We Looked into the Effects of Hurricane Harvey and Here’s What We Found

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Unless you’ve been away from a TV, computer or smartphone for the past week, you’ve likely seen scores of pictures and videos of the unprecedented devastation that Hurricane Harvey has brought to South Texas and Louisiana. As a Texan by way of Canada, I’d like to take a moment this week to reflect on the human and economic impact of this storm, one of the worst natural disasters to strike the U.S. in recorded history.

Below are some key data points and estimates that help contextualize the severity of Harvey and its aftermath.

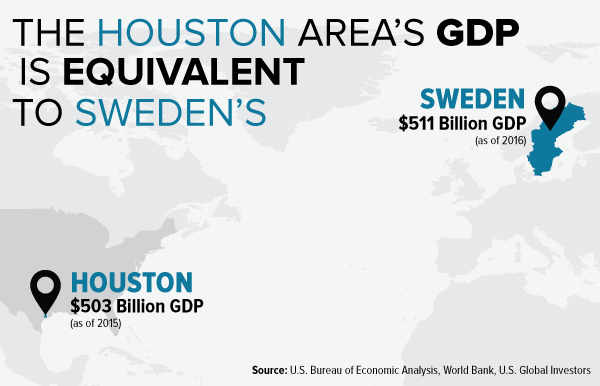

$503 Billion

In a previous Frank Talk, “11 Reasons Why Everyone Wants to Move to Texas,” I shared with you that the Lone Star State would be the 12th-largest economy in the world if it were its own country—which it initially was before joining the Union in 1845. Following California, it’s the second-largest economy in the U.S. A huge contributor to the state economy is the Houston-Woodlands-Sugar Land area, which had a gross domestic product (GDP) of $503 billion in 2015, according to the U.S. Bureau of Economic Analysis. Not only does this make it the fourth-largest metropolitan area by GDP in the U.S., but its economy is equivalent to that of Sweden, which had a GDP of $511 billion in 2016.

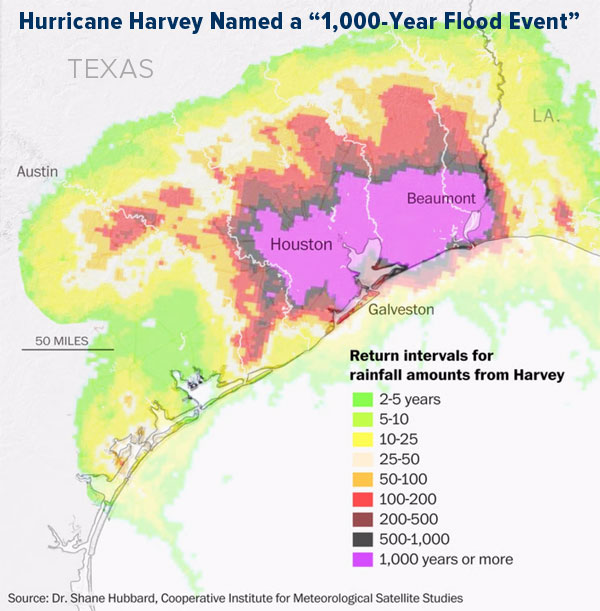

1-in-1,000 Years

The amount of rain that was dumped on parts of Southeast Texas set a new record of 51.88 inches, breaking the former record of 48 inches set in 1978. But now we believe it exceeds that of any other flood event in the continental U.S. of the past 1,000 years. That’s according to a new analysis by the Cooperative Institute for Meteorological Satellite Studies and Dr. Shane Hubbard, a researcher with the University of Wisconsin-Madison. Hubbard’s conclusion required the use of statistical metrics since rainfall and flood data go back only 100 years or so, but the visual below might help give you a better idea of just how rare and exceptional Harvey really is.

$190 Billion

According to one estimate, Hurricane Harvey could end up being the costliest natural disaster in U.S. history. Analysts with Risk Management Solutions (RMS) believe economic losses could run between $70 billion and $90 billion, with a majority of the losses due to uninsured property. This is a conservative estimate compared to AccuWeather, which sees costs running as high as $190 billion, or the combined dollar amounts of Hurricanes Katrina and Sandy. If so, this would represent a negative 1 percent impact on the nation’s economy.

The wind and rains damaged more than just houses, schools, refineries and factories. According to Cox Automotive, which controls Kelley Blue Book, Autotrader.com and other automotive businesses, as many as half a million cars and trucks could have been rendered inoperable because of the flooding. That figure’s double the number of vehicles that were destroyed during Hurricane Sandy in 2012. What this means, of course, is that auto dealerships are going to have their work cut out for them once the waters recede and insurers start cutting some checks. Buyers can likely expect to see a huge premium on used cars.

24%

Most people know that Texas is oil country. What they might not know is that it’s also the nation’s number one gasoline-producing state, accounting for nearly a quarter of U.S. output, as of August. In addition, the Lone Star State leads the nation in wind-powered generation capacity, natural gas production and lignite coal production, according to the Energy Information Administration (EIA).

600,000 Barrels a Day

The largest oil refinery in the U.S. belongs to Motiva Enterprises, wholly controlled by Saudi Aramco, the biggest energy company in the world. Located in Port Arthur, about 110 miles east of Houston, Motiva is capable of refining up to 603,000 barrels of crude a day. As floodwaters gradually filled the facility, the decision was made Wednesday to shut it down completely, and as of Friday morning, there’s no official timetable as to when operations might begin again, according to the Houston Business Journal. The consequences will likely reverberate throughout the energy sector for some time.

Motiva isn’t the only refinery that was affected, of course. As much as 31 percent of total U.S. refining capacity has either been taken offline or reduced dramatically because of Harvey, according to CNBC. The Houston area alone, known as the energy capital of the world, is capable of refining about 2.7 million barrels of crude a day, or 14 percent of the nation’s capacity.

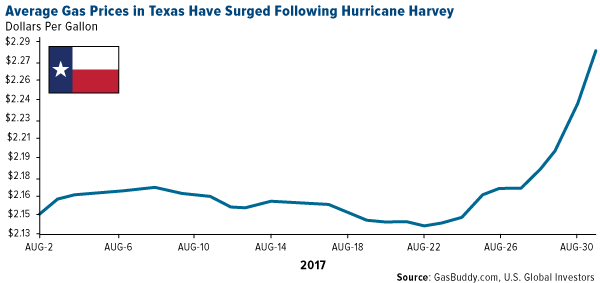

$2.33 a Gallon

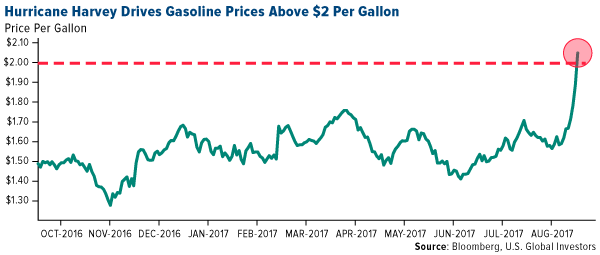

As of Friday morning, gas prices in Texas had surged to $2.33 a gallon on average, more than a two-year high, according to GasBuddy.com. In the Dallas-Ft. Worth area, prices at some pumps are reportedly near $5 a gallon.

With concerns that a gas shortage might hit the state, panicked Texas consumers lined up outside numerous stations, sometimes for miles, to drain them dry. By 5:00 on Thursday, the 7-Eleven next door to U.S. Global headquarters was serving diesel only.

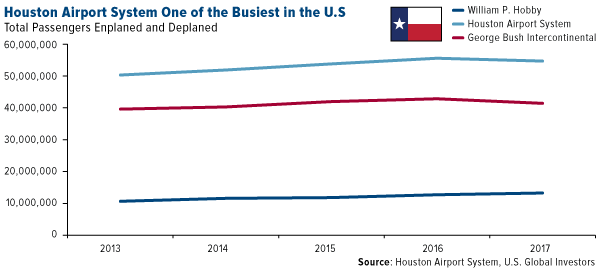

The Houston Airport System is one of the busiest in the world, with the total number of passengers enplaned and deplaned standing at roughly 54 million, as of April 2017. Flights at the city’s two largest airports, Bush Intercontinental and Hobby, were suspended Sunday, with more than 900 passengers stranded between the two. Commercial traffic resumed on Wednesday, though service was limited. According to Bloomberg, United Airlines, which has a major hub at Bush Intercontinental, was scheduling only three arrivals and three departures a day.

The International Business Times reports that several major airlines are offering frequent flyer miles in exchange for donations to Hurricane Harvey disaster relief. American Airlines, for example, will provide 10 miles for every dollar donated to the American Red Cross after a minimum $25 contribution. Other carriers have similar programs, including United, Delta Air Lines, Southwest Airlines and JetBlue Airways.

The Kindness of Strangers

For all the talk of economic impact and barrels of oil, it’s important we keep in mind that Hurricane Harvey has had real consequences on individuals, families and businesses. Many of them have lost everything.

I might not have been born in the U.S., but I’ve always been moved and inspired by how selflessly Americans rally together and rush to each other’s aid in times of dire need.

This, of course, is one of those times, and I urge everyone reading this to consider donating to a reputable charity of your choice. For our part, U.S. Global Investors will be donating money, food, clothing and other necessities to one of our favorite local charities, the San Antonio Food Bank.

Please keep the people of South Texas and Louisiana in your thoughts and prayers, and have a blessed weekend!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.80 percent. The S&P 500 Stock Index rose 1.37 percent, while the Nasdaq Composite rose 2.71 percent. The Russell 2000 small capitalization index gained 2.62 percent this week.

- The Hang Seng Composite gained 0.69 percent this week; while Taiwan was up 0.75 percent and the KOSPI fell 0.88 percent.

- The 10-year Treasury bond yield fell less than 1 basis point to 2.16 percent.

Domestic Equity Market

Strengths

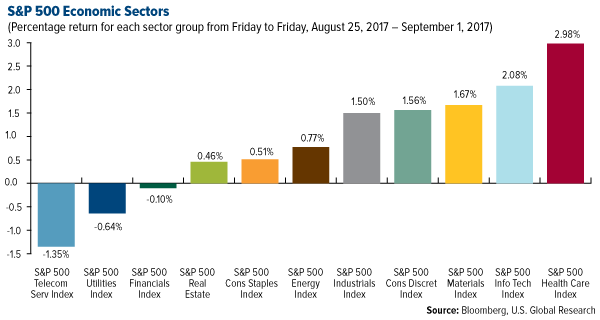

- Healthcare was the best performing sector of the week, increasing by 2.98 percent versus an overall increase of 1.43 percent for the S&P 500.

- Gilead Sciences was the best performing stock for the week, increasing 13.50 percent.

- Gilead Sciences gained 7.3 percent after Swiss drug maker Novartis was awarded the first approval by the FDA for a certain type of promising new cancer treatment. While this does not benefit Gilead directly, it does bolster investors' confidence that the company made the right decision when it acquired Kite Pharma, Inc. on Monday.

Weaknesses

- Telecommunication was the worst performing sector for the week, falling 1.35 percent versus an overall increase of 1.43 percent for the S&P 500.

- Best Buy was the worst performing stock for the week, falling 11.94 percent.

- Best Buy shares plunged after the company warned about gross margin pressures on its earnings call.

Opportunities

- Apple's Siri efforts are now being led by software Senior VP Craig Federighi instead of online services Senior VP Eddy Cue, who previously led its development according to official corporate bios. The change highlights the increasing importance of artificial intelligence and so-called intelligent assistants like Siri as the top technology companies like Amazon, Google, Microsoft and Facebook all ramp up their own efforts.

- President Donald Trump is backing down from a threat to force a government shutdown over funding for his proposed wall along the U.S.-Mexico border, according to a Friday report from The Washington Post. Any threat of a shutdown poses big potential turmoil for stocks.

- The dollar dipped after the August jobs report came in weaker than expected. The greenback has been tumbling since U.S. President Donald Trump's inauguration, falling by about 10 percent so far. A cheaper dollar is bullish for export-oriented companies.

Threats

- The EU Competition Commissioner compared German car cartels with Google. Volkswagen, Daimler, BMW, Audi and Porsche have to face drastic consequences in the diesel sector, according to Business Insider Deutschland.

- Gas prices are spiking after the biggest U.S. refinery shut down. Higher gas prices could dampen consumer spending, hurting the overall economy, especially consumer discretionary stocks.

- The damage from Hurricane Harvey could cost insurance companies billions of dollars, leading to major financial losses.

August 30, 2017Got a Bully Problem? Send in a Tough Guy |

August 28, 2017Are You Prepared for These Potentially Disruptive Economic Storms? |

August 22, 2017Exclusive Interview (Part II): Alex Green on the Biggest Threat We Face |

Strengths

- U.S. second-quarter growth was revised upward to the fastest pace in two years on stronger household spending and a bigger gain in business investment, according to Commerce Department data. GDP rose at an annualized rate of 3 percent from the prior quarter, revised upward from an initial estimate of 2.6 percent.

- Manufacturing activity was the strongest in six years in August, according to a survey of purchasing managers released Friday. The ISM Manufacturing Index climbed to 58.8 percent in August from 56.3 percent in July. That was the highest reading since April 2011.

- In global fixed-income markets, U.S. bonds are the best performers across major markets this year based on broad market indexes for developed countries, according to Bloomberg. The U.S. broad bond market has returned 3.3 percent this year through August 24, with Australia and the U.K. next and Germany the worst with a 0.2 percent loss.

Weaknesses

- Job growth lagged in August, with the economy adding a lower-than-projected 156,000 jobs (versus expectations of 180,000) and the unemployment rate ticking up slightly to 4.4 percent.

- U.S. construction spending unexpectedly fell in July, falling to a nine-month low amid a steep decline in investment in private structures. The Commerce Department said on Friday that construction spending decreased 0.6 percent. That was the lowest level since October 2016 and followed a downwardly revised 1.4 percent decrease in June.

- Consumer sentiment pulled back to a final August reading of 96.8 in August from a preliminary reading of 97.6, according to the University of Michigan gauge released Friday.

Opportunities

- President Trump reiterated his commitment to a 15 percent business tax rate in a speech August 30. He also said changes to the tax code would cut loopholes that benefit special interests and reshape the system into one that is “simple, fair and easy to understand.”

- Offering incentives to spur spending by states, localities and the private sector will be the largest federal piece of President Trump’s $1 trillion infrastructure plan, said Budget Director Mick Mulvaney. One such possible incentive being considered is encouraging governments to move assets they own off their books into the private sector, generating funding for new projects.

- Given the damage wreaked by Hurricane Harvey in Texas, there is concern about the impact on municipal bonds in that area. According to Moody’s, it is extremely unlikely that a borrower will default. In the past, natural disasters haven’t caused a single default by a municipal borrower that was rated by Moody’s.

Threats

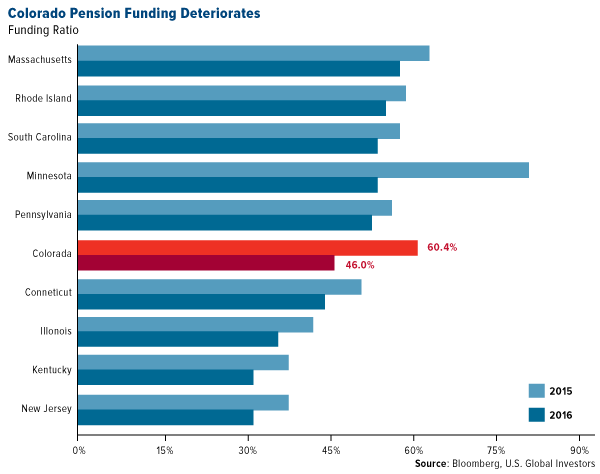

- The funding level of U.S. state pensions declines almost 5 percent to 68.6 percent on average between 2015 and 2016, according to Bloomberg. For the second consecutive year, New Jersey, Kentucky, Illinois and Connecticut have had the lowest state pension funding ratios. Notable moves in the worst 10 states for pension funding include Colorado, rising from eighth to the worst funded, and Minnesota moving from 30th to seventh. Actuarial changes account for the worsening positions of both states.

- Hurricane Harvey’s damage may affect Municipal Utility Districts, which issue bonds to finance infrastructure for new housing developments. The debt is repaid through a portion of homeowners’ property taxes. If there is an exodus of people after the storm it could hinder their ability to make debt payments, according to S&P.

- A bond market crash is one of the top tail risks from Bank of America Merrill Lynch’s August fund manager survey.

This week spot gold closed at $1,324.95 up $33.58 per ounce, or 2.60 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 5.75 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index came in up just 1.17 percent. The U.S. Trade-Weighted Dollar finished the week slightly higher by 0.10 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Aug-29 | Conf. Board Consumer Confidence | 120.7 | 122.9 | 120.0 |

| Aug-30 | Germant CPI YoY | 1.8% | 1.8% | 1.7% |

| Aug-30 | ADP EMployment Change | 185k | 237k | 201k |

| Aug-30 | GDP Annualized QoQ | 2.7% | 3.0% | 2.6% |

| Aug-31 | Eurozone CPI Core YoY | 1.2% | 1.2% | 1.2% |

| Aug-31 | Initial Jobless Claims | 283k | 236k | 235k |

| Aug-31 | Caixin China PMI Mfg | 51.0 | 51.6 | 51.1 |

| Sep-1 | Change in Nonfam Payrolls | 180k | 156k | 189k |

| Sep-1 | ISM Manufacturing | 56.5 | 58.8 | 56.3 |

| Sep-5 | Durable Goods Orders | 1.0% | -- | -6.8% |

| Sep-7 | ECB Main Refinancing Rate | 0.000% | -- | 0.000% |

| Sep-7 | Initial Jobless Claims | 245k | -- | 236k |

Strengths

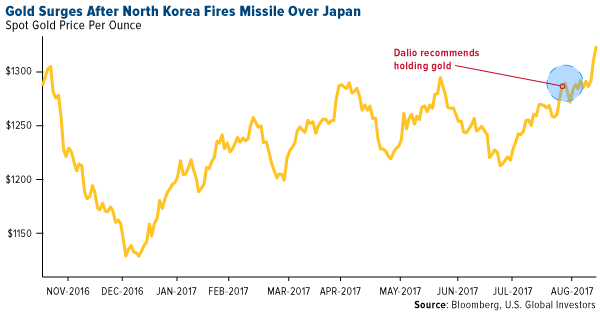

- The best performing precious metal for the week was palladium up 5.86 percent on speculation that automobile sales will jump to replace ruined vehicles in Texas, post Hurricane Harvey. That rally could be short lived as the auto inventories are high and all the water damaged vehicles along the Gulf Coast will simply have their catalytic converters recycled here in North America. Gold traders and analysts surveyed by Bloomberg are bullish for an 11th week straight, reports Bloomberg, as the yellow metal broke above the $1,300 an ounce. In addition, gold futures headed for the first close above $1,300 an ounce this year following no real news from Jackson Hole. As the dollar dropped, demand for the metal rose.

- North Korea fired a ballistic missile over Japan early this week, sending gold to its highest level this year, reports Bloomberg. Hedge fund billionaire Ray Dalio “may feel vindicated as gold trades well north of $1,300 an ounce” on the news, the article continues. Earlier this month, Dalio wrote about holding up to 10 percent of a portfolio in gold, warning of rising risks.

- U.S. Treasury Secretary Steven Mnuchin spoke about a weaker U.S. dollar helping to boost trade this week, allowing gold to hold its gains as the greenback dropped, reports Bloomberg. According to Naeem Aslam, chief market analyst at Think Markets U.K., gold is poised for further gains and could reach $1,370 this month.

Weaknesses

- Gold ended up lagging its peers in the precious metals space but still gained a respectable 2.60 percent for the week. Sibanye Gold canceled its dividend, reports Bloomberg, after debt ballooned while the South African producer swung to a loss. Following Sibanye’s $2.2 billion purchase of Stillwater Mining, it will focus on cutting borrowing costs. In Indonesia, mining company Freeport-McMoRan has agreed to give a majority stake of the Grasberg mine back to the Indonesian government; a 51-percent stake. The deal is meant to bring an end to years of rising public anger over American control of one of the mining industry’s crown jewels, the New York Times reports. However, major issues still linger, including what the Indonesian government might have to pay for that stake.

- Another political crisis is deepening in Guatemala, reports Bloomberg, as the courts blocked President Jimmy Morales’ attempt to expel a UN-backed, anti-corruption chief. Morales ordered the expulsion of Ivan Velasquez, just days after he said he was investigating the president for illegal campaign financing (Morales failed to properly report at least $825,000 in contributions in 2015), the article notes. Tahoe Resources has had its mining license suspended in Guatemala.

- The bailout of Russia’s second largest private bank, Otkritie FC, signals the failure of a strategy to have private lenders compete with state giants and dominate the industry, reports Bloomberg. “It’s no secret that many Russian private banks are ill-prepared to meet international standards of accounting, risk control and even simple business strategy,” said Anastasia Nesvetailova of City University in London. Otkrite’s unexpectedly low credit rating due to its loan portfolio and the failure of a rival triggered its downfall, “leading to a run on deposits that drained 527 billion rubles,” the article continues. In addition, the bank bought a diamond mine from its own shareholders for $1.45 billion. Switching over to the U.S., President Trump is set to undo another Obama-era initiative, reports Bloomberg, lifting his predecessor’s ban on giving local police departments military-grade equipment.

Opportunities

- According to BMO Technical Analyst Russ Visch, gold’s price rally could trigger a major, long-term buy signal for the metal if prices close above $1,375 an ounce, reports Bloomberg. If such a breakout happens, Visch believes this would shift the long-term trend back to bullish, opening an initial target of $1,705 an ounce. And when it comes to gold stocks, Mark Steele writes that BMO Capital Markets continues to “recommend an allocation toward gold shares, as painful as that has been so far this year, but impactful in a time like this where U.S. yields and yield curves continue to trend lower, and gold is an alternative to that experience.”

