Warm temperatures prevail in most of the United States at the moment, a trend that is mirrored in recent economic data. We don’t expect conditions to cool as autumn approaches.

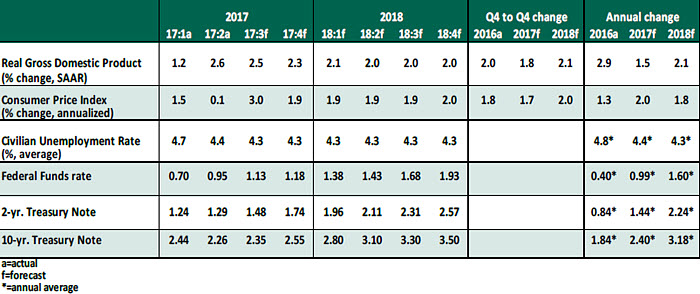

Second-quarter growth in gross domestic product (GDP) has been estimated at 2.6% on an annualized basis. This is more than twice the pace of the first quarter and brings expansion in the first half of 2017 close to the 2% level that we had projected at the start of the year. We are forecasting slightly better results during the balance of the year for reasons detailed below.

Key Economic Indicators

Key Elements of the Forecast

-

- Personal consumption was a highlight of the second quarter GDP report, rising by 2.8% on annualized basis. This was a pleasant surprise to some who had become concerned at the sluggish pace of retail sales growth during the April-June period. But it is important to remember that services compose a substantial fraction of household expenditures, and many of these are not captured in the retail sales data. Wealth effects created by the exceptionally strong equity markets are certainly a strong tailwind for spending.

-

- Employment was another likely contributor to the positive tone for consumers. U.S. nonfarm payrolls expanded by 209,000 in July, the fifth month this year that job creation exceeded 200,000. It bears repeating that a reading of 100,000 new positions is thought to be sufficient to keep the monthly unemployment rate steady; recent outperformance has lowered the unemployment rate to 4.3% and generated a modest increase in labor force participation.

-

- The restoration of income among new job holders certainly augurs well for consumption gains during the balance of the year. For those in the workforce, wage gains remain very modest by late-expansion standards. During the past twelve months, hourly earnings have risen by just 2.5% in contrast to past upturns, when wage gains routinely exceeded 3% as the cycle aged. There have been various theories for why pay raises have been so muted, but our sense is that the labor market is getting tighter and compensation is bound to respond.

-

- While consumption has been strong, inventories have not. American industry reduced its collective stocks during the second quarter following a negligible gain during the first quarter. A case can certainly be made that inventories are due for some rebuilding, which will also increase growth prospects during the balance of the year. This might be one reason why the Institute of Supply Management’s Purchasing Managers Index remains solidly in expansionary territory, reading 52 overall and 57.8 for manufacturing. (A level of 50 separates advance from decline.)

-

- Existing home sales fell in June, and home construction remains cautious. We think housing has upside potential during the remainder of 2017, given the very low level of new homes for sale, persistently low mortgage rates and lending standards that are becoming less restrictive.

-

- Inflation showed little movement last month. The consumer price index (CPI) was flat last month; its year over year change fell to just 1.6% (1.7% when food and energy costs are removed). The Federal Reserve’s favored inflation measure, the deflator on core personal consumption expenditures, has risen only 1.5% over the last twelve months. There are some transitory factors restraining inflation, but there are also some more lasting effects.

-

- As expected, the Fed took a pause from its rate increasing program during its July meeting, and it expressed an expectation that its balance sheet would begin declining “relatively soon.” The odds of another interest rate hike before the end of the year stand at about 40%. In spite of all of this, long-term U.S. interest rates are slightly lower than they were one month ago.

The month ahead will likely be a quiet one as summer holidays lure people away from work. But things should heat up again after Labor Day, when Congress and portfolio managers get back to business.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2017 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust