Are You Prepared for These Potentially Disruptive Economic Storms?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

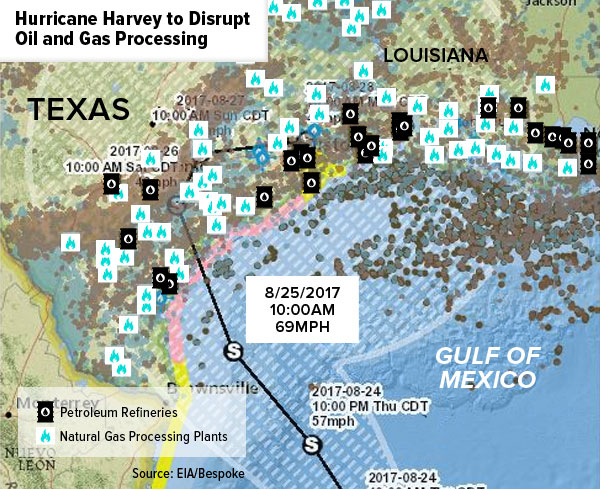

Here in San Antonio, grocery stores are packed with families stocking up on water and canned food in preparation for Hurricane Harvey, which is expected to make landfall soon after midnight tonight. I hope everyone who lives in its path has taken the necessary precautions to stay safe and dry—this storm looks as if it could be one to tell your grandkids about one day.

Similarly, I hope investors have taken steps to prepare for some potentially disruptive economic storms, including this weekend’s central bank symposium in Jackson Hole, Wyoming, and the possibility of a contentious battle in Congress next month over the budget and debt ceiling.

As you’re probably aware, central bankers from all over the globe are visiting Jackson Hole this weekend to discuss monetary policy, specifically the Federal Reserve’s unwinding of its $4.5 trillion balance sheet and the European Central Bank’s (ECB) ongoing quantitative easing (QE) program. Today Janet Yellen gave what might be her last speech as head of the Federal Reserve.

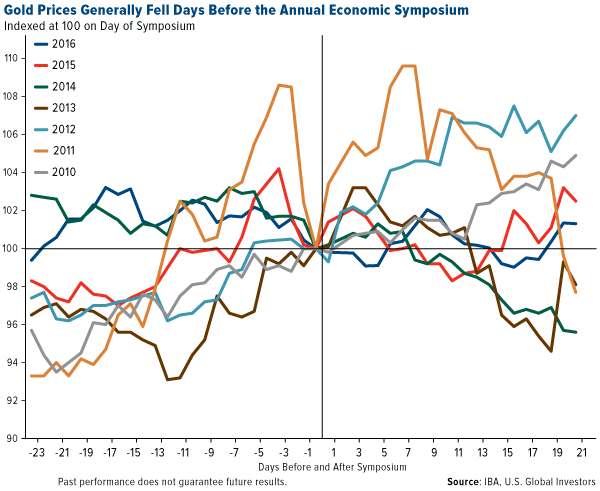

As I told Daniela Cambone on this week’s Gold Game Film, there are some gold conspiracy theorists out there who believe the yellow metal gets knocked down every year before the annual summit so the government can look good. I wouldn’t exactly put money on that trade, but you can see there’s some evidence to support the claim. In most years going back to 2010, the metal did fall in the days leading up to the summit. Gold prices fell most sharply around this time in 2011 before rocketing back up to its all-time high of more than $1,900 an ounce.

Many of the economic and political conditions that helped gold reach that level in 2011 are in effect today. That year, a similar Congressional skirmish over the debt ceiling led to Standard & Poor’s decision to lower the U.S. credit rating, from AAA to AA+, which in turn battered the dollar. The dollar’s recent weakness is similarly supporting gold prices.

In August 2011, the real, inflation-adjusted 10-year Treasury was yielding negative 0.59 percent on average, pushing investors out of government bonds and into gold. Because of low inflation, we might not be seeing negative 10-year yields right now, but the five-year is borderline while the two-year is definitely underwater. Bank of America Merrill Lynch sees gold surging to $1,400 an ounce by early next year on lower long-term U.S. interest rates.

Are Government Inflation Numbers More “Fake News”?

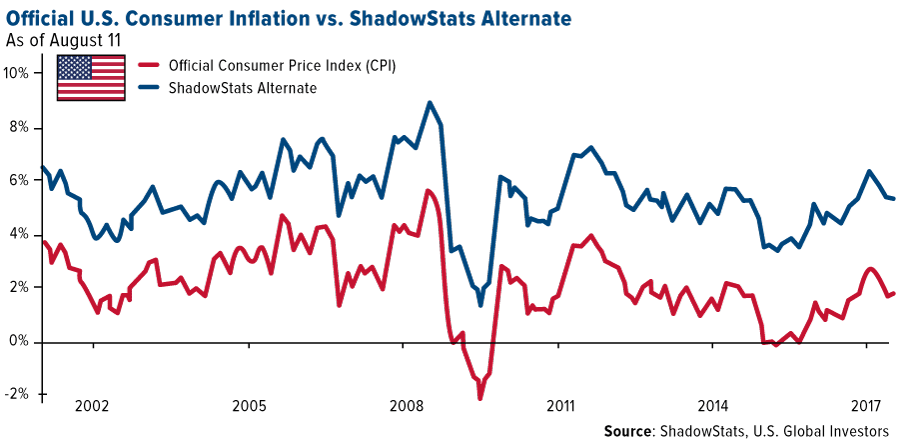

If we use another inflation measure, though, yields of all durations look very negative. For years, ShadowStats has published alternate consumer price index (CPI) figures using the methodology that was used in 1980. According to economist John Williams, an expert in government economic reporting, “methodological shifts in government reporting have depressed reported inflation” over the years. The implication is that inflation might actually be running much higher than we realize, as you can see in the chart below.

If you believe the alternate CPI numbers, it makes good sense to have exposure to gold.

Last week I shared with you that Ray Dalio—manager of Bridgewater, the world’s largest hedge fund with $150 billion in assets—was one among several big-name investors who have added to their gold weighting in recent days on heightened political risk. That includes Congress’ possible failure to raise the debt ceiling and, consequently, a government shutdown. Dalio recommends as much as a 10 percent weighting in the yellow metal, which is in line with my own recommendation of 10 percent, with 5 percent in physical gold and 5 percent in gold stocks, mutual funds and ETFs.

Falling Dollar Good for U.S. Trade

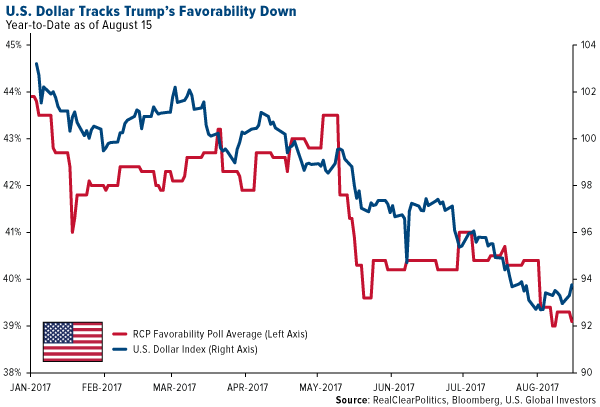

Returning to the dollar for a moment, respected CLSA equity strategist Christopher Wood writes in this week’s edition of GREED & fear that it’s “hard to believe that the political news flow in Washington has not been a factor in U.S. dollar weakness this year.”

The U.S. media certainly wants you to believe that Trump is bad for the dollar. Take a look at this chart, showing the dollar’s steady decline alongside President Donald Trump’s deteriorating favorability rating, according to a RealClearPolitics poll.

However, a weak dollar is good for America’s economy. I’ve commented before that Trump likes a falling dollar, because it is good for the country’s export trade of quality industrial products. It’s also good for commodities, which we see in a rising gold price and usually energy prices.

Ready for a Big Fight?

You might be planning to watch the Mayweather vs. McGregor fight, but have you been watching the fight between Trump and the Fed?

At the symposium in Jackson Hole earlier today, Fed Chair Janet Yellen squared up directly against Trump when she defended the strict regulations that were put in place after the financial crisis. Echoing these comments was Dallas Fed chief Robert Kaplan. This is the opposite of what Trump has been calling for, which is the streamlining of regulations that threaten to strangle the formation of capital.

It’s important to recognize that the market is all about supply and demand. The number of public companies in the U.S. has been shrinking, with about half of the number of listed companies from 1996 to 2016. Readers have seen me comment on this previously, and I believe that the key reason for this shrinkage is the surge in federal regulations. The increasingly curious thing is that we are seeing the evolution of more indices than stocks, as the formation of capital must morph.

As I told CNBC Asia’s Martin Soong this week, there is a huge amount of money supply out there, and investors are looking for somewhere to invest. The smaller pool of stocks combined with the greater supply of money means that the market has seen all-time highs. In addition, major averages were regularly hitting all-time highs not necessarily on hopes that tax reform would get passed, but on strong corporate earnings, promising global economic growth and the weaker U.S. dollar.

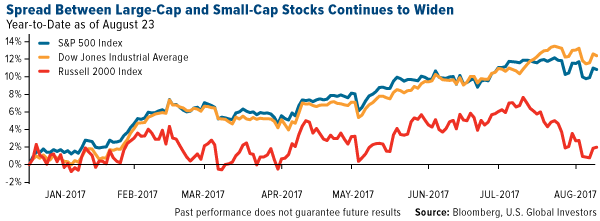

Meanwhile, small-cap stocks are effectively flat for 2017 and heading for their worst year since 1998 relative to the market, according to Bloomberg. Hedge funds’ net short positions on the Russell 2000 Index have reached levels unseen since 2009. Remember, these are the firms that were expected to be among the biggest beneficiaries of Trump’s “America first” policies.

However, the weakness in U.S. manufacturing has a great impact on the growth of these stocks, as indicated by the falling purchasing managers’ index (PMI). The slowdown in manufacturing is offset by strength in services, shown by the Flash composite PMI score of 56.0 which came out this week. Though there is a spread between large-cap and small-cap stocks, historically this strong score is an indicator of growth to come.

Stay Hopeful

It’s important to keep in mind that there will always be disruptions in the market, and adjustments to your portfolio will sometimes need to be made. For those of you who read my interview with the Oxford Club’s Alex Green, you might recall his “Gone Fishin’” portfolio, which I think is an excellent model to use—and it’s beaten the market for 16 years straight. Green’s portfolio calls for not just domestic equities, Treasuries and bonds but also 30 percent in foreign stocks and as much as 10 percent in real estate and gold.

Stay safe out there! In the meantime, explore investment opportunities in emerging markets!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.64 percent. The S&P 500 Stock Index rose 0.72 percent, while the Nasdaq Composite climbed 0.79 percent. The Russell 2000 small capitalization index gained 1.45 percent this week.

- The Hang Seng Composite gained 2.80 percent this week; while Taiwan was up 1.88 percent and the KOSPI rose 0.85 percent.

- The 10-year Treasury bond yield fell 3 basis points to 2.17 percent.

Domestic Equity Market

Strengths

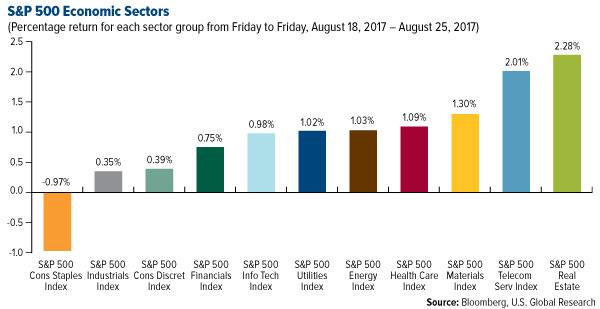

- Real estate was the best performing sector of the week, increasing by 2.28 percent versus an overall decrease of 0.85 percent for the S&P 500.

- Signet Jewelers was the best performing stock for the week, increasing 16.96 percent.

- Signet Jewelers’ shares jumped more than 15 percent in Thursday premarket trading after the company reported earnings and sales that beat expectations. The company also announced an acquisition.

Weaknesses

- Consumer staples was the worst performing sector for the week, falling 0.97 percent versus an overall decrease of 0.85 percent for the S&P 500.

- Coty was the worst performing stock for the week, falling 14.72 percent.

- Snap's lead IPO underwriter, Morgan Stanley, has turned even more bearish on the stock. In a note to clients on Wednesday, the bank lowered its price target from $16 to $14.

Opportunities

- According to Bloomberg analysts, deregulation could lift the annual pretax income of the six largest banks in the U.S. by about 20 percent. This is based on adjustments that banks can make to the mix of securities they can hold and the interest they can earn on such assets. Proposed changes would allow the banks to take on more deposits, move a greater portion of excess cash into higher yielding assets, and issue less debt.

- Apple is reportedly planning to introduce a new Apple TV capable of streaming 4K content. It would come with an updated app, and be announced at the company's hardware event alongside the refreshed iPhone and Apple Watch next month.

- The top Walmart analyst says the company has one big advantage over Amazon. That advantage is the nexus of stores and e-commerce, where Walmart’s ability to link what customers do in stores and online is ahead of Amazon.

Threats

- According to the head of quantitative research at Strategas, corporate earnings growth, which historically is the biggest contributor to share-price appreciation, has nowhere to go but down.

- Federal Reserve Chairwoman Janet Yellen had a clear message for the Trump administration Friday in her Jackson Hole speech. She warned that undoing the hard work of overhauling the financial system after the financial crisis could have dangerous consequences.

- Amazon's acquisition of Whole Foods will officially close next Monday. The two companies plan to lower the price of a number of items starting next week, and it's said that Amazon Prime members will soon get further discounts and offers. This announcement has already rattled the stocks of other grocery companies.

The Economy and Bond Market

Strengths

- According to a report released Wednesday, growth in service-based businesses helped a measure of private-sector activity reach its highest level since May 2015, reports Morningstar. “New order growth, fueled by strong economic conditions,” helped the U.S. Services PMI rise to 56.9 in August from 54.7 in July, the article continues.

- Although U.S. stocks pared gains on Friday, they did remain in positive territory after several weeks of declines, following Federal Reserve Chairwoman Janet Yellen’s speech at Jackson Hole. According to MarketWatch, Yellen offered no clues to the central bank’s monetary policy path.

- Although the Labor Department reported that initial claims for state unemployment benefits increased 2,000 for the week ended August 19, Reuters reports that claims are still below 300,000 (a threshold associated with a robust labor market). Thursday’s report shows a seasonally adjusted number of 234,000 claims.

Weaknesses

- U.S. home resales unexpectedly fell to an 11-month low in July, reports Reuters, as a “chronic shortage of properties boosted prices.” This could be the latest indication that the housing market recovery was slowing. The National Association of Realtors reported existing home sales fell 1.3 percent last month, the lowest level since August 2016.

- The U.S. dollar dropped to a three-week low today, after Yellen did not comment on monetary policy at the Jackson Hole meeting. Central bankers around the world were hoping to learn more about the Federal Reserve’s monetary policy plans.

- On Wednesday, the U.S. announced its consideration on trading limits of Venezuelan bonds. Although the market seemed muted on the news, one of the largest holders of Venezuela’s debt thinks sanctions could be a bigger problem than investors think, reports Bloomberg. Jim Craige of Stone Harbor Investment Partners says “that the economic penalties against the South American nation, especially restrictions on oil exports, could provide President Nicolas Maduro with the perfect excuse to default,” the article continues.

Opportunities

- Financial stability is on the agenda for today’s symposium in Jackson Hole. Weakening the regulations on America’s biggest banks is not a good idea, according to Robert Kaplan, chief of Federal Reserve Bank of Dallas. Kaplan said that the strong regulatory regime put in place after the financial crisis is the reason why debt levels aren’t greater than they are.

- Durable goods orders fell by 6.8 percent in July, led mainly by a sharp drop in volatile aircraft, reports Reuters. However, underneath the volatility were some bright spots and opportunities, the article continues. If transportation is excluded, orders for durable goods actually rose 0.5 percent, which would be the third straight monthly gain. “And another key measure, orders for core capital goods, a proxy for business investment, rose 0.4 percent in July,” the article continues.

- Speaking in defense of post-crisis financial regulation on Friday at the Jackson Hole Summit, Janet Yellen opened the door to at least one step that would provide substantial relief for Wall Street banks, reports the Wall St. Journal. Yellen said she would be open to some changes in simplifying the Volcker rule, which could have positive implications for investors in bank stocks.

Threats

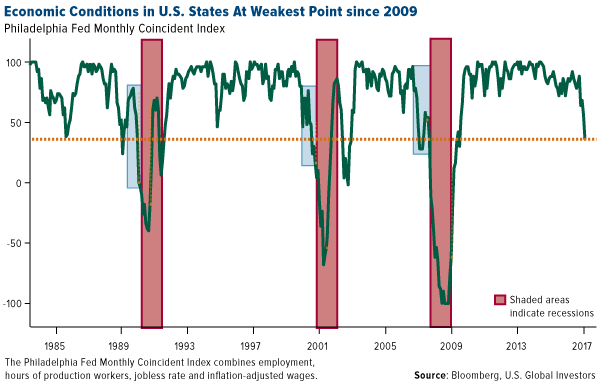

- The Federal Reserve Bank of Philadelphia’s one-month diffusion index for all 50 states fell 20 points to 36 in July, the weakest reading since 2009. The measure combines employment, hours of production workers, the jobless rate and inflation-adjusted wages. While deterioration in the index measure has often preceded past recessions, there have also been several false positives.

- According to Oppenheimer, state and local bonds are likely to become more volatile for the rest of the year.

- Municipal bond rating downgrades outpaced upgrades in the second quarter for the first time in a year, according to Moody’s. The cuts affected $81.2 billion of debt, compared to $32.5 billion of upgraded debt.

This week spot gold closed at $1,291.19 up $7.24 per ounce, or 0.56 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.07 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index came in slightly down 0.28 percent. The U.S. Trade-Weighted Dollar finished the week lower by 0.92 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

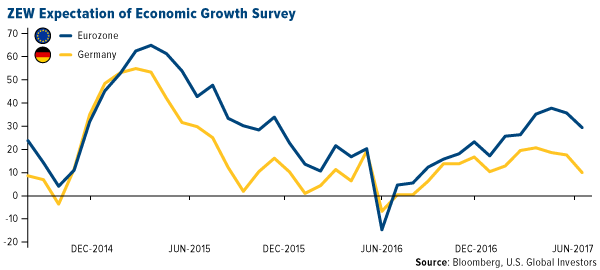

| Aug-22 | Germany ZEW Survey Current Situation | 85.2 | 86.7 | 86.4 |

| Aug-22 | Germany ZEW Survey Expectations | 15.0 | 10.0 | 17.5 |

| Aug-23 | New Home Sales | 610k | 571k | 630k |

| Aug-24 | Hong Kong Exports YoY | 9.2% | 7.3% | 11.1% |

| Aug-24 | Initial Jobless Claims | 238k | 234k | 232k |

| Aug-25 | Durable Goods Orders | -6.0% | -6.8% | 6.4% |

| Aug-29 | Conf. Board Consumer Confidence | 120.0 | -- | 121.1 |

| Aug-30 | Germany CPI YoY | 1.8% | -- | 1.7% |

| Aug-30 | ADP Employment Change | 183k | -- | 178k |

| Aug-30 | GDP Annualized QoQ | 2.7% | -- | 2.6% |

| Aug-31 | Eurpzone CPI Core YoY | 1.2% | -- | 1.2% |

| Aug-31 | Initial Jobless Claims | 263k | -- | 234k |

| Aug-31 | Caixin China PMI Mfg | 51.0 | -- | 51.1 |

| Sep-1 | Change in Nonfarm Payrolls | 180k | -- | 209k |

| Sep-1 | ISM Manufacturing | 56.5 | -- | 56.3 |

Strengths

- The best performing precious metal for the week was gold, closely followed by silver, up in tandem 0.56 percent and 0.47 percent, respectively, after a see-saw week in price action for the metals. Prices have been choppy over the last seven trading sessions but have held onto recent gains.

- As reported by ZeroHedge, the price of gold started moving up on Friday after Dallas Federal Reserve Bank President Robert Kaplan spoke on Bloomberg TV. Kaplan, who shared his thoughts ahead of Janet Yellen’s speech, said that a market correction wouldn’t necessarily hurt the economy, but instead could be healthy. The dollar also headed lower Friday after Yellen’s speech that left the possibility of a rate hike up to interpretation.

- Some investors have been pulling money from ETFs betting on gold, but hedge funds are flocking to gold, reports the Financial Times. According to the article, buying of gold futures contracts by hedge funds and other speculators has surged a record $19 billion or 474 tonnes over the past month. Analysts say this movement is spurred by concern over “lofty equity market valuations and geopolitical tensions.” Just prior to Yellen’s speech on Friday, futures contracts representing 2 million ounces of gold crossed hands, keeping the trend alive.

Weaknesses

- The worst performing precious metal for the week was platinum, down just 0.44 percent on little price-moving news over the course of the week.

- Tahoe Resources took another leg down, about 19 percent of Friday, as news from a Guatemalan Constitutional Court issued a decision to uphold the lower court’s preliminary decision to suspend mining at its Escobal Mine.

- Gold prices fell lower on Thursday as investors awaited signs on interest rates from the Jackson Hole Economic Summit, along with pressure from a firmer dollar, reports Reuters. Gold failed to break through the top of its $1,200 - $1,300 range in April and June of this year as well, but with the threat from Trump of a government shutdown, there is still underlying support for the yellow metal.

Opportunities

- The president of Novo Resources has spent 13 years searching for clues that back a hunch, reports Bloomberg: that the world’s biggest gold resource has lost siblings elsewhere on the planet. Now Quinton Tood Hennigh thinks he may have found what he has been looking for near Australia’s northwest coast. In July, Novo zeroed in on a gold find that’s confounded geologists and sparked a 500-percentsurge in the company’s share price, writes Bloomberg. Hennigh admits he isn’t 100 percent sure that this will turn into a mine, but the potential upside is seen by some as huge.

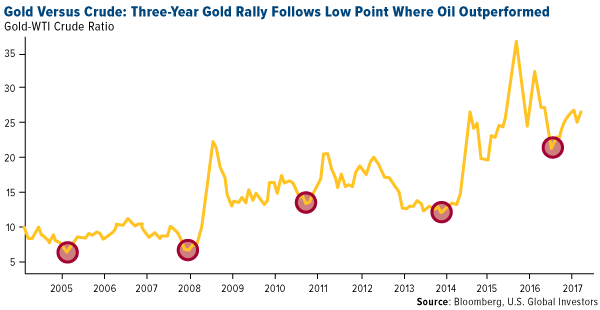

- Traders have pushed gold futures to near a nine-month high, reports Bloomberg, but if the history of gold’s relationship with oil is any guide, the surge in the yellow metal could last longer than the flare-up in geopolitical tension. Looking at the chart below, the current price divergence in oil and gold may still be going (meaning gold should continue to outperform oil before the roughly 34-month cycle ends).

- Bank of America Merrill Lynch has a bullish outlook on gold and believes the price could surge to $1,400 an ounce early next year, reports Kitco News. The bank’s global head of commodities research, Francisco Blanch, says one major catalyst for this could be the European Central Bank embarking on a tightening cycle. Nearer term, Trump’s threat to shut the government down, (unless Congress agrees to fund the border wall with Mexico) with the approaching debt ceiling coming into focus, could generate enough uncertainty to spark a convincing rally through $1,300 per ounce.

Threats

- More of China’s consumers “are giving up substance for style when it comes to gold,” reports The Asian Review. Happy to buy less-pure pieces if it means keeping up with the latest trends, sales of platinum and 18-karat gold pieces in China climbed 22 percent on the year for the April-June quarter. China is the world’s second-largest gold consumer, “but overall consumption of the yellow metal in China could start to dip if 18- and 22-karat jewelry gains traction,” the article continues.

- Investors have made a fortune on palladium this year; in fact, the metal surged 38 percent to its highest price since 2001, reports Bloomberg. That’s the good news. The bad news? ETFs that track the precious metal have lost more than $49 million as investors are cashing out. “The explanation for the outflows lies in part in the scarcity of physical palladium and a robust borrowing market that has developed among users and speculators,” the article reads.

- Is the Brazilian government trying to balance the books on the back of the Amazon jungle? Opening an area for mining known as Renca or the National Reserve of Copper and Associates, which was set aside by the military government three decades ago to safeguard resources and sovereignty, is drawing plenty of criticism from environmental groups. Belo Sun Mining has had its mining permits in limbo after indigenous groups got the company’s mining license suspended.

August 22, 2017Exclusive Interview (Part II): Alex Green on the Biggest Threat We Face |

August 21, 2017Exclusive Interview: How Alex Green Beat the Market 16 Years Straight |

August 16, 2017Gold Was Chemically Destined to Be Money All Along |

Energy and Natural Resources Market

Strengths

- Gasoline was the best-performing commodity in the energy sector this week, rising 3.3 percent. The commodity rallied as Hurricane Harvey, expected to make landfall this weekend over southeast Texas, has driven gulf refineries to shut down temporarily as a precaution.

- The best-performing sector this week was the FTSE 350 Mining Index. The index of major diversified miners rose 5 percent, tracking a rising copper price as well as news that BHP plans to sell its U.S. onshore oil assets, which were well received by investors.

- JSW SA, an industry-leading Polish coal miner, was the best-performing stock this week, finishing up 17 percent. The company rallied to its highest level since 2011 after reporting earnings that beat analyst expectations the previous week, as well as rallying thermal and metallurgical coal prices this week.

Weaknesses

- Zinc was the worst-performing commodity this week, dropping 0.2 percent on the London Metals Exchange. After last week’s breathtaking rally, which took the metal to a 10-year high, the price dropped after the Shanghai Futures Exchange enacted changes to curtail speculation in its zinc trading amid record volumes.

- The worst-performing sector this week was construction and materials. The group fell 1.7 percent after disappointing housing data for July suggests the industry may be slightly oversupplied and weakness may in the cards for the short term.

- The worst-performing stock for the week was BlueScope Steel Limited. The largest Australian steelmaker dropped 20 percent after the company projected a drop in profit and warning that its business is being hit by a “flood of very cheap product,” likely referring to China’s rapid steel output growth in the past few months.

Opportunities

- China's largest state-owned commercial banks have begun to raise tens of billions of dollars to fund the country's “Silk Road” investments. Chinese President Xi Jinping in May pledged a $124 billion funding boost to help his plan to build a modern “Silk Road,” connecting China with new and old trading partners. The projects comprised of roads, railways and other major civil works should provide a tailwind for commodity demand over the next decade.

- U.S. crude oil production rose at a rate of 26 thousand barrels per day (kb/d) this past week, significantly below the recent pace of production increases. Investors reacted favorably to the data release, with the expectation that further weakness in U.S. production growth may support a much anticipated rebalancing in the global crude oil market.

- The buying of gold futures contracts by hedge funds and other speculators has surged a record $19 billion over the past month, spurred by concern over geopolitical tensions. Unfortunately, the action hasn’t yet translated into significantly higher gold prices, as gold-backed ETFs have recorded outflows over the same period. There is opportunity for long-term funds and retail investors, who are more likely to purchase gold-backed products to also hedge their best as geopolitical tensions remain elevated.

Threats

- Steel and iron ore prices dropped heavily on Wednesday, cutting short a rally that lifted iron ore to five-month highs earlier in the week. The slide came after the China Iron and Steel Association said it saw little likelihood of a big shortage in steel supply, despite a crackdown against polluting industries and producers of low-quality steel, limiting the prospect of further price surges.

- The Shanghai Futures Exchange (SHFE) has enacted changes to curtail speculation in its zinc contracts trading after prices rallied to a ten-year high amid a surge in volumes. The exchange imposed a cap on new position sizes and raised transaction fees. The SHFE’s curbs come a week after a warning that investors should be cautious in their trading as the exchange will look to intervene when necessary to stop speculators from becoming the driving force behind prices.

- July new U.S. home sales dropped 9.4 percent year-on-year, well below expectations and to the slowest pace since December. In addition, the supply of new homes for sale rose 1.5 percent, the highest supply growth rate since June 2009. The reading has negative connotations for prices of lumber and other construction materials.

Strengths

- Hong Kong’s Hang Seng Composite Index (HSCI) climbed 2.80 percent for the week, buoyed by earnings and relative market optimism while bucking a one-day closure for Typhoon Hato.

- The Shanghai Composite Index, which rose 1.93 percent for the week, jumped to new 52-week highs, reclaiming levels last seen in the early days of 2016.

- Thailand’s second-quarter GDP came in ahead of expectations. Second-quarter GDP beat quarter-over-quarter, coming in at 1.3 percent and ahead of surveyed expectations for 1.0 percent. Year-over-year GDP for the second quarter period came in up 3.7 percent, ahead of expectations for 3.2 percent.

Weaknesses

- Singapore’s Straits Times Total Return Index dropped 82 basis points for the week, while the FTSE Bursa Malaysia KLCI Index fell 22 basis points for the week.

- A maximum category 10 typhoon hit Hong Kong earlier this week, reports Reuters, leaving the financial hub with uprooted trees, flooded streets and closed businesses. There were 34 people injured in Hong Kong, and three people died in Macau. More than 450 flights were cancelled, financial markets were suspended for one day and schools were closed, the article continues. Markets did reopen and follow global markets higher the one-day reprieve.

- Year-over-year export orders in Taiwan came in up 10.5 percent, shy of analysts’ expectations for a rise of 13.0 percent for the July period.

Opportunities

- Despite China installing industrial robots at a furious pace, data from the International Federation of Robotics shows that the nation’s level of automation remains relatively low, at least compared with other major economies, reports Bloomberg. Although China is lagging in comparison, as seen in the chart below, this only indicates significant scope for further investment, the article continues. The task of “retooling” (if you will) the Chinese economy for a China 2.0 is not without obvious challenges, e.g. existing manpower, employment and industrial overcapacity, but the sheer scale of growth potential on the robotics side in China remains impressive nonetheless.

- According to Reuters, Saudi Arabia is considering funding itself partly in Chinese yuan, said a senior Saudi official on Thursday. Such a move would mean closer financial ties between the two countries. “Obtaining some funds in yuan could give Riyadh more financial flexibility and would mark a success for China, the biggest market for Saudi oil, in its drive to make the yuan a top international currency,” the story reads.

- While both Great Wall and Geely Auto have denied current talks about any sort of Fiat Chrysler deal, analysts have continued to speculate about the possibilities, with Great Wall allegedly and particularly interested in the Jeep SUV brand. To be sure, the are-the-sum-of-the-parts-worth-greater-than-the-whole question seems to be very much in play among analysts at the moment. We take no particular slant on the possibilities here, other than to observe the growth within the auto industry, broadly speaking, of Chinese producers and of their increasingly global reach and place within the conversation.

Threats

- The U.S. is probing China’s practices on intellectual property and the Asian nation is not happy about it, reports Bloomberg. Ministry of Commerce spokesman Gao Feng said on Thursday that the two nations have more shared interests than disputes, but China is displeased nonetheless and is accusing the Trump administration of “sabotaging the international trading system.”

- Chinese President Xi Jinping’s efforts to strengthen the Communist Party’s role throughout the country has reached the China operations of foreign companies, reports Reuters, and executives at some of those entities aren’t liking the demands they are facing. All companies in China, even foreign firms, have long been required by law to establish a party organization. And while that has been more symbolic, the bigger worry comes from “political pressure” to revise the terms of their joint ventures to allow the party final say over business operations and investment decisions.

- Starting next week, the next round of PMI numbers for the region start rolling in. Investors will be looking for the data to continue to support relative market optimism and valuations.

Emerging Europe

Strengths

- Poland was the best performing country this week, gaining 3.4 percent. The unemployment rate was reported at 7.1 percent, the lowest reading since 1991. Poland also set next year’s budget deficit at 41.5 billion zloty, 30 percent below this year’s level. The Polish government expects growth to accelerate and consumption to remain strong.

- The Turkish lira was the best performing currency this week, gaining 2.3 percent against the dollar. The lira appreciated the most after Janet Yellen’s remarks in Jackson Hole were released. She largely defended post-crisis financial regulations, not commenting on monetary policy or the outlook for the economy, bucking speculation that she might strike a hawkish tone. The lira remains the worst performer among major currencies over the last year, and could be a big winner if the Federal Reserve decides not to change its policy drastically in the near future.

- The financial sector was the best performing sector among eastern European markets this week.

Weaknesses

- The Czech Republic was the worst relative performing country this week, gaining 35 basis points. The Consumer and Business Confidence reading was reported at 5.5, above the prior level of 3.3. Komercni Bank was the weakest performing equity on the Prague Exchange, losing more than 2 percent in the past five days.

- The Russian ruble was the worst relative performing currency this week, gaining 50 basis points against the dollar. The Bank of Russia will probably resume easing in September. BI Economics expects a 50 basis point cut to 8.5 percent in September and a 25 basis point move in December, with a pause in between.

- The real estate sector was the worst performing sector among eastern European markets this week.

Opportunities

- According to an article published this week in the Wall Street Journal, growth is taking off around the world. All 45 countries tracked by the Organization of Economic Cooperation and Development are on track to grow this year, and 33 of them are poised to accelerate from a year ago. It is the first time since 2007 that all countries are growing and most countries are in acceleration since 2010.

- The MSCI Emerging Markets Index is up 23 percent year-to-date, and Credit Suisse is saying that it is not too late to get on the emerging markets stocks bandwagon. Emerging market equities are in “mid-cycle” of their current outperformance phase versus developed markets. The broker recommends an overweight of Russian and Polish stocks, and market weight of Turkish equities.

- Today is the first day of the annual Jackson Hole symposium, during which leaders from around the world are discussing important economic issues. So far, no major changes to monetary policies were announced. If U.S. and EU leaders continue to support monetary easing, emerging markets will likely continue to rally.

Threats

- Germany’s economic confidence weakened to a 10-month low in August. The ZEW Indicator of Economic Sentiment declined to 10.0 from 17.5 in the prior month. ZEW President Achim Wambach said that the significant decrease reflects the high degree of nervousness over the future path of growth in Germany. Contradictory, preliminary August Manufacturing PMI data, which is considered a good guide to economic growth too, was reported at 59.4, the third-highest reading in more than six years.

- A Russian court ordered private conglomerate Sistema to pay 136 billion rubles ($2.3 billion) to Rosneft , the largest state owned oil company, for illegally stripping assets from Bashneft while under the conglomerate’s ownership between 2009 and 2014. Bashneft was sized by the Russian state from Sistema in 2014, after investigators found that its initial privatization was illegal. Many investors are nervous about legal protection of private property in an economy with a long history of state controlled entities taking control of private assets.

- There has been a growing concern about the financial stability of Bank Otkritie, Russia’s second-largest private bank. In the months of June and July, clients withdrew 26 percent of their deposits. Local media reported that the central bank is considering transferring the lender to a bailout fund.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits