The Biggest Global Tax Break Ever Bubbles Up from Texas Oil Industry

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Last Friday I had the privilege of appearing on “Countdown to the Closing Bell,” Liz Claman’s program on Fox Business. When asked if I was nervous that stocks are heading too high, I said that I’m very bullish. All around the world, exports are up, GDPs are up and the global purchasing manager’s index (PMI) is up.

Oil prices continue to remain low, however, thanks in large part to the ingenuity of Texas fracking companies. As I told Liz, this has served as a multibillion-dollar “peace dividend” that has mostly helped net importing markets, including “Chindia”—China and India combined, where 40 percent of the world’s population lives—Japan and the European Union.

I can’t emphasize enough how impressive it is that Texas shale oil producers continue to ramp up output even with crude remaining in the $50 per barrel range.

This underscores their efficiency and innovation in drawing on oil reserves that were largely out-of-reach as recently as 10 or 12 years ago. What’s more, common law property rights here in the U.S. benefit mining companies in ways that simply can’t be found in Latin America and other parts of the world that operate under civil law.

According to the Energy Information Administration’s (EIA) most recent report on drilling productivity, total U.S. shale oil output is expected to climb above 6 million barrels a day for the first time in September. The biggest contributors are Texas shale oilfields, which will exceed 4 million barrels a day. West Texas’ Permian Basin alone represents nearly 400 percent of these gains, according to research firm Macrostrategy Partnership.

The typical Permian well remains very profitable even with $50-a-barrel oil, according to Bloomberg New Energy Finance. The research group estimates that oil would need to drop below $45 a barrel for some Permian wells to become unprofitable.

Christi Craddick, the Texas Railroad Commissioner, praised the Texas fracking industry in her address at the annual Panhandle Producers and Royalty Owners Association (PPROA) meeting this week. She noted how essential shale oil producers are to the Texas economy, adding that despite the downturn in oil prices, “the Texas oil and gas industry has shown extraordinary resilience.”

“When times were tough, the industry did what it does best—innovate,” she said. “Because of your ingenuity, we’re seeing industry growth today despite the price of oil.”

Again, it’s this ingenuity that’s kept oil prices relatively low, which in turn has helped strengthen GDPs in oil-importing emerging markets and squeeze the revenue of exporters such as Russia, Qatar, Saudi Arabia and others.

Texas-based oil and gas exploration company Anadarko Petroleum was one of the top performing natural resource stocks this week, gaining more than 12 percent. The surge came on the heels of the company’s announcement that it approved a $2.5 billion stock buyback program.

Coming Together as a Community

A month after the Texas Gulf Coast was devastated by the unprecedented wind and rains of Hurricane Harvey, the cleanup and rebuilding continues. As I shared with you in an earlier post, the Texas economy is one of the strongest in the world, and its residents are committing to rebuilding Houston and other affected areas better than ever before. As a proud Texan by way of Canada, I can say that it’s in our culture to come to one another’s aid in times of need and help rebuild.

Synchronized Global Growth Is Finally Here: OECD

I believe that my bullishness was validated this week with the release of the Organization for Economic Cooperation and Development’s (OECD) quarterly economic outlook. According to the Paris-based group, synchronized global growth is finally within sight, with no major economy in contraction mode for the first time since 2008. World GDP is expected to advance 3.5 percent in 2017—its best year since 2011—and 3.7 percent in 2018.

This news comes only a couple of weeks following the release of the August global manufacturing PMI, which shows that manufacturing activity around the world accelerated to its highest level in over six years. Not only is the index currently above its three-month moving average, but it’s also now held above the key 50 threshold for a year and a half, indicating strong, sustained industry expansion.

As I’ve shown before, the global PMI has been a good indicator of exports and commodity prices three to six months out, so I see this as very positive.

