The German phrase Sturm und Drang (literally: storm and stress) describes situations that become especially dramatic. This seems an apt expression to describe both the immediate past and the near future for the United States economy.

Hurricane Harvey is the recent event that will bear importantly on the outlook. Damage assessments are still being assembled, and disaster relief funds have yet to be appropriated. For now, we have reduced our expectation of third quarter economic growth to reflect the disruption of activity in the Houston area, but added a bit to subsequent quarters in anticipation of rebuilding.

There is stormy weather on the horizon, too. As of this writing, Hurricane Irma is threatening the Florida coastline and could create a second series of challenges for residents and rescuers. And there are stressful times ahead over the next few weeks for the U.S. Congress, as legislators try to reach consensus on a new budget, tax reform and an extension to the Federal debt ceiling.

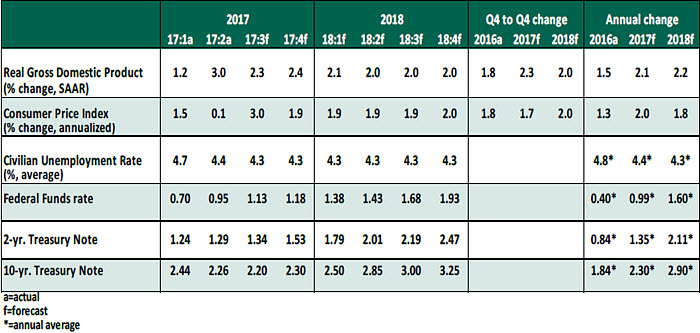

Key Economic Indicators

Influences on the Forecast

- Growth in the second quarter was revised up to an annual rate of 3%, the best reading in three years. Consumption was the main contributor to the upward adjustment. We expect spending to remain a strong contributor to gross domestic product, but with saving rates beginning to diminish, it may be difficult to sustain the recent trajectory of household outlays.

- The August employment report reflected a more modest pace of job creation. An estimated 156,000 new positions were created last month; strong readings for June and July were revised downward. August is generally an awkward month for employment readings, as back-to-school trends work their way irregularly through the final weeks of summer, so revisions are certainly possible. In general, the labor market remains healthy.

Wage growth is still stuck at around 2.5%, despite declines in all measures of labor capacity. The apparent suspension of the Phillips Curve has been attributed to several factors, some persistent and others transitory.

Hurricane Harvey will likely wreak some havoc on employment reports for the next couple of months. The next “clean” reading may not arrive until the beginning of December, depriving the Federal Reserve of critical information as it decides on whether to raise interest rates one more time this year. We still have an increase projected in December, supported by the Fed’s desire to control financial conditions. But the odds are getting longer.

- Manufacturing seems well-positioned for the balance of 2017. The Institute for Supply Management (ISM) index now stands at 58.8%, its best reading since 2011. (On the ISM scale, the 50% mark separates advance from contraction.) Plans for output and hiring both look solid, and inventories are at a low level. The exception to this bright outlook is the U.S. auto industry, which is facing declining sales; production may eventually have to be tapered.

- Inflation has drifted further from the 2% level targeted by the Fed. The overall and core rate of increase in the consumer price index stands at 1.7% over the past twelve months; the core rate is about 0.5% lower than it was earlier in the year. Similar trends are seen in the personal consumption expenditure (PCE) deflator. Some contributors to the reversal are temporary, but others appear to be more lasting. We still expect inflation to rise in the medium term, but progress may be slower than previously thought.

- Long-term interest rates continue to collapse. The ten-year U.S. Treasury yield may test the 2% level before long; some flight to quality in the wake of escalating tensions with North Korea may be a proximate cause. But flagging inflation and the prospect of an inactive Fed are also supporting bond prices. For now, bond investors do not appear overly alarmed by the fiscal battles to come, or by the prospect of a debt ceiling impasse.

As I write this, I am heading back out on the road for the first time in six weeks. Business travel can also involve storms and stress, but I am really looking forward to the upcoming conversations.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2017 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.