A quote often attributed to St. Augustine, the early Christian theologian, is: “The world is a book, and those who do not travel read only a page.” I feel blessed to be able to travel as much as I do—not because I’m a big fan of 10-hour flights or living out of a hotel room. I feel blessed because travel allows me to meet and speak at length with some truly fascinating and successful people, from CEOs of firms both large and small, to deal lawyers, to audit partners.

Hearing varying opinions on global issues and politics has helped expand the scope and depth of my “book,” or understanding of the world. In turn, I enjoy sharing some of these thoughts with you, as regular readers of Investor Alert and Frank Talk know well.

Opinions come a dime a dozen, of course, and in today’s hyper-partisan world, it’s impossible to expect everyone to agree on all things all of the time.

Case in point: I recently polled readers on their approval of the way Donald Trump has handled his job as president so far. This isn’t a scientific poll by any stretch of the imagination, but for whatever it’s worth, a combined 56 percent of participants said they approve of the president. Amazingly, that’s roughly the percentage of Electoral College votes given to Trump in November. (The exact figure is 56.87 percent.)

click to enlarge

Some could easily take from this poll that Frank Talk readers are huge Trump supporters—and many of them are—but that would be overlooking the fact that nearly 40 percent said they disapprove of the way he’s handled his job.

I share this because it serves as a relatively accurate cross section of the types of opinions and perspectives I come across during my travels. Some of those opinions end up informing my own thinking, some don’t—but all of them are added to my “book.”

Now with North Korea launching even more rockets over Japan, the market makes new highs. This is what I was asked most often this week on CNBC Asia, Bloomberg Radio and Fox Business. As I said then, I’m bullish because the purchasing manager’s index (PMI) is up and oil prices are down, thanks to the ingenuity of Texas fracking, which has created a global peace tax break. The weaker dollar is favorable for exports and gold.

Bitcoin on Sale After the China-Dimon One-Two Punch

Someone whose opinion I greatly admire, even if I don’t always agree with it, is Jamie Dimon’s. The highly-respected JPMorgan Chase CEO was asked this week at a global financial services conference in New York to share his thoughts on bitcoin—which can be as polarizing as President Trump. Some people love the cryptocurrency, some people hate it.

Dimon, who’s decidedly in the latter camp, didn’t mince his words.

Although he likes blockchain technology, which bitcoin is built on top of, he began by saying he would fire any JPMorgan trader who was caught trading bitcoin, which he went on to call “stupid,” “dangerous” and “a fraud.”

“You can’t have a business where people can invent a currency out of thin air,” he said.

With all due respect to Dimon, some might point out that “inventing a currency out of thin air” is how we got Federal Reserve Notes and other forms of paper money in the first place. Even he admits this:

“The first thing a nation does when it forms itself—literally the first—is forming currency.”

Bitcoin—and any of the 800 other cryptocurrencies—takes this idea to the next level, the main difference being that no third party or monetary authority controls its issuances or transactions. It’s all peer-to-peer.

Governments tend to resist anything that disrupts the status quo, which is why we saw China restrict new initial coin offerings (ICOs) last week. I suspect we’ll see a few more countries attempt to regulate ICOs in other ways, and as long as these regulations are fair and reasonable, I welcome them.

The bitcoin price was knocked down following the one-two punch of China and Dimon, falling 39 percent from its peak of $4,919 on September 1. Yesterday it lost more than $611 a unit, one of its worst days ever, but today the cryptocurrency rallied strongly again.

With its ability to validate all transactions in an immutable electronic ledger, the blockchain has the potential to be as disruptive as Amazon was in the late 1990s. When the company went public in 1997, there were serious doubts whether people would willingly give up their credit card information just to buy a book. Since then, Amazon stock is up 8,000 percent, and founder Jeff Bezos briefly overtook Bill Gates in July to become the world’s wealthiest person.

If you’re curious to learn more about how blockchains work, I recommend that you watch this engaging two-minute video.

Gold Price Correlated to Money Supply Growth

In some ways, cryptocurrency more closely resembles gold. Just as there’s only so much gold that can be mined in the world, the number of bitcoins that can ever be mined is set at 21 billion. But the exact amount is irrelevant. It could have been set at 21 trillion—the point is that supply is limited and finite.

The same cannot be said of the U.S. dollar, or any fiat currency, which today is printed “out of thin air” with abandon. This has led to hyperinflation in some instances and destroyed the value of several countries’ currency, including the Zimbabwean dollar and, more recently, the Venezuelan bolivar.

I’m not suggesting we’ll see the same thing happen here in the U.S. Nevertheless, rampant money-printing has certainly contributed to many people’s dwindling trust in traditional monetary systems. A 2016 Gallup poll found that Americans’ confidence in banks is stuck below 30 percent, where it’s been since the beginning of the financial crisis nearly 10 years ago.

When more money is printed, gold has traditionally been a beneficiary, for two key reasons: 1) If the money-printing is accompanied by economic growth, greater access to capital might boost demand for luxury items, including gold (the Love Trade); and 2) If the money-printing isn’t accompanied by economic growth, inflationary pressures might prompt investors to increase their exposure to real assets, such as gold (the Fear Trade).

These were among the findings in a 2010 World Gold Council (WGC) study. Even after seven years, the findings still apply. As you can see below, the price of gold expanded over the years as more and more money was printed.

click to enlarge

If we want to get really technical, the WGC estimates that for every 1 percent increase in U.S. money supply, the price of gold tends to rise 0.9 percent—nearly as much—within six months.

According to the most recent Federal Reserve report (September 7), more than $13.67 trillion in M2, or broad money, are now in circulation. That’s up about 1 percent since the end of June, when M2 stood at $13.54 trillion.

So will the gold price climb 1 percent in response? That would amount to only $13 an ounce, but remember, there are other factors driving gold, including negative real interest rates and geopolitical uncertainty.

One final note: A former UBS metals trader was arrested and charged this week with fraud and conspiracy over his alleged role in placing “spoof” orders for precious metals futures contracts. Andre Flotron, a Swiss citizen, was arrested while visiting his girlfriend in New Jersey. Flotron began working for UBS in 1999 but was put on leave in 2014.

See Zero Hedge for more on conspiracies and convictions in court over price manipulation of precious metals. Many cryptocurrency advocates allege this is why Jamie Dimon is so aggressive in knocking down bitcoin. The enthusiasm for bitcoin has accelerated this year with South Korean and Japanese banks accepting them as a form of money.

The Economy and Bond Market

Strengths

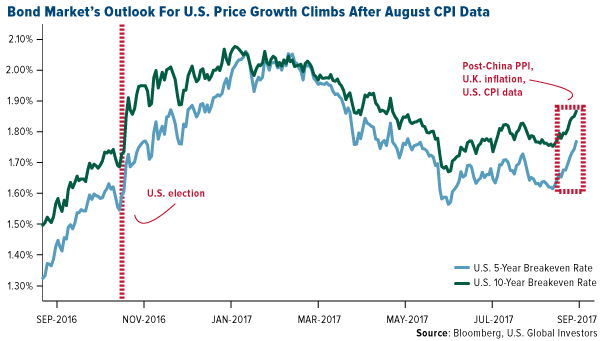

- The outlook for faster U.S. inflation is at its highest since the spring. Breakeven rates, which measure the yield spread between treasuries and similar Treasury inflation protected securities, on five and 10 year notes surged after the August CPI report showed an acceleration. The index rose 0.2 percent month-over-month and matched estimates after five months of missing the mark. Core prices were up 1.7 percent year-over-year, beating estimates.

click to enlarge

- The U.S. Empire Manufacturing Index for the month of September showed a slight dip to 24.4 from 25.2 last month but that was much better than expectations for 18.0.

- The NFIB Small Business Optimism Index for August increased to 105.3, above expectations of 104.8.

Weaknesses

- U.S. retail sales fell in August, likely impacted by Hurricane Harvey fallout on motor vehicle purchases. Retail sales dropped 0.2 percent last month, the biggest decline in six months. Data for July was revised to show sales increasing 0.3 percent instead of the previously reported 0.6 percent increase.

- U.S. industrial output fell in August for the first time since January as Hurricane Harvey battered oil, gas and chemical plants along the Gulf Coast and a cool summer sapped utility demand in the east, the Federal Reserve said on Friday. Overall industrial production fell 0.9 percent over the month after a July increase revised upward to 0.4 percent.

- Consumer confidence declined in September, after hitting a seven-month high in August. The consumer sentiment index, a survey of consumers by The University of Michigan, recorded 95.3 in its preliminary report for the month. Hurricanes Harvey and Irma have greatly impacted expected economic conditions in September.

Opportunities

- Wednesday's FOMC meeting will take center stage in the week ahead. The Federal Reserve is widely expected to keep rates on hold, but announce plans to unwind its balance sheet. Investors will also be looking for any changes to the Fed's economic and interest rate forecasts.

- In the euro area, September's flash PMIs next Friday will give a timely update on the economy. Recent PMIs have been pointing to firm GDP growth.

- The September preliminary U.S. Manufacturing PMI out on Friday is expected to show continued robustness.

Threats

- Moody’s slashed Hartford, Connecticut’s general obligation rating two notches to Caa1 from B2 and put it on review for additional downgrades. According to the firm, the city is in a “precarious” liquidity position with debt service payments every month “compounding the possibility of default at any time.”

- An increasing number of U.S. cities are saying it’s becoming a struggle to make ends meet. Nearly a third of those surveyed by the National League of Cities said they are less able to cover their economic needs this year than they were in 2016, the most in five years. Aging infrastructure and the cost of employee wages and benefits are the biggest drags on municipal finances, officials said.

- August’s Leading Index out on Thursday is expected to contract from the previous month’s, pointing to a slowdown.

Gold Market

This week spot gold closed at $1,321.28, down $25.17 per ounce, or 1.87 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 4.44 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index came in higher by 0.99 percent. The U.S. Trade-Weighted Dollar finished the week slightly higher by 0.45 percent.

| Date |

Event |

Survey |

Actual |

Prior |

| Sep-13 |

GE CPI YoY |

1.80% |

1.80% |

1.80% |

| Sep-13 |

US PPI Final Demand YoY |

2.50% |

2.40% |

1.90% |

| Sep-13 |

CH Retail Sales YoY |

10.50% |

10.10% |

10.40% |

| Sep-14 |

US Initial Jobless Claims |

300k |

284k |

298k |

| Sep-14 |

US CPI YoY |

1.80% |

1.90% |

1.70% |

| Sep-18 |

EC CPI Core YoY |

1.20% |

-- |

1.20% |

|

Sep-19

|

GE ZEW Survey Current Situation |

86.3 |

-- |

86.7 |

| Sep-19 |

GE ZEW Survey Expectations |

12 |

-- |

10 |

| Sep-19 |

US Housing Starts |

1175k |

-- |

1155k |

| Sep-20 |

US FOMC Rate Decision (Upper Bound) |

1.25% |

-- |

1.25% |

| Sep-21 |

US Initial Jobless Claims |

300k |

-- |

284k |

Strengths

- The best performing precious metal for the week was gold, down slightly 1.86 percent. Jeff Christian, managing director of research consultancy CPM Group, thinks that the price of gold is headed much higher in the next three years, reports TheStreet.com. “We thought gold would find a bottom in 2015 and that by 2020 we could see gold set a new record gold price in nominal terms, above $1,700 an ounce,” Christian said.

- According to Deutsche Bank strategist George Saravelos, it doesn’t look like the U.S. dollar will see a reversal of fortunes anytime soon, reports Business Insider. Since January, the greenback has lost around 11 percent versus a basket of peers. In a note to clients, Saravelos says there are a couple of key changes showing that the dollar is in trouble. The first is that the market still isn’t pricing additional rate hikes and the second is that the drivers of the foreign exchange market are seeing a fundamental shift. If the dollar stays low, gold could continue to shine.

- This week, Victoria Gold Corp. announced analytical results from its ongoing 2017 Dublin Gulch campaign, specifically the Olive zone. Exploration drilling at Olive included 3.3 meters of 1.5 g/t gold, highlighting that additional, near-Olive gold mineralization exists at Dublin Gulch and validating the Potato Hills Trend mineralization model, according to a press release.

Weaknesses

- Although all of the precious metals were down this week, the worst performer was platinum, dropping 3.83 percent. Platinum investors were spooked by Impala Platinum’s annual results earlier in the week, reports Business Day, as production came in below targets. In addition, Bloomberg reports that the company’s Zimbabwe unit has authorized the handover of 24,000 hectares of land to the Zimbabwe government.

- Gold weakened on Thursday following the announcement of better-than-expected U.S. inflation data for August, reports Kitco News. The U.S. consumer price index (CPI) rose 0.4 percent in August, led by increased gasoline and shelter costs. Gold prices plunged in an immediate reaction to the data released by the U.S. Labor Department.

- Canadian mining company Eldorado Gold on Monday threatened to suspend a major investment in Greece in 10 days, reports the Associated Press, accusing the government of delaying permits and licenses. Eldorado is one of Greece’s largest foreign investors, but its mines in the northern part of the country have faced “vehement opposition from parts of local communities on environmental grounds, with protests often turning violent,” the article reads. The decision will take effect September 21 unless talks with the government end permit delays.

Opportunities

|

|

- Alamos Gold announced its friendly acquisition of Richmont Mines, whereby Alamos will acquire all of the issued and outstanding shares of Richmont. The arrangement further enhances Alamos’ position as a leading intermediate gold producer, reports Bloomberg. The acquisition provides Alamos with a high-quality, free cash flowing mine in a world class jurisdiction. In other company news, Centerra Gold has reached a comprehensive settlement with the government of Kyrgyz Republic, where the company agreed to make a one-time lump sum payment totaling $57 million. The company will continue to work closely with the government to expeditiously satisfy the strategic agreement. U.S. Global’s gold portfolio manager Ralph Aldis is doing his own boots-on-the-ground review of another company this week, Klondex Mines. The photo below shows a large gold bearing quartz vein in the company’s Hollister Mine, specifically from the Gloria Vein.

- After China outlawed new initial coin offerings last week, the Asian nation said it will ban the trading of bitcoin and other virtual currencies on domestic exchanges, reports Bloomberg. While dealing another large blow to the cryptocurrency market, this could mean a rush to gold as investors move back to the yellow metal as a store of value. In addition, the People’s Bank of China has done trial runs of its own prototype cryptocurrency, the article continues, taking it a step closer to being the first major central bank to issue digital money.

- Amid a recent rally in the price of gold, many metal producers are seeking acquisitions. Shandong Gold Group, one of the biggest Chinese miners of the metal, is considering bids for EMR Capital’s Indonesian gold and silver mine, reports Bloomberg. China Gold International is also exploring a possible bid. EMR Capital is a resources-focused private equity firm, and its sale of the Martabe mine could fetch as much as $1.5 billion, the article continues.

Threats

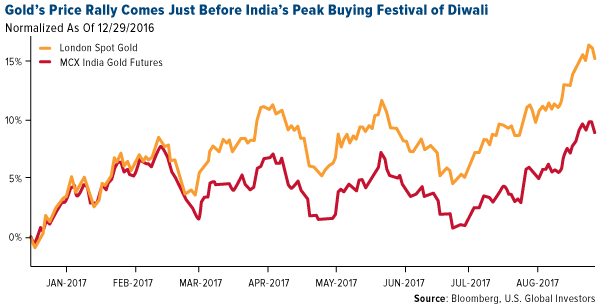

- Rising gold prices, along with government measures to enforce India’s jewelry industry, are stifling demand in the world’s second-largest bullion market, reports Bloomberg. Typically buying explodes at the start of the traditional festival season of Diwali, but as bullion climbs nearly 10 percent on the Indian market this year, paired with global tensions and reduced chances of a further hike in U.S. rates, the demand outlook has soured, the article continues.

click to enlarge

- According to Bloomberg, the U.S. is poised to experience its first annual decline in solar-panel installations, as a drop in rooftop demand slows growth in the world’s second-biggest market. Possibly adding to the decline is a trade complaint that could prompt President Trump to impose tariffs on imported panels. Imposing tariffs would mean “installations would significantly drop,” the article continues.

- An ex-trader with UBS Group has been arrested and charged with fraud and conspiracy over his suspected role in manipulating the price of precious metals, reports Bloomberg. Andre Flotron, a Swiss citizen, is the second person publicly charged in the U.S. investigation into the fixing of gold, silver, platinum and palladium prices, and could face up to 25 years in prison. “Flotron’s arrest extends the Justice Department’s examination of whether bank traders conspired to rig interest-rate benchmarks and manipulate currency exchanges from 2008 to 2013,” the article reads.

Emerging Europe

Strengths

- The Czech Republic was the best performing country this week, gaining 2.9 percent. Czech National Bank’s Chief Economist Tomas Holub said that rising inflation may prompt the central bank to hike rates further this year. The bank’s main rate was raised by 20 basis points from the record low of 0.5 basis points at the last meeting in August. The Czech Republic is the first European country to raise rates.

- The Russian ruble was the best relative performing currency this week, losing 40 basis points against the U.S. dollar. Historically, the correlation between the ruble and Brent crude oil is high. In the past five days the price of Brent increased by 3 percent.

- Energy was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 3.3 percent. The third review may take longer to complete. Until now, the government has targeted December for the completion of the review. The official’s comments indicate that more time will be needed to complete a total of 113 prior actions, 95 of which have been completed by Christmas, wrote Alex Boulougouris from Wood & Company.

- The Hungarian forint was the worst performing currency this week, losing 1.6 percent against the U.S. dollar. European currencies fell while the dollar gained on increased expectations of rate hikes in U.S. later this year.

- Consumer staples was the worst performing sector among eastern European markets this week.

Opportunities

- Germany will go to the polls on September 24 in a federal election. Angela Merkel’s Christian Democratic Union Party (CDU) is leading in the polls. Record-high employment, rising real wages and low borrowing costs will continue to support consumer spending and economic growth.

- Turkey’s economy had a strong second quarter and growth is set to be even quicker in the third quarter, according to Capital Economics. Second quarter GDP was reported at 5.1 percent, exports and fixed investment were the main drivers of the economy.

- The Russian central bank resumed monetary easing, cutting its main rate by 50 basis points from 9.0 percent to 8.5 percent, after inflation fell to a record low. Central bank’s governor, Elvira Nabiullina, has said the key rate can reach its nominal equilibrium level of 6.5 to 7 percent once inflation is stable at 4 percent for one to two years. Many analysts expect more cuts to follow.

Threats

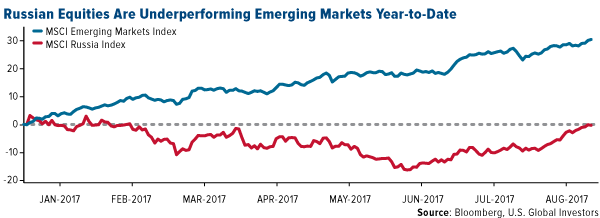

- Russian equities are underperforming emerging markets after a strong 2016. In 2016, the MSCI emerging markets index rose 11.5 percent while the MSCI Russia index gained 56 percent. This year, the MSCI emerging markets index is up 30 percent, while Russia is slightly down. This underperformance should continue, says Win Thin from the BBH Global Currency Strategy Team, as the group’s emerging markets equity model has Russia in an underweight position. The correlation between Russian stocks and oil prices has fallen near 0.10, well below 0.70 seen in 2015 and 2016.

click to enlarge

- Putin is conducting a military exercise that is alarming officials across Europe. Russia sent thousands of troops into Belarus to defend against an imaginary invasion from the west. Belarus says only 12,700 troops are involved, a level just below the 13,000 that would trigger compulsory international monitoring. Germany and Poland put the real total at more than 100,000. Putin may be using this military move as an excuse to deploy more weaponry and personnel along Russia’s borders and keep them there, according to a presidential spokeswoman in Vilnius.

- Reuters cited Fitch analyst Ed Parker, who said the stability of Italy's government remains a source of risk for the euro zone. He added its biggest concern in Italy, is that we might not get a stable government. Furthermore, he highlighted that we can't completely discount the bigger downside risk of a euro-sceptic party being part of a coalition.

© US Global

www.usfunds.com

© U.S. Global Investors

Read more commentaries by U.S. Global Investors