In some states, when a couple enters into divorce, the court may award “alimony,” or spousal support, to one of the former spouses for the express purpose of limiting any unfair economic effects by providing a continuing income to the spouse. The purpose is to help that spouse continue the “standard of living” they had during the marriage.

The idea of “maintaining a standard of living,” has become a foundational bedrock in our society today. Americans, in general, have come to believe they are “entitled” to a certain type of house, car, and general lifestyle which includes NOT just the very basic necessities of living such as food, running water and electricity, but also the latest mobile phone, computer, and Internet connection. Really, what would be the point of living if you didn’t have access to Facebook every two minutes?

One of the charts that are often bantered about in the media is the increasing prosperity of the average American as witnessed by the following chart.

But, like most data extracted from the Federal Reserve, you have to dig behind the numbers to reveal the true story.

So let’s do that, shall we?

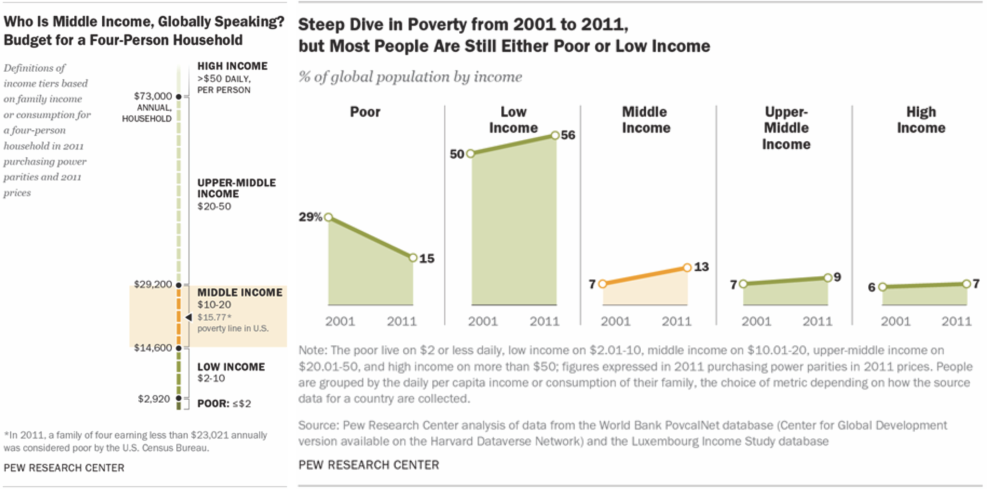

In America, the problem of maintaining the basic lifestyle is becoming ever more problematic as shown in an updated 2015 Pew Research study.

“In the U.S., the poverty line in 2011 was $15.77 per day per capita for a household with four people (the precise poverty line varies by household size and composition). The poverty line is defined as the income three times the cost of an economy food plan as determined by the U.S. Department of Agriculture (Orshansky, 1965). In July 2011, the daily per capita cost of the USDA’s thrifty food plan was $5.07 for a family of four with two children ages 6-8 and 9-11 years.”

In the U.S., the definition of

“poor” is enviable in most every other region of the world. Yet, despite higher levels of low income,

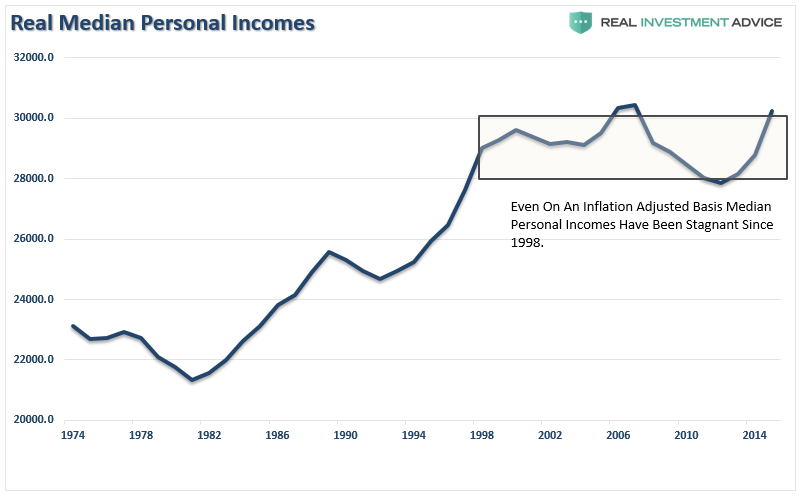

(now there’s an oxymoron) inflation-adjusted median incomes have remained virtually stagnant since 1998.

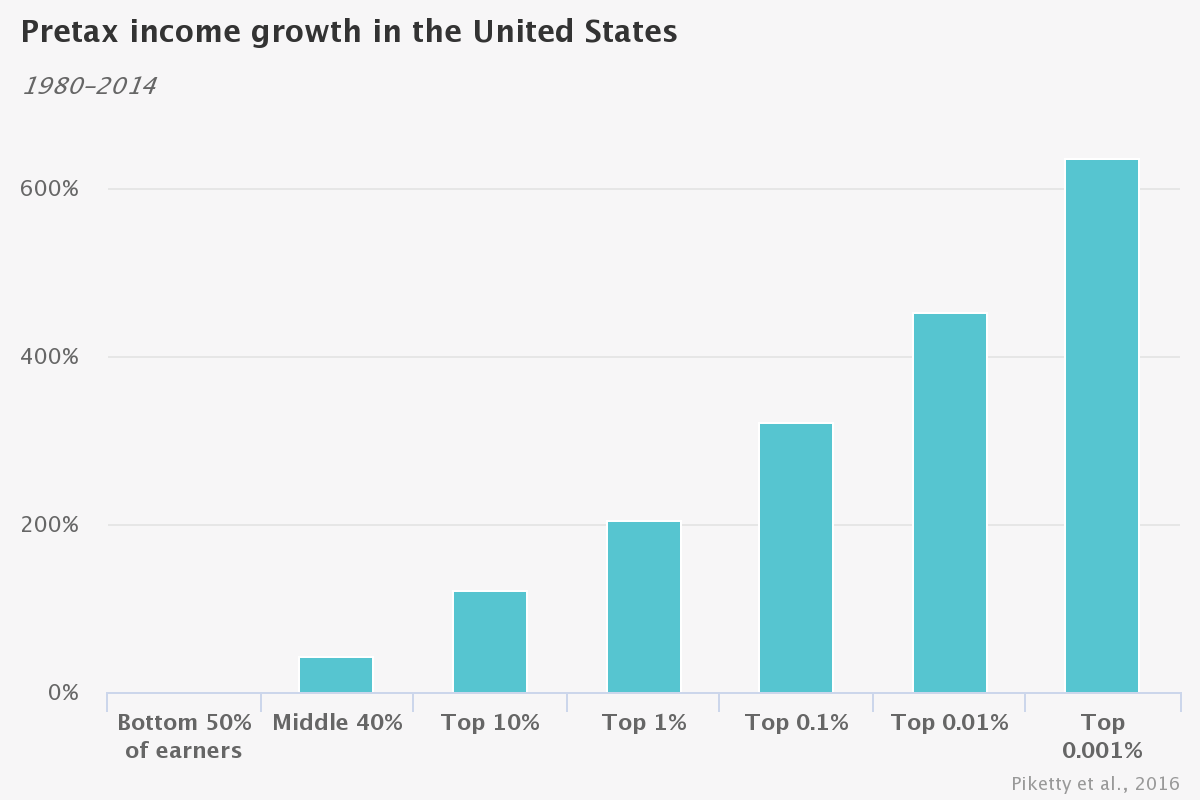

But here is why looking at the “median” of personal incomes is misleading as to what is happening within the economy. A recent study from the Chicago Booth Review revealed the underlying problem with income strata:

“The data set reveals since 1980 a ‘sharp divergence in the growth experienced by the bottom 50 percent versus the rest of the economy,’ the researchers write. The average pretax income of the bottom 50 percent of US adults has stagnated since 1980, while the share of income of US adults in the bottom half of the distribution collapsed from 20 percent in 1980 to 12 percent in 2014. In a mirror-image move, the top 1 percent commanded 12 percent of income in 1980 but 20 percent in 2014. The top 1 percent of US adults now earns on average 81 times more than the bottom 50 percent of adults; in 1981, they earned 27 times what the lower half earned.“

