSE reform should continue promoting homeownership and stability in the secondary mortgage market and therefore must include the following characteristics:

- A continuation of a national mortgage rate through the “to be announced” (TBA) market.

- An explicit “full faith and credit” government guarantee for future and legacy GSE MBS as we do not believe a uniform national mortgage rate can exist without it.

- A guarantor-established guaranty fee (“g-fee”), which we believe is far superior to a fluctuating g-fee determined by the cost of private capital in providing stability to the market and preserving a national mortgage rate.

- Continuation and extension of credit risk transfer, which we see as an effective mechanism to minimize taxpayer risk. However, we believe that CRT must be “back-ended,” meaning the GSEs buy the loans first, prior to CRT issuance, to maintain investor confidence that selling and servicing provisions are enforced to their benefit.

- Balance-sheet acquisitions should be limited to distressed mortgage management and the provision of countercyclical liquidity mandated by the regulatory agencies.

- Loan limits should be based on national median income as opposed to house prices.

The first three provisions would perpetuate the public good: a broad and deep secondary mortgage market that delivers affordable middle-class homeownership across regions through a national mortgage rate – which the GSEs have historically provided. Provisions four and five would minimize the taxpayer risk in providing national housing subsidies. Finally, loan limits based on national median income rather than home prices would be more likely to attract significant private capital into the mortgage credit market.

Conclusion

Housing finance reform should focus, first, on addressing the most acute problem: the lack of credit availability. While housing continues to be a critical part of the U.S. economy, the market is too reliant upon the GSEs for the vast majority of housing finance with many creditworthy borrowers unable to gain access. We therefore believe that policymakers should focus on reviving the private mortgage market first before turning their attention to GSE reform.

Unlike the complexities of GSE reform, a few minor, straightforward changes – some of which can be done through regulation, not legislation – can be made to bring private capital back to the market, breathe new life into an important sector of the economy, and importantly provide access to homeownership in a responsible manner. A viable private market would by definition make GSE reform easier to do, which is yet another added benefit.

A word about risk: All investments contain risk and may lose value. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and their value may fluctuate in response to the market’s perception of issuer creditworthiness; while generally supported by some form of government or private guarantee, there is no assurance that private guarantors will meet their obligations. Certain U.S. government securities are backed by the full faith of the government. Obligations of U.S. government agencies and authorities are supported by varying degrees but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. The credit quality of a particular security or group of securities does not ensure the stability or safety of the overall portfolio.

Statements concerning financial market trends are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

This material contains the opinions of authors but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

© PIMCO

© PIMCO

Read more commentaries by PIMCO