What a week it’s been.

First and foremost, I’d like to acknowledge the horrific mass shooting that occurred in Las Vegas, the deadliest in modern American history. On behalf of everyone at U.S. Global Investors, I extend my sincerest and most heartfelt condolences to the victims and their families.

The memory of the shooting was still fresh in people’s minds during Tuesday’s Hollywood premiere of Blade Runner 2049, which nixed the usual red carpet and other glitz in light of the tragedy. Before the film, producers shared poignant words, saying that in times such as these, the arts are crucial now more than ever.

I had the distinct privilege to attend the premiere. My good friend Frank Giustra, whose production company Thunderbird Entertainment owns a stake in the Blade Runner franchise, was kind enough to invite me along. Despite the somber mood, I thought the film was spectacular. Even if you’re not a fan of the original 1982 film, it’s still worth experiencing in theaters. Hans Zimmer and Benjamin Wallfisch’s synth-heavy score is especially haunting.

CNET recently published an interesting piece examining the accuracy of future tech as depicted in the original Blade Runner, from androids to flying cars to off-world travel read the article here.

Still in the Early Innings of Cryptocurrencies

Speaking of the future, I spoke on the topic of the blockchain this week at the Subscriber Investment Summit in Vancouver. My presentation focused on the future of mining—not just of gold and precious metals but also cryptocurrencies.

Believe it or not, there are upwards of 2,100 digital currencies being traded in the world right now, with a combined market cap of nearly $150 billion, according to Coinranking.com.

Obviously not all of these cryptos will survive. We’re still in the early innings. Last month I compared this exciting new digital world to the earliest days of the dotcom era, and just as there were winners and losers then, so too will there be winners and losers today. Although bitcoin and Ethereum appear to be the frontrunners right now, recall that only 20 years ago AOL and Yahoo! were poised to dominate the internet. How times have changed!

It will be interesting to see which coins emerge as the “Amazon” and “Google” of cryptocurrencies.

For now, Ethereum has some huge backers. The Enterprise Ethereum Alliance (EEA), according to its website, seeks to “learn from and build upon the only smart contract supporting blockchain currently running in real-world production—Ethereum.” The EEA includes several big-name financial and tech firms such as Credit Suisse, Intel, Microsoft and JPMorgan Chase, whose own CEO, Jamie Dimon, knocked cryptos a couple of weeks ago.

To learn more about the blockchain and cryptocurrencies, watch this engaging two-minute video.

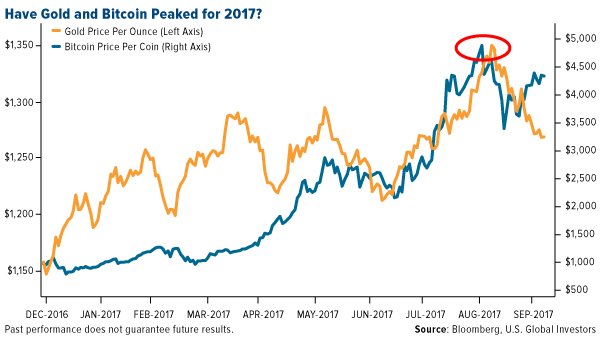

Will Bitcoin Replace Gold?

Lately I’ve been seeing more and more headlines asking whether cryptos are “killing” gold. Would the gold price be higher today if massive amounts of money weren’t flowing into bitcoin? Both assets, after all, are sometimes favored as safe havens. They’re decentralized and accepted all over the world, 24 hours a day. Transactions are anonymous. Supply is limited.

click to enlarge

But I don’t think for a second that cryptocurrencies will ever replace gold, for a number of reasons. For one, cryptos are strictly forms of currency, whereas gold has many other time-tested applications, from jewelry to dentistry to electronics.

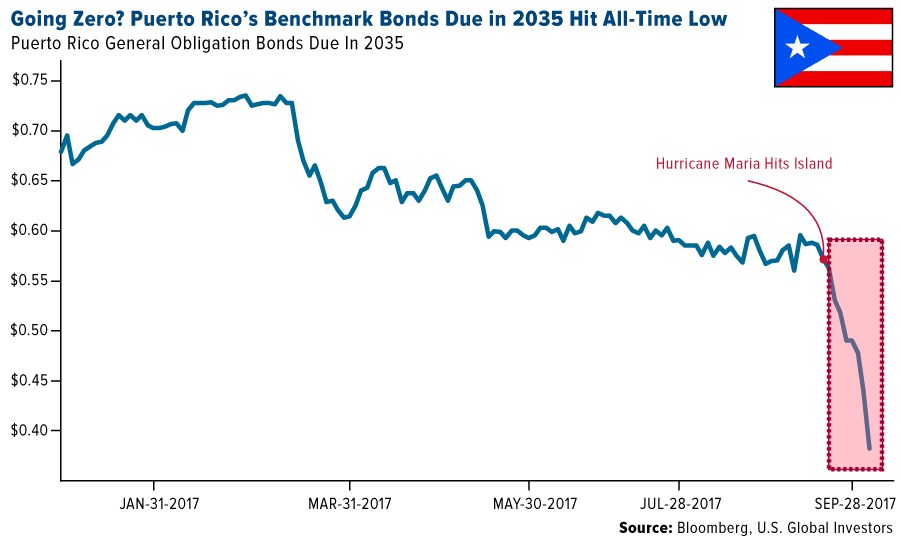

Unlike cryptos, gold doesn’t require electricity to trade. This makes it especially useful in situations such as hurricane-ravished Puerto Rico, where 95 percent of people are reportedly still without power. Right now the island’s economy is cash-only. If you have gold jewelry or coins, they can be converted into cash—all without electricity or WiFi.

Finally, gold remains one of the most liquid assets, traded daily in well-established exchanges all around the globe. Every day, some £13.8 billion, or $18 billion, worth of physical gold are traded in London alone, according to the London Bullion Market Association (LBMA). The cryptocurrency market, although expanding rapidly, is not quite there yet.

I will admit, though, that bitcoin is energizing some investors, especially millennials, in ways that gold might have a hard time doing. The proof is all over the internet. You can find a number of TED Talks on bitcoin, cryptocurrencies and the blockchain, but to my knowledge, none is available on gold investing. YouTube is likewise bursting at the seams with videos on cryptos.

Bitcoin is up 350 percent for the year, Ethereum an unbelievable 3,600 percent. Gold, meanwhile, is up around 10 percent. Producers, as measured by the NYSE Arca Gold Miners Index, have gained 11.5 percent in 2017, 23 percent since its 52-week low in December 2016.

Look Past the Negativity to Find the Good News

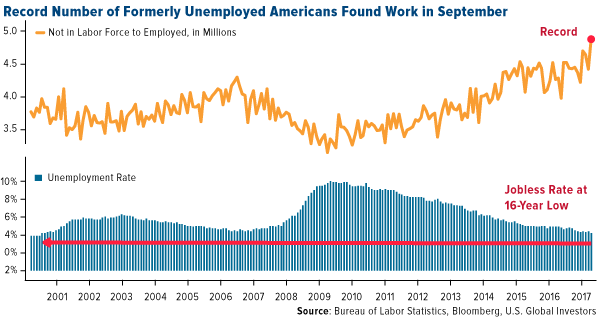

The news is filled with negative headlines, and sometimes it’s challenging to stay positive. Take today’s jobs report. It showed that the U.S. lost 33,000 jobs in September, the first month in seven years that this happened. A weak report was expected because of Hurricane Irma, but no one could have guessed the losses would be this deep.

The jobs report wasn’t all bad news, however. For one, the decline is very likely temporary. Beyond that, a record 4.88 million Americans who were previously sitting out of the labor force found work last month. This helped the unemployment rate fall to 4.2 percent, a 16-year low.

click to enlarge

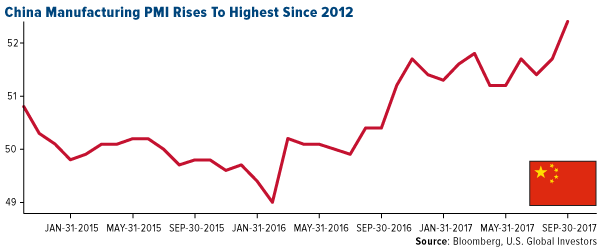

There’s more that supports a stronger U.S. economy. As I shared with you this week, the Manufacturing ISM Purchasing Managers’ Index (PMI) rose to a 13-year high in September, indicating rapid expansion in the manufacturing industry. Factory orders were up during the month. Auto sales were up. Oil has stayed in the relatively low $50-a-barrel range, which is good for transportation and industrials, especially airlines. Small-cap stocks, as measured by the Russell 2000 Index, continue to climb above their 50-day and 200-day moving averages as excitement over tax reform intensifies.

These are among the reasons why I remain bullish.

One final note: Speaking on tax reform, Warren Buffett told CNBC this week that he’s waiting to sell assets until he knows the plan will go through. “I would feel kind of silly if I realized $1 billion worth of gains and paid $350 million in tax on it if I just waited a few months and would have paid $250 million,” he said.

It’s a fair comment, and I imagine other like-minded, forward-thinking investors, buyers and sellers will also wait to make huge transactions if they can help it. Tax reform isn’t a done deal, but I think it has a much better chance of being signed into law than a health care overhaul.

Upcoming Event

Later this month I’ll be in Barcelona attending and speaking at the 18th annual LBMA/LPPM Precious Metals Conference, where I’ll be speaking on quant investing. If you’re in the area between October 15 and 17, I’d be thrilled to see you! You can register here.

Gold Market

This week spot gold closed at $1,275.24, down $4.91 per ounce, or 0.38 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.34 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index came in up 0.91 percent. The U.S. Trade-Weighted Dollar finished the week higher by 0.77 percent.

| Date |

Event |

Survey |

Actual |

Prior |

| Sep-29 |

Caixin China PMI Mfg |

51.5 |

51.0 |

51.6 |

| Oct-2 |

ISM Manufacturing |

58.1 |

60.8 |

58.8 |

| Oct-4 |

ADP Employment Change |

135k |

135k |

228k |

| Oct-5 |

Initial Jobless Claims |

265k |

260k |

272k |

| Oct-5 |

Durable Goods Orders |

1.7% |

2.0% |

1.7% |

| Oct-6 |

Change in Nonfarm payrolls |

80k |

-33k |

169k |

| Oct-12 |

PPI Final Demand YoY |

51.5 |

-- |

51.6 |

| Oct-12 |

Initial Jobless Claims |

252k |

-- |

260k |

| Oct-13 |

Germany CPI YoY |

1.8% |

-- |

1..8% |

| Oct-13 |

CPI YoY |

2.3% |

-- |

1.9% |

Strengths

- The best performing precious metal for the week was silver up 1.07 percent. Precious metals rallied to mid-day highs on Friday as it was rumored North Korea will test a missile this weekend that is capable of reaching the U.S. West Coast. Gold traders and analysts surveyed by Bloomberg on Thursday were equally split between bulls and bears this week, reports Bloomberg, after saying gold prices will go down three weeks in a row. According to data released by the Perth Mint this week, gold coin and minted bar sales increased to 46,415 ounces in September. This is up from sales of 23,130 ounces in August.

- In the week ended September 28, inflows into U.S.-listed commodity ETFs totaled $644 million, reports Bloomberg, a 27-percent expansion. Precious-metals funds had $782 million of gains, the article continues, compared with $589 million the week prior.

- Since Vladimir Putin went on a geopolitical offensive in the Ukraine in 2014, gold had its first annual gain in four years in 2016, writes Bloomberg, and is now on track for another gain in 2017. In addition, the Bank of Russia has more than doubled the pace of gold purchases, accounting for 38 percent of all gold purchased by central banks in the second quarter alone. According to the World Gold Council, this brings the share of bullion in Russia’s international reserves to the highest of Putin’s 17 years in power, the article continues.

Weaknesses

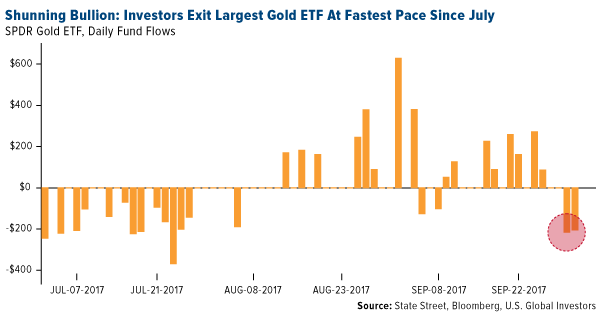

- The worst performing precious metal for the week was palladium down 1.46 percent. Palladium prices overtook platinum prices last week for the first time in 16 years, perhaps triggering some profit taking as the metal traded more than $25 lower to start the week. On Monday, investors pulled the most money in more than two months out of the SPDR Gold Shares ETF, reports Bloomberg, meaning that perhaps they are “growing immune to the war of words between Donald Trump and Kim Jong Un.” Similarly, coin sales are shrinking in the U.S., down by two-thirds in the first nine months of the year from the same period in 2016, reports the U.S. Mint. Amid increasing odds that the Federal Reserve will hike interest rates by year-end, bullion has slumped more than 6 percent since trading at the highest in a year in early September, the article continues.

click to enlarge

- Bank of America only sees limited upside to gold into year-end. Michael Widmer, analyst with BofAML wrote in a report on October 2, “the Fed has recently reinforced intentions to normalize monetary policy and a rate hike in December is now increasingly priced in.” Brian Lan of Singapore-based GoldSilver Central adds that gold is also floundering on lack of support from Chinese markets during the week-long national holiday and dollar strength, reports Bloomberg.

- BullionValut’s Gold Investor Index, which measures the balance of client buyers against sellers, is climbing back from a 14-month low in September, as prices touched a one-year high prior to retreating. Increasing expectations of a rate hike have also affected gold open interest, a tally of outstanding futures contracts, which dropped to the lowest in more than five weeks, reports Bloomberg. Another movement in the gold market is seen in the ratio of Comex paper claims to physical gold, which continues to creep higher at 93:1 currently, versus the average of 50:1 year-to-date. According to Desjardins, Comex-registered (deliverable) gold is now down to 588,000 troy ounces – down 62 percent since the beginning of the year.

Opportunities

- Christopher Woods of CLSA, in a report titled “A Question of Contraction,” writes that the commencement of quantitative tightening (QT) represents the biggest risk to still presumably Wall Street correlated world stock markets. Woods says that gold remains “essential insurance” despite obvious risks posed by QT, and that the more the Fed tightens, the more likely it will trigger a renewed deflationary reality check. This could lead, again, to some form of unconventional monetary policy. It is the central banks’ (and the Fed’s) inability to exit from unconventional monetary policy, that the team at CLSA maintains its long-term bullish view on gold bullion. The ultimate price target remains at $4,200 an ounce, Woods continues.

- According to Barclays, one question that the group has been asked by investors recently is whether mining companies are under-capitalizing their businesses. According to the Report dated October 5, Barclays writes, “We believe under-capitalization is not substantial on balance. But conditions are ripe for further capex increases given low capex/sales and D&A versus history, balance sheets are now fixed, dividends have been reinstated and commodity prices continue to be strong.” However, Barclays notes that capex upside is limited “by a paucity of growth projects that can be accelerated.” Also note, that according to Bloomberg Intelligence, for the first time in five years, capital spending for the BI global senior gold valuation peers is projected to increase in 2017, based on past 12-month trends and 2018 estimates.

- In a report published on Tuesday, Metals Focus says that the macroeconomic backdrop remains positive for precious metals prices through to 2018, reports Bloomberg, along with expected weakening of the dollar. The firm stated that, “crucial to this view is that monetary policies are likely to remain accommodative.” Other news in the gold sector comes from a Paradigm Capital Report, outlining the group’s favorite explorers from the Beaver Creek Conference, specifically highlighting 12 companies. One positive sign was record attendance by corporate acquirers at the event, a sign that producers are hungrier. Paradigm Capital also notes the shortage of new discoveries, which makes the good ones all the more exceptional. The report goes on to explain that in the 1990-1999 decade, for every ounce produced globally, there was 1.4 ounces found in significant new greenfield projects. Then, from 2000 to 2009, the rate declined to 0.7 ounces per ounce produced. Since 2010, SNL estimates that only 0.3 ounces have been found. “Many of the ounces discovered, maybe one-third, are in inhospitable locations or are uneconomic, making the good ones all the more exceptional,” it reads.

Threats

- David Doyle of Macquarie Research says the group is more optimistic about 2018 and beyond. The group is lifting its estimates for U.S. real GDP growth for 2018 by 50 basis points, while also increasing its estimates for 2019 through 2021 by 30 to 40 basis points. Doyle writes that Macquarie sees two to three interest rate hikes in 2018, and one to two hikes in 2019. In another note from Macro Strategy Partners this week, it reports that Congressional Republicans approved a 2018 fiscal spending blueprint to help advance the eventual tax bill. And although the market took the news positively, Fed officials have warned despite the delivery of a short-term boost, it could also bring high inflation and much higher debt – lowering growth even further.

- If Western Australia moves forward with its proposed gold royalty rate hike, four of the biggest gold producers in Australia have warned they will likely close mines or direct investment dollars elsewhere, reports the Australian Financial Review. “If you get these royalty increases that wipe out all of your profits while you are trying to set up the long-term future of the mine you have to question, ‘do we really put that capital here or should we put it elsewhere’ and these are the sort of decisions that will get taken,” said Sandeep Biswas, chief executive of Newcrest Mining.

- Jason Schenker, president and founder of Prestige Economics, told Bloomberg Television in an interview Monday that gold is facing numerous bearish factors. He noted a stronger dollar, U.S. stocks at all-time highs and signs of weakness in China’s economy. Looking at the political landscape in the U.S., advisers and allies of President Trump are floating the idea of Secretary of State Rex Tillerson being replaced by CIA Director Mike Pompeo, reports Bloomberg. On October 4, Tillerson actually vowed to stay in position following reports that he was near resigning.

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 1.8 percent. Fitch raised the country’s growth forecast this year from 3.2 percent to 3.6 percent. In September, central banks cut deposit rates further below zero. Marton Nagy, deputy governor of the National Bank of Hungary, said that real negative interest rates could remain as is for seven to eight years offering a historical opportunity to businesses, household and the government to borrow at very low rates.

- The Czech koruna was the best relative performing currency this week, losing 35 basis points against the U.S. dollar. Policymakers are talking about hiking rates again at the next meeting. They increased the key rate to 0.25 percent from a record-low 0.05 percent on August 3.

- Material services was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 1.3 percent. Banks continue to trade lower on political uncertainty in Germany, and fears of another asset quality review remain.

- The Turkish lira was the worst performing currency this week, losing 1.4 percent against the U.S. dollar. According to Bloomberg, the dollar has historically been strong in the fourth quarter over the past six years. A stronger dollar will push emerging Europe currencies lower; especially the Turkish lira which is sensitive to dollar strength.

- Consumer staples was the worst performing sector among eastern European markets this week.

Opportunities

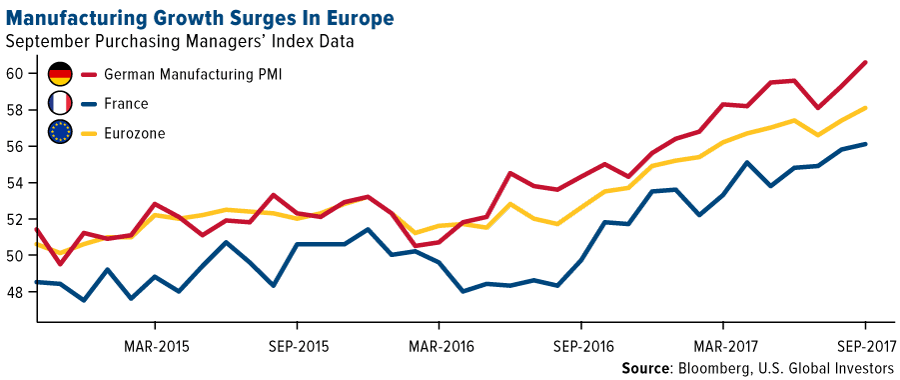

- September’s final manufacturing PMI for the eurozone was reported at 58.1, compared with 57.4 in August. France and Germany, two of the biggest Western Europe economies, reported higher PMIs. In central Eastern Europe, Poland, Hungary, the Czech Republic, Russia and Greece all saw improvement in their PMIs as well, while Turkish PMI declined to 53.5 (although remains above the 50 level). Anything above 50 indicates that the manufacturing economy is expanding, while a reading below 50 indicates a contraction.

click to enlarge

- The FTSE announced that Poland will be reclassified from the Advanced Emerging Markets to the Developed Markets universe, effective as of the semi-annual review in September 2018. Poland is the first Central and Eastern European market to join the FTSE’s Developed Markets universe. The upgrade may attract new investors to local equities.

- JPMorgan in its CEEMEA Equity Research, recommends overweighting Russia and Central Europe versus South Africa and Turkey. The group thinks that central Europe (CE3) stocks can re-accelerate. The stocks being led by financials, the raise in European bond yields, and ongoing strength in the core European economy all add to this reasoning. Rising oil prices are positive for Russia and negative for Turkey.

Threats

- The European Central Bank wants European banks to be fully covered against losses from non-performing loans. The new banking rule under discussion would require lenders to set aside 100 percent of the value of the unsecured loan within two years and it would give lenders seven years to put aside the full amount of a secured loan. The rule would only apply to loans declared non-performing after January 2018, not the existing 1 trillion euros of bad debts on banks books. However, it could hurt credit creation and boost capital needs of European banks.

- Catalonia, which generates more than one-fifth of Spain’s economy, held a referendum on independence last Sunday. The results show that about 90 percent of those voting backed independence. However, the turnout was low, at just over 40 percent. Under Spanish law, the referendum is considered illegal. Should Catalonia declare independence, Spain’s government may disband the region’s government, taking back control. Investors are relatively calm so far in reaction, but if the political situation worsens in Spain, European markets may respond negatively.

- Alexei Navalny, the anti-corruption Russian activist who would like to run for president against Putin in the next year’s election, has been arrested again and is serving a 20-day detention. Navalny planned a rally in St. Petersburg, the president’s hometown, for October 7. Authorities withheld permission for the gathering and Navalny refused to change his plans. According to his campaign manager Leonid Volkov, Navalny has spent every fifth day of his “presidential campaign” behind bars. His campaign manager was also sentenced to 20 days on Thursday, for tweeting calls for an illegal rally in Moscow.

© U.S. Global Investors

www.usfunds.com

© U.S. Global Investors

Read more commentaries by U.S. Global Investors