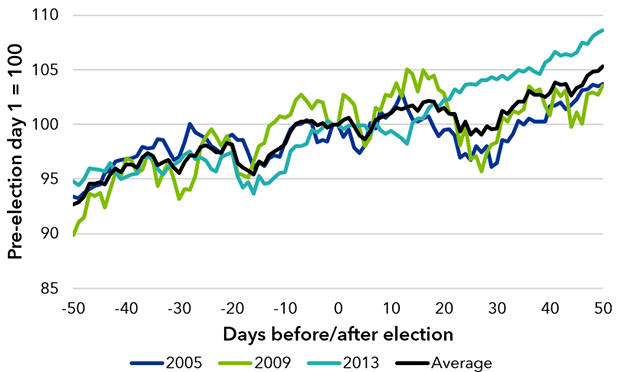

1 Source: The Emnid Institute, weekly Sunday opinion poll, as at 27 August 2017

Key takeaways

- Germany will hold national elections for Chancellor on September 24 with Angela Merkel seeking a fourth term. The election occurs at a time when Europe is enjoying an above-trend pace of economic growth and a broadening recovery, which has helped make Europe one of the favored investor regions this year (even if the euro’s strength is prompting inflows to slow). With many European elections in recent years having surprise results that moved markets, investors are wise to monitor developments leading up to the vote.

- We believe a Merkel win would likely be positive for markets, although we do not expect a strong reaction given that current polls show Merkel with a healthy lead. Instead, the makeup of the government could have greater ramifications.

- A Merkel win would likely lead to either the reinstatement of the current grand coalition between the conservative Christian Democratic Union-Christian Social Union (CDU-CSU) alliance and the Social Democrats (SPD), a new three-way coalition with the liberal FDP and the Greens, or even to a CDU/FDP coalition.

- Any of these scenarios is potentially favorable for German equities, with the inclusion of the FDP in any governing coalition adding even more impetus.

- We see a more muted increase in German bond yields under Merkel than an SPD-led government.

What might the German election mean for markets?

Although the SPD has typically managed to gain or recover ground in the immediate run-up to general elections, the 15% lead held by the CDU at the time of writing1looks hard to beat.

A Merkel win would likely lead to either the reinstatement of the current grand coalition between the conservative Christian Democratic Union-Christian Social Union (CDU-CSU) alliance and the Social Democrats (SPD), a new three-way coalition with the liberal FDP and the Greens, or even to a CDU/FDP coalition.

We believe that any of these scenarios would be favorable for German equities, with the inclusion of the FDP in any governing coalition adding even more impetus. We see a more muted increase in German bond yields under Merkel than an SPD-led government.

Should the result fall in line with expectations, we will be closely watching not only Merkel's choice of coalition partner (or partners) but which ministries will be held by which party. Both coalition make-up and ministerial responsibility could have a significant impact on economic policy over the term of the next government – and therefore what we might expect from markets.

A Merkel victory could signal greater European integration, particularly following President Emmanuel Macron’s election as president of France earlier this year. However, it is also important to place the election in the context of a broader European economic recovery. Europe is enjoying an above-trend pace of economic growth and has been one of the favored regions among investors in 2017. Recent strength of the euro has slowed inflows, however. Ultimately, the pace of economic growth may have a greater impact on German equities than the election outcome.