Is this the Start of a Hot New Metals Bull Market?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Major U.S. indices slid for a second straight week as President Donald Trump and North Korea both escalated their saber-rattling, with Kim Jong-un explicitly targeting Guam, home to a number of American military bases, and Trump tweeting today that “Military solutions are now fully in place, locked and loaded.” The S&P 500 Index fell 1.5 percent on Thursday, its largest one-day decline since May. Military stocks, however, were up, led by Raytheon, Lockheed Martin and Northrop Grumman.

As expected, the Fear Trade boosted gold on safe haven demand. The yellow metal closed just under $1,300, a level we haven’t seen since November 2016. This week, Ray Dalio, founder of Bridgewater Associates, the largest hedge fund in the world, said it was time for investors to put between 5 and 10 percent of their portfolio in gold as a precaution against global and domestic geopolitical risks. The threat of nuclear war is at the top of everyone’s mind, but Dalio reminds us that our indecisive Congress could very well fail to agree on raising the debt ceiling next month, meaning a “good” government shutdown, as Trump once put it, would follow.

Dalio’s not the only one recommending gold right now. Speaking to CNBC this week, commodities expert Dennis Gartman, editor and publisher of the widely-read Gartman Letter, said that he believed “gold is about to break out on the upside strongly” in response to geopolitical risks and inflationary pressures. Gartman thinks investors should have between 10 and 15 percent of their portfolio in gold.

Government shutdowns haven’t always been harmful to the stock market—during the last one, in October 2013, stocks actually gained about 3 percent—but I agree that it might be prudent right now for investors to de-risk and ensure their portfolios include safe haven assets such as gold and municipal bonds. Dalio and Gartman’s allocation percentages mirror my own. For years, I’ve recommended a 10 percent weighting in gold, with 5 percent in bullion and 5 percent in high-quality gold stocks, mutual funds and ETFs.

Analysts Bullish on Metals and Commodities

|

|

| click to enlarge |

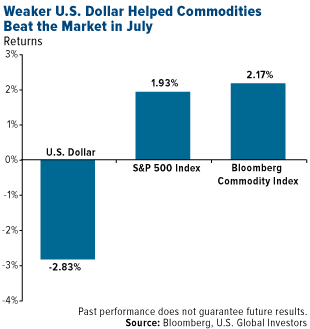

Like stocks, the U.S. dollar continued its slide this week. This has lent support not just to gold but also commodities, specifically industrial metals. The Bloomberg Commodity Index actually beat the market in July, the first time it’s done so this year.

If we look at the index’s constituents, we find that six metals—aluminum, copper, zinc, gold, silver and nickel—have been the top drivers of performance this year, thanks to a weaker dollar, China’s commitment to rein in oversupply and heightened demand. According to Bloomberg, an index of these six raw metals has jumped to its highest in more than two years.

Some market observers believe this is only the beginning. Guy Wolf, an analyst with Marex Spectron Group, told Bloomberg that he doesn’t “see anything” to make him doubt the firm’s belief that metals “are now in a bull market.”

“As people start to realize that the reasons for prices going up are robust and sustainable, that’s going to bring more money into the market,” Wolf added.

This bullish sentiment is shared by Mike McGlone, senior commodities analyst with Bloomberg Intelligence, who writes that commodities’ strong performance in July “could be the beginning of a trend.”

“Supported by demand exceeding supply, on the back of multiple years of declining prices, a peaking dollar should mark an inflection point for sustained commodity recovery,” McGlone says.

I can’t say whether we might eventually see the highs of the commodities supercycle in the 2000s, but this news is certainly constructive.

Aluminum Liftoff

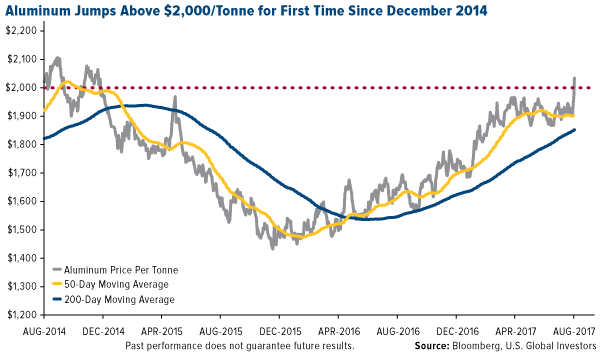

The top performer right now is aluminum, up more than 20 percent year-to-date. This week it breached $2,000 a tonne for the first time since December 2014 and is currently trading strongly above its 50-day and 200-day moving averages.

Demand for aluminum is growing in the automotive and packaging industries, its two key markets. With consumers and governments demanding better fuel efficiency, automakers are increasingly turning to aluminum, which is around 40 percent lighter than steel. According to Ducker Worldwide, a market research firm, the amount of aluminum used to build each new vehicle will double between the early 2010s and 2025, eventually reaching 500 pounds. That’s up from only 100 pounds per vehicle, which was the case in the 1970s. Airline manufacturers such as Boeing and Airbus are also expected to increase demand for the lightweight metal.

Supply-side conditions are also improving. Prices have struggled in recent years as China—which accounts for roughly 40 percent of world output—flooded the market with cheap, and often illegal, metal. Recently, however, the Asian giant has called for dramatic capacity cuts in a number of provinces. By the end of 2017, an estimated 4 million metric tons of capacity will have closed, or one-tenth of the country’s total annual output, according to MetalMiner.

Also supporting prices is the Commerce Department’s decision this week to slap duties on aluminum coming into the U.S. from a number of Chinese producers that were found to be heavily subsidized by the Chinese government. Subsidy rates range in size from 16.56 percent to 80.97 percent for at least five separate companies.

The Virginia-based Aluminum Association applauded the decision, saying that its members “are very pleased with the Commerce Department’s finding and we greatly appreciate Secretary [Wilbur] Ross’s leadership in enforcing U.S. trade laws to combat unfair practices.”

The aluminum industry, the trade group says, supports more than 20,000 American jobs, both directly and indirectly, and accounts for $6.8 billion in economic activity.

Miners Getting Back to Work

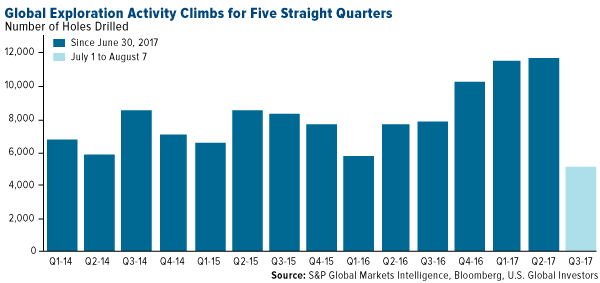

There’s perhaps no greater signal of a shift in sentiment than an increase in mining activity as producers take advantage of higher prices. Bloomberg reported this week that the number of new holes drilled around the globe has accelerated for five straight quarters as of June. What’s more, drilling activity so far this quarter, as of August 7, suggests that number could extend to six quarters.

I believe activity will only continue to expand as China pursues further large infrastructure projects, which will require even more raw materials such as aluminum, copper, zinc and other base metals. And I still have confidence that Trump and Congress can deliver on a grand infrastructure deal—the president has been turning up the heat on Senate Majority Leader Mitch McConnell, writing on Twitter that the Kentucky senator needs to “get back to work” and put “a great Infrastructure Bill on my desk for signing.”

With government spending on infrastructure falling to a record low of 1.4 percent of GDP in the second quarter, such a bill would help modernize our nation’s roads, bridges, waterways and more. It would also serve as a huge bipartisan win for Trump, which he sorely needs to build up his political capital.

But beyond that, a $1 trillion infrastructure deal would greatly boost demand for metals and other raw materials, perhaps ushering in a new commodities supercycle.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.06 percent. The S&P 500 Stock Index fell 1.43 percent, while the Nasdaq Composite fell 1.50 percent. The Russell 2000 small capitalization index lost 2.70 percent this week.

- The Hang Seng Composite lost 2.51 percent this week; while Taiwan was down 1.68 percent and the KOSPI fell 3.16 percent.

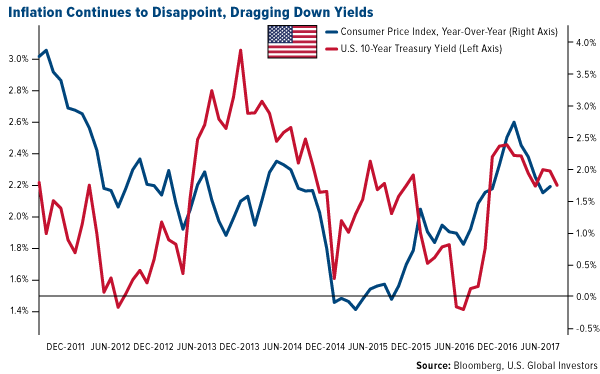

- The 10-year Treasury bond yield fell 7 basis points to 2.19 percent.

Domestic Equity Market

Strengths

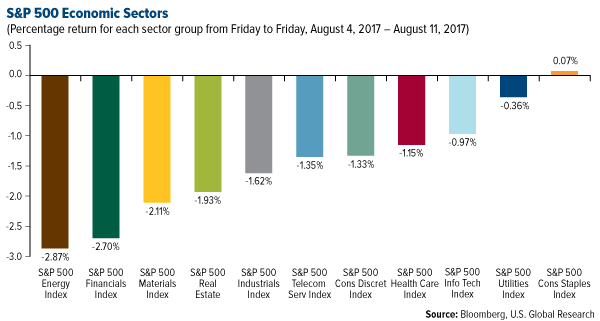

- The consumer staples sector was the best performing sector for the week, increasing by 0.07 percent versus an overall decrease of 1.34 percent for the S&P 500.

- Michael Kors was the best performing stock for the week, increasing 21.44 percent.

- Canaccord Genuity analyst Dewey Steadman noted that with the beat-and-raise in its latest earnings report, Perrigo is "bucking recent industry trends." The stock rallied on its strong quarterly performance.

Weaknesses

- Energy was the worst performing sector for the week, falling 2.87 percent versus an overall decrease of 1.34 percent for the S&P 500.

- Macy’s was the worst performing stock for the week, falling 11.50 percent.

- Snap's shares sold off after its earnings report was released. The company fell short on earnings and revenue expectations.

Opportunities

- According to Reuters, Saudi Arabia is leaning toward picking New York for the main foreign listing of state oil giant Aramco, even though some financial and legal advisers have recommended London as a less problematic option.

- Amazon is seeking to partner with U.S. venue owners to sell event tickets, four sources have told Reuters. If it enters the ticketing business, the company could loosen Ticketmaster's grip on the market.

- According to UBS, a strong denim fashion cycle has begun and it will benefit brands that not only specialize in the fabric like Levi’s, but other brands like Nike as well. Brands like Nike could benefit because, historically, when denim is popular, basketball shoes tend to be popular as well.

Threats

- According to analysts from RBC Capital Markets, execution challenges have led management to lower future growth estimates at Blue Apron. The firm lowered its price target to $8 from $10.

- The deterioration of the middle class in America is decimating department stores. Shares of Macy's, Dillard's, Kohl's and JC Penney fell as much as 15 percent this week after the companies reported weak quarterly sales.

- The escalating tension with North Korea is scaring traders and shocking the market. The CBOE Volatility Index, commonly known as the stock market fear gauge, burst from near-record lows on Thursday spiking 44 percent, its biggest increase since May.

August 9, 2017How to Invest in China’s New High-Tech Economy |

August 7, 2017Storm Advisory—What You Need to Know Now |

August 3, 2017Surprise! Gold Prices Have Beaten the Market So Far this Century |

The Economy and Bond Market

Strengths

- The Index of Small Business Optimism increased to 105.2 from 103.6 in June. This increase was the first since January. Business owners signaled optimism in their ability to expand partly due to a pick-up in consumer spending. This follows solid hiring activity among small businesses in July.

- The Labor Department said that nonfarm productivity increased at a 0.9 percent annualized rate in the second quarter. Compared to the second quarter of 2016, productivity increased at a 1.2 percent rate. Economists polled by Reuters had forecast productivity increasing at a 0.7 percent pace in the second quarter.

- The U.S. government on Thursday reported a smaller deficit for July compared to the previous year as a result of an increase in tax receipts and lower spending on health care. The deficit of $43 billion compared to a deficit of $113 billion the prior year.

Weaknesses

- U.S. consumer prices increased less than expected in July, pointing to benign inflation that could make the Federal Reserve cautious about raising interest rates again this year. The Labor Department announced the Consumer Price Index (CPI) edged up 0.1 percent last month after being flat in June. That lifted the year-on-year increase in the CPI to 1.7 percent. Economists polled by Reuters had forecast the CPI rising 0.2 percent in July and climbing 1.8 percent year-on-year. Lagging inflation has prevented long-term yields from rising along with the Fed’s rate hikes, causing the yield curve to flatten.

- U.S. producer prices in July fell for the first time in 11 months. The Producer Price Index (PPI), a key measure of industrial inflation, fell 0.1 percent in July from the previous month, said the Labor Department. That came in below expectations of a 0.1 percent increase.

- The number of initial claims for unemployment benefits was unexpectedly higher than anticipated last week, the Labor Department reported Thursday. Economists had forecasted the number of claims would be unchanged from last week at 240,000, but the actual number of applications was 244,000.

Opportunities

- The August Empire State (Tuesday) and Philly Fed (Thursday) surveys will give a timely read on the U.S. manufacturing sector.

- Investors will be attentive to the minutes of the July FOMC meeting (Wednesday) for additional insights to the Fed's thinking on the economy and monetary policy.

- U.S. economic expansion will last at least another two years, according to a majority of economists polled by Reuters.

Threats

- Tuesday's retail sales report and Friday's consumer sentiment survey will provide an update on the state of the U.S. consumer. With real consumer spending stalling in June, investors and Fed officials need a rebound in July's retail sales.

- The Leading Index (Thursday) will give an update into the potential future of the U.S. economy. It is forecasted to slow down from the previous month’s reading.

- U.S. month-over-month Industrial Production for July (Thursday) is forecasted to soften from the prior month’s pace.

This week spot gold closed at $1,289.35, up $30.58 per ounce, or 2.43 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.52 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index fell 0.37 percent. The U.S. Trade-Weighted Dollar finishing the week lower by 0.51 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Aug-10 | Initial Jobless Claims | 240k | 244k | 241k |

| Aug-10 | PPI Final Demand YoY | 2.2% | 1.9% | 2.0% |

| Aug-11 | Germany CPI YoY | 1.7% | 1.7% | 1.7% |

| Aug-11 | CPI YoY | 1.8% | 1.7% | 1.6% |

| Aug-10 | China Retail Sales YoY | 10.8% | -- | 11.0% |

| Aug-10 | Housing Starts | 1225k | -- | 1215k |

| Aug-11 | Eurozone CPI Core YoY | 1.2% | -- | 1.2% |

| Aug-11 | Initial Jobless Claims | 240k | -- | 244k |

Strengths

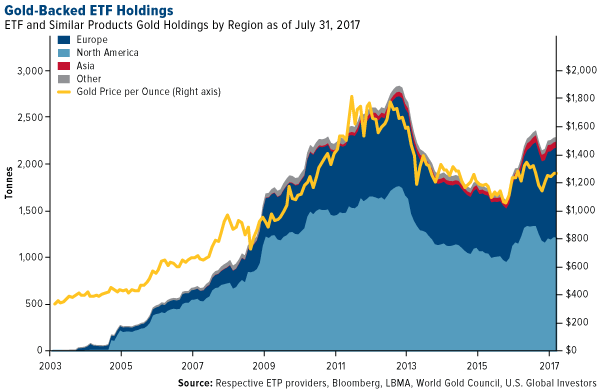

- The best performing precious metal for the week was silver, which was up 5.18 percent for the week on back of a strong 2.52 percent rise in gold amid soft inflation and a weaker U.S. dollar. Gold traders and analysts surveyed by Bloomberg are bullish for the eighth week. Looking over the longer term, gold-backed exchange traded products have seen a resurgence in demand, particularly in Europe.

- Rising tensions between the U.S. and North Korea have boosted demand for gold as investors look to it as a “safe haven” and the gold price is beating U.S. stocks. In addition, Bloomberg reports that gold imports to India more than doubled in July.

- According to CFTC data, gold net-long positions have been raised by 64 percent in the week ending August 1. UBS analyst Joni Teves stated that, “Although speculative positions on Comex have increased in the past couple of weeks, overall levels remain lean.”

Weaknesses

- The worst performing precious metal for the week was palladium, which was still positive, appreciating 1.81 percent. The U.S. consumer price index (CPI), the core measure of the U.S. cost of living, came in below forecast last month, rising just 0.1 percent. Bloomberg reports this dampens the likelihood that the Federal Reserve’s target inflation goal would be reached soon.

- Labor unrest has “paralyzed” operations at Gran Colombia Gold’s Segovia mine. A paramilitary group, Autodefensas Gaitanistas de Colombia, is supporting protests by informal miners since July 21. Bloomberg reports that the informal workers are protesting against a senate initiative to formalize their work, and the company has temporarily suspended workers’ contracts. Labor disputes have also affected Primero Mining, as well as liquidity issues. Shares of Primero are down as much as 48 percent on the news after the second quarter update.

- Investors are pulling assets out of silver-backed exchange-traded funds. Bloomberg data shows that holdings in silver-backed ETFs have fallen 1.6 percent, or 331 metric tons. This is the fastest drop since December.

Opportunities

- Ray Dalio, the manager of the world’s largest hedge fund at Bridgewater Associates, recommends that investors place 5 to 10 percent of their assets in gold. Dalio states that with current geopolitical risks, odds of Congress not raising the debt ceiling leading to a technical default and shutdown of the government, and the loss of faith in the effectiveness of our political processes, it would make sense to have a portion of a portfolio in gold as a hedge.

- Evolution Mining Ltd. chair Jake Klein commented on the challenges of passive investing, and said that mining companies could benefit from more investor activism. Activism campaigns have increased in mining centers like Australia and Canada, and Klein also commented, “Investors are almost too tolerant, and too accepting.”

- Klondex Mines Ltd. announced impressive second-quarter results, with record revenue of $86.8 million and operating cash flows that increased 95 percent year-over-year. Klondex also raised its 2017 production guidance. A writer on Seeking Alpha who uses the handle “Simple Digressions” has urged investors to stop shorting Klondex shares and start covering. Going into their earnings announcement, there were 16.4 million shares of short sells on Klondex which is equivalent to about 14 days of trading volume. The share price of Klondex jumped 9.22 percent on Friday when the Seeking Alpha article was published.

Threats

- Bullion Vault reports that China’s jewelry demand is at a five-year low for the quarter, but attributes this to changing consumer tastes in the younger generation. Younger buyers apparently have less affinity for gold, and are interested in spending on a variety of luxury alternatives, such as travel.

- Jeffrey Gundlach is taking a conservative approach, saying that risky assets are overvalued. He is reducing positions in junk bonds and emerging-market debt, Bloomberg reports. Gundlach commented, “This is not the time period where you say, ‘I can buy anything and not worry about the risk of it.’”

- The threats of war due to tensions between the U.S. and North Korea pose a wide risk to the markets in general.

Energy and Natural Resources Market

Strengths

- Natural gas was the best performing commodity this week, rising 7.64 percent. The commodity had its biggest weekly gain in eight months after weekly inventory reports showed a smaller than expected build, and weather forecasters suggested temperatures may rise above normal averages for the remainder of the month.

- The best performing sector this week was the S&P/TSX Gold Index. The index rose 3.70 percent as gold prices reached their highest in two months propelled by news headlines showing an escalation of hostilities between the U.S. and North Korea.

- San Juan Basin Royalty Trust, a trust which receives royalties from oil and gas properties in New Mexico, was the best performing stock this week finishing up 9.24 percent. The company rallied on the back of rising natural gas prices.

Weaknesses

- Crude oil was the worst performing commodity this week dropping 1.57 percent. The commodity slid as OPEC members revealed their consolidated July production volume, showing that compliance with the November output cap agreement fell as output rose to the highest level in 2017.

- The worst performing sector this week was the S&P 1500 Construction Materials Index. The index fell 5.48 percent after a major component of the index downgraded its full year earnings outlook citing unfavorable weather patterns for construction activity despite a robust project pipeline.

- The worst performing stock for the week was Mosaic Co. The major fertilizer producer and marketer dropped 9.92 percent to its lowest level in 10 years as prices for potash and phosphate continue to drop as additional industry capacity is expected to come online in 2017.

Opportunities

- A London Metal Exchange gauge of prices for six industrial metals has jumped to its highest in more than two years, beating major assets including U.S. equities and bonds, according to a recent Bloomberg report. China appears to be behind the metals surge as efforts by authorities to spur economic growth boosted manufacturing demand.

- The Organization of Petroleum Exporting Countries raised forecasts for the amount it needs to supply in 2017 and 2018 by about 200,000 barrels a day for each year, according to a report from its secretariat in Vienna.

- Bridgewater, the world's largest hedge fund, told clients that risks are rising and gold is set to outperform. Volatility is low, and geopolitical risks, like those between the U.S. and North Korea, are rising. Everyone should consider a 5 to 10 percent allocation to gold as a hedge, Bridgewater says.

Threats

- The recent rally in industrial metals may fade as the China Iron and Steel Association said in a statement the recent price surge isn’t driven by demand or supply cuts, but a misunderstanding of the impact government policies are having. The warning came as China’s steelmakers have been churning out record volumes to meet demand for rebar and coil that’s been underpinned by state-backed stimulus. Total steel output in June was an unprecedented 73.2 million tons.

- The global oil supply rose for a third consecutive month in July, even as the market continues to rebalance, the International Energy Agency (IEA) said Friday. In its closely watched report, the IEA said oil supply had increased by 520,000 barrels a day last month to 98.16 million barrels a day, up 500,000 barrels on a year earlier.

- The U.S. 2017 corn and soybean harvests will be bigger than expected despite a slow start to planting and concerns that hot and dry conditions stressed the corn crop during critical periods of development, the government said on Thursday.

Strengths

- The Philippines’ PCOMP Index fell a mere 6 basis points for the week in peso terms, largely escaping some of the worst negative price action for the week amongst regional peers. Also relatively better faring was Indonesia’s JCI Index, which declined 19 basis points for the week despite okay growth numbers (Indonesia’s year-over-year GDP growth came in up 5.01 percent, in line with the previous reading and slightly behind survey numbers). Malaysia’s FTSE Bursa Malaysia KLCI Index fell only 26 basis points for the week.

- China’s Producer Price Index (PPI) increased 5.5 percent year-over-year in July, reports Zacks, as a result of soaring commodity prices and resilient demand. Although the data missed analyst forecasts for a 5.6 percent rise, PPI still increased 0.2 percent on a monthly basis after three consecutive declines.

- Both imports and exports beat in Taiwan this week, coming in up 6.5 percent and 12.5 percent, respectively, both numbers ahead of expectations.

Weaknesses

- Korea’s KOSPI Index sank 3.16 percent for the week in won terms, perhaps to be expected given the escalation of rhetoric between the United States and North Korea (and the perception of somewhat higher prospects of military action in the Korean peninsula). The Shanghai Composite and the Hang Seng Composite were also down for the week, off 2.51 and 3.16 percent, respectively.

- Singapore’s retail sales missed for the month, dropping by 0.5 percent and coming in shy of expectations for a month-over-month gain of 0.6 percent.

- On Wednesday, the provincial government and official media of China reported a 7.0-magnitude earthquake that struck a remote, mountainous part of China’s southwestern province of Sichuan. According to Reuters, the quake killed 19 people and injured 247. And in the nation’s far northwestern region of Xinjiang, a separate earthquake of 6.6 magnitude hit, injuring 32 people.

Opportunities

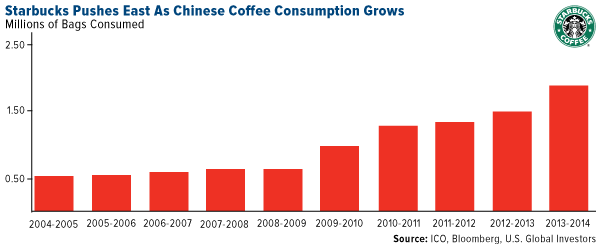

- Chinese coffee consumption is growing, reports Bloomberg, as the Asian nation prospers from urbanization, a growing middle class and rising incomes. This growth has grabbed the attention of big-brand chains including Starbucks Corp., which last month extended its reach in China.

- The U.S. and China came to a mutually agreeable proposal on upping North Korean sanctions last weekend for the United Nations—a nice stride forward on diplomatic efforts and one that may well have been (and still is being) overlooked by many given the “fire and fury” rhetoric later in the week. In some ways, after suffering a relative stinging “loss” in the form of higher sanctions—agreed to by China, no less—wouldn’t one expect an escalation of taunting rhetoric from North Korea? (It would certainly be nothing new…)

- While a government adviser in China has dismissed talk of a new round of robust growth in the nation, the opportunity to enter a new stage of “stable” economic growth (that could last a decade) has presented itself instead. Liu Shijin, vice-chairman of China Development Research Foundation, says this is thanks to more stabilized final demand, reports Reuters.

Threats

- The potential for geopolitical escalation around the North Korean situation is a primary threat this week, although at this point, most of the rhetoric and statements from both sides seem, for better or for worse, somewhat par for the course. Pyongyang threatens Guam specifically, Washington threatens “fire and fury,” and China state media suggests neutrality in the event of a North Korean first strike. Pyongyang speaks of a mid-August date; Washington talks up preemptive strikes; Beijing urges calm. Indeed, the situation and talk around it appear so elevated that hopefully the situation has already peaked.

- The Chinese authorities announced government investigations into some of the news and Internet services of major technology players, including Tencent, Weibo and Baidu, which might be a sign that Beijing is tamping down slightly on the recent rally. Tencent tumbled 5.19 percent on Friday.

- The recent pullback this week may put more profit-takers’ trigger fingers on alert in the near term.

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 40 basis points. Inflation accelerated to 2.1 percent in July, climbing back within the central bank’s 1-percent tolerance band around its 3-percent target. With inflation remaining around the lower-level band, the dovish tone could be kept in place for a bit longer.

- The euro was the best performing currency this week, gaining 46 basis points against the dollar. Morgan Stanley’s strategist, Andrew Sheets, called for a stronger euro, predicting it would reach $1.25 early next year, and trade one-for-one against the British pound for the first time. The work that Germany and France are doing together on reforms is “structurally bullish for the euro,” he said.

- The industrial sector was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing country this week, losing 1.5 percent. Turkey's industrial production grew at a slightly slower pace in June. Industrial production grew by 3.4 percent in June from the previous year. Output had advanced 3.5 percent in May and 6.7 percent in April. Production was expected to climb 3.6 percent.

- The Polish zloty was the worst performing currency this week, losing 60 basis points against the dollar. The currency weakened due to rising geopolitical tensions between the U.S. and North Korea.

- The real estate sector was the worst performing sector among eastern European markets this week.

Opportunities

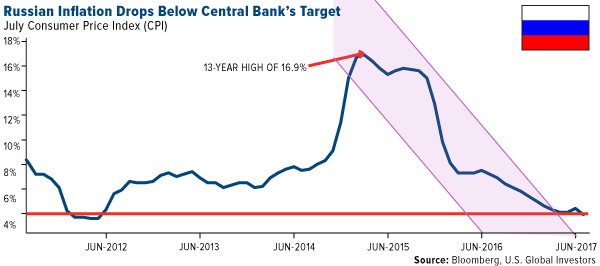

- Russia’s annual inflation rate unexpectedly fell to 3.9 percent in July, below the central bank’s target. Bank of Russia Governor Elvira Nabiullina aimed to reach 4 percent inflation by the end of this year. She may resume cutting rates at the September meeting.

- Turkish banks are seen posting a 16 to 18 percent rise in annual loans by the end of 2017, the general secretary of the Turkish Banks Association said. Loan growth in the first seven months of this year was twice that compared to the same period last year, as President Tayyip Erdogan has asked banks to lend more to help boost growth after the last year’s failed coup.

- U.S. government sanctions have no immediate implications for Russia’s sovereign credit rating, S&P Global Ratings said in a report. The rating continues to be supported by the nation’s strong external and fiscal balance sheets. Russia is rated one level below investment grade at BB+, with positive outlook at the S&P credit rating agency.

Threats

- Turkey and Germany have extensive links in trade totaling $36 billion annually, according to Wood & Company’s research team. Turkey is more dependent on Germany as exports to Germany make up around 10 percent of its total exports, while less than 2 percent of German exports are to Turkey. The tension between Germany and Turkey has dominated news recently, and Turkey has much more to lose if tension between the countries intensifies.

- Germany reported a decline in both exports and industrial output. Exports fell 2.8 percent and imports dropped 4.5 percent in June, compared with a 1.5 percent rise in exports and revised 1.3 percent gain in imports the previous month. Industrial output fell by 1.1 percent for the month, the first decline since December.

- Emerging markets are up 26 percent since December of last year, and there is a potential for a pullback. The Renaissance Capital research team expects a correction to happen by year-end, with the possibility of one as early as September when we expect to hear news from both European Central Bank (ECB) and the U.S. Federal Reserve about their balance sheet strategies. The ECB is expected to announce that it will start tapering it monthly bond buying program, and the Fed is expected to announce that it will start reducing the size of its balance sheet (by allowing mature bonds to roll off).

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All