World markets seem to agree. Not only are domestic averages closing at record highs on a near-daily basis, but global stocks continue to head higher as well. The MSCI World Index, which tracks equity performance across 23 developed countries, is up 14 percent so far this year as of September 20. And just so we’re clear that emerging countries aren’t being left out, the MSCI Emerging Markets Index has gained close to 30 percent over the same time period.

One of the most attractive regions to invest in right now is Asia, specifically the China region, which has outperformed both the American and European markets year-to-date. The Hang Seng Index has advanced more than 27 percent, driven mostly by financials and tech stocks such as Tencent and AAC Technologies.

In addition, Asian stocks look very cheap, trading at only 13.97 times earnings. The S&P 500 Index, by comparison, is currently trading at 21.44 times earnings.

A Rebalance of Monetary and Fiscal Policies Needed for Sustainable Growth

But back to the OECD report. The group points out that the good times could easily come to an end if world governments don’t make efforts to balance monetary and fiscal policies, something I’ve been urging for years now.

Central banks are eyeing the stimulus exit door, with the Federal Reserve planning to begin unwinding its $4.5 trillion balance sheet as early as next month, the European Central Bank (ECB) ready to reduce its monthly bond-purchasing program sometime in early 2018 and the Bank of England (BOE) expected to raise interest rates in November for the first time since 2007.

As such, governments need to strengthen business investment, global trade and wage growth. The OECD adds that “more ambitious structural reforms” in emerging economies “are needed to ensure that the global economy moves to a stronger and more sustainable growth path.”

Only then can this new period of synchronized global growth be sustained in the long term.

Invasion of the Quants in the Gold Space

For the next few days I’ll be in Colorado Springs, Colorado, attending the Denver Gold Group’s 28th annual Gold Forum. My keynote presentation, scheduled for Monday, will be about how our firm uses quantamentals in our gold investing strategy. Quantamentals, as I’ve explained before, is a blended approach that combines old fashioned, bottom-up stock picking with big data and machine learning. If you happen to be in the Colorado Springs area, stop by and say hi!

September 21, 2017Markets Move Higher Despite Geopolitical Noise |

September 21, 2017U.S. Global Investors Announces... |

September 13, 2017Oil, Gold and Economic Growth |

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.36 percent. The S&P 500 Stock Index gained 0.08 percent, while the Nasdaq Composite fell 0.33 percent. The Russell 2000 small capitalization index gained 1.33 percent this week.

- The Hang Seng Composite gained 0.94 percent this week; while Taiwan was down 1.24 percent and the KOSPI rose 0.11 percent.

- The 10-year Treasury bond yield rose 5 basis points to 2.25 percent.

Domestic Equity Market

Strengths

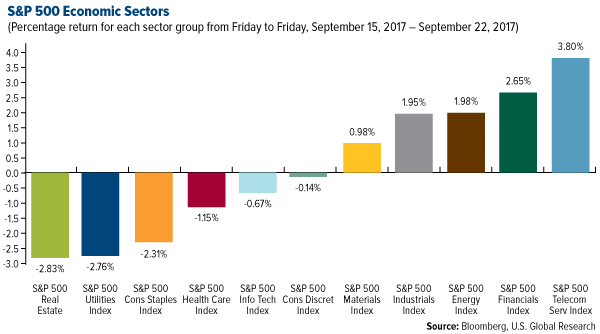

- Telecommunications was the best performing sector of the week, increasing by 3.80 percent versus an overall increase of 0.10 percent for the S&P 500.

- Equifax was the best performing stock for the week, increasing 12.97 percent.

- We're officially in the second-largest bull market since World War II. Stocks have climbed roughly 270 percent from their March 2009 low, eclipsing the bull run from June 1949 to August 1956, according to data from LPL Financial.

Weaknesses

- Real estate was the worst performing sector for the week, falling 2.83 percent versus an overall increase of 0.10 percent for the S&P 500.

- Foot Locker was the worst performing stock for the week, falling 9.02 percent.

- Toys R Us filed for bankruptcy. The toy retailer filed for Chapter 11 bankruptcy on Monday as a result of online competition and a huge debt load.

Opportunities

- Apple's new A11 chip, which powers the iPhone X, iPhone 8 and iPhone 8 Plus, is more powerful than 2017's MacBook Pro models. The phones are all considerably faster than any competition out there at the moment, an advantage which could allow Apple to increase market share.

- U.S. defense contractor Northrop Grumman agreed to buy the missile and rocket maker Orbital ATK Inc. for about $7.8 billion in cash, with plans to establish a new business segment. Orbital has billion-dollar contracts with NASA and the U.S. Army.

- Tesla and AMD are reportedly teaming up. The companies are working together to make chips for self-driving cars, CNBC said, citing a source familiar with the matter.

Threats

- Google is trying to avoid another massive European Union fine by offering to show rivals' shopping sites via an auction in its search results. However, EU regulators dismissed Google's proposal as inadequate, according to Reuters.

- Bed Bath & Beyond plummeted after missing big on earnings. Shares of the company fell more than 15 percent after announcing earnings of $0.67 a share on revenue of $2.94 billion, both well below estimates, as restructuring charges, Hurricane Harvey and a new accounting standard weighed, according to Investing.com.

- FedEx missed on its earnings report and lowered its outlook. The company missed on both the top and bottom lines and said it saw fiscal 2018 adjusted earnings in a range of $11.05 to $11.85, down from its previous estimate of $12.45 to $13.25.

The Economy and Bond Market

Strengths

- The Leading Index for August came in at 0.4 percent, ahead of the expected 0.3 percent. This reading is a positive sign for the economy.

- Retail investors in the U.S. are at record levels of optimism. The preliminary University of Michigan survey of consumer sentiment for September showed that the mean expected probability that stocks would climb over the next year hit a record 65 percent.

- September’s preliminary Markit U.S. Manufacturing PMI data came in at 53, above the previous month’s reading of 52.8.

Weaknesses

- China’s credit rating was downgraded at Standard & Poor’s. The credit-rating agency lowered China's rating one notch to A+, citing the country’s rising debt load.

- U.S. existing home sales for August came in softer than expected. Sales of existing homes totaled 5.35 million, below expectations for 5.45 million.

- September’s Markit U.S. Services PMI came in at 55.1, below the expected reading of 55.8.

Opportunities

- The likelihood of a Federal Reserve rate increase this year moved up as traders boosted the odds to about 62 percent, based on Fed funds futures, on Wednesday after Janet Yellen stuck to the Fed’s forecast for another hike this year. The probability was around 50 percent prior to the meeting and as low as 22 percent on September 8.

- The Federal Reserve raised its outlook for the U.S. economy. It now expects real GDP to grow from 2.2 percent to 2.5 percent in 2017, up from June's projection of 2.1 percent to 2.2 percent.

- Next Friday's PCE data will be the most anticipated U.S. economic release of the week. August's income and spending may be temporarily depressed by the hurricane. But more importantly, following the 0.2 percent month-over-month increase in August's core consumer price index (CPI) data, investors will be watching for a similar rise in the core PCE deflator. This should keep a December Fed rate hike in play.

Threats

- The Federal Reserve announced Wednesday it would embark next month on its biggest post-recession policy shift since it first raised interest rates at the end of 2015. The central bank confirmed that it would start trimming the $4.5 trillion balance sheet it built up after the Great Recession. This balance sheet unwinding carries risks for the bond market.

- Durable goods orders have been in decline for the past two months. Next Wednesday’s release will provide an update on this trend.

- S&P Global Ratings downgraded Pennsylvania’s general obligation rating to A+ from AA-. According to S&P, the downgrade reflects the commonwealth’s chronic structural imbalance dating back nearly a decade, and a history of late budget adoption.

This week spot gold closed at $1,296.95, down $23.21 per ounce, or 1.76 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 3.12 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index came in slightly lower by 0.20 percent. The U.S. Trade-Weighted Dollar finished the week slightly higher by 0.37 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep-18 | Eurozone CPI YoY | 1.2% | 1.2% | 1.2% |

| Sep-19 | Germany ZEW Survey Current Situation | 86.2 | 87.9 | 86.7 |

| Sep-19 | Germany ZEW Survey Expectations | 12.0 | 17.0 | 10.0 |

| Sep-19 | Housing Starts | 1147k | 1180k | 1190k |

| Sep-20 | FOMC Rate Decision (Upper Bound) | 1.25% | 1.25% | 1.25% |

| Sep-21 | Initail Jobless Claims | 302k | 259k | 282k |

|

Sep-26 |

Hong Kong Exports YoY | 9.5% | -- | 7.3% |

| Sep-26 | New Home Sales | 590k | -- | 571k |

| Sep-26 | Conf. Board Consumer Confidence | 120.0 | -- | 122.9 |

| Sep-27 | Durable Goods Orders | 1.0% | -- | -6.8% |

| Sep-28 | Germany CPI YoY | 1.8% | -- | 1.8% |

| Sep-28 | GDP Annualized QoQ | 3.1% | -- | 3.0% |

| Sep-28 | Initial Jobless Claims | 265k | -- | 259k |

| Sep-28 | Caixin China PMI Mfg | 51.5 | -- | 51.6 |

| Sep-29 | Eurozone CPI Core YoY | 1.2% | -- | 1.2% |

Strengths

- Typical of FOMC meeting weeks, we tend to see the precious metals take a hit. The best performing precious metal for the week was palladium, off 0.43 percent on little market moving news. Ford announced that it will add more downtime to five North American automobile plants due to a decrease in demand as inventories rise on dealer lots.

- The gold price could soon recover, says Jason Schenker, president and founder of Prestige Economics, the reason being that the Federal Reserve might raise rates less rapidly because of low U.S. inflation. “The fact that the Fed members lowered their forecast for their own future Fed funds rate indicates that the Fed may again kind of undershoot what they’re predicting they’re going to do for rates,” Schenker told Bloomberg. This could end up being neutral to bearish for the dollar, which would help support the gold price.

- Gold has begun to climb back toward $1,300 an ounce on safe-haven demand now that tensions between Washington and Pyongyang are steeply escalating. Following new U.S. sanctions against North Korea, the rogue Asian country’s leader Kim Jong-un threatened to detonate a hydrogen bomb in the middle of the Pacific Ocean. With the back-and-forth rhetoric intensifying, investors’ interest in safe havens, gold included, has been renewed.

Weaknesses

- The worst performing precious metal for the week was platinum, off 3.77 percent. Platinum prices has been out of favor for the last couple of years, recently prompting Impala Platinum, the world’s second largest producer, to propose some job cuts in South Africa that could lead to supply disruptions if labor is not on the same page. Earlier this week, gold dropped below $1,300 an ounce as risks receded of another hurricane striking the mainland U.S. and as major stock market averages continued to hit record highs on a near-daily basis. In addition, a diplomatic resolution to the nuclear standoff with North Korea appeared likely, with Secretary of State Rex Tillerson saying the U.S. is seeking a peaceful conclusion.

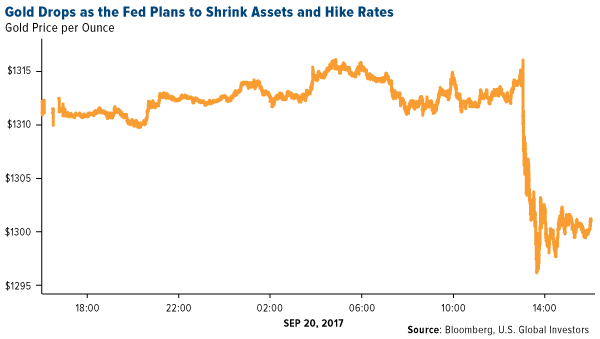

- The gold price responded negatively to Fed officials’ announcement that the central bank would begin unwinding its $4.5 trillion balance sheet as soon as October and also signaled additional rate hikes in 2018 following a December hike. Speaking with Bloomberg, RJO Futures’ Bob Haberkorn said that “the unwinding, coupled with the hawkish tone for December and the three hikes next year, could weigh on gold for the time being.”

- The world’s 20 leading gold producers’ share of metal output is expected to fall to its lowest level in a decade in 2019, according to Bloomberg industry analyst Eily Ong. The mining group’s share of world output fell from 47 percent in 2010 to 39 percent in 2016, and could fall even further by 2019. “As gold producers’ focus shifts from volume to profitable ounces, their existing gold mines’ life expectancies have also continued to declined,” Ong writes.

Opportunities

- Thursday and Friday of last week, Klondex Mines hosted a visit to its operations in Nevada to update the market on Hollister, Fire Creek, and Midas. We attended the site visits. Klondex is in a unique situation, having three, high-grade mines filling one centrally located mill at the Midas site. Overall, we would say investors and analysts came back with a favorable outlook. The share price outperformed the major gold equity ETF’s by over 550 basis points this week as several more positively toned analyst reports made the rounds. What we also think is noteworthy, was the quality of new people that have been attracted to Klondex, as operations have expanded, and the buy-in to the values of Klondex’s culture of safety at its operations. Prior to the trip, Klondex Mines completed the donation of the Rock Creek Lands to the Western Shoshone. For thousands of years, the Rock Creek Lands, about 20 miles northeast of Battle Mountain, Nevada, were used by the Western Shoshone. This was a goal of management and the board of Klondex to repair community relations with the Native Americans in the area which the previous owner of Hollister had ignored. Consequently, Klondex received drilling permits to now drill from the surface at Hollister to expand the exploration potential of the land package more cost effectively.

- Wesdome Gold Mines announced management changes driven by the CEO, Duncan Middlemiss, with full support of the board. The current CFO, COO and VP of Corporate Development & Exploration were all replaced immediately, which completes a realignment of staffing started by the addition of Chairman Charles Page to the board a little over a year-and-a-half ago. We see Wesdome Mines, with its Kiena Deeps exploration target, becoming more catalyst rich heading into the fourth quarter.

- With two of the bigger gold mining conferences for the year being held this week and next, there has been a swath of news releases distributed. Barsele reported a drill hole that intersected 19.75 meters grading 5.07 g/t gold, indicating continuity along a 100-meter gap between two lobes of the deposit. Jaguar Mining rose in excess of 25 percent on drill results that showed down plunge continuity of the principal ore body contained within the Banded Iron Formation. Both Golden Star and Red Pine Exploration reported double-digit grades from their respective orebodies that should lead to resource additions. In addition, Roxgold increased its production guidance for the year from 105,000-115,000ounces, up to 115,000-125,000 ounces.

Threats

- According to U.S. Trade Representative Robert Lighthizer, President Donald Trump’s chief trade negotiator, China poses an “unprecedented” threat to world trade, highlighting the country’s massive subsidies to “create national champions” and “distort markets.” Because current global rules are too inadequate to address the problem, Lighthizer adds, the president should unilaterally impose tariffs on China and any other country that practices “unfair” trade policies. Doing so, it should be noted, could lead to a U.S. trade war with China, the second-largest economy in the world, causing dramatic price swings in commodities and other raw materials.

- B&N Bank, a top-five closely held lender in Russia, has asked the country’s central bank for a bailout, reports Bloomberg, making it the second nationalization in less than a month. This highlights the complications accompanying the Bank of Russia’s efforts to clean up the financial sector after the dual economic shocks of a collapse in oil prices and international sanctions in 2014, the article continues. “The story of Otkritie, and now B&N, seriously raises questions about the actual state of private banks,” Dmitry Polevoy, chief economist for Russia at ING Groep NV in Moscow said.

- With the debt-cap suspension expiring on December 8, Bloomberg reports that there is a growing sense among investors and analysts that the Treasury will have to “slow or hold off on the inevitable.” It is unknown how the Treasury will respond to the Federal Reserve’s tapering. “The mix of maturities it decides on has far-reaching implications for the world’s biggest bond market, with the potential to alter the shape of the yield curve for years to come,” the article reads.

September 18, 2017The Blockchain Could Potentially Be as Disruptive as Amazon Was in the 1990s |

September 13, 2017Natural Disasters Have Not Caused a Single Muni Default: Moody’s |

September 11, 2017Gold and Bitcoin Surge on North Korea Fears |

Strengths

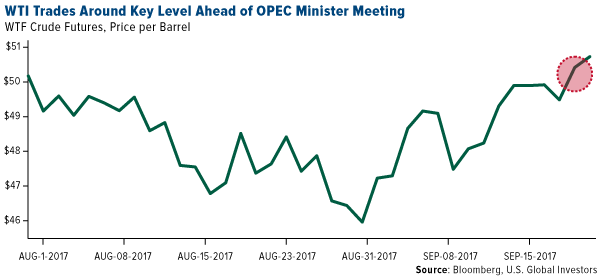

- Crude oil was the best performing major commodity this week rising 2.1 percent. Oil prices rallied as investors awaited clues from a meeting of OPEC oil producers that could extend production cuts. Ministers from the Organization of the Petroleum Exporting Countries, Russia and other producers meet in Vienna on Friday and are due to consider extending output cuts that began in January.

- The best performing sector this week was the S&P 1500 Oil & Gas Explorers and Developers Index. The index of major producers rose 4.4 percent on the back of rising crude oil prices, which broke above key technical resistance levels.

- Anadarko Petroleum Corp., a major Texas-based oil producer, was the best performing stock in the broader resource market this week. The stock rallied 12.1 percent after the company announced a $2.5 billion share buyback program.

Weaknesses

- Iron ore was the worst performing major commodity this week dropping 11.9 percent. The steel-making raw material dropped after a barrage of bad news, with concerns about rising global supply, questions about the outlook for demand in China, and a warning from Australia’s central bank that China may be nearing peak steel production.

- The worst performing sector this week was the TSX Gold Index. The index fell 3.2 percent as gold posted a second consecutive weekly drop on news that the Federal Reserve still expects to raise rates one more time in 2017, and as many as three times in 2018.

- The worst performing stock for the week was VALE SA. The Brazilian diversified miner dropped 6.4 percent in response to weaker iron ore prices.

Opportunities

- Germany’s ZEW economic sentiment index rose 7 points in September to 17. A rise in bank lending and increasing investment activities by both the government and private firms are likely reasons for the financial market experts’ significantly more positive outlook compared to that of last month. The release suggests the strong growth momentum in Europe may continue, and the high growth in EU oil and energy demand – which has helped rebalance the global oil market – may continue for the remainder of the year.

- Global nitrogen price benchmarks have risen almost 40 percent since the second quarter as the nitrogen distribution channel prepares for the seasonal increase in farm applications. As coal prices in China continue to climb, they will add upward momentum to nitrogen prices, as suggested by a recent Bloomberg report.

- Aluminum prices hit their highest in nearly six years on a report that Aluminum Corp of China, known as Chinalco, has started cutting production in the Henan province almost two months before official winter restrictions kick in. The surprising reduction in supply may continue to drive aluminum prices higher for the remainder of 2017.

Threats

- China’s sovereign credit rating was downgraded from AA- to A+ by S&P, the second international rating agency to do so this year after Moody’s lowered its sovereign rating in May. The agency cited concerns “that credit growth in the next two to three years will remain at levels that will increase financial risks gradually.” The rating downgrade may reduce the availability of capital for Chinese corporations, which could result in weaker demand for imports and commodities.

- The Shanghai Metals Market’s (SMM) international division estimates that environmental policy-related closures could reduce steel output by up to 30 million tons this year in China. As a result, SMM expects iron ore consumption to drop by 50 million tons, a number that may create a large supply demand imbalance in the already well-supplied iron ore market.

- Ford Motor Co. has announced it will curtail production at five plants in North America as U.S. sales slow. Ford said it would temporarily idle production to cope with slowing vehicle sales and rising industry inventories. The news has potential negative implications for steel, aluminum and other raw materials used in vehicle production.

Strengths

- The Philippines Stock Exchange PSEi Index returned 1.23 percent for the week, putting in a strong showing within the region. The peso also strengthened for the week.

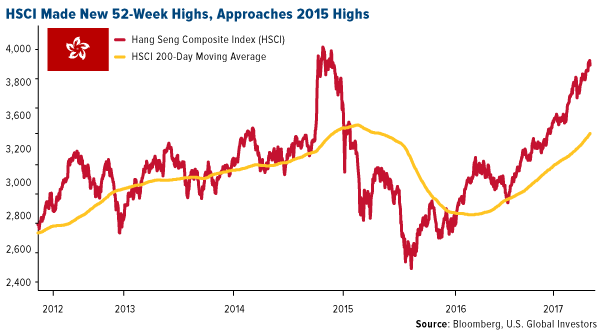

- Also notable is Hong Kong’s Hang Seng Index, which made new 52-week highs this week and which has continued to creep closer to its five-year highs, seen below:

- Taiwan’s year-over-year industrial production orders came in better than expected for the August period, rising 3.25 percent, ahead of analysts’ anticipation of a 1.85 percent gain and up from the prior showing of 2.38 percent.

Weaknesses

- The Taiwan Stock Exchange Weighted Index fell 1.22 percent for the week, with most of the decline coming on Friday.

- Standard & Poor’s lowered China’s sovereign credit grade to A+ from AA- this week. The ratings agency also downgraded Hong Kong to AA+ from AAA this week, citing the “strong institutional and political linkages” to mainland China.

- New home prices in China rose in only 46 out of 70 cities, whereas last month they rose in some 56. On the bright side, the various (and apparently effective) measures the Chinese government have taken to cool house price appreciation may mean that soon, given the relative success, such measures may be loosened slightly once again.

Opportunities

- Several important stories came out this week related to the electric vehicle market in China. The country is said to be studying a relaxation on the rules for foreign electric vehicle makers, according to press reports, with a possible allowance for wholly owned foreign producers able to set up shop in free trade zones. The news comes even as China recently announced that government officials are considering setting a deadline after which sales of internal combustion vehicles will be prohibited. (Automaker BYD has since come out and predicted a 2030 deadline.)

- Tech giant Tencent announced a couple of interesting strategic agreements this week. First, Tencent announced a cooperation agreement with Guangzhou Auto on “internet service for vehicles, smart-driving technology, big data and marketing,” Bloomberg reports. Second, Tencent entered into an agreement with China International Capital Corp., or CICC, on precision marketing and big data analysis. Tencent also subscribed to an issuance of new H-shares in CICC.

- Reports suggest that the People’s Bank of China (PBOC) is drafting possible reforms for a broader opening of the Chinese financial markets, including the possibility of foreign institutions maintaining control over local financial JVs and raising the foreign ownership threshold for Chinese banks.

Threats

- North Korea remains near the forefront of investor risks, with “Rocket Man” rhetoric and threats of H-bombs spicing up the press this week.

- The concerns of both Moody’s (earlier this year) and now S&P on China’s debt—while not necessarily immediate or alarming—demonstrate continued concern about the situation under the hood. Clearly, the yuan has enjoyed relative stability for the last several months and outflow concerns have moderated, even as the government has pushed deleveraging and domestic investment, but the downgrade this week from S&P ought to serve as a bit of a reminder or refresher on the overall situation.

- Central banking policies worldwide may continue to have outsized or unknown effects on markets.

Strengths

- Russia was the best relative performing country this week, losing 10 basis points. Russian stocks started to outperform Turkish stocks since the end of August, and investors are switching from Turkey to Russia, according to Bloomberg. Turkish equities gained 33 percent year-to-date, while Russian stocks lost 8 percent.

- The Polish zloty was the best performing currency this week, gaining 20 basis points against the U.S. dollar. Economic data released this week in Poland points to the strength in the economy and supports the country’s local currency. Average gross wages continue to grow, industrial output and retail sales are improving, and the unemployment rate is at record low level.

- Energy was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing country this week, losing 3.3 percent. A weakening of the Turkish lira and rising political risks sent Turkish stocks lower extending their decline to a third week.

- The Turkish lira was the worst performing currency this week, losing 1.6 percent against the U.S. dollar. A hawkish tone from the Federal Reserve and tensions around the independence referendum in Kurdistan pushed the lira lower.

- Real estate was the worst performing sector among eastern European markets this week.

Opportunities

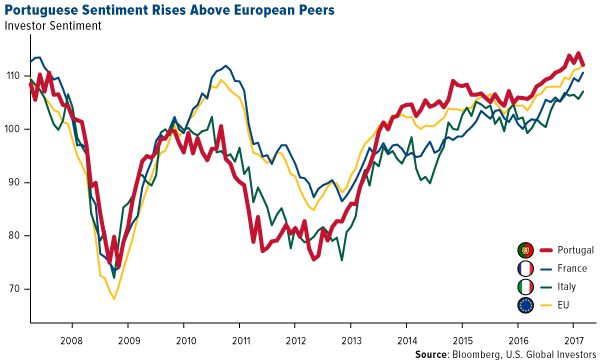

- Standards and Poor’s upgraded Portuguese bonds to investment grade, a rating that the country lost during the euro crisis in 2012. S&P said the bond upgrade reflected a growing economy, a reduced budget deficit and the receded risk of market deterioration in external financing conditions. Portugal’s GDP expanded 2.9 percent on the year in the second quarter. Investor confidence has been the strongest among the biggest European economies, with a slight correction recently. After the credit rating agency announced the upgrade, yields fell to the lowest since late 2015, and bond prices rallied.

- The euro area economy may have grown at the fastest pace in more than two years in the third quarter after an upturn in September .The composite PMI jumped to a four-month high of 56.7 from 55.7 in August. Germany’s composite PMI is at the highest in more than six years. France’s PMI also beat estimates.

- The German election takes place this Sunday, and Merkel’s Christian Democrats (CDU) party is well ahead in polls, but will most likely fall short of a majority. Six parties are polling well above the 5 percent national threshold required to enter the parliament. We should know the winner by Sunday, although it will be several more weeks until a coalition government is officially agreed on.

Threats

- Kurdistan is planning to hold an independence referendum on September 25, which the Kurds consider a culmination of decades of struggle for a state of their own, but that Iraq calls a violation of its constitution. Washington remains friendly with the Kurds, who are helping to fight the Islamic State, but is concerned about the independence bid leading to the breakup of Iraq or more political tension in Turkey, Reuters reports.

- B&N Bank, one of the top Russian banks, asked the central bank for help. B&N is under pressure from tighter regulations that the central bank has been introducing slowly, along with a high level of bad debt. At the same time, falling rates in Russia are putting pressure on banks’ margins, a major source of profit for Russian banks. B&N Bank is the second bank asking for a bailout within a month.

- Only a quarter of Russians (26 percent) keep their savings in banks, according to state-owned Russian Public Opinion Research Centre. That is slightly down from 2013 when 28 percent of Russians used banks to hold their savings. The fear of losing savings due to a bank crisis has fallen to 29 percent from 50 percent in 2013. Most of the respondents (73 percent) reported that they have no savings at all, up from 71 percent.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits