With the arrival of late summer come quarterly earnings announcements. Most large- and mid-cap companies have already reported while a little more than half of small-caps have yet to weigh in.

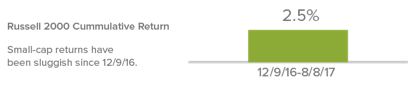

So far, the news is about what we would expect from a stock market that has been better for large-caps than small-caps in 2017, one that has seen the latter asset class consolidating as it struggles to move meaningfully past its initial post-election high on 12/9/16.

According to a recent report from Credit Suisse, quarterly earnings strength has been particularly good for large- and mid-cap stocks. For example, with roughly 61% of the companies in the Russell Midcap Index reporting, 74% of them exceeded EPS (earnings per share) estimates.

The small-cap picture is less stellar, but still positive. About 44% of the companies in the Russell 2000 have announced earnings, and 61% of them beat consensus EPS estimates.

From our perspective as small-cap specialists, however, what was most interesting was the report’s observation that both a weaker dollar and greater levels of international exposure have helped to generate earnings increases across the market cap spectrum.

The report points out that, “On an all-cap basis, so far 74% of companies with high international revenue exposure and 61% of companies with more domestic exposure have beaten consensus EPS estimates.”

This is consistent with what we have been hearing and seeing from many companies in our portfolios. Those holdings with direct or indirect global exposure have tended to see more robust increases in sales and earnings.

So while a reviving global economy could keep U.S. mid- and large-caps ahead of small-caps as a whole, we see this growth as a potential advantage for active small-cap managers who, as we do, carry a more cyclical tilt in their portfolios.

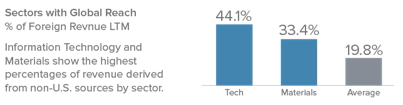

And many small-cap companies have a healthy amount of revenue coming from outside the U.S. So while the average company in the Russell 2000 derived only 19.8% of its sales from outside the U.S. at the end of June (versus about 40% for the S&P 500), the percentage of foreign sales varies widely by sector and industry.

Information Technology (44.1%) and Materials (33.4%) showed the highest percentages of revenue derived from non-U.S. sources by sector.

To be sure, our thought is that even modest global economic expansion can spur solid earnings growth, which should fuel greater relative advances for small-cap cyclicals.

Mindful of the big astronomical event that takes place on 8/21, we think there is little risk of these kinds of small-caps being eclipsed by their bigger siblings.

Stay tuned…

Important Disclosure Information

Mr. Gannon's thoughts and opinions concerning the stock market are solely his own and, of course, there can be no assurance with regard to future market movements. No assurance can be given that the past performance trends as outlined above will continue in the future.

The Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. The Russell 2000 Index is an unmanaged, capitalization-weighted index of domestic small-cap stocks. It measures the performance of the 2,000 smallest publicly traded U.S. companies in the Russell 3000 Index. The performance of an index does not represent exactly any particular investment, as you cannot invest directly in an index.

Sector weightings are determined using the Global Industry Classification Standard ("GICS"). GICS was developed by, and is the exclusive property of, Standard & Poor's Financial Services LLC ("S&P") and MSCI Inc. ("MSCI"). GICS is the trademark of S&P and MSCI. "Global Industry Classification Standard (GICS)" and "GICS Direct" are service marks of S&P and MSCI.

This material is not authorized for distribution unless preceded or accompanied by a current prospectus. Please read the prospectus carefully before investing or sending money. Investments in securities of micro-cap, small-cap, and/or mid-cap companies may involve considerably more risk than investments in securities of larger-cap companies. (Please see "Primary Risks for Fund Investors" in the prospectus.) Investments in foreign companies may be subject to different risks than investments in securities of U.S. companies, including adverse political, social, economic, or other developments that are unique to a particular country or region. (Please see "Investing in International Securities" in the prospectus.)