- ABN Amro Bank lifted its price estimate for gold after the metal broke through $1,300 an ounce. The bank now sees the yellow metal rallying to $1,400 in the third quarter of 2018, reports Bloomberg. Similarly, Citi said in an email this week that gold could have upside bias for the rest of this quarter, especially if the geopolitical climate deteriorates. As a side, North Korea has stated that the missile over Japan earlier this week was a “prelude” to containing Guam.

- According to The Daily Prophet, it’s time to start paying attention to gold. Whether it’s a weak dollar, tension from North Korea or hurdles from tax reform, “the list of worries continues, but the point is that there’s no shortage of risks facing investors,” Bloomberg writes. Even Thomas J. Lee of Fundstrat Global Advisors (who had the most bullish forecast for the S&P 500 for most of last year), is worried of stocks breaking down. Jim Rickards, best-selling author of Currency Wars, is not giving up on gold. Rickards noted that gold is one of the best performing assets of 2017 and in an interview added that the yellow metal could eventually touch $10,000 an ounce.

Threats

- Are central banks nationalizing the economy? That is a question raised by the Mises Institute, and related to an article recently ran in the Financial Times, stating that “leading central banks now own a fifth of their governments’ total debt.” The figures are staggering – for example, right now the Bank of Japan is a top 10 shareholder in 90 percent of the Nikkei. The report explains that “believing that this policy is harmless because ‘there is no inflation’ and unemployment is low is dangerous.” At the extreme, total debt has soared to 325 percent of GDP in Japan. “Government-issued liabilities monetized by the central banks are not high-quality assets, they are an IOU that is transferred to the next generations, and will be repaid in three ways: with massive inflation, with a series of financial crises, or with large unemployment,” the article continues.

- When it comes to India’s $45 billion gold industry, Anand Ghurgre, who owns a family jewelry shop in Mumbai, has seen the past and future colliding, reports Bloomberg. “We still operate the way my father did for 50 years,” Ghugre said, explaining that transactions were usually done in cash and not always recorded. This way of doing business is under threat due to Prime Minister Modi’s financial reforms including demonetization and a new goods and services tax. This, combined with a younger generation that shops online, could usher in a wave of takeovers and mergers in their stock market, perhaps drawing attention away from gold, the article continues.

- Mohamed El-Erian noted that based on historical models, gold’s responsiveness to recent geopolitical tensions, as well as its price, appear weaker than would have been expected, reports Bloomberg, and for understandable reasons. “The precious metal’s status as a haven has been eroded by the influence of unconventional monetary policy and the growth of markets for cryptocurrencies,” the article continues. El-Erian noted that gold’s traditional role could be re-established down the road as central banks are just beginning to unwind their unconventional policies and cryptocurrencies are certainly more vulnerable to unsettling air pockets. Government policies may emerge that target these cryptocurrencies with regard to tax evasion and anti-money laundering laws.

Energy and Natural Resources Market

Strengths

- Gasoline was the best-performing commodity this week, rising 4.6 percent. The commodity rallied as Hurricane Harvey led to temporary closures of major refineries and pipelines, which are expected to create supply shortages across Texas and parts of the East Coast over the coming days and weeks.

- The best-performing sector this week was the NYSE Arca Gold Miners Index. The index of large and mid-cap gold miners rose 5.8 percent as gold posted is best weekly advance of the year. North Korea tensions continued to occupy headlines and labor market indicators in the U.S. disappointed.

- BHP Billiton, the largest diversified miner by market capitalization, was the best-performing stock this week, finishing up 3.8 percent. The company profited from positive momentum in steel prices, which rallied to three-year highs in China following concerns over further supply disruptions.

Weaknesses

- Crude oil was the worst-performing commodity this week, dropping 1.2 percent. Prices came under pressure after Hurricane Harvey battered the Gulf Coast, leading to temporary shutdowns at the refining complexes. As a result, crude oil is expected to build in inventory for the next days and weeks as refiners slowly restart operations.

- The worst-performing sector this week was oil and gas. The sector was flat for the week as investors focused their attention elsewhere, either in the refining sector within the energy sector, or in the metals and mining space, which outperformed across the board.

- The worst-performing stock for the week was Freeport MacMoRan. The largest American base metals producer dropped 1.4 percent despite positive tailwinds in the base metals space. Investors reacted negatively to news that Freeport will divest 42 percent of PT Freeport Indonesia to bring local ownership to 51 percent in exchange for a license to operate the Grasberg copper and gold mine through 2041.

Opportunities

- China's Caixin Manufacturing PMI for the month of July posted its highest reading since February 2017. The reading was driven higher by a much stronger than expected rebound in exports, as orders reached the highest level since 2010. The strength in the Chinese PMI data has in previous occasions coincided with a rally in industrial and base metals.

- Steel prices continue their advance as Chinese steel futures contracts surge to three-year highs. In addition to the bullish PMI reading, futures contracts rallied by their daily limits on news that a newly built furnace at Benxi Steel caught fire. As a result, market specialists believe the current tight supply conditions could worsen, driving prices higher.

- Buyers withdrew record amounts of copper from inventory this week as commodity specialists suggest China may move ahead with a ban on scrap copper imports, thus increasing demand for other raw types of copper. On Wednesday, buyers withdrew more copper from the London Metals Exchange global warehouses than at any time since records began in 1996.

Threats

- The Port of Houston is reopening for ships today after officials noted there was no evidence of flooding on terminals or damage to equipment. In addition, Marathon Refining announced the restart of two of its gulf refineries as Hurricane Harvey made no serious damage to its facilities. The quick restart of activity across the hydrocarbon processing chain in the gulf may result in a quick correction for runaway gasoline prices as suppliers re-enter the market.

- The U.S. dollar may be gearing up for a correction after its worst performance in 14 years. So far in 2017, the dollar has endured its longest monthly losing streak in 14 years, with six straight months of declines. Now sitting at a statistical oversold condition, the U.S. dollar may rebound into quarter end, thus creating headwinds for commodity prices.

- July U.S. construction spending dropped 0.6 percent compared to an estimated 0.5 percent rise. In addition, June numbers were revised down to negative 1.4 percent. Although May numbers were revised upwards, the current weakening trend in construction and housing activity continues to provide a headwind for construction materials, as well as lumber and forest related sectors.

Strengths

- The Stock Exchange of Thailand (SET) Index rose 3.01 percent for the week.

- “China is creating the world’s largest power company,” writes Bloomberg. The nation’s top coal miner, Shenhua Group Corp., and one of its largest power generators, China Guodian Corp., will merge into a new entity with assets of 1.8 trillion yuan. “This confirms the direction of state-owned enterprise reform, with companies in the same industry merging to reduce redundant investment and improve efficiency,” the article continues.

- China’s Manufacturing PMI beat expectations, coming in at 51.7 for the August period, ahead of analysts’ anticipation of a 51.3 print and up from July’s reading of 51.4. The Caixin China Manufacturing PMI came in 51.6, also ahead of expectations (for 51.0) and last month’s 51.1 showing.

Weaknesses

- South Korea’s KOSPI Index declined 76 basis points for the week.

- On Monday, a landslide in southern China buried dozens of homes, killed one person and left 37 others missing, reports the Associated Press. Guizhou is one of the poorest provinces in China and the provincial government estimates losses at more than 5.1 million yuan.

- China’s official Non-Manufacturing PMI came in at 53.4, below last month’s 54.5 print.

Opportunities

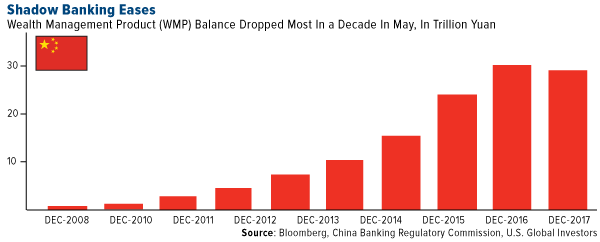

- According to the China Banking Regulatory Commission, shadow banking has eased this year in the Asian nation, reports Bloomberg. As seen in the chart below, the balance of wealth management products (WMPs) dropped by the most in a decade this May. “The government’s deleveraging efforts, renewed in earnest since the start of April, have sought to curb shadow financing and unravel the complex web of ties between Chinese lenders,” the article reads.

- The Chinese and Indian border standoff over a disputed piece of land in the Himalayas came to a sudden close at the end of August, reports the South China Morning Post. Both sides’ foreign ministries released statements acknowledging the drawdown, and later reports confirmed that India secured a withdrawal of Chinese troops, the article continues.

- Macau casino stocks rebounded this week amid better-than-expected August casino revenue numbers and as concerns on traffic and the typhoon’s effects may have been too extreme.

Threats

- Measured concerns over North Korea remain near the forefront of investors’ minds after recent missile tests and provocative rhetoric.

- Potential central banking policy missteps—or perceived missteps—remain a threat to markets.

- While Freeport McMoran appears to have reached an agreement with the Indonesian government to divest the majority stake of its Grasberg mine, details still remain to be worked out.

Emerging Europe

Strengths

- Poland was the best performing country this week, gaining 1.7 percent. Strong economic data is lifting the stock market higher despite increasing tension between Poland and Germany over Poland’s approach to the rule of law. Analysts recommend overlooking politics, as there is limited practical impact possible in the near future. Instead, they say to focus on strong gross domestic product and improving zloty appreciation.

- The Russian ruble was the best performing currency this week, gaining 1.9 percent against the U.S. dollar. Economists raised their forecast for Russia’s growth over the next three years after GDP in the second quarter beat estimates. In addition, analysts at UBS Group AG and Morgan Stanley recommend buying the currency of the world’s biggest energy exporter.

- Consumer staples was the best performing sector among eastern European markets this week.

Weaknesses

- Romania was the worst performing country this week, losing 3.1 percent. Banks noticed the biggest losses on the Bucharest stock exchange. The government has discussed imposing a tax on banks’ assets. The proposed tax could range from 0.2 to 0.3 percent, and if imposed at maximum level could cost banks 25 percent of 2017 net profits, according to Wood & Company.

- The Hungarian forint was the worst performing currency this week, losing 80 basis points against the U.S. dollar. The Economic Sentiment Index edged down to 4.2 in August, but still remains near a record high. Central bank of Hungary, as expected, left its main rate unchanged at 90 basis points.

- The utility sector was the worst performing sector among eastern European markets this week.

Opportunities

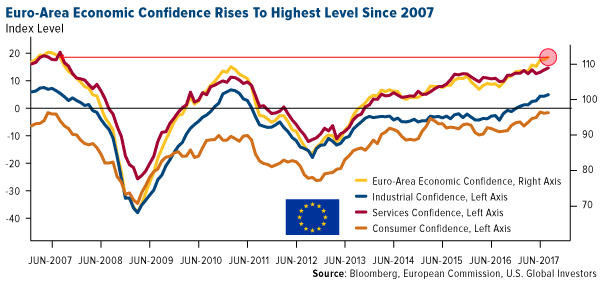

- Euro-area economic confidence rose to the highest level in a decade, led by rising confidence among industrial companies and the service sector. Among the largest EU economies, Italy, France and Spain recorded the sharpest rise in economic sentiment as Germany and the Netherlands eased slightly. Growth should accelerate through the rest of the year.

- Reuters reports that on Wednesday, French government outlined its planned tax cuts over President Macron’s five-year term, in line with the election promises to ease the country’s fiscal burden. The corporate cut would be to 31 percent in 2019, 28 percent in 2020, 26.5 percent in 2021, and 25 percent by the end if Macron’s term in 2022. The current corporate tax rate stands at 33 percent.

- According to Jonathan Lamb from Wood & Company, refining margins will be higher and oil prices will move lower for the next couple of weeks due to Hurricane Harvey that hit the Texas coast, a region where there are significant refining and petrochemical capacities. Hellenic Petroleum and Lotos, that are more heavily indebted, should be the ones to benefit most.

Threats

- This week’s third round of Brexit talks have seen little progress, with the EU maintaining that the UK has still not provided enough clarity on its Brexit approach. The UK has been pushing to move discussions on the future relationship and Brexit transition, and called for a more flexible approach from the EU. There are differences of opinion on the Brexit bill, which means talks are unlikely to move to the next stage until the end of the year.

- A stronger euro increases the chance of a delay in the quantitative easing decision or a more gradual phasing out of the European Central Bank’s asset purchase program. Euro appreciation is already causing monetary tightening and is equivalent to interest rate rises, according to Reuters. Deutsche Bank is projecting that every 10 percent rise in the trade-weighted euro lowers earnings per share by 5 percent. The euro is among the best performing currencies, gaining 11.5 percent year-to-date against the U.S. dollar.

- Russia’s central bank bailed out Otkritie, one of Russia’s biggest lenders, after clients withdrew more than a quarter of deposits in June and July. Russia is divided into banks that get rescued and those that get crushed. In the past four years, the central bank shot down more than 300 lenders. Otkritie fell into the too-big-to fail category, but having reported a Tier 1 capital ratio of over 12 percent as recently as December, is anything but reassured.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All