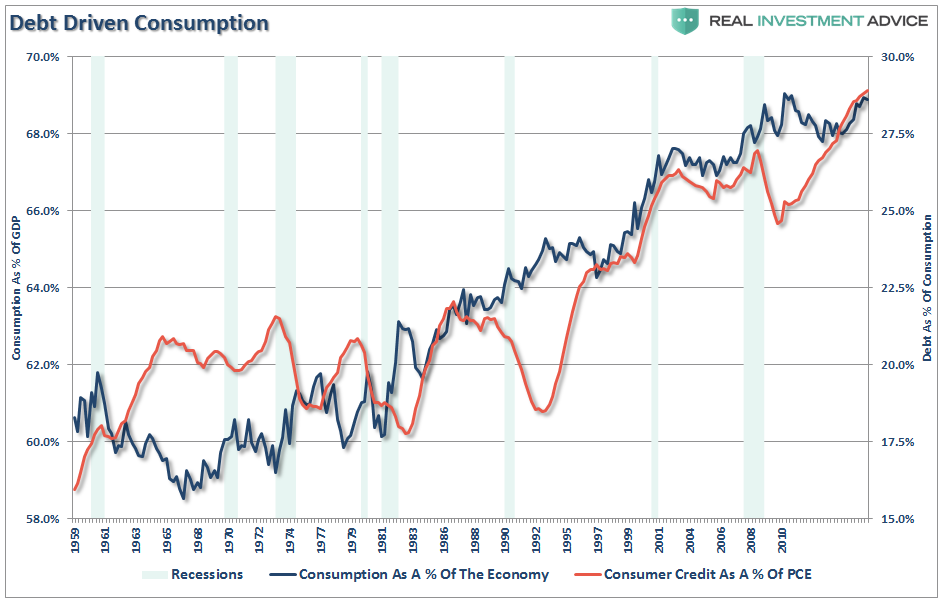

Given this information, it should not be surprising that personal consumption expenditures, which make up roughly 70% of the economic equation, have had to be supported by surging debt levels to offset the lack wage growth in the bottom 90% of the economy.

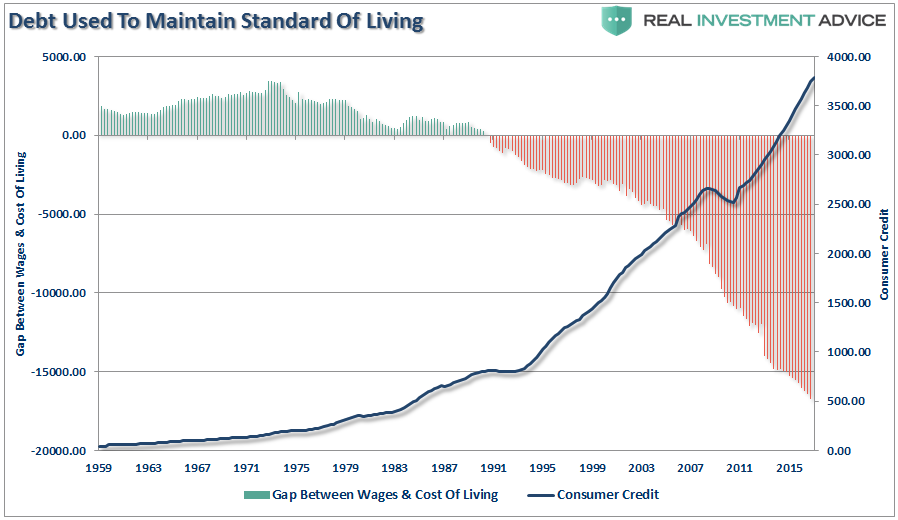

Furthermore, this also explains why the gap between wages and the cost of supporting the required “standard of living” continues to expand.

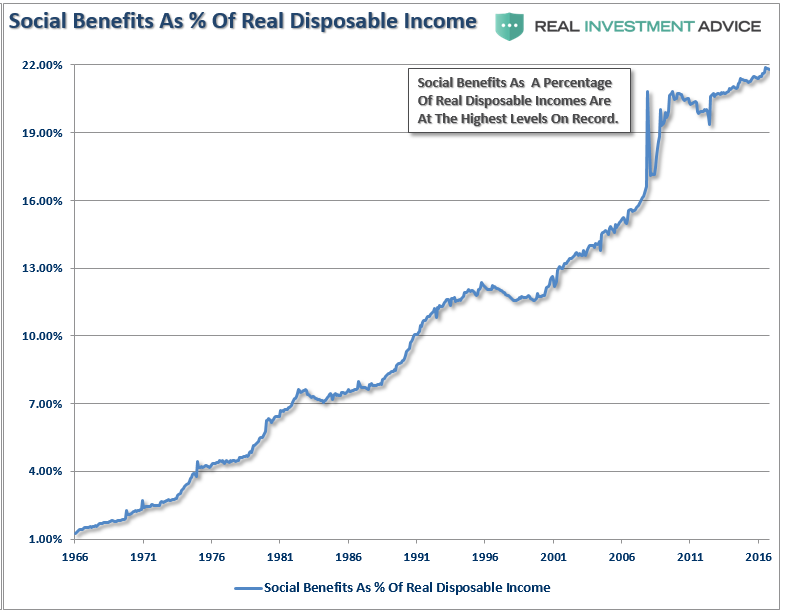

More importantly, despite economic reports of rising employment, low jobless claims, surging corporate profitability and continuing economic expansion, the percentage of government transfer payments (social benefits) as compared to disposable incomes have surged to the highest level on record.

This anomaly was also noted in the study:

“Government transfer payments have ‘offset only a small fraction of the increase in pre-tax inequality,’ Piketty, Saez, and Zucman conclude—and those payments fail to bridge the gap for the bottom 50 percent because they go mostly to the middle class and the elderly. Pretax income of the middle class (adults between the median and the 90th percentile) has grown 40 percent since 1980, ‘faster than what tax and survey data suggest, due in particular to the rise of tax-exempt fringe benefits,’ the researchers write. ‘For the working-age population, post-tax bottom 50 percent income has hardly increased at all since 1980.’”

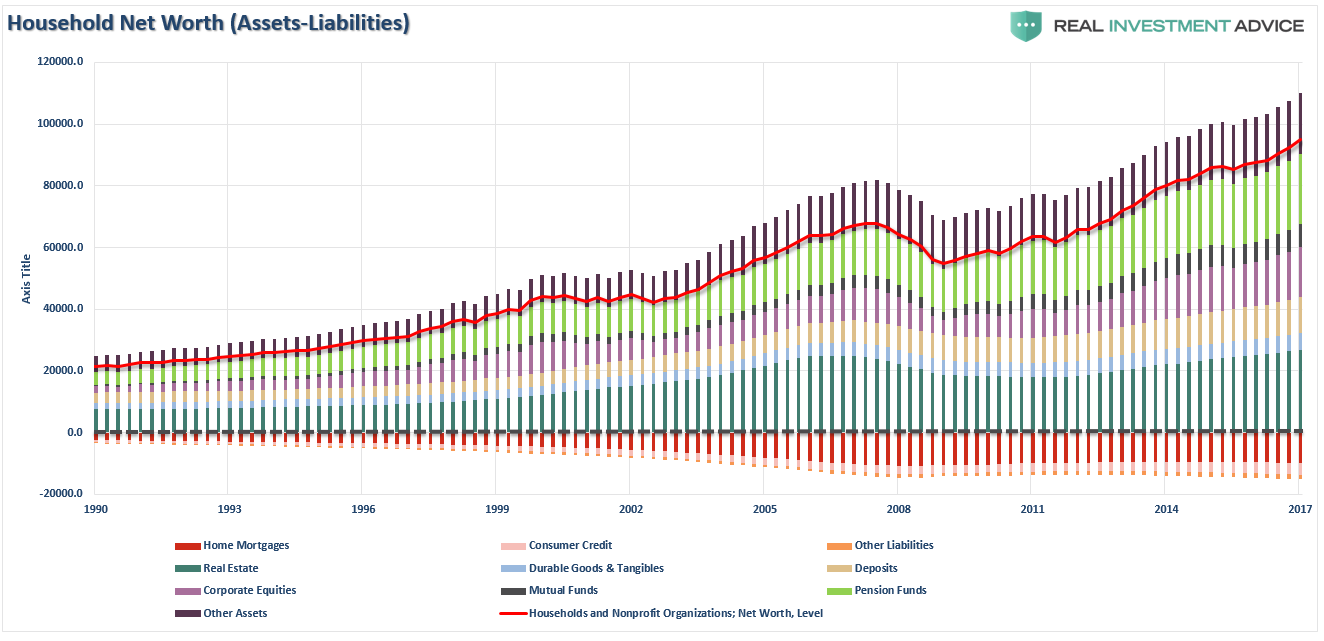

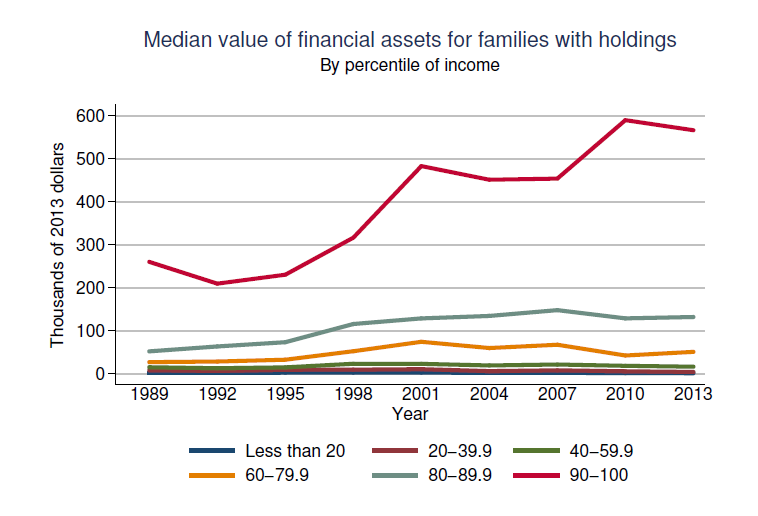

Of course, by just looking at household net worth, once again you would not really suspect a problem existed. In the Fed’s latest Flow of Funds report, the Fed revealed households currently held $110.0 trillion in assets with just a modest $15.2 trillion in liabilities, which brought the net worth of the average US household to a new all-time high of $94 trillion. The majority of the increase over the last several years has come from increasing real estate values and the rise in various stock-market linked financial assets like corporate equities, mutual and pension funds.

However, once again, the headlines are deceiving even if we just slightly scratch the surface. Given the breakdown of wealth across America we once again find that virtually all of the net worth, and the associated increase thereof, has only benefited a handful of the wealthiest Americans.

Despite the mainstream media’s belief that surging asset prices, driven by the Federal Reserve’s monetary interventions, has provided a boost to the overall economy, it has really been anything but. Given the bulk of the population either does not, or only marginally, participates in the financial markets, the “boost” has remained concentrated in the upper 10%. The Federal Reserve study breaks the data down in several ways, but the story remains the same – “if you are wealthy – life is good.”

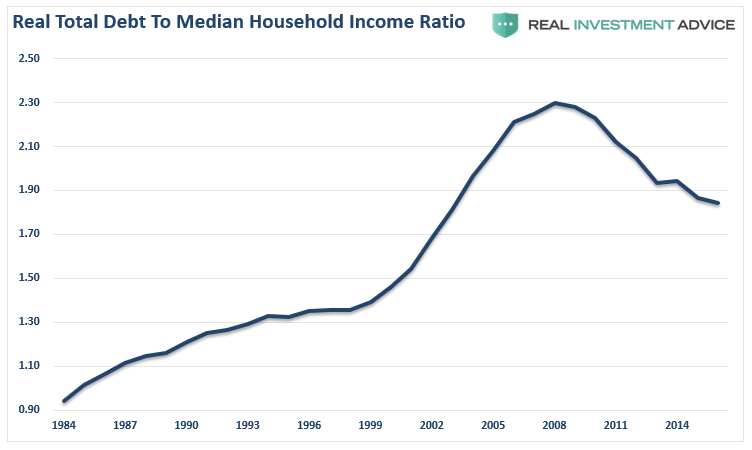

The illusion of the decline in the debt-to-income ratios leaves the majority of Americans with an inability to increase consumption, the driver of economic growth, without increasing debt burdens further. For those in the top-10% of the wealth holders, things like higher asset prices, tax cuts, etc. do not lead to further boosts in consumption as they are already consuming as needed.

The problem is quite clear. With interest rates already at historic lows, the consumer already heavily leveraged and wage growth stagnant, the capability to increase consumption to foster higher rates of economic growth is limited.

While the ongoing interventions by the Federal Reserve have certainly boosted asset prices higher, the only real accomplishment has been a widening of the wealth gap between the top 10% of individuals that have dollars invested in the financial markets and everyone else. What monetary interventions have failed to accomplish is an increase in production to foster higher levels of economic activity.

Corporate profitability, which has primarily been a function of cost cutting, increased productivity, stock buybacks, and accounting gimmicks can certainly maintain the illusion of economic prosperity on the surface, however, the real economy remains very subject to actual economic activity. It is here that the inability to re-leverage balance sheets, to any great degree, to support consumption provides an inherent long-term headwind to economic prosperity.

With the average American still living well beyond their means, the reality is that economic growth will remain mired at lower levels as savings continue to be diverted from productive investment into debt service. The issue, of course, is not just a central theme to the U.S. but to the global economy as well. After eight years of excessive monetary interventions, global debt levels have yet to be resolved.

The “structural shift” is quite apparent as burdensome debt levels prohibit the productive investment necessary to fuel higher rates of production, employment, wage growth, and consumption. Many will look back at this point in the future and wonder why governments failed to use such artificially low-interest rates and excessive liquidity to support the deleveraging process, fund productive investments, refinance government debts, and restructure unfunded social welfare systems.

Until the deleveraging cycle is allowed to occur, and household balance sheets return to more sustainable levels, the attainment of stronger, and more importantly, self-sustaining economic growth could be far more elusive than currently imagined.

In the meantime, those in the top 10% of income brackets are very likely enjoying an increase in overall prosperity. For everyone else, it is highly unlikely that debt-to-income ratios have actually improved much. But at least can bask in the reality they are “rich” compared to everyone else in the world.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“.

© Real Investment Advice

© Real Investment Advice

Read more commentaries by Real Investment